We say that in the formula for the limit of profitability of green power companies: ROE=IRR+(IRR-LR)*S, resource endowment determines the IRR of the project, and the asset-liability ratio determines the space S that green power companies can increase leverage. In this article, let’s take a look at the last variable that affects ROE: financing cost LR.

Because green power investment itself is a highly leveraged business, the difference in financing costs is crucial to the return on capital. It just so happened that we entered a low interest rate environment. For green power companies, it can be described as a golden period of development. If the general loan interest rate exceeded 6% in the early years, this business would not be possible.

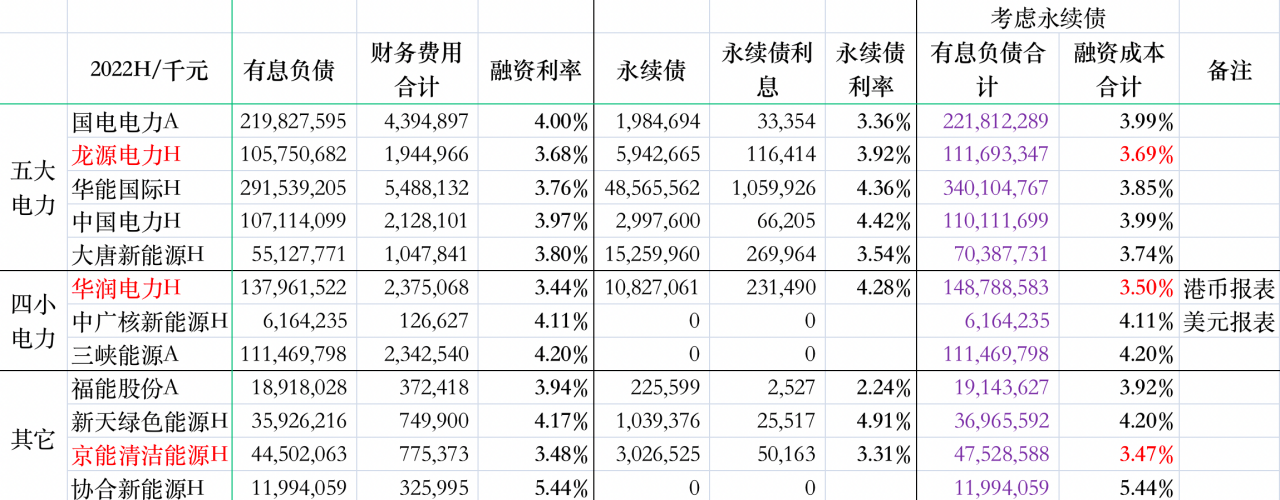

State-owned enterprises can obtain lower financing costs, and the living space of private enterprises in this field is squeezed. We have calculated the comprehensive financing costs of mainstream green power companies in the first half of the year, as shown in the figure below:

Statistics show that the comprehensive financing costs of the five major power central enterprises are all lower than 4%, and the financing costs of the four small power central enterprises and local power state-owned enterprises are not high, around 4%. The financing costs of China Resources Power and Jingneng Clean Energy are among the lowest, lower than those of the five major power companies.

However, on the whole, the differences in the financing costs of state-owned enterprises are not large. For banks, the endorsement of state-owned enterprises is enough to issue loans with lower interest rates. The low debt ratios of CR and BEH are more helpful for them to obtain low-interest loans. CGN New Energy’s excessive leverage, some of the loans come from brother companies, and the interest rate is slightly higher.

By comparison, it can be found that the financing cost of private enterprise Concord New Energy is 150 basis points higher than that of state-owned enterprises. This makes it more difficult for it to compete with state-owned enterprises. Don’t underestimate the 150 basis points. With a capital ratio of 20%, the difference in ROE is 6%. Under other conditions being equal, state-owned enterprises can achieve 15% ROE, while private enterprises only have 9%.

Concord is still a leader among private enterprises, and many other private enterprises have left this market in the last round of reshuffle. Fortunately, Concord has always insisted on high-return wind power projects, and the current financing gap of 150 basis points can still be tolerated. At present, the financing spread between the company and state-owned enterprises has a tendency to further narrow, and it is expected to narrow to less than 100 basis points. It may bring unexpected gains to investors.

(Finally, by the way, the financing costs disclosed in the management performance PPT and conference calls are often low, because there are many calibers for financing costs, and the management always tends to disclose the lowest one. For example, the interest on deposits is also Counting it in, or removing high-cost perpetual bonds, or ignoring the capitalized interest part, or using a larger time-point financing base as the denominator will lower the actual loan interest rate of the enterprise. Excerpts from our statistical data The actual interest expense in the report is replaced, the capitalized interest is restored, and the perpetual bond income is considered. The denominator adopts the arithmetic mean value at the beginning of the year and the middle of the year, and the results obtained are more meaningful.)

Series review:

Green Code 1: Amazing Models

Green Power Code 2: Illusion of Capital Return (EIRR)

Green Power Code 3: The business model of green power has shifted from “high leverage” to “cash cow”

Green Power Code 4: The ROE of a single project is also an illusion

Green Power Code 5: All-investment IRR has universal comparative significance

Web links

Green Power Code 6: Profitability: “Extreme Formula”

Green Power Code 7: Asset-liability ratio represents room for growth

Green Power Code 8: The special case where IRR is equal to ROE (green power model and hotel model)

There are 21 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/3727797950/237540214

This site is only for collection, and the copyright belongs to the original author.