After Amazon’s 22Q3 earnings report, I completed the clearance in 3 transactions. From 2020 to clearance, almost 3 years. Part of the decision to trade was a gradual change in my perception of the company itself, but it was the recent determination to reduce leverage that drove the order. Here I only talk about the former.

From the perspective of stock prices, after benefiting from the sharp rise in the epidemic in 2020, it has not risen since September 2020. It was not until recent quarters with the expectation of interest rate hikes and economic recession that superimposed its own fundamental problems. .

Figure: Amazon stock price

Of course, since entering 2022, it is stronger than Microsoft and Apple, and the stock price trend is not very good, but it is still better relatively speaking.

Figure: Microsoft stock price

Looking back at Amazon in the past three years, it has gone through two stages:

1. In 2020, benefiting from the epidemic, Amazon’s shipping capacity is 100% full. At this stage, Amazon began to recruit a lot of people, and a lot of capital was invested in shipping capacity.

Mentioned in the 20Q3 conference call:

We had a lot of people in the last quarter and then we added another 100,000 people in October so far. 100,000 new employees in October

In terms of enhancing logistics capabilities, the management in 20Q4 gave a long-term view: ” Logistics investment will continue in 2021. 20 years of increased user purchase frequency will have long-term effects. 』 . Bezos started to mention retirement in 20Q4.

In the 21Q1 conference call, some investors began to worry that the company’s performance growth rate would begin to decline after the epidemic resumed, but the management denied this concern: “I don’t have a downside case yet”.

In the 21Q2 conference call, the growth in capacity was mentioned:

Over the past 18 months, our fulfillment network has nearly doubled in size. We have been discussing expanding the scope of same-day delivery in the US market since 2019. Same-day delivery for European markets is part of the Prime service. The trend of investment expansion will continue throughout the year, with a growing transport network supporting faster deliveries.

The expansion of capacity in 21Q3 has not yet seen its head:

we have grown our global headcount by 628,000 employees in the past 18 months and are recruiting for more, including more than 150,000 in the US to support Q4 seasonal demand. There will even be an additional 150,000 HC for seasonal demand

At this time, some investors began to care about the issue of oversupply of distribution services.

In 21Q4, investors started to care about future capex. Management also made a summary in this regard for 2020 and 2021:

Looking back at the investment ratio in the past few years, about 40% of the investment expenditure has flowed to infrastructure construction, such as Amazon Cloud Services (AWS), etc.; about 30% of the investment expenditure has flowed to the improvement of distribution capacity, (fulfillment capacity building warehouses — warehouse only, not fulfillment capacity building warehouses — warehouse only, not transportation) such as building new warehouses, improving transportation efficiency, etc.; about 25% of the investment expenditure flows to the improvement of transportation capacity, (transportation capacity) such as building and improving the transportation capacity of Amazon’s self-operated logistics (AMZL) in the world; in 2022, the general direction of expenditure will not change , the focus may change: investment in infrastructure will further increase, after all, global consumer demand is further strengthening, and we will cover more countries and regions; as for Amazon logistics centers, investment in this field in the past two years accounted for about 30%, the growth rate of investment in this area will gradually slow down. As for investment in transportation capacity, investment in this field will continue to rise in 2022 (that is, investment in warehousing will slow down, and investment in transportation needs to continue)

Second, in 2022, the previous large investment suddenly began to overcapacity. At the same time, it also began to face inflation.

22Q1:

Over the past two years, there has been significant cost expenditure to meet customer demand. During that time, Amazon doubled in size and nearly doubled its workforce to 1.6 million. Labor and distance are no longer bottlenecks. In the consumer business, however, Amazon will continue to face various cost pressures. We will split these into two parts, externally driven costs, mainly inflation; and internal controllable costs, mainly productivity and fixed costs.

In the second half of 2021, Amazon is in a labor-tight environment. (Following up with hiring, and furloughed staff returning to work, again with excess labor) In the last few weeks of the quarter, productivity improvements across the network can be noticed, and these cost headwinds are expected to ease in the second quarter. Our freight forwarding and transportation network is currently overcapacity.

In 22Q3, the macro environment is more complicated and difficult, such as the energy crisis introduced by the war; the foreign exchange problem caused by the US interest rate hike; the investment problem of small and medium enterprises caused by the economic recession.

The most volatile is the international business, which we believe is driven by the declining global macroeconomic environment. Judging from the current data, the situation in Europe is relatively bad, and there are many influencing factors, including the Russian-Ukrainian war, the energy price crisis, etc. The regional situation is more complicated.

AWS faces demand issues:

Unlike the 2020 period, in the short term, some companies’ own demand has declined, and everyone’s attitude towards spending has become more cautious.

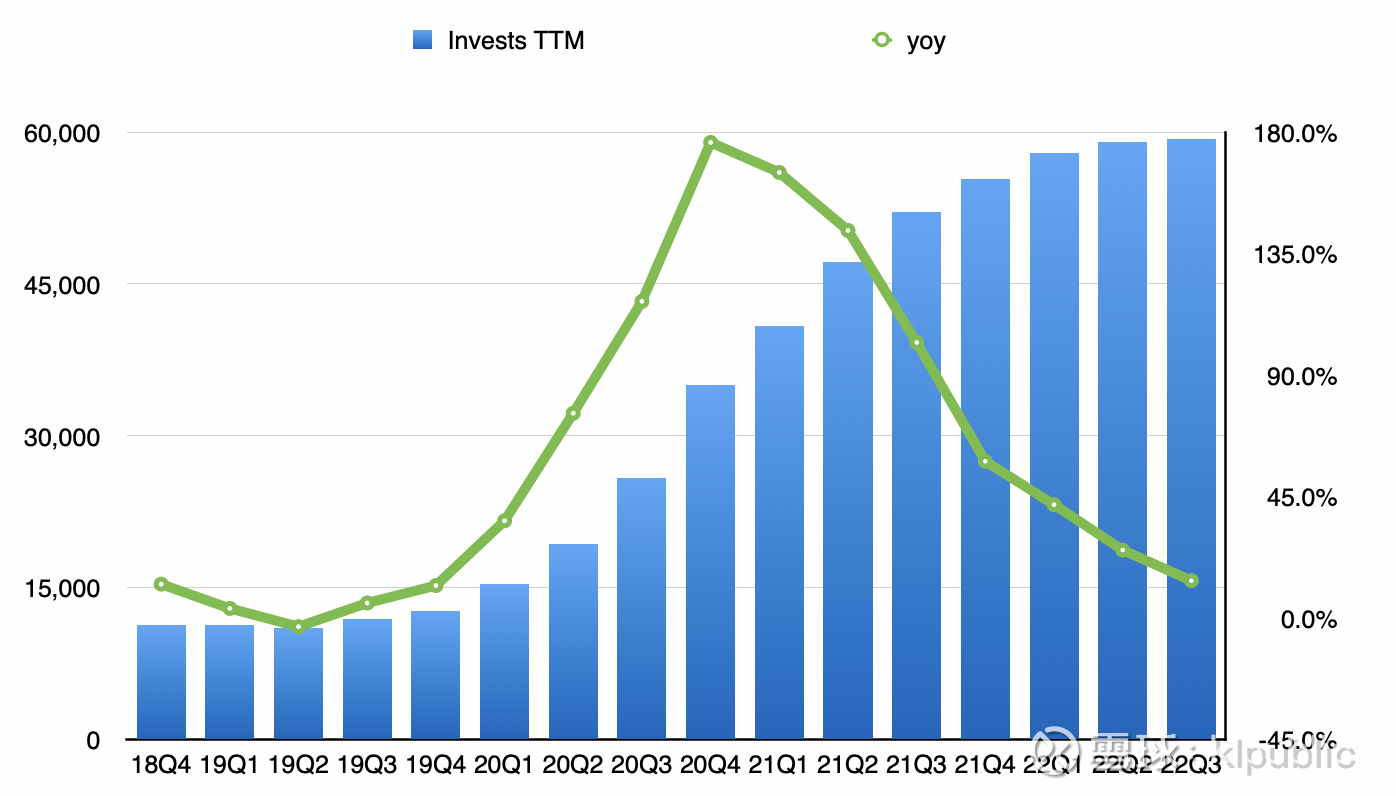

The changes in the past three years can also be seen from the investment cash flow TTM:

Chart: Investing Cash Flow TTM

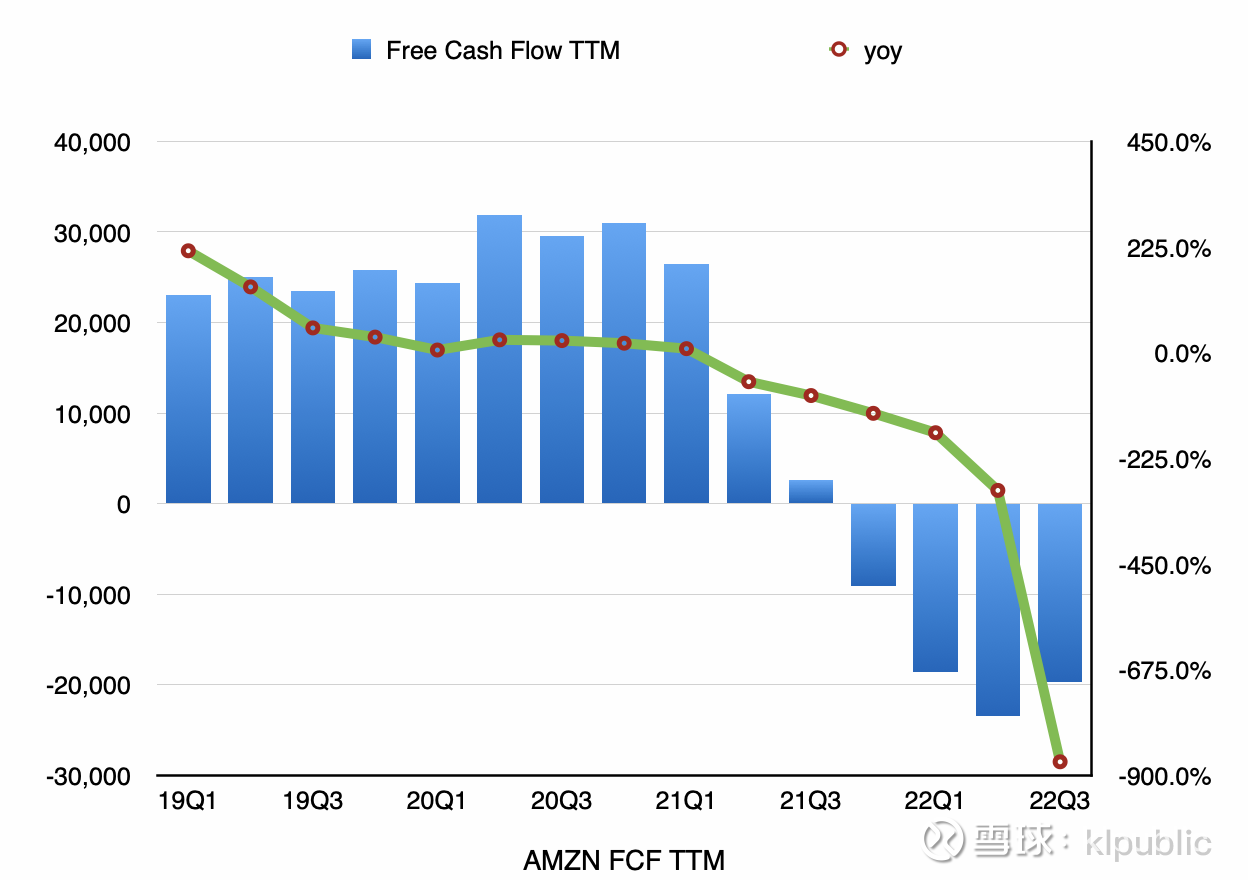

Free cash flow, which Amazon has always valued, has long been negative:

Chart: Free Cash Flow TTM

Some thoughts:

1. Bad business model: About 1-2 years ago I found out that retailers are a bad business model, with low single-digit profit margins that require companies to improve their operating turnover. Amazon’s business of excluding AWS is essentially a retailer.

2. Defects of asset-heavy companies: When faced with a large number of online shopping demands in 2020, Amazon’s shipping capacity cannot keep up, which limits revenue growth to a certain extent. Maybe Amazon originally planned to expand logistics (it began to expand the same-day delivery business in 2019), and when a large amount of demand came, it also took advantage of the situation. When the capacity increases, the demand may change again (such as offline opening, macro impact), then the capital will have surplus capacity. Staff wages and capital depreciation all add to the cost.

3. The growth that Amazon has always believed in has developed a lot of seemingly unrelated businesses, such as games and video content. Sometimes you can feel it a bit like Costco’s membership system, which endorses Prime members through e-commerce delivery services and various other services. But growth is not necessarily a good thing for shareholders. If the growth has good business synergies and can strengthen the main business, there is no problem. Instead, I think it should be returned to shareholders like Apple (it seems that investors have been asking Apple management how to view acquisitions in the last 2 quarters, and Apple is obviously more cautious in this regard). Finally, as I mentioned before, diversified growth, at Amazon’s level, is hard to imagine how difficult it is to manage.

$Amazon(AMZN)$ $JD(JD)$ $Apple(AAPL)$

This topic has 13 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9260251114/234639731

This site is for inclusion only, and the copyright belongs to the original author.