Generally speaking, on Friday night, the China Securities Regulatory Commission will release some news: either heavy fund varieties, important new regulations, or drafts for new regulations. . . and many more.

Normally, one Friday, one message is enough.

Yesterday was Friday, and the China Securities Regulatory Commission issued an official new regulation—ETF interoperability, a draft for comments—personal pensions. Really, many people are busy again this Friday.

Reporters or other practitioners have already reported relevant reports, so I will not interpret the full text. If it is not necessary, I will talk about my concerns about the two regulations.

Let me talk about ETF interoperability first.

Opinions have been solicited before the ETF interoperability, and the announcement last night was regarded as the official finalization.

I’ll say it briefly.

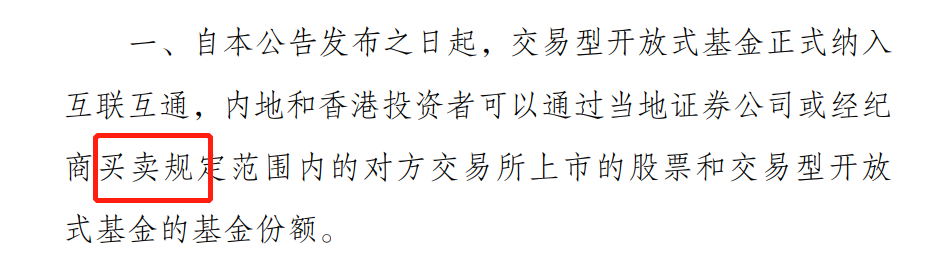

Now that the mainland and Hong Kong have exchanged stocks, mainland investors can use the Hong Kong Stock Connect, mainland investors can buy Tencent Holdings and HSBC, and overseas investors can invest in Kweichow Moutai and Ningde Times through Shanghai Stock Connect or Shenzhen Stock Connect.

Now, the exchange of ETFs between China and Hong Kong is also very meaningful.

Let me say two things:

1. Trading.

Well, you can only buy and sell. If you want to apply for cross-border redemption, you can’t do it for the time being. You can’t do it in one step.

2. Identification code.

In fact, you must have a real-name system, and the supervision can see you. If you use a Hong Kong account to buy and sell mainland ETFs, or you use a mainland stock account to buy and sell Hong Kong ETFs, the supervision can see you.

Of course, as long as you don’t commit crimes or break the law, the supervision will not take extra care of you.

This effect is not too big, because the interconnected stocks between the two places are already like this, but the policy continues.

Okay, the ETF interoperability is over. Now let’s talk about the draft for personal pension investment in public funds, the draft for comments. As the name suggests, it is definitely not a formal draft, or it is drafted. First, ask for opinions from all parties, and if there are differences, please submit them quickly.

Individual pension accounts are the latest news.

The status quo of pensions in my country is basically as follows:

1. The pension that most people participate in is commonly known as social security, or more commonly known as pension, including employees and residents (farmers). This is mandatory and has the highest degree of participation.

2. The participation of civil servants or career staff is occupational annuity, and the participation of enterprise employees in enterprise annuity is greatly reduced.

Let’s not talk about public officials. For companies that have enterprise annuities, the benefits are generally good.

Some units publicize when recruiting: We provide five insurances and two funds . The other fund besides the provident fund is basically an enterprise annuity or an occupational annuity. Of course, the annuity can only be withdrawn after retirement, so don’t be excited.

3. Personal pension

In the past few years, the pilot program has been carried out to invest for oneself and set a limit, and the money invested within the limit can be exempted before tax every year.

In the past few years, it was mainly the exploration in the field of insurance, but you also know that pension cannot only rely on insurance.

So this time I came up with an individual pension account.

The initial plan is that in the future, each person can invest 1,000 yuan per month, and a total of 12,000 yuan per year. In particular, this money can be deducted before tax, and can be invested in funds, insurance, wealth management, etc., and the investment scope has been expanded.

This is not a personal social security account, because it is prepared for your future retirement, so you can’t take it out until you retire. Many people call it the Chinese version of “401K” .

Because the idea of designing a personal pension account is that it can invest in various pension products such as funds, insurance, and wealth management, it must involve multiple regulatory departments.

The China Securities Regulatory Commission released a draft for personal pension investment in public funds last night. It is estimated that other relevant departments will also launch it in the near future.

The draft for comments was issued yesterday, and major media have already reported it.

Let me tell you my opinion: Generally speaking, I have a positive evaluation of the draft issued by the China Securities Regulatory Commission yesterday, but I also have a few comments.

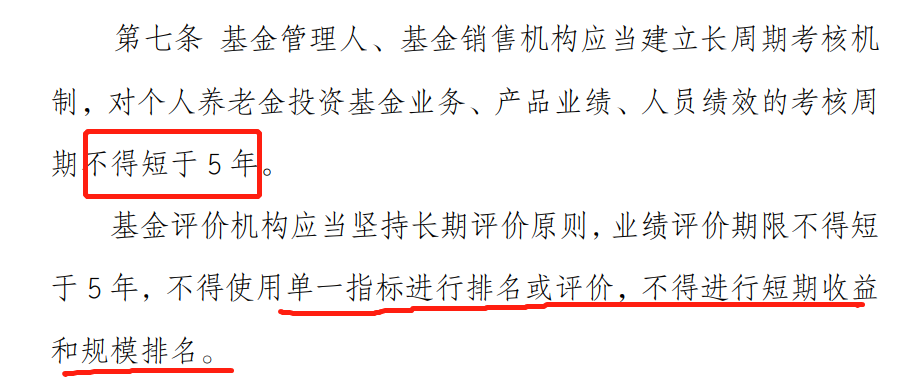

1. Long-term assessment, praise.

Article 7 stipulates that the assessment period is at least 5 years, and a single index ranking cannot be carried out.

Many people are still decades away from retirement, so the assessment period for individual pensions should be extended.

As we all know in the past two years, public funds have gradually become popular among post-90s, post-95s, and even post-00s investors because of their high degree of choice and low threshold.

Some investors have an immature idea of investing in funds. They follow the trend and follow the hot spots. I will buy the one that goes up . There are also star-chasing funds. In the short period of 2021, the performance is obvious.

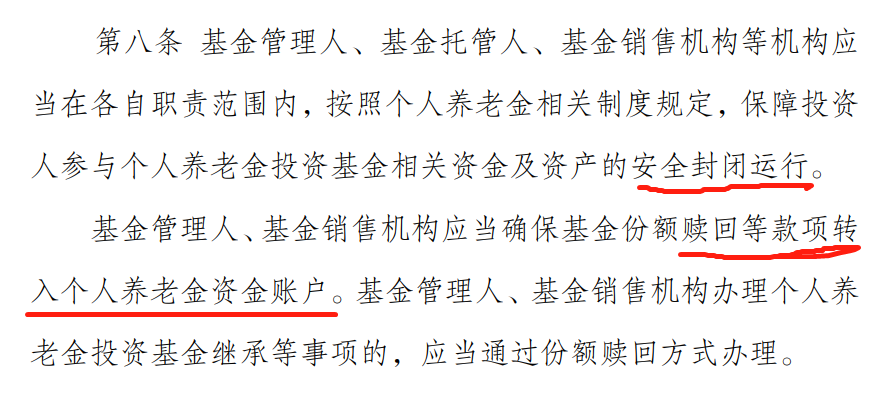

2. Closed operation

Because personal pensions can be deducted before tax when calculating personal income tax, you want to buy a fund with the money deducted before tax, and then redeem the fund, can the cash be tax-free?

Don’t think about it, close the operation, return it to the personal pension account after redemption, and wait until retirement to take it out.

I estimate that the same is true for personal pension accounts when buying public funds, and it is the same when buying wealth management and insurance.

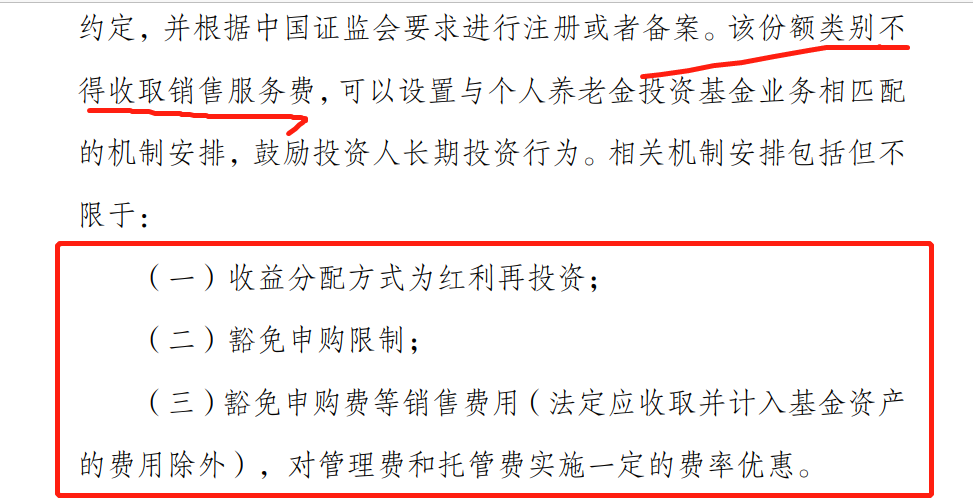

3. Cost concessions

Long-term investment is encouraged, so discount rates are available. Subscription fees can be free, and management fees or custody fees may be discounted.

However, except for the fees that should be charged and included in the fund assets, this is the 1.5% redemption fee for short-term operations of some funds (such as the redemption fee that is held for less than 7 days), which is also to persuade everyone to practice long-term investment. idea.

4. Scale

Well, the best part and the biggest doubt are in this one.

Personal pension is a kind of pension encouragement (pre-tax deduction) measure for investors across the country. We must choose good funds and institutions, and try to choose some large institutions. There is no problem with this logic.

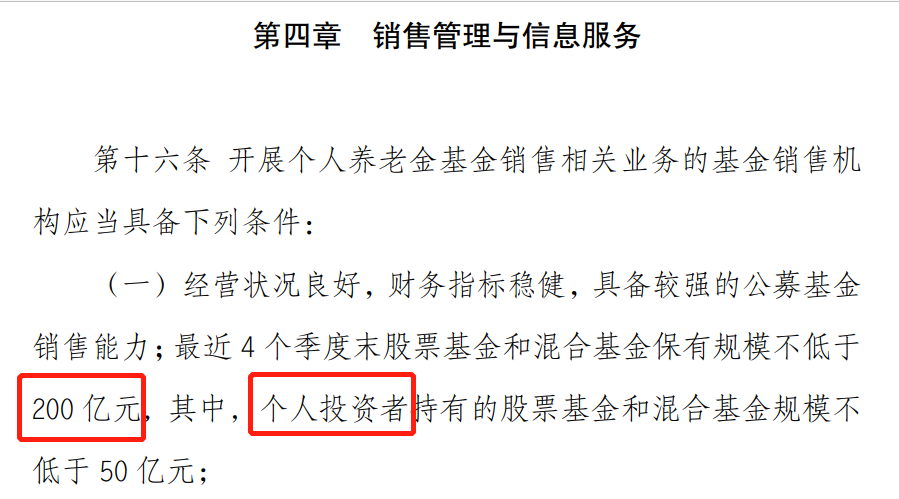

The regulations issued by the China Securities Regulatory Commission also reflect that if you want to carry out personal pension sales, you must have a total of more than 20 billion in stock funds and mixed funds at the end of the last four quarters.

Because it is a personal pension business, mainly for ordinary people, the China Securities Regulatory Commission has specially emphasized that individual investors hold more than 5 billion stock funds and mixed funds, which is not popular with individual investors. Is there any service for individual investment? the ability of the person.

This is also a good place for the SFC, which I personally like.

But, but, but.

Here comes the question: my biggest comment on the content of the draft for individual pensions also came up at the same time.

As mentioned above, this is the part that I most agree with in the draft for personal pensions, and it is also the place that I least agree with.

The scale is the scale at the end of the quarter.

And the size calculation is stock funds and hybrid funds, OK, what do you think of?

Yes, as smart as you, you must have thought of it: at the end of the quarter, the sales agency will take the certificate of deposit fund for impulse.

The risk of certificate of deposit funds is roughly the same as that of currency funds, but currency funds are not currently in scale, but certificate of deposit funds are considered as hybrid funds, and they are considered scale, and only the scale at the end of the quarter is assessed, not the usual scale.

This trick can even be said to be bug-level.

The certificate of deposit fund is a hybrid fund, and it is a bug-level existence . Wasn’t the market not very good a while ago this year, and the fund could not be sold? Some sales agencies or grass-roots salespersons used the certificate of deposit fund to complete their tasks.

At present, the general fund sales assessment is stock fund (including index fund) + mixed fund sales. Certificate of deposit funds are mixed funds, and they have to be sold even if they can’t be sold. Customers also need them. , hit it off.

OK, why do you think certificate of deposit funds are popular? That’s how it fires.

As a result, some sales agencies have begun to convert the sales of certificates of deposit funds when assessing grass-roots sales personnel. I heard that selling 3 yuan or 5 yuan of certificates of deposit funds is regarded as an ordinary mixed fund.

So I think: the original intention of assessing the sales volume of stock-based and mixed-based sales at the end of 4 quarters is good, but the actual implementation needs to be reconsidered-whether the quarterly average scale can be used to replace the time point value, or whether the 4-quarter end-of-season value can be replaced by At the end of each month for 12 months, even if you want to make an impulse, you must increase the impulse cost of the sales agency. It is recommended that the mixed fund is not counted as a certificate of deposit fund. There is a difference between a certificate of deposit fund and a currency fund, but the essential difference is not big.

This prevents individual sales agencies from taking the CD funds at the end of the quarter to rush their own rankings, and also avoids the large inflow of funds before and after the end of the quarter, and then a large outflow, which will become a new factor that affects the instability of the financial market.

Finally, my country is gradually entering an aging society, and this personal pension is slowly being planned and promoted. It is not only the matter of the China Securities Regulatory Commission, the China Banking and Insurance Regulatory Commission, or the Ministry of Human Resources and Social Security. It involves all aspects and also concerns We ordinary people.

This was originally a draft for comments, and it was published to solicit opinions from all sides. It is suggested that everyone must know everything, say everything, and work together to make continuous efforts for this personal pension to better serve the elderly.

This is my personal opinion. As you know, I am not a highly educated person, nor do I have good investment ability. I generally agree with the draft of the regulations on personal pension investment in public funds, but I think it is necessary for me to express my different views on a certain article.

There are 9 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1062883669/223616727

This site is for inclusion only, and the copyright belongs to the original author.