I. Introduction

In the previous article “Is the interest income on the bank’s impaired loans (provisions) included in the current operating income? “, I introduced in detail how the bank handles the interest income of impaired loans, and came to the conclusion that no amount of accrual or impairment will affect the bank’s operating income. Therefore, if a bank’s operating income growth rate has been very low, it will inevitably suppress the bank’s profit growth rate, which has nothing to do with whether the bank reserves more or less!

In the next two articles, I will discuss in detail the question that everyone is highly concerned about: Can a bank with high provisions release provisions to increase profits?

In this article, we will first study the changing process of loan impairment provisions, and discuss what “release provisions” are. In the next article, we will discuss how much provisions banks can release.

2. Five major changes in loan impairment provisions

First, let’s understand the complete life cycle of a provision, that is, what changes will be experienced in loan impairment provisions.

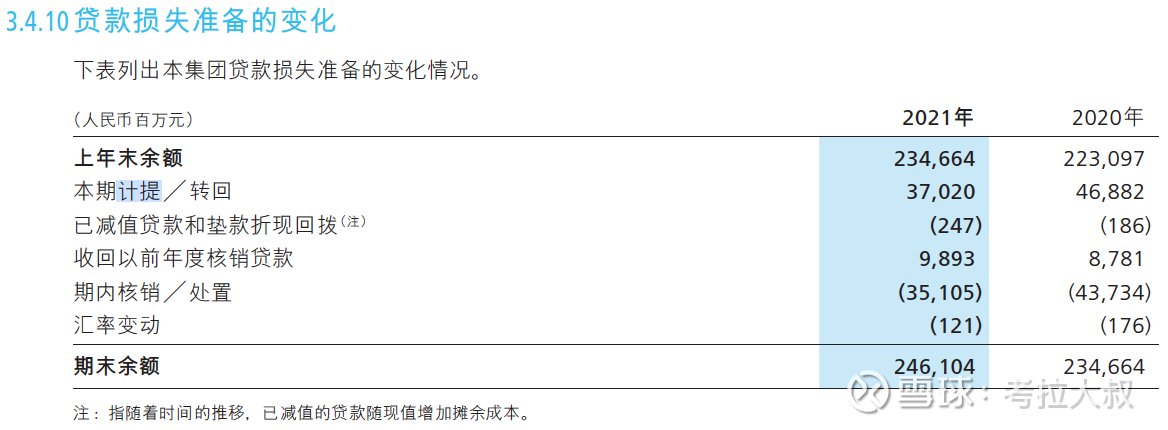

Figure 1 – Changes in Loan Loss Provisions in China Merchants Bank’s 2021 Annual Report

As shown in Figure 1, China Merchants Bank’s loan impairment reserves include “accrual in the current period”, “reversal in the current period”, “discounted write-back of impaired loans”, “recovery of loans written off in previous years”, Changes in “period write-offs and disposals”, “exchange rate changes”, etc.

in:

“Accrual/return” has a great relationship with the release of provisions to improve profits, so I will split it into two processes: “accrual” and “return”.

“Writing off/disposal”, disposal including the sale of non-performing assets, etc., are considered write-off for the sake of simplicity.

“Exchange rate changes”, which have nothing to do with the loan itself, are random and are ignored here.

In this way, changes in loan impairment provisions are divided into the following five processes:

1. Provision for impairment (when the expected loss of a loan increases, it will be transferred to the operation)

2. Reversing the provision for impairment (when the expected loss of a loan decreases, it will be transferred out)

3. Discounted value reversal (when the discounted value of an impaired loan increases, it will be transferred out)

4. Write-off provision for impairment (when writing off and disposing of a non-performing loan, it is transferred out)

5. Write back the impairment provision (when a written-off loan is recovered, it will be transferred to the operation)

Note: The increase in the discounted value of impaired loans refers to the interest income generated by the impaired loans. For a detailed explanation, please refer to “Is the interest income of the bank’s impaired loan (provision) included in the current operating income? 》

3. The changing process of loan impairment provision

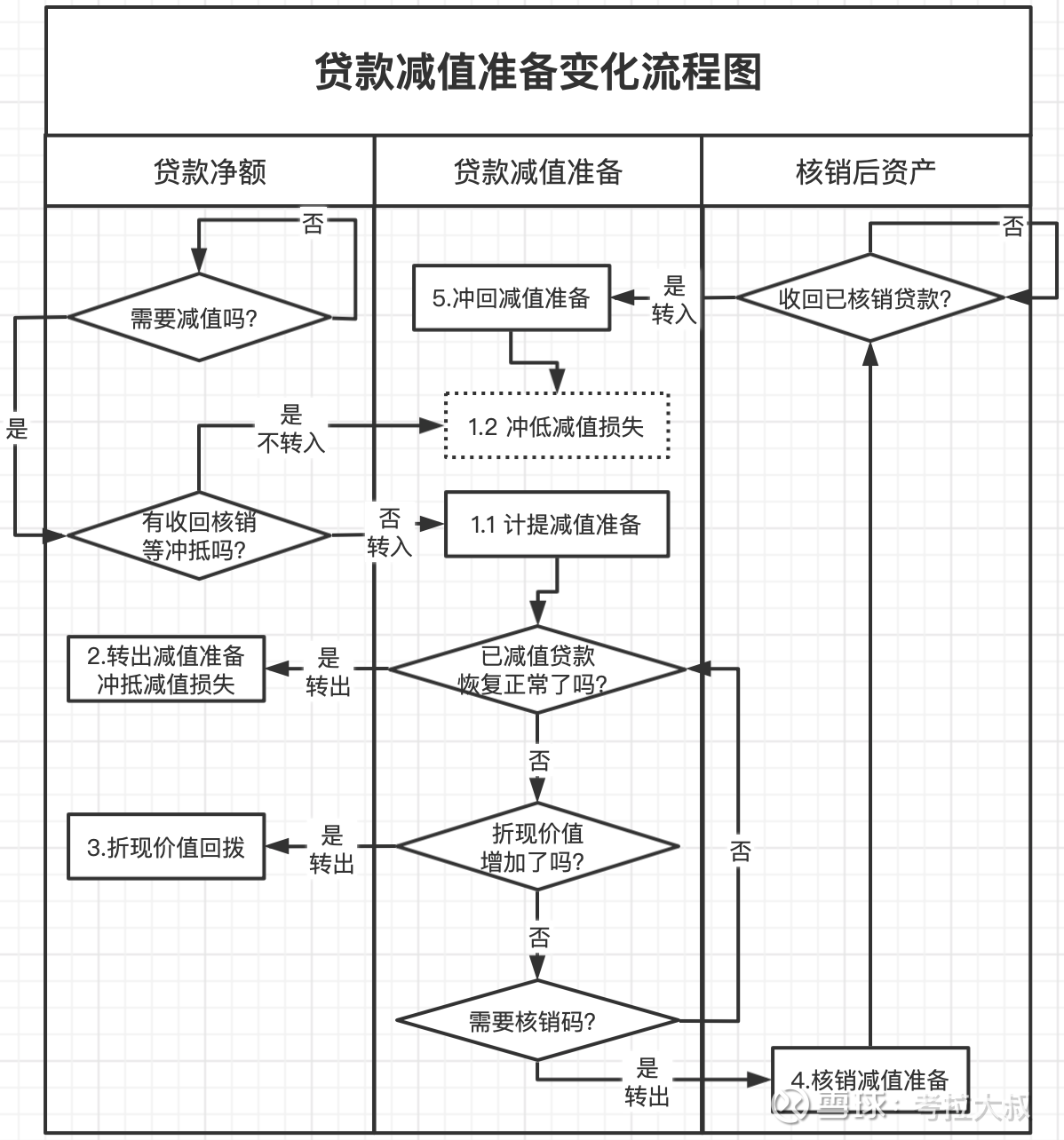

Figure 2 – Flowchart of Changes in Loan Impairment Allowance

Figure 2 is a flow chart of the five main changes above:

Change 1: The bank will regularly check the expected loss of the loan. When the loan needs to be impaired, it will trigger the accrual operation, the loan will be impaired, and the amount corresponding to the impairment loss will be transferred to the provision balance. However, there are two situations at this time. In 1.1, if there is no offsetting operation for impairment losses at this time, then the normal accrual will be made, the loan provision will increase, the net loan amount will decrease, and the total loan amount will remain unchanged. In 1.2, if there is currently a write-off operation for impairment loss, such as the recovery of a written-off loan or exchange rate changes, the loan impairment operation will still occur, but the impairment loss will be offset (offset) The end result is that the loan provision is unchanged, the net loan amount is unchanged, and the total loan amount is unchanged. But in fact, in 1.2, there is a process of increasing loan provision and then decreasing (being offset), and the net loan amount also has a process of decreasing first and then increasing, but the final result does not seem to have changed.

Change 2: When the bank regularly checks the expected loss of a loan, if it finds that the expected loss of a loan has decreased or disappeared, it will trigger a reversal operation to transfer the expected impairment loss of the loan out of the provision. At this time, the loan provision decreases, the net loan amount increases, and the total loan amount remains unchanged.

The “accrual/reversal” shown in Figure 1 (i.e. loan impairment losses in the income statement or income statement) is the combined result of Change 1 and Change 2, and is a net concept.

Change 3: When the discounted value of a provision increases (that is, the impaired loan generates interest income), a reversal operation will be triggered, and the increased discounted value (interest income) will be transferred out of the provision. At this time, the loan provision decreases, the net loan amount increases, and the total loan amount remains unchanged. For details, please refer to “Is the interest income of the bank’s impaired loans (provisions) included in the current operating income? 》

Change 4: When the bank regularly checks the expected loss of the loan, if it finds that a loan has been confirmed to be completely irrecoverable, the write-off operation will be triggered, and the corresponding loan amount will be transferred out of the provision. At this time, the loan provision decreases, the net loan amount remains unchanged, the total loan amount decreases, and the assets increase after write-off. The post-write-off asset here is a special account used to continue the recovery of non-performing assets after write-off, and it does not belong to the bank’s balance sheet.

Change 5: When the bank recovers a part of the written-off loan through litigation or judicial auction, it will trigger the reversal operation, transfer the corresponding recovered amount to the provision, and then transfer it out of the provision to offset the loan impairment loss. At this time, the final result is that the loan provision remains unchanged, the net loan amount remains unchanged, the total loan amount remains unchanged, cash and deposits with the central bank increase, and assets decrease after write-off. There is also a process of first increasing and then decreasing loan provisions. For details, please refer to “In what form does a bank’s provision exist? Where is it? (3) The official has revealed the answer to the accounting treatment of recovering the written-off loan”

It should be noted that the process of change 5 usually occurs at the same time as the process of change 1.2, or more accurately, the bank will usually combine the process of change 5 and change 1.2. The cancelled loans led to an increase in the balance of loan provisions, but in fact, the increase in the balance of loan provisions was caused by the impairment of loans in Change 1.2, but the amount recovered in Change 5 offset the reduction in Change 1.2. loss of value, as if the loan impairment in Variation 1.2 had not occurred.

4. The actual impairment of the loan is usually greater than the impairment loss of the loan

From Change 1, Change 2 and Change 5 above, we can see that there are two offsetting operations for impairment losses, one is the recovery of impaired loans due to better quality (reduced expected losses), The other is due to the receipt of a fund (recovery of a written-off loan). Obviously, the former can be offset with the current loan impairment, because there are indeed loans that have improved, and we only care about the net loan amount that has deteriorated, but the latter should not be offset, because the funds received mask the changes. Poor loans make the real loan impairment smaller.

The loan impairment loss disclosed in the bank’s financial report is actually the result of the superposition of the above two offsetting operations, which is a concept of net accrual. Therefore, if you want to know the real loan impairment level of the bank in the current period, you need to exclude the recovery and verification. Disruption of selling loans.

Calculation formula:

Actual loan impairment in the current period = loan provision balance at the end of the period – loan provision balance at the beginning of the period + write-off/disposal in the current period

For example, the impairment loss of China Merchants Bank’s loans in 2021 (accrued/reversed in the current period in Figure 1) is 37.020 billion yuan, while the actual loan impairment in the current period is 46.545 billion yuan. The difference between the two is mainly 9.893 billion yuan. Recover the written-off loan.

5. What is meant by “release provisions and increase profits”

Investors in banks often expect high-provision banks to “release provisions and increase profits” when asset quality improves. In fact, “release provisions” refers to “change 2” in Figure 2 and “Change 5” two types of processes, when the expected loss of bank loans is reduced, part of the impaired loans can be transferred back to normal loans, at this time, the current “loan impairment loss” will be reduced, and this will be reduced. At the same time, it will increase the net profit. The process of “Change 5” has a similar effect.

But from Figure 2, we can find that in fact, the process of “release provisions and increase profits” occurs in every financial report of the bank, and it is a process. It’s just that when the bank discloses the data, all the changes in Figure 2 are combined, and only the final net amount is disclosed. Therefore, the statement we often see: “Banks with high provisions will not have so many bad debts in the future will release provisions and increase profits” is actually a wrong statement. Or, this statement is not accurate. The correct or accurate statement should be: “If the bank reduces the loan-to-loan ratio by lowering the standard of loan impairment in the future, it will increase its profits.”

Because the bank’s loan scale has been growing rapidly, if the loan-to-loan ratio is not reduced by lowering the impairment standard, the trend of net interest margin or non-interest income needs to be reversed, otherwise the newly provided provision will always cover the transfer rate. We have never seen the bank release the provision. Agricultural Bank is a typical example. For details, see “Can the Super-Provisioned Agricultural Bank Release Profits and Achieve Davis Double-Click? 》

6. Conclusion

To sum up, we can see from the change process of loan impairment provision that banks can release profits only when they lower the loan-to-loan ratio by lowering the impairment standard. At present, the loan-to-loan ratios of listed banks vary greatly, with more than 4% and less than 2.5%. Can banks lower the impairment standard? Or how much loan ratio does the bank need? In the next article we will focus on this issue.

To be continued. . .

[This article is original, your likes, shares and comments are the greatest support for my continuous creation! At the same time, you are also welcome to pay attention to “Uncle Koala Snowballing” and discover my sharing in time! 】

$ China Merchants Bank (SH600036)$ $ Industrial Bank (SH601166)$ $ Ping An Bank (SZ000001)$

@Today’s topic @snowball talent show #snowball star plan# #Investment alchemy season in mid-2022#

This topic has 10 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/2836571636/231385730

This site is for inclusion only, and the copyright belongs to the original author.