I. Introduction

In the previous article, How do banks release provisions to boost profits? In “The Change Process of Bank Loan Impairment Provisions”, we discussed in detail the change process of bank loan impairment provisions, and finally came to the conclusion that banks are actually releasing a large amount of provisions every year, and in the future only by lowering the impairment standard to reduce Loan ratio can increase profits.

So, what should the bank’s reasonable loan-to-loan ratio be? Is the current loan ratio high? How much downside is there? This article and the next two articles have a total of 3 articles. Through the stress test of provision consumption, we will discuss whether the current provision-to-loan ratio of banks is sufficient, and how much room for decline. At the same time, we can also see how much non-performing loans and the impact of revenue reduction can be resisted by banks’ current provisions.

2. The difference in the provision-to-loan ratio between banks comes from the provision for normal loans

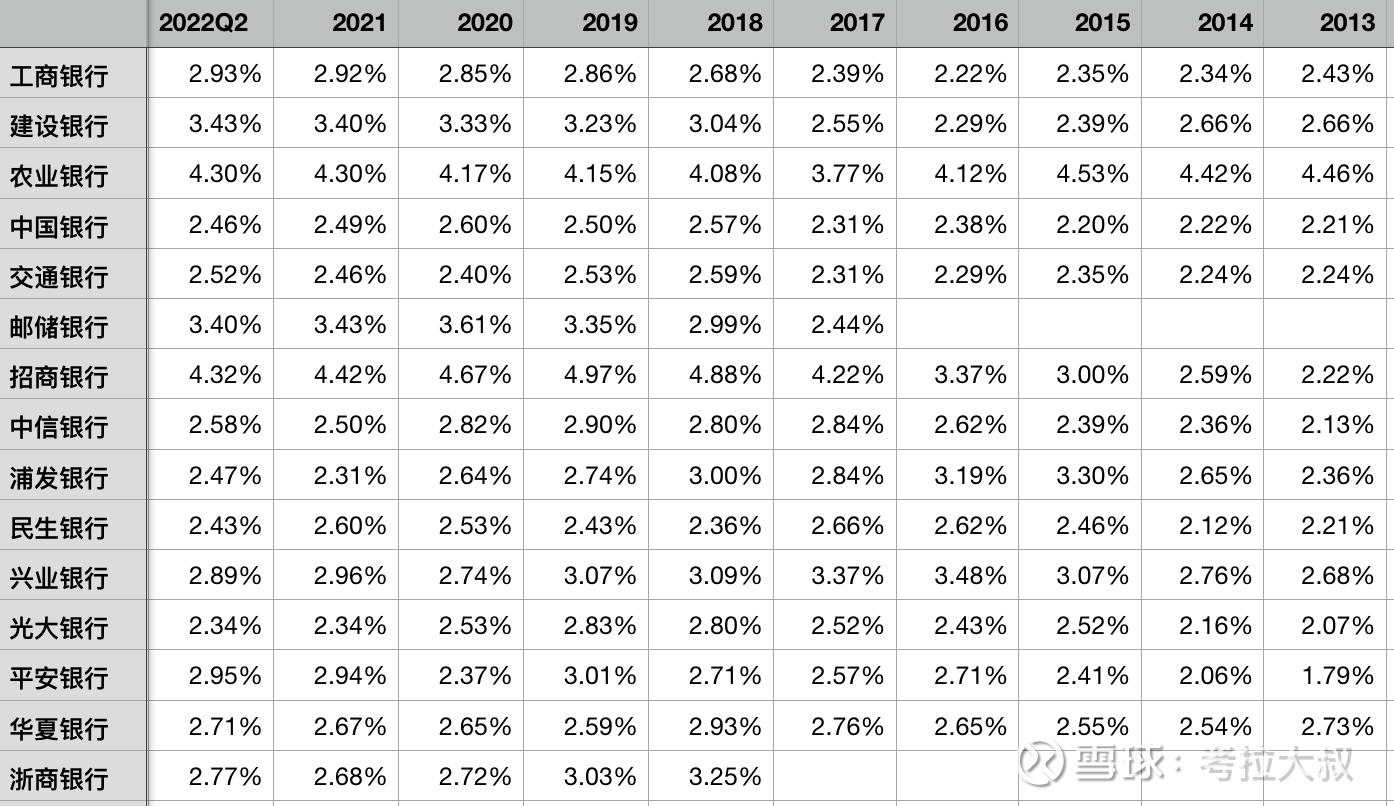

Loan provision ratios (provision-to-loan ratios) vary widely among listed banks.

Table 1 – Loan Provision Ratio (Appropriation to Loan Ratio)

Calculation formula:

Loan provision ratio (provision-to-loan ratio) = loan provision balance ÷ total loan

Among them, the balance of loan provisions includes the sum of the balance of loan provisions measured at amortized cost and the balance of loan provisions measured at fair value.

As shown in Table 1, in the middle of 2022, China Everbright Bank, Minsheng Bank and Shanghai Pudong Development Bank with the lowest loan-to-value ratios are all less than 2.5%, while the highest China Merchants Bank and Agricultural Bank are all over 4.3%, the difference between the two is nearly double.

However, the difference is even more disparity in the provision rate of normal loans.

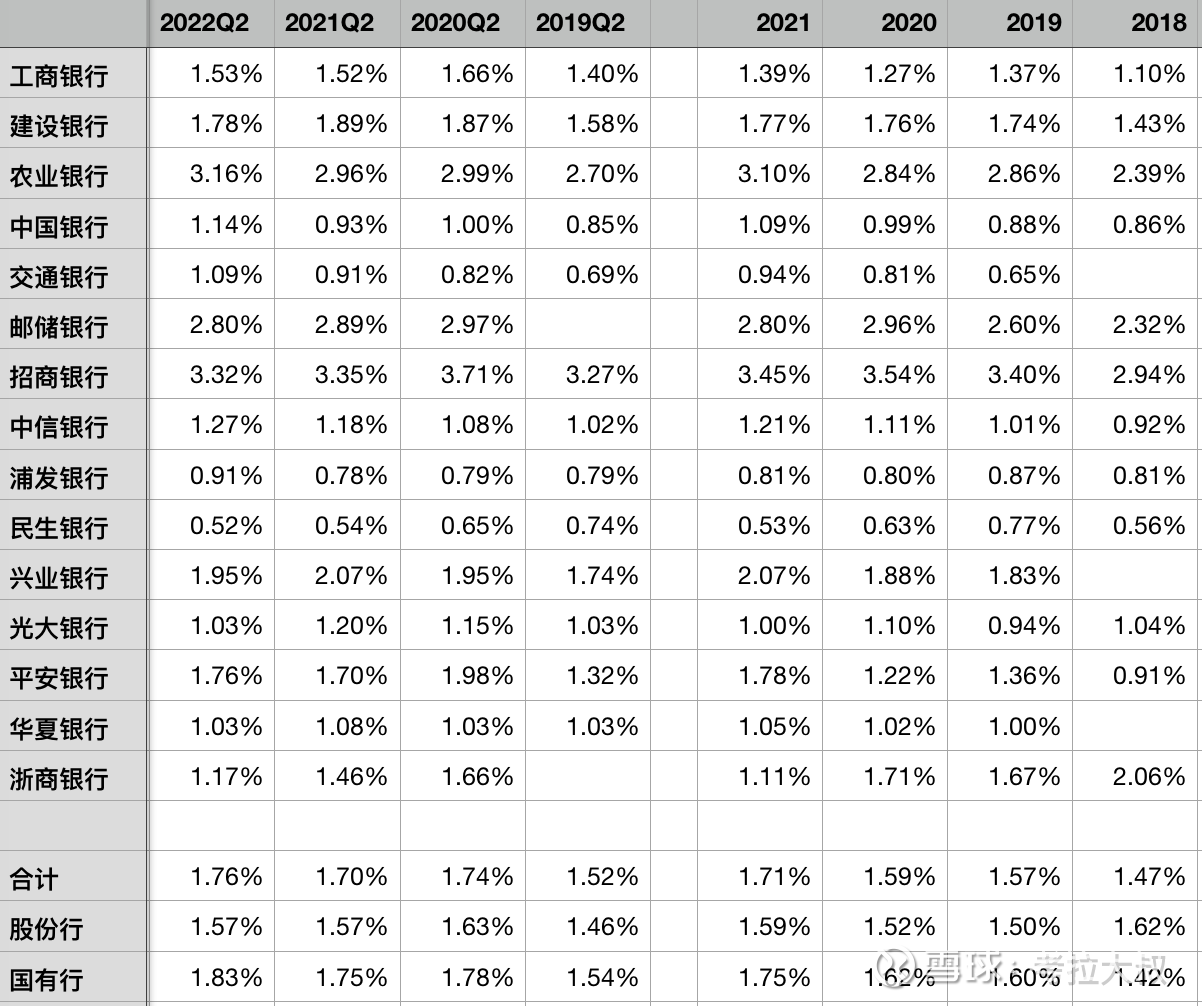

Table 2 – Loan provision rate for the first stage (measured at amortized cost)

Calculation formula:

First-stage loan provision rate = first-stage loan provision balance ÷ first-stage loan balance

Note: This is the loan measured at amortized cost

As shown in Table 2, in the middle of 2022, Minsheng Bank’s loan provision ratio for the first stage is only 0.52%, Shanghai Pudong Development Bank is less than 1%, and many banks are only slightly over 1%, while China Merchants Bank and Agricultural Bank have exceeded 1%. 3%, the difference between high and low is more than 3 times, and this gap is more significant than the difference in loan-to-grant ratio in Table 1.

Therefore, the difference in the provision rate of normal loans (first-stage loans) is the main reason for the large difference in the provision-to-loan ratio between banks. So how should normal loans be provided for?

3. Why do normal loans also need to be provided for?

First, briefly review the concept of the three-stage model: the first stage is that the credit risk has not increased (normal category), the second stage is that the credit risk has increased significantly but there is no evidence of impairment (concerned category), and the third stage is that there has been an objective reduction in credit risk. Value evidence (bad class).

Here, the second and third stages of impairment preparations are easier to understand. After the credit risk of an asset has risen significantly, it will naturally need to be depreciated, and it is natural for assets with objective evidence of impairment to be depreciated. But why should assets with no credit risk be impaired? What is the basis for the proportion of its impairment?

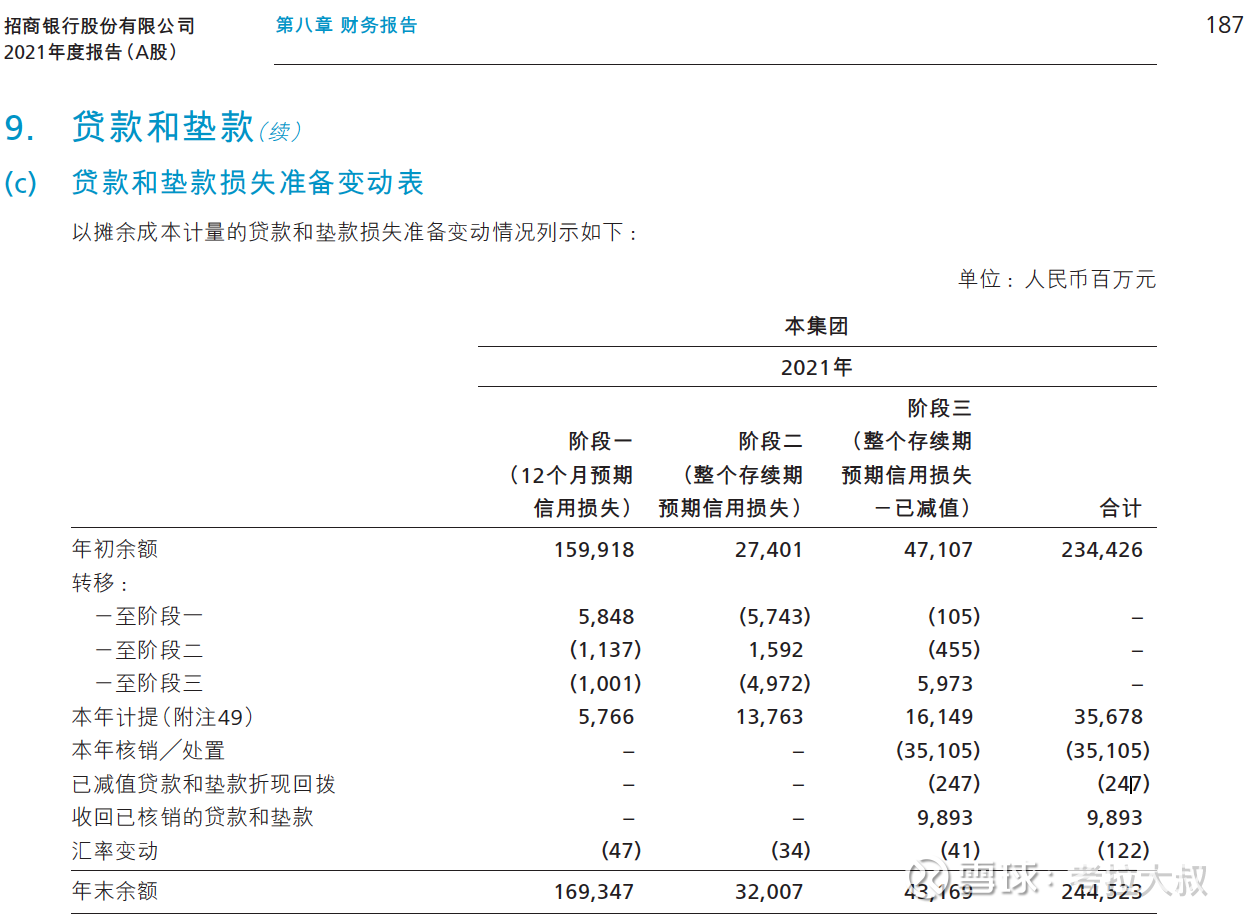

Table 3 – Changes in Loan Impairment Provisions in China Merchants Bank’s 2021 Annual Report

As shown in Table 3, China Merchants Bank’s loan provision balance was 244.5 billion by the end of 2021, but 169.3 billion (69%) of which were impairment provisions for the first-stage loans. So why does China Merchants Bank make so many impairment provisions from the first-stage loan? Is it hiding profits?

In fact, we can get a general understanding by looking at the header part in Table 1 below. In the second and third stages, because the credit risk has already occurred, the entire duration of the asset can be depreciated according to the size of the risk. Although the first stage has not yet Credit risk, subject to impairment for expected credit losses (expected risk) for the next 12 months.

So the question is, how to predict the credit loss of the first stage loan (normal loan) in the next 12 months?

In fact, each bank has its own expected credit loss model, such as the normal loan migration rate announced in the annual and interim reports. This migration rate refers to the normal loans at the beginning of the period (January 1) to the end of the year (12 loans). month) what percentage has migrated downwards (becomes special mention or non-performing loans). That is to say, banks usually use models such as the migration rate of normal loans to estimate how much the first stage loans will migrate to the second and third stages in the next 12 months, and then based on the second and third stage loans. The accrual ratio is used to depreciate the first-stage loan.

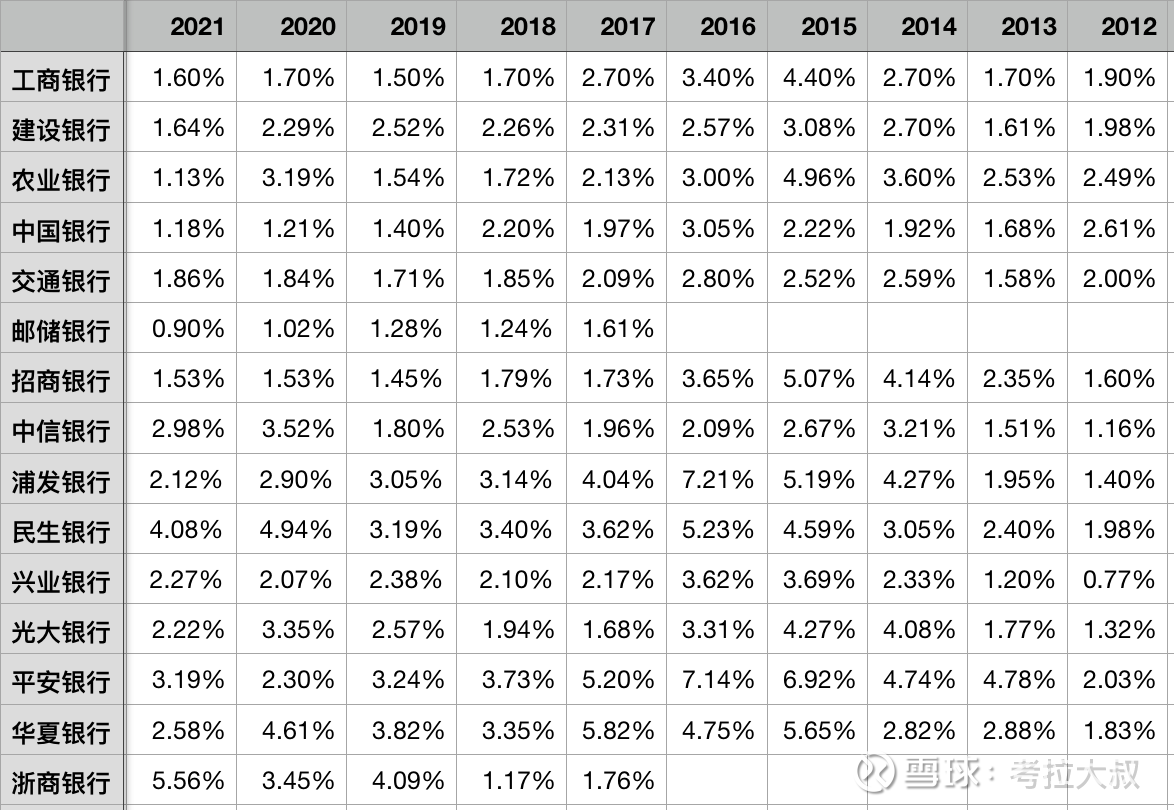

Table 4 – Migration rate of normal loans

Calculation formula (schematic):

The balance of the first stage loan provision = the first stage loan balance✖️ (the migration rate of the first stage loan to the second stage✖️the second stage loan accrual ratio + the first stage loan to the third stage migration rate✖️the third stage loan calculation ratio)

For prudent banks, the provision rate for the first phase of loans should at least be able to guarantee the following guarantees for the bank: when the bank suffers a large non-performing impact in the next year (12 months), its normal loans When the downward migration rate rises sharply, the bank’s stock provision is still sufficient after a large amount of consumption, and there is no need to make excessive provision in the current period, so that the performance will not be significantly affected.

Therefore, let’s look back at the provision rates of the first-phase loans of the 15 banks listed in Table 2. You can use this data to compare the migration rates of normal loans of various banks (Table 4), and you will find It is found that the provision rate of many banks’ first-stage loans is significantly lower than the migration rate of their normal loans, which shows that the provision rate of their normal loans is seriously insufficient.

4. Conclusion

The bank’s provision is a counter-cyclical adjustment tool. The bank keeps increasing the ratio of loans to loans in the period of low NPL generation (in Table 1, the ratio of loans to ABC before 2015 and after 2018), while in the period of high NPL generation If the write-off is increased, the loan-to-appropriation ratio will decrease (in Table 1, the loan-to-appropriation ratio of the Agricultural Bank of China from 2016 to 2017).

In the past 10 years, most banks have not been able to raise the loan-to-pay ratio to a relatively ideal value. Therefore, very few banks can actually release their performance by reducing the loan-to-pay ratio (Figure 1, 2019). China Merchants Bank’s loan-to-grant ratio after 2019)

So what is the bank’s ideal loan-to-grant ratio? In fact, this problem has a lot to do with the bank’s loan migration rate or non-performing generation rate in the past, because the loan migration rate and non-performing generation rate presented by different banks in the latest round of non-performing major cycles are very different. This difference is the difference between banks. An important reason for the disbursement ratio difference. See the next article for details.

[This article is original, your likes, shares and comments are the greatest support for my continuous creation! At the same time, you are also welcome to pay attention to “Uncle Koala Snowballing” and discover my sharing in time! 】

related articles:

How do banks release provisions to boost profits? The Change Process of Bank Loan Impairment Provision”

“Is the interest income of the bank’s impaired loans (provisions) included in the current operating income? (S-level difficulty! Enter carefully!)”

“In what form do bank provisions exist? Where is it? (3) The official has revealed the answer to the accounting treatment of recovering the written-off loan”

“Can the ultra-high-provisioned Agricultural Bank release profits to achieve Davis’s double-click? 》

$ China Merchants Bank (SH600036)$ $ Industrial Bank (SH601166)$ $ Ping An Bank (SZ000001)$

@Today’s topic @snowball talent show #snowball star plan#

There are 48 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/2836571636/231642131

This site is for inclusion only, and the copyright belongs to the original author.