Disclaimer: This article is only my thoughts and staged combing in my personal investment process. I am just an ordinary casual person. The opinions of the article may not be correct, and the investment level is also very average. The stocks or funds involved in the article may have the risk of a sharp decline , please maintain independent thinking, the market is risky, investment needs to be cautious, the opinions of the article are for communication only, and do not constitute any investment advice, readers and friends, please do not operate accordingly!

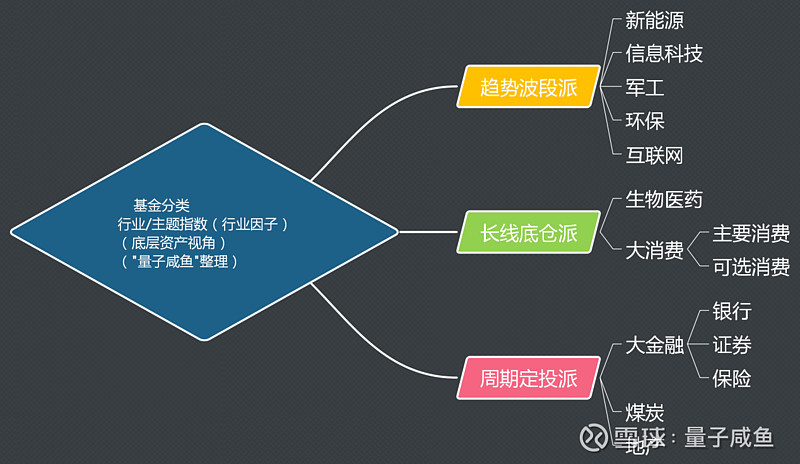

The subject positioning of this issue of the essay is very good. The industry index covers mainstream industries such as consumption, medicine, new energy, technology, military industry, big finance, and cycle. For the investment mentality of the industry index, I mainly use the “three major schools” rotation The allocation method, that is, the industry index/theme index is divided into three core investment method schools according to the industry attributes: the trend band group, the long-term bottom position group, and the cycle fixed investment group. For industry index funds, my point of view is mainly: most Each industry index has its own subdivision value. For different industry indexes, specific investment methods must be combined to achieve good results.

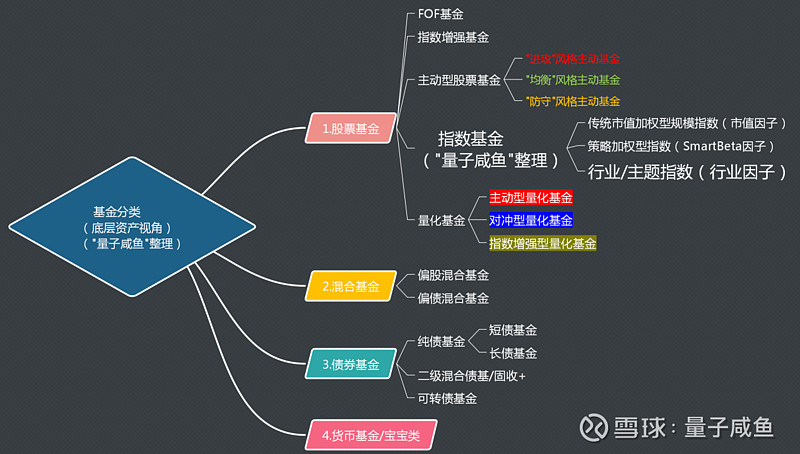

We have written many varieties in the “arsenal” of fund investors, such as FOF funds, stock active funds, fixed income funds, index funds, quantitative funds, index enhanced funds, hybrid funds, bond funds, etc. Before talking about industry index/theme funds, let’s revisit the fund classification based on the perspective of underlying assets:

It can be seen that industry index/theme funds are mainly classified into the “index fund” category of “stock funds” based on the nature of the underlying assets, and are mainly listed alongside traditional market value-weighted scale indexes and strategy-weighted indexes. The breakdown of the investment methods of the “Three Major Schools”:

The following is a specific introduction to the industry index investment mentality: the “three major schools” rotation allocation method:

I. Long-term bottom position pie:

The long-term bottom position group is relatively easy to understand. It is mainly aimed at “big consumption” and “big medicine”. Only sell when the overall index valuation is seriously overestimated. At other times, long-term holdings are used to obtain the long-term income of index constituent stock performance growth + dividends. The point setting can be higher, for example, when the index quantile point is higher than 90%, start selling in batches to avoid missing long-term position gains;

II. Trend band faction:

The trend band group mainly invests in the industry’s prosperity, and deploys when the industry’s prosperity begins to enter an upward inflection point, such as new energy, military industry, Internet, information technology, environmental protection industry, etc. It will be more difficult to grasp the inflection point of the industry’s prosperity. Of course, as a fund investor, you don’t need to earn every copper plate. This is the advantage of fund investors. When the bottom rises, it is often a sign of a wave of recovery in the industry. Investment in the trend band industry index needs to be sensitive to the valuation quantile of the industry index;

III. Periodic fixed investment distribution:

For the cyclical fixed investment group, the investment method is mainly aimed at strong cyclical industry indexes, such as banking, insurance, securities, real estate, and coal. For investment in such strong cyclical industry indexes, we must pay special attention to the margin of safety in valuation, and the industry has begun to enter a downward cycle. At that time, the market will fully price the downward performance expectations of the industry index, which is reflected in the absolute valuation bottom in the industry index valuation. For the industry index with periodic fixed investment, I usually only when the industry index valuation is at the absolute bottom (such as PB The valuation quantile point is below 10%. Note that it is generally safer to adopt a PB perspective for the valuation of strong cyclical industries. PE valuations tend to fluctuate inversely with the industry cycle.) Start to widen the price difference and slowly invest in batches. After the bullet is fired, the investment period for industries with strong cycles will be relatively long, so there must be sufficient compensation for investment odds. To invest in such industries with strong cycles, you must be prepared for a protracted war and control the absolute position ratio. When the cyclical fixed investment allocation industry index starts to reach the inflection point of the cycle, the valuation quantile point of the sold index must not be set too high, otherwise it will be easy to ride a roller coaster, for example, when the quantile point of the index is higher than 50%, it will be sold in batches;

In the industry index investment method: the “three major schools” rotation configuration method often uses index valuation quantile data. I personally recommend using historical data of the past 5-6 years. The time is too short and has no statistical significance. Time It is too long. If the industry valuation center moves with the industry life cycle, then it is meaningless to refer to its historical valuation data. The historical data of the past 5-6 years is a more appropriate perspective, of course, this is not absolute.

The subdivision value of industry index/theme funds is mainly reflected in the following three points:

a. Obtain the β income of the industry as a whole

Each industry will have its own industry attributes and business models. Compared with the broader market, the allocation of industry/theme indexes can obtain the beta fluctuation income of the industry as a whole, which is endowed by the track itself;

b. Obtain the alpha income of industry rotation

The phenomenon of industry style rotation in the big A market is also obvious, large cap/small cap, value/growth, strong cycle/weak cycle, core assets/small cap growth, etc., during the switching process of various market styles, if you can pass Industry/theme index to grasp this rhythm, you can get the α income of the industry rotation allocation;

c. Use industry index valuation fluctuations to obtain excess returns

In terms of index valuation, the large-cap broad-based index covers more industries and its constituent stocks are more dispersed. Therefore, for the large-cap broad-based index, large fluctuations in index valuation are relatively rare, unless extreme market conditions occur. However, the industry/theme index is affected by industry prosperity, market style preference, industry cyclical fluctuations, etc., and the valuation of the industry/theme index is more likely to fluctuate sharply. The management method can obtain excess returns on valuation fluctuations;

Let’s analyze the protagonists of this article in detail: Tianhong China Securities Agricultural Theme Index A (F010769) , China Merchants Shanghai Stock Exchange Consumption 80ETF Link (F217017) , E Fund China Securities Wonder Biotechnology Index (LOF) (F161122) , Tianhong China Securities Medicine 100A (F001550) , China Merchants China Securities Photovoltaic Industry Index A (F011966) , Tianhong China Securities New Energy Vehicle Index A (F011512) , Invesco Great Wall China Securities Technology Media Communication 150ETF Connection (F001361) , Penghua China Securities Information Technology Index (LOF )(F160626) , Wells Fargo CSI Industry 4.0 Index (F161031) , E Fund CSI Military Industry Index (LOF)A (F502003) , Bosera CSI All Index Securities Company Index (F160516) , Wells Fargo CSI Coal Index (F161032)

As mentioned earlier, for industry index funds, my point of view is that most industry indexes have their own subdivision value. For different industry indexes, specific investment methods must be combined to achieve good results.

Therefore, in the analysis process, I will mainly analyze the business model attributes of the industry, the development space of the industry, etc., and simply combine the industry/theme index with the “relative performance of the attributes of the sect” in the classification of the corresponding index investment “three sects” to analyze.

Analysis of the long-term bottom position industry index:

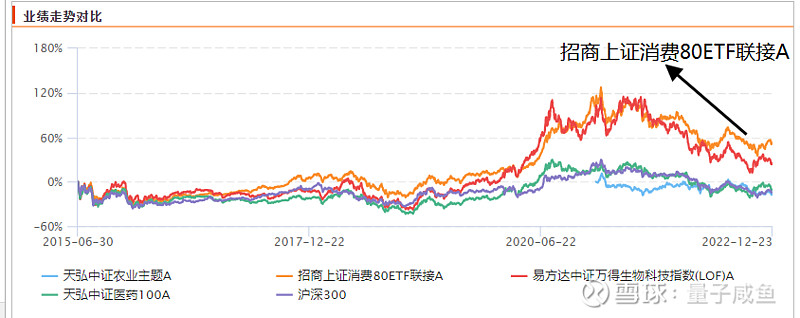

First look at the index trend performance:

Note: The content of the picture comes from choice

It can be seen that among the four long-term bottom position index, the one that can significantly outperform the Shanghai and Shenzhen 300 is the China Merchants Shanghai Stock Exchange Consumption 80ETF Link (F217017). From the perspective of the strength and weakness of the industry cycle, the cycle of the big consumer track is weaker than that of medicine , and large consumption will not be affected by the policy;

Annualized rate of return performance:

Note: The content of the picture comes from choice

It can be seen that although China Merchants Shanghai Stock Exchange Consumer 80ETF Connection (F217017) surpassed the Shanghai-Shenzhen 300 part reflected in the industry β income, but due to the impact of the epidemic in the past two years, the performance of the constituent stocks of the large consumer track has been under pressure. With the 2023 epidemic improvement, consumption recovery is expected to gradually strengthen;

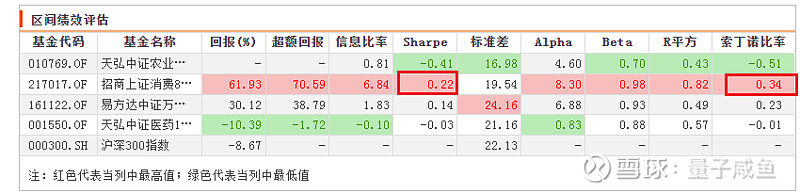

Excess return performance:

Note: The content of the picture comes from choice

The indicators for evaluating the excess return of funds are generally the Sharpe ratio and the Sordino ratio. I personally value the Sordino ratio more. Some children’s shoes may not know the Sharpe ratio and the Sordino ratio. Here is a brief introduction:

Sharpe ratio: Sharpe ratio = (annualized rate of return – risk-free interest rate) / portfolio annualized volatility = excess return / annualized volatility

The Sharpe ratio is meaningless by itself, only in comparison to other combinations

Sodino ratio: It is similar to the Sharpe ratio, the difference is that it does not use the standard deviation as the standard, but uses the decline deviation, that is, the degree to which the investment portfolio deviates from its average decline, to distinguish the quality of volatility. Therefore, when calculating volatility Instead of the standard deviation, it uses the downward standard deviation

Judging from Sodino’s data, China Merchants Shanghai Stock Exchange 80ETF Connection (F217017) is also the best performer among the four long-term bottom positions;

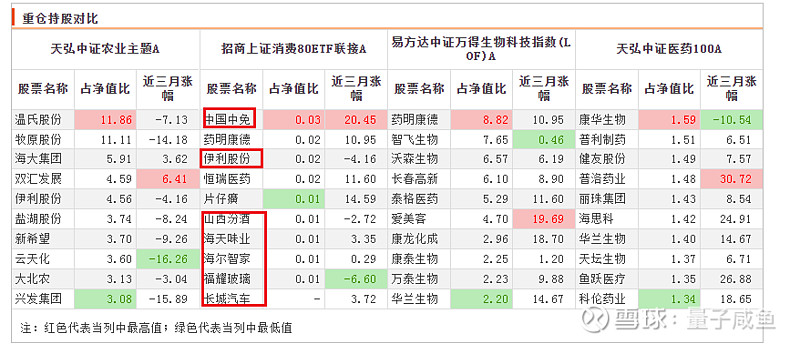

Top ten weight analysis:

Note: The content of the picture comes from choice

Judging from the allocation of the top ten weights, China Merchants Shanghai Consumption 80ETF Connection (F217017) allocates more consumer stocks in addition to pharmaceutical stocks. Compared with the other two pharmaceutical indexes, the cycle is weaker. For the Hongzhong Securities Agricultural Theme Index A (F010769) , the configuration of consumption segmentation tracks is more abundant, such as China Duty Free, which has a duty-free track, Yili shares, which has a food and beverage track, and Shanxi Fenjiu, which has a high-end liquor track. There are condiment tracks such as Haitian Flavor Industry, etc. Compared with pure agricultural and food stocks, the subdivision tracks covered in the big consumption track are more abundant, and the anti-cyclicality will be stronger;

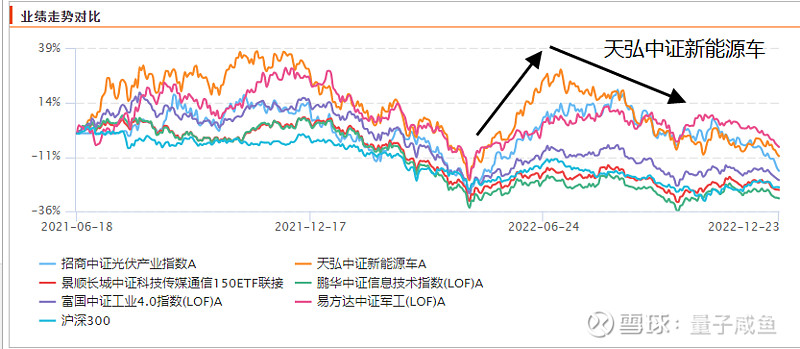

Trend band industry index analysis:

First look at the index trend performance:

Note: The content of the picture comes from choice

It can be seen that although the E Fund CSI Military Industry Index (LOF) A (F502003) has the best run in the range comparison, the investment window period of the military industry is shorter and the game is stronger, which is more suitable for most fund investors. It is difficult to grasp, but the Tianhong CSI New Energy Vehicle Index A (F011512) not only outperformed the performance of the Shanghai and Shenzhen 300 Index in the same period, but also showed stronger flexibility in the net worth curve, which is an attack in the trend band industry index Stronger, more in line with the temperament of the trend band industry index;

Excess return analysis:

Note: The content of the picture comes from choice

It can be seen that Tianhong CSI New Energy Vehicle Index A (F011512) is second only to E Fund CSI Military Industry Index in terms of excess returns. In addition, from the perspective of industry fundamentals, new energy vehicles are the future development direction. From a perspective, the new energy vehicle industry has more room for development. The military industry is subject to the influence of the military product pricing mechanism with low profit margins, and the market is more competitive. From the perspective of industry fundamentals, new energy vehicles are better than the industry in terms of industry space and growth. military industry;

Analysis of cyclical fixed investment industry index:

First of all, let’s look at the index trend performance:

Note: The content of the picture comes from choice

It can be seen that it is also a strong cyclical industry. The Fuguo CSI Coal Index (F161032) is more flexible than the Bosera CSI All-Share Securities Company Index (F160516). As I have written before, the investment method of the periodic fixed investment industry index is mainly in When the industry index valuation is at the absolute bottom (for example, the PB valuation quantile point is below 10%), the price difference will be widened and the investment will be made slowly in batches. The investment cycle for industries with strong cycles will be longer, so there must be sufficient investment odds. From the perspective of the performance of the securities industry and the coal industry, the return rate of the CSI Coal Index is stronger after entering the inflection point of the cycle, that is, the investment odds are higher. We can observe the PB valuation trend of the CSI Coal Index This cycle inflection point is observed to be consistent with PB valuations:

Note: The content of the picture comes from choice

It can be seen that the PB valuation trend of the CSI Coal Index is highly correlated with the trend of the CSI Coal Index, which once again shows that it is very effective to refer to the PB valuation quantile point for investment in highly cyclical industries, combined with the position management method of index fixed investment Good results can also be achieved;

Finally, to summarize:

For the investment mentality of the industry index, I mainly use the “three major schools” rotation configuration method, and divide the industry index/theme index according to the industry attributes:

Long-term bottom position allocation ( long-term positions to obtain long-term income from index constituent stock performance growth + dividends, and set a higher sell valuation quantile point )

Trend wave group ( combined with industry prosperity and overall industry valuation investment )

Periodic fixed investment group ( open the price difference at the absolute bottom of the valuation and slowly set the investment in batches, prepare for a protracted war and control the proportion of absolute positions, and the valuation points of the sold index cannot be set too high )

There are 3 core factions, and most industry indexes have their own subdivision value. For different industry indexes, specific investment methods must be combined to achieve good results. The subdivision value of the industry/theme index is mainly reflected in:

a. Obtain the β income of the industry as a whole;

b. Obtain the α income of industry rotation;

c. Obtain excess returns by utilizing industry index valuation fluctuations;

Among the 12 industry index funds analyzed in this article, China Merchants Shanghai Stock Exchange Consumption 80ETF Connection (F217017), Tianhong CSI New Energy Vehicle Index A (F011512) and Fuguo CSI Coal Index (F161032) are the “long-term bottom position group and trend band group” respectively. For fund investors, the “three major schools” rotation allocation method can be used as the investment mentality of the industry index, and the related style schools The combination of the index fund target and the corresponding investment method will have a better effect .

#老司基hard core evaluation# #雪球创作者中心# #工业基金怎么入#

@ China Merchants Fund @ Tianhong Index Fund @ Rich Country Fund

$China Merchants SSE Consumption 80ETF Connection(F217017)$ $Tianhong CSI New Energy Vehicle Index A(F011512)$ $Fuguo CSI Coal Index(F161032)$

There are 51 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/9600110938/238541019

This site is only for collection, and the copyright belongs to the original author.