Around the end of the 20th century, when the bull market peaked, I bought some funds one after another. At that time, the media was all promoting: buying stocks is not as good as buying foundation, and buying foundation is suitable for Xiaobai Yunyun. That meeting was indeed fierce, and the group stocks pushed up the stock price of Baijiu. Regardless of public offering or private placement, the performance is very good. Everyone knows the story after that. Let’s talk about how to buy foundation and how to avoid pitfalls. Welcome to exchange, old bird light spray ![]()

How to choose a fund? I also think the easiest funds for beginners to start with are index-enhanced funds. But that doesn’t mean you can buy without thinking. Buying this kind of broad-based index needs to look at the entry time. For example, I bought the Shanghai-Shenzhen 300 Index in October 21, and the current loss of 6% and the highest point loss of 20% also subverted the previous perception. At that time, it was not a relatively safe entry position.

The industry is basically the same. For example, if you want to buy a liquor index fund, you can judge for yourself at the current position. Personally, I think there is not much room for imagination to rise.

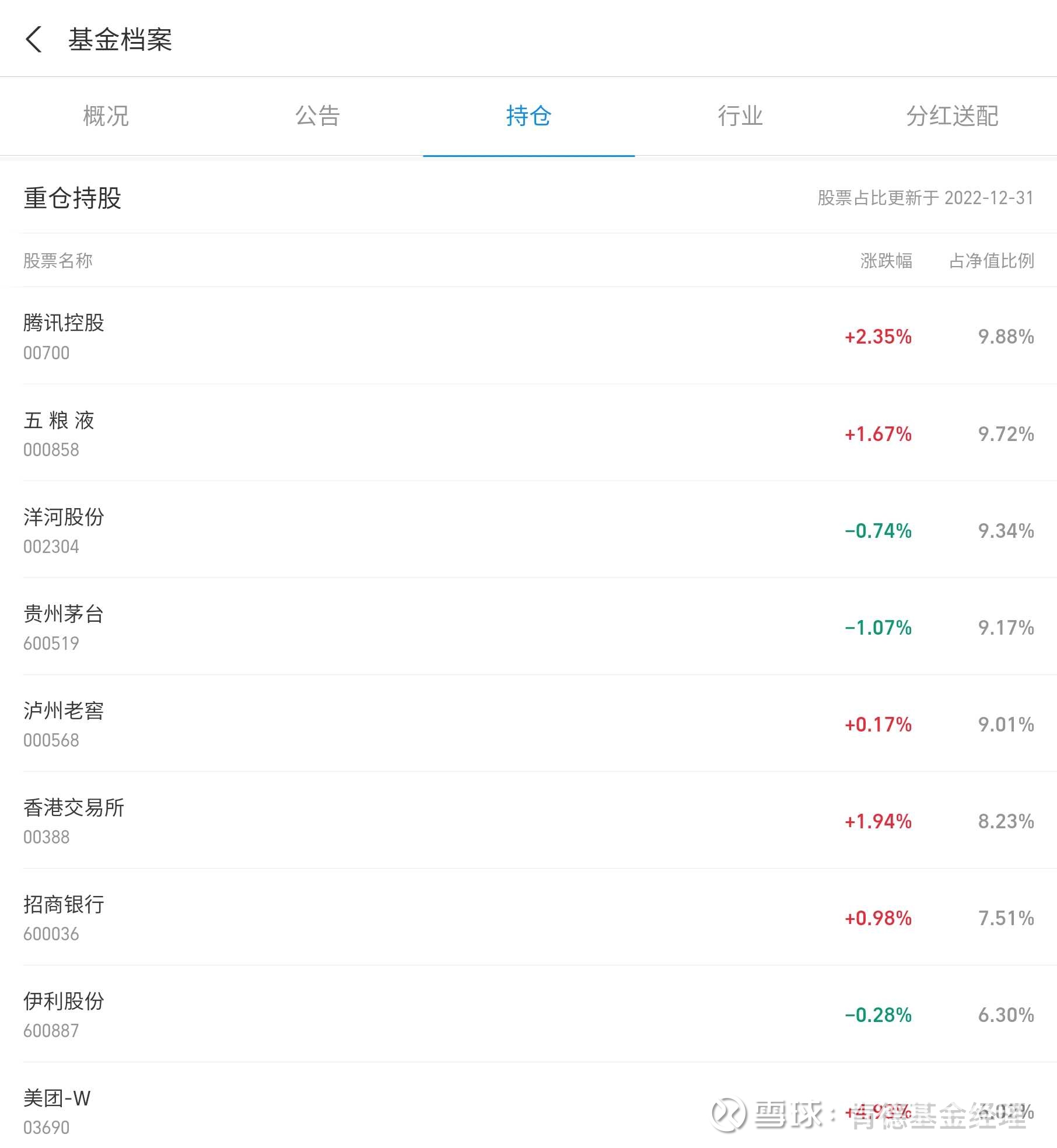

Novices are more exposed to some star groups, such as Kun Kun and Lan Lan. I recommend staying away from large-scale public funds. As the scale increases, fund managers can only choose to embrace big blue chips. Kunkun’s fund has soared by 28% in the past three months. I think it’s just a restoration of its heavy holdings, and it doesn’t mean that Kunkun’s ability to make money is very strong at this stage. People who look at the 28% yield rate and kill them may be the same type of people as the novices who entered the market three years ago. Look more at small-scale funds. Although the holdings are not necessarily accurate, you can analyze the style preferences of fund managers. I personally don’t like this kind of public offering where most of the positions are big-ticket hot stocks. For potential public offering funds, the scale must not be too large, and the mix of growth stocks must not be small. They are all big tickets, why should I buy yours?

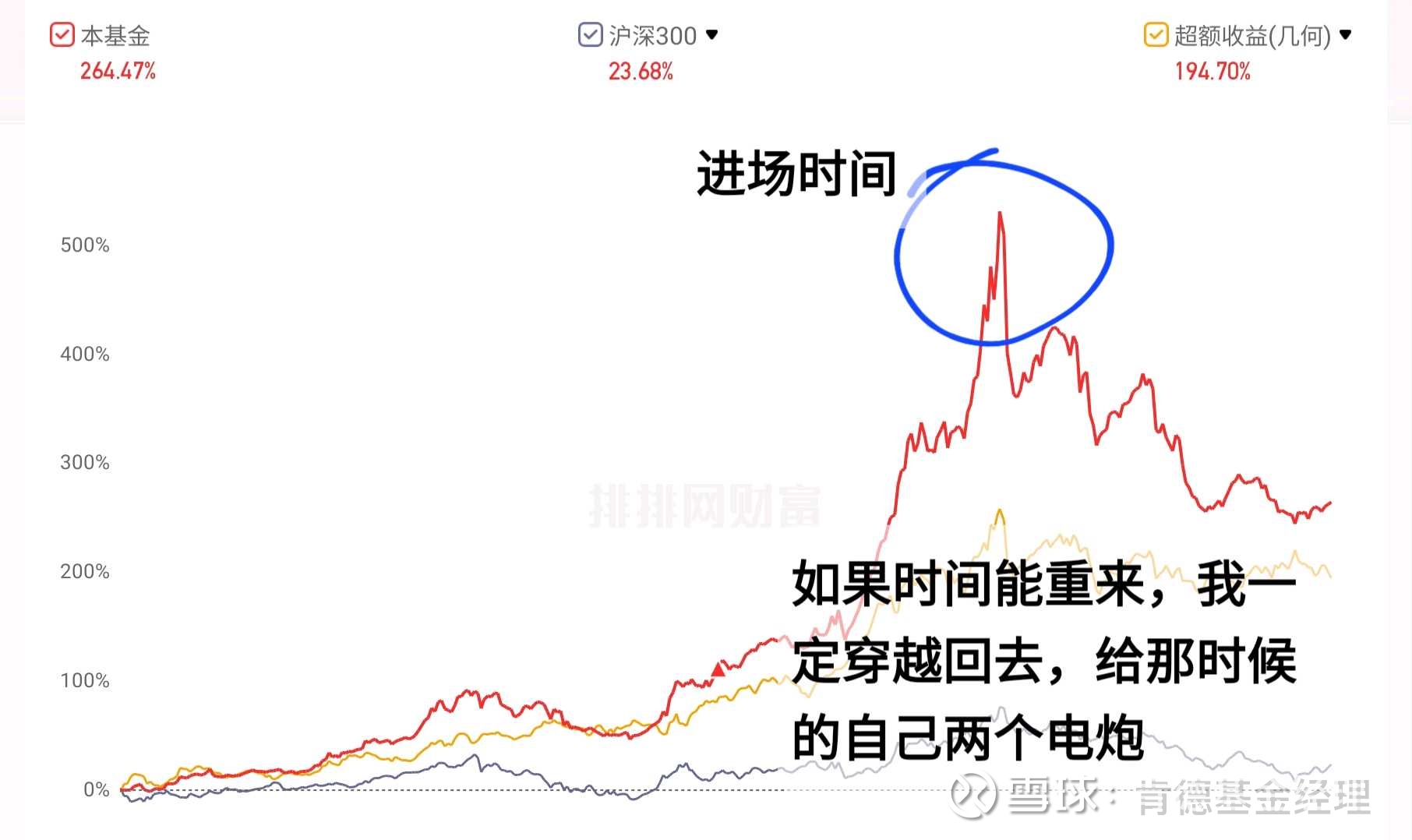

When it comes to private equity, there are tears. I talked about it in a previous article. Three years ago, I let the road show of private equity and the copywriting of investment advisors come to the fore. At that time, the net worth was indeed against the sky, and the double-digit growth in a single week made people lose their minds. Then entered the market at the highest point, and then was caught up to the current floating loss of about 17%. See, no matter what fund you buy, the time to enter the market is always the primary consideration.

Stock private placement is basically divided into subjective long and quantitative. Let’s talk about subjectivity first. In recent years, being a subjective private equity fund manager has fallen from the altar one after another. Among this group of people, there are also some arrogant managers who feel that investors don’t understand anything. And their investment logic may have long been outdated. I only know how to group consumer stocks, or only know how to buy liquor stocks, and I don’t know anything about other sectors and I don’t bother to study them. Let me tell you that this is called long-term value investment. Investors who happened to buy this kind of scumbag private equity, if the closing period has not yet arrived, they can only admit it. In the subjective field, there are many ghost fund managers. I have also been fooled, just look at the past resume, there are almost no fund managers with bad resumes. Who hasn’t won the Golden Bull Award? What awards he has won, what outstanding performance he has had in the past, and whether you make money buying his fund are two different things.

How to buy subjective long private equity? Again, try not to buy more than 10 billion yuan. 3-5 billion can be focused on. Neither is it too small. Let’s analyze his real performance in recent years. If you can buck the trend and rise sharply, you must figure out how he made the money. Just like a private equity fund, which bucked the trend and rose by 80% in 2018. Later, when I inquired, the manager actually took a heavy position in a stock with a single ticket. I keep a respectful distance from this kind of gambling fund manager.

Don’t stay closed for too long. Investment consultants will tell you that private equity with a long closed period can help customers cut their meat when they fall sharply. This is probably the same rhetoric. On the other hand, you find that this is a mediocre fund manager. If the market rises sharply and he doesn’t rise, you can’t even run away.

Needless to say, it is necessary to analyze the industry that the private equity fund manager is good at. For example, if you are only good at private equity for consumption and medicine, this kind of thing is not interesting.

But you said that private equity is better than public equity, I thought so three years ago, but I really haven’t seen it in recent years ![]() During the sharp drop, few leading private equity funds were able to flexibly lighten their positions, especially those with a low turnover rate, and they dared not cut their meat easily. If the return of private equity is less than that of public equity, many private equity investors will really feel that they are losing money. They don’t need to divide the excess of public equity, so why buy your private equity?

During the sharp drop, few leading private equity funds were able to flexibly lighten their positions, especially those with a low turnover rate, and they dared not cut their meat easily. If the return of private equity is less than that of public equity, many private equity investors will really feel that they are losing money. They don’t need to divide the excess of public equity, so why buy your private equity?

There is nothing much to say about quantification. One is the scale, the other is the benchmarking index (I will pay more attention to stock selection in the whole market), and the third is the effect of the model. As long as supervision does not suppress, quantification is still possible, and it is hard to say who is good and who is not. And some small-scale quantitative public offerings can also be paid attention to. I remember when I first paid attention to Sheng Fengyan. At that time, his management scale was not large, and his performance was good. Do not lose some quantitative private equity.

As for CTA, neutral these, novices should not touch it first. It’s more complicated than a few words can’t finish.

I hope that in 2023, everyone’s funds can turn losses into profits, and the performance will be Changhong ![]()

There are 2 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/6354539217/240579892

This site is only for collection, and the copyright belongs to the original author.