Image source: Visual China

Reporter | Zhou Shuqi

On November 9, the latest data released by the Passenger Car Association showed that the retail sales of the passenger car market in October 2022 reached 1.84 million units, a year-on-year increase of 7.3%, but a month-on-month decrease of 4.3%. This is also the first time since 2013. Ten” chain drop characteristic.

The Passenger Federation believes that the month-on-month trend of new energy vehicles and traditional fuel vehicles in October was affected by the epidemic prevention measures in individual regions, and the situation of store closures was more prominent. The epidemic prevention and control efforts in various places are strong, and the important methods of attracting customers at the store have a certain impact, which has changed the pattern of strong sales at the end of the year and formed a relatively flat “golden nine and silver ten”.

On the whole, self-owned brands still maintain continuous sales growth, with a domestic retail market share of more than 50%, an increase of 6 percentage points year-on-year to 51.5%; the cumulative share of self-owned brands from January to October is 49%, an increase of 5.4 percentage points compared to the same period in 2021 .

The China Passenger Car Association pointed out that self-owned brands have achieved significant growth in the new energy market and export market, leading traditional automakers have performed well in transformation and upgrading, and the share of traditional auto brands such as BYD Automobile, Geely Automobile, Changan Automobile, and Chery Automobile has increased significantly.

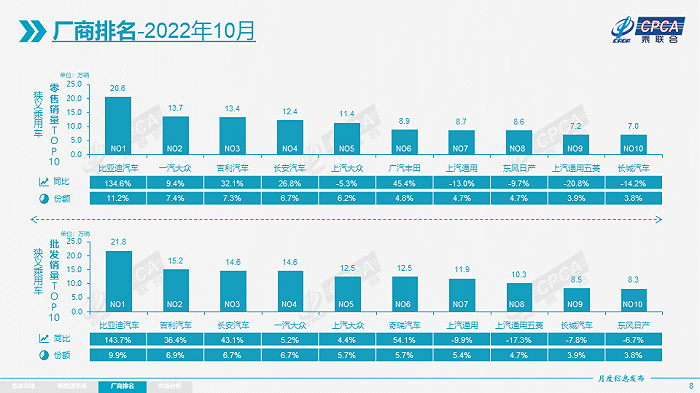

According to the October Manufacturers’ Wholesale Sales Ranking of the China Passenger Car Association, BYD, Geely Automobile and Changan Automobile ranked in the top three, surpassing the long-term “topping list” of North and South Volkswagen. Among them, BYD has topped the list for the fourth consecutive month this year.

Manufacturer sales ranking. Image source: Passenger Association

In contrast, the market share of joint venture brands was further compressed. In October, the retail sales of mainstream joint venture brands was 700,000 units, a year-on-year decrease of 9% and a month-on-month decrease of 6%. Japanese brands saw the largest decline, down 3.7 percentage points year-on-year to 18.9%, while German and American retail shares fell by 0.1 percentage points and 1.7 percentage points, respectively.

Among the mainstream Japanese brands, only GAC Toyota maintained its growth momentum, with retail sales increasing by 45.4% year-on-year to 89,000 units. FAW Toyota fell by 3.2% year-on-year, Dongfeng Nissan fell by 9.7% year-on-year, and GAC Honda fell more sharply, down 28.3% year-on-year, and sales fell to 56,000 units.

The upward thrust of independent brands is closely related to the development of new energy vehicles. In the period of traditional fuel vehicles, there is still a big gap between independent brands and joint venture brands, but the development of new energy vehicles has given independent brands the opportunity to “overtake on curves”.

Zhu Huarong, chairman of Changan Automobile, bluntly stated at the recent 2022 China Auto Forum that in the traditional field, joint venture brands and independent brands are two levels that do not interfere with each other, while in the new energy field, more and more young users are beginning to choose independent brands. And the selection ratio hit a record high.

“It turns out that there is a 40% to 50% price difference between us and joint venture brands in the traditional field. In the new round of competition, through the blessing of new energy and intelligence, the price difference has quickly narrowed to 20%, 10%, and some premiums have even been Beyond the original joint venture brand.”

Data show that in October, the wholesale sales of new energy passenger vehicles reached 676,000 units, a year-on-year increase of 85.8% and a month-on-month increase of 0.4%. The wholesale penetration rate of new energy vehicle manufacturers exceeded 30%. Under the policy of halving the car purchase tax, new energy vehicles were not only not affected, but continued to improve more than expected.

Among them, the penetration rate of self-owned brand new energy vehicles is 47.7%; the penetration rate of new energy vehicles among luxury cars is 31.4%; while the penetration rate of mainstream joint venture brand new energy vehicles is only 4.7%.

Specifically, in the wholesale sales of new energy manufacturers in October, BYD ranked first with 217,500 units, Tesla China ranked second with 71,700 units, SAIC-GM-Wuling and Changan Automobile sold 520,800 units and 35.05% respectively. 10,000 vehicles.

In terms of new forces, the retail share of new forces accounted for 11.4% in October, a year-on-year decrease of 2.9 percentage points; the sales of new forces such as Nezha, Ideal, Leapmotor, and NIO were still relatively strong year-on-year and month-on-month, especially Nezha Auto 10 The monthly delivery volume reached 18,000 units, ranking first among the new car-making forces.

Among the mainstream joint venture brands, North and South Volkswagen has obvious advantages. The wholesale of 16,800 new energy vehicles accounts for 53.8% of the mainstream joint venture pure electric vehicles.

New energy vehicle retail sales rankings. Image source: Passenger Association

It is worth noting that the strong development of new energy vehicles has also begun to seize the market share of fuel vehicles, and the differentiation phenomenon of “ice and fire” was obvious in October.

Cui Dongshu, secretary general of the Passenger Federation, told Jiemian News that because the new energy vehicle market currently has the advantages of low taxation and low cost of use, consumers are more willing to buy new energy vehicles, and the market performs better than the fuel vehicle market. However, the fuel vehicle market is still facing the problem of insufficient purchasing power of consumers, and the general consumer groups are under great purchasing pressure.

Judging from recent sales data, the retail sales of conventional passenger vehicles (excluding new energy vehicles) nationwide in October was 1.28 million, down 8% year-on-year, reversing the positive growth trend of 6% year-on-year growth from June to September this year. From January to October, the retail sales of the conventional fuel vehicle market was 12.28 million, a year-on-year decrease of 13%.

Cui Dongshu said that the fuel vehicle market should continue to develop, which belongs to the needs of people’s livelihood models. New energy vehicles are an improved demand for replacement purchases. At present, the consumption demand of low-income and first-time buyers still needs to be released, and the policy should be more inclined to fuel vehicles. .

media coverage

interface

event tracking

- 2022-11-10 The market share of self-owned brands exceeded 50% in October, and the differentiation between new energy vehicles and fuel vehicles is obvious

- 2022-10-11 Passenger Association: Retail sales of new energy passenger vehicles in September reached 611,000 units, an increase of 82.9% year-on-year

- 2022-08-11The Passenger Federation announced that the sales of new energy vehicles in July increased by 123.7% year-on-year and decreased by 1.1% month -on-month

- 2022-08-09 Passenger Association: July sales of new energy vehicles reached 486,000, a year-on-year increase of 117.3%

- 2022-07-08 Passenger Association: Wholesale sales of new energy passenger vehicles reached 571,000 in June, a year-on-year increase of 141.4%

This article is reprinted from: https://readhub.cn/topic/8kNMRnbG3qw

This site is for inclusion only, and the copyright belongs to the original author.