Welcome to the WeChat subscription number of “Sina Technology”: techsina

Reporter Yan Liting Editor Gao Yulei

Source: Power Plant

In 2022, with the continuous rise of external pressure, Tesla’s life will not be easy.

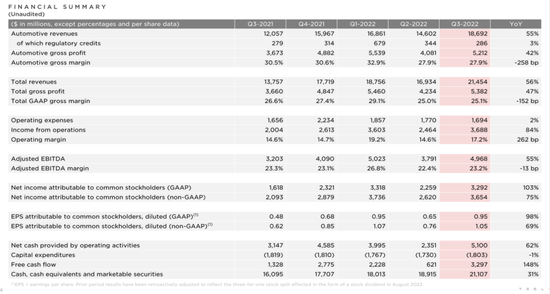

On October 20, Tesla disclosed its latest financial report. The data shows that in Q3 2022, Tesla’s total revenue was $21.45 billion, a year-on-year increase of 56%, and its adjusted net profit was $3.65 billion, a year-on-year increase of 75%. . Overall, this is still a good report card, but the market has higher requirements for top students. Compared with the revenue forecast of 22.09 billion US dollars, Tesla obviously did not meet the passing line.

It is worth noting that this is a rare performance of Tesla in the past year, and the gross profit level, which has always been praised, has continued to be sluggish. According to the financial report data, in Q3 2022, Tesla’s gross profit margin is only 25.1%, far lower than the market expectation of 26.6%. Among them, the gross profit margin of the automobile business is 27.9%. Auto gross margin fell below 30% for the second time.

Although Tesla has been reiterating its annual growth target of 50% at the performance analysis meeting, Musk has even thrown out a potential repurchase plan as high as $5 billion to $10 billion, but the special feature that is already in the downward channel Sla’s stock price still fell nearly 7 points after the market, and finally closed at $208.1, a drop of more than 6%. According to this calculation, Tesla’s overall market value has shrunk by more than 40% this year.

Behind the Q3 failure, the bicycle gross profit fell by more than 6%

From the perspective of revenue structure, the automotive business is still the key to Tesla’s underperformance.

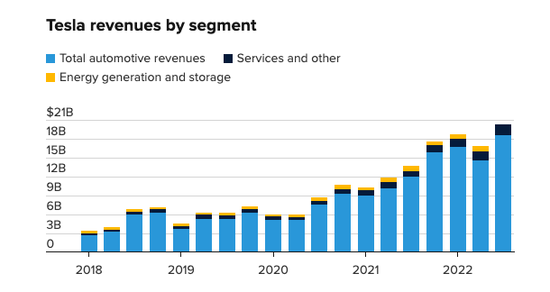

In Q3 2022, Tesla’s total revenue was $21.45 billion, a 56% increase from $13.76 billion in the same period last year. Among them, the automobile business income was 18.69 billion US dollars, the energy storage business income was 1.12 billion yuan, and the service income was 1.65 billion yuan. However, as a pillar of Tesla’s performance, affected by the decline in vehicle deliveries, the revenue growth rate of the automotive business was 55%, slightly lower than the growth rate of Tesla’s broader market.

In this regard, Tesla has given the market a shot of precaution before the release of the earnings report. On October 3, Tesla announced that the final delivery volume of Q3 was 343,800 vehicles, a year-on-year increase of 42% and a month-on-month increase of 35%, but far lower than the market expectation of 358,000 vehicles, and the capital market has also responded to this. In response, Tesla’s stock price plummeted 8.6% that day, and many investment banks, including Morgan Stanley, lowered their target prices after hearing the news.

Even so, the final financial report data still fell short of market expectations. On the one hand, in Q3 2022, Tesla’s revenue from the sale of carbon emission credits was $290 million, down 17% month-on-month and hitting a new low in revenue in a year. On the other hand, even if the impact of “carbon sales revenue” is ignored, in Q3 2022, Tesla’s corresponding single-vehicle sales revenue is $51,700, a decrease of 3.5 percentage points from the previous month.

At the same time, Tesla’s costs have continued to climb. The financial report shows that in Q2 2022, the cost of sales of Tesla vehicles will be US$13.1 billion, a year-on-year increase of 61%, while the overall cost of revenue will be US$16.07 billion, a year-on-year increase of 59%, both of which are higher than the revenue growth rate. In this regard, Tesla gave 4 reasons: rising raw material costs, drag on new factories, expansion of 4680 battery production, and fluctuations in the foreign exchange market.

Affected by this, Tesla’s profitability has also suffered. In Q3 2022, Tesla’s overall gross profit margin was 25.1%, down 1.5 percentage points year-on-year. Among them, the gross profit of the automobile business was 5.21 billion US dollars, and the corresponding automobile gross profit margin was 27.9%, a year-on-year decrease of 2.6 percentage points. According to the delivery volume of 343,800, Tesla’s single-vehicle gross profit was 15,000 US dollars, a month-on-month decrease of more than 6% %.

According to the financial report, in Q3 2022, foreign exchange fluctuations will drag down Tesla’s profits by US$250 million. In addition, the ramp-up speed of the two new factories in Berlin and Texas is not satisfactory, further dragging down the overall gross profit margin. In this regard, Tesla’s CFO Zachary Kirkhorn pointed out at the performance meeting, “If the impact of carbon sales is excluded, Tesla’s overall gross profit margin is about 30%.”

Judging by the results, Tesla’s banknote capabilities are still online. In Q3 2022, Tesla’s net profit was US$3.29 billion, doubling the year-on-year growth. The adjusted net profit was US$3.65 billion, a year-on-year increase of 75%. The corresponding EPS was US$1.05, which was higher than analysts’ expectations. $1.01. Of course, that’s largely thanks to Tesla’s control over overall operating expenses.

The data shows that in Q3 2022, Tesla’s total operating expenses will be $1.69 billion, a year-on-year increase of only 2%. Among them, research and development expenses will be $730 million, a year-on-year increase of 20%, and sales and management expenses will be $960 million, a year-on-year decrease. 3%, and the overall operating rate is less than 8%. However, this has failed to restore market confidence. Since the release of sales on October 3, Tesla has fallen by more than 16%.

Tesla’s hidden worries Why is the buyback difficult to solve?

Judging from the market reaction, the lower-than-expected performance is not the whole truth of Tesla’s stock price decline.

In fact, after Tesla announced its Q3 delivery data, Cowen & Co. analyst Jeffrey Osborne pointed out that the market suspects that the real reason for Tesla’s decline in deliveries is weaker market demand. On the one hand, according to officially disclosed data, in Q3 2022, Tesla’s total production is 365,000 vehicles, which is a gap of 20,000 units compared to the delivery volume. On the other hand, Tesla’s delivery cycle is also shortening.

According to the latest data from Tesla’s official website, the pickup cycle of the domestic Model 3 is about 4 to 8 weeks, the pickup cycle of the domestic Model Y long-life/high-performance version is 4 to 8 weeks, and the pickup cycle of the domestic Model Y rear-wheel drive version is about 4 to 8 weeks. The cycle is 1 to 4 weeks, and the overall pick-up cycle is within 2 months.

Regarding the drop in delivery volume, following the announcement on October 3, Tesla management further explained at this performance analysis meeting that, as a major production base outside North America, Tesla’s shipping from Shanghai to Europe has encountered difficulties. Huge challenges, and the main line logistics of direct transportation from the United States to the European market is also facing difficulties, “this is a point that Tesla did not expect, or did not expect to be so serious.”

Tesla’s predicament is not a lie, according to The Power Plant. With the continuous acceleration of the pace of domestic car companies going overseas, the export of automobiles by sea has long been difficult to obtain. Earlier, Wang Shouwen, an international trade negotiator and deputy minister of the Ministry of Commerce, publicly stated that due to the lack of ro-ro shipping capacity, the official is actively coordinating the transportation of automobiles through the China-Europe freight train.

At the same time, the cost of transporting cars has also gone up. According to data from Clarksons, a third-party agency, at the end of September, the daily rent of large ro-ro ships with 6,500 parking spaces had hit a new high of $55,000. To this end, BYD, which is frantically deploying overseas markets, has recently begun to build its own shipping fleet. As of now, BYD has ordered 8 ro-ro ships, each costing more than 600 million yuan.

In contrast, Tesla’s solution is more direct. Kirkhorn said at the performance meeting that in the next step, Tesla will change the status quo through closer deliveries. According to Tesla, although the climbing speed is lower than expected, the productivity of the two new factories has reached a new high in Q3. Among them, Tesla’s Berlin factory produced more than 2,000 Model Ys using 2170 batteries within a week.

“Tesla is moving towards a more stable delivery rhythm”, Musk is also continuously releasing positive signals, and claims that the market demand in Q4 is still very strong, and the Q4 delivery is expected to be quite good, which means that in 2022, “Tes Ra will have an epic ending”. However, CFO Kirkhorn said he expects Tesla’s full-year deliveries to grow by less than 50% due to an increase in backlogs in transit at the end of the year.

In this regard, Jesse Cohen, a senior analyst at Investing.com, also believes that Tesla is likely to miss its delivery target of 1.4 million vehicles this year. In addition to the production capacity challenges facing Tesla itself, weak demand caused by the downward pressure on the economy is another key point.

An unavoidable fact is that starting from September 16 this year, Tesla China has achieved a disguised price reduction of up to 8,000 yuan through insurance subsidies, but even so, Tesla China’s sales are still slowing down. According to the latest research report of Guosheng Securities, from October 3 to October 16, Tesla China has accumulated a total of 3,942 insurance vehicles, a year-on-year decrease of 84% and a month-on-month decrease of 89%.

This has further aroused investors’ concerns about the growth trend next year. Previously, Gary Black, co-founder of Future Fund Active ETF, also wrote a letter to Tesla’s board of directors, advising the latter to repurchase shares. , Musk responded that the repurchase is meaningful, and Tesla is going through the corresponding process. Once approved by the board, the repurchase amount will reach 5 billion to 10 billion US dollars.

In addition, the market’s expectations for Tesla’s price cuts are getting stronger. Recently, there have been rumors in the industry that Tesla’s next round of price cuts may reach 40,000 yuan, and Musk also revealed at the performance meeting that Tesla is developing cheaper electric vehicles. Will price really be the ultimate sales tool? In this regard, the market may have given the answer. As of press time, Tesla’s stock price plummeted by another 6% before the market.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2022-10-20/doc-imqqsmrp3227568.shtml

This site is for inclusion only, and the copyright belongs to the original author.