Yesterday, Sungrow’s investor communication meeting announced that it would reduce the scale of energy storage and inverter shipments. Today caused a big drop and a big drop in the sector (especially the battery component and inverter sector), what should we think?

1. The installation cycle of the photovoltaic industry

【1】A common sense winter is generally the off-season for installations, which usually lasts from November to February of the following year (in the northern hemisphere).

There are several main reasons:

1. The construction conditions are not allowed. In the snowy weather, due to the many people wearing clothes, the construction slows down and the road is slippery;

2 In terms of yield, the sunshine in winter is about half of that in summer and autumn. The sunshine time is short and the power generation is low. That is to say, after the installation, the power generation income is lower than the average monthly amortization of the power station, which is actually a negative loss.

3. Under the dual effects of increased labor costs and reduced power generation revenue, the owner does not insist on installing the machine as soon as possible. (The following is the weather forecast for major cities in Europe)

【2】Why is there a rush to install in winter? Generally related to subsidy policies.

For example, China uses the year as the settlement unit. January is the start of the subsidy and December is the deadline, so only the Chinese market will see the “installation wave” in the fourth quarter. Similarly, Japan and some states and regions in the United States have subsidies in the past, but their scale is smaller than that of China, so they are not counted.

To some extent, my country has been rushing to install in December in the past few years, mainly due to policy factors, and rush to install as soon as possible. One aspect shows that although my country’s installed capacity is not much lower than that of foreign countries, it is enough to balance the short-term cost increase and income decline, and it can be equal to the subsidy. Another reason is the tradition of the Chinese New Year. In November and December, workers can get more overtime pay. Before the Spring Festival, it is the financial settlement time. Usually, after the installation is completed on December 30, the finance will pay wages, and the workers will return one after another. It’s Chinese New Year at home. Therefore, there are fewer domestic installed capacity in January and February every year, and the Energy Bureau also calculates the grid-connected capacity from January to February.

2. The impact of different global climates and installed capacity.

In the northern hemisphere, the installed capacity usually increases gradually from spring to autumn. This is due to the convergence of main statistical caliber fluctuations.

Taking 250GW in 2022 as an example, China will account for 1/3 of 60-80GW. Traditionally 20-30 in Europe (40-50 this year), 25-30 in the United States, 3-5 in Japan and South Korea, these account for 60% of the global installed capacity, and the basic climate is consistent, so they play a leading role in fluctuations in global installed capacity.

South Asia, Southeast Asia and the equatorial region. It is basically tropical, except for Uttar Pradesh, India, it can be installed all year round without any impact. In the southern hemisphere, mainly in Brazil, Argentina and Australia (a total of 30GW including transshipment), their installation period is from June to April of the following year.

Therefore, if there is no rush to install, the manufacturing cycle of photovoltaics should be more consistent with the installation cycle, maintaining a fluctuation of 40-60-70-50 in the first to fourth quarters. If they are relatively matched, the inventories of component factories and inverters remain at an average low level.

But starting from the second half of 2021, the cycle has been gradually disrupted.

3. The global photovoltaic manufacturing cycle is changing. The so-called operating rate no longer reflects the market heat.

Since 90% of the world’s photovoltaic products are located in China and Southeast Asia, and are basically influenced by the Chinese cultural circle, there will be an impact cycle of “Chinese New Year” stocking.

Stocking usually occurs during the European and American New Year cycle in November and the Spring Festival stocking cycle in January. Usually in November and January, the module manufacturing volume of the month will be exceeded by about 30-40%.

In 2021, LONGi will become the first, and various companies will continue to explore and learn from its model. Not only the integrated operation of the industrial chain, but also the rebuilding of the global marketing system.

1. Traditional model – production based on sales

In the past, the global trade of components basically adopted the order system, which is commonly known as “production based on sales” . The main structure of component order sources: 1. Centralized orders accounted for 60-80%; 2. Self-propelled component demand accounted for 20%; 3. Others (last order distribution) 10%.

In its model, the bulk is centralized, so the format and raw materials are basically fixed BOM. Due to the large quantity and relatively concentrated layout, it is possible to sign a long-term agreement with the supply chain and make a small profit. Self-built components are mainly orders from self-sustained power stations and long-term cooperative installation companies, mainly for centralized ones, and more orders are made, and they are the main source of gross profit. The last order is mainly to deal with low-efficiency and slightly problematic components for the purpose of cost recovery.

Due to the high degree of matching between orders and manufacturing, the supply chain is basically matched according to this model. For example, this month’s industry-wide orders are 10GW. Generally, materials and other companies can maintain more than 90% of their production, and the total design output will not exceed 12GW/month. Basically, it will be close to full production and sales, and the gross profit will also be relatively stable.

2. Supply chain leverage model

LONGi, Jinko, etc. are the templates, and in 2020, they will start to realize the “leverage model of the supply chain”, that is, in certain cycles, more components or raw materials will be produced, which will break the balance model of the supply chain in the past. Through the method of purchasing more raw materials at low prices (commonly known as “stocking”), the cycle will be retrograde and the cost will be reduced, thereby improving the competitiveness of components. At the same time, because the cycle of raw materials is broken, there will be shortages of raw materials, resulting in uneven procurement in the industry. Rising prices and partial shortages have further strengthened the competitiveness brought about by hoarding goods.

Photovoltaic glass triggered in the past, silicon material, quartz sand, and even adhesive films and particles this year are all affected by this strategy. Of course, the resilience of each industry is different, so although the strategy is the same every time, the direction and results are different.

glass , triggering switching from single to double glass. In the short term, the increase in double glass is too fast, and a long-term price reduction agreement was signed, which increased the price of glass from 22 yuan to 48 yuan per square meter. Under the inquiry of relevant departments, the production of glass has been expanded crazily, so that the price per square meter has exploded to 19 yuan this year. The previously promised payback cycle and the huge profits have all evaporated

The same is true for silicon materials at the beginning, but the production capacity of silicon materials is slow to climb, coupled with the concentration of the industry, and new external forces disrupt the situation, basically getting silicon materials out of control. Although LONGi Zhonghuan has lowered its purchases several times, it has not been able to lower the price of polysilicon. Simply starting to sign long-term agreements this year, further pushing up, triggering “mutual harm” in the entire industry. Judging from the results, the profit of the component factory has continued to increase, which has overwhelmed the power station. It’s hard to say how it will end.

Quartz sand , despite many analysts touting a shortage of quartz sand. But from a practical point of view, there is no shortage. Quartz sand has been gradually replaced by localization, especially at the annual meeting of the photovoltaic industry in Chuzhou, a large factory began to use 30% foreign materials and 70% domestic materials. It can be seen that if there is enough pressure, there will be enough motivation for technology development. ![]() too fierce

too fierce

Film and particles , the pre-hype is the shortage of EVA film, but Shenghong and Levima Shinco have begun to expand production, and at the same time Sinochem, Sinopec, etc. have participated. The huge production capacity has been released in the third quarter, and there will be no shortage by next year. . The shortage of POE that is being hyped now is to hype Wanhua Chemical and Xiangbang Technology, which is about to go public. The standpoint is that N-type components require pure POE packaging. At this conference, several component factories in the TOPCon camp announced to start using EPE packaging to reduce the bottleneck caused by insufficient POE capacity. The HJT camp also began to use EPE packaging in the second quarter of this year, gradually reducing the proportion of pure POE used. It can be seen that if there is enough pressure, there will be enough motivation for technology development. ![]() Too fierce +2

Too fierce +2

The above lists only a few well-known examples. In fact, brokers have already made a lot of money through rounds of speculation. They can obtain priority research information, buy at low prices before the stock price takes off, and then brainwash through the secondary market, cooperate with a group of brainless analysts to hype, and then gradually leave the market at high positions, earning huge profits. Only the leeks standing guard in high positions are left. ![]()

Therefore, I often say that a lot of basic knowledge comes from basic analysis. Don’t listen to external “noises” completely. No one will shout at you to make money. Selling must have a purpose, not to mention that they all have a lot of cost.

Back to the topic, since supply chain management comes first, what impact will it bring?

1. First of all, for the enterprises themselves, because they hope to make more components in the low-cost cycle, their marketing structure will change from centralized dependence to other aspects. That is, a new round of “sales based on production”.

That is to say, the company prepares a large amount of funds, prepares goods and raw materials, and mass-produces within a certain period.

Take this as an example. For example, in a normal cycle, a module factory can produce according to market demand, that is to say, the modules are basically produced last month, so the inventory cycle is short, and the longest period will not be broken. Its own receivables and payables basically maintain an equal ratio. The cost of raw materials and half of the inventory is basically maintained under its own 30-day turnover cycle.

For cross-cycle production, it is to first determine the matching degree of factory production capacity and raw materials. In the off-season, more components are produced and more materials are purchased, so the cost is lower. When the peak season is approaching, under the condition of limited production capacity, we can achieve more shipments, so as to earn higher profits than our peers. How did you discover this strategy? It can be found from the increase in inventory, the capital turnover cycle, and the prolonged cash retention time. This is one of the reasons why tens of billions of inventory is pending.

We can see that integrated companies such as Longi, Jinko, Trina, and JA Solar are gradually playing this strategy. Other companies are following up with their own financing capabilities. The sharp recovery in profits of component and cell companies this year is due to the huge role played by supply chain leverage.

It should be added that leading companies can obtain huge cash flow by exporting silicon wafers and other products. This is also the reason why this “leverage” dares to play so big. However, the problem this year is that silicon materials continue to rise. As a raw material for silicon wafers, the capital occupation is large and cash is limited. Therefore, the stockpiling in the early stage cannot cover the price increase after the grouping of silicon materials in the later stage. This is why this strategy “play” got out of hand this year.

Brokerage companies often provide so-called module operating rate forecasts, silicon materials, and cell operating rate forecasts. This year, there is no time when it is lower than 80%. And our total module production capacity this year is 400-450GW, and the 8 achievement is 360GW. According to the general consensus this year, the module manufacturing volume is around 250GW, so the total operating rate should be 50-60%.

How do you compile the operating rate of your brokerage firm? unknown.

4. Significant changes in the component marketing model.

Starting in 2020, front warehouses have been set up all over the world. Mainly used for channel distribution. Channels are divided into two concepts, two different groups.

One is self-built , such as setting up a subsidiary overseas, so that the sales company can purchase the products of the manufacturing company and put them in the overseas front warehouse, and then the sales company will sell them in the region according to the volume of goods.

The second category is dealers , especially in the distributed field, there are basically secondary dealers. There is a slight difference between domestic and foreign countries. Most of the domestic dealers sell to the regions where the installation is distributed. The third-tier distributors are stores and projects, usually packaged and sold cables, inverters and other products for the purpose of installation. Foreign distribution and engineering exist at the same time, because the power station development systems in Europe, America and Japan are relatively complete, so there will be more of the latter, basically how many components are purchased in the early stage for installation. (Larger companies have a strong voice) The main profit of dealers comes from the rebates brought by hoarding goods. For example, if they sell 50 million this year, the rebate is 1 million. According to the total amount.

This year, due to the impact of the Russo-Ukraine war, individuals and businesses have become the main installation force. Consumers are more inclined to see the real thing for negotiation. Therefore, the proportion of dealers opening new stores and small warehouses in the region has increased significantly. This year, the inventory in China, Southeast Asia, the United States, and Europe has soared.

In the past, power station factories and installation companies were the main force for importing components from Europe, America and Japan, basically B2B business. Beginning in 2020, the module factory’s own circulation began to gradually increase, that is, subsidiaries and distributors purchased more modules. In this way, the ” pre-determined ” sales performance in the financial report is realized, and the shipment data is particularly good-looking in the quarterly report.

Here is an answer to the previous question about Sungrow’s reduction in shipments: As mentioned earlier, there has been a burst of warehouses in Europe. Due to the slowdown of local installation progress, the inventory of distribution warehouses remains high. There have been cases where Chinese goods cannot be sent to Europe. It can only be recovered after the inventory is consumed next year. Inverters and energy storage equipment have been exported more in the early stage, so it is reasonable to lower the expectation.

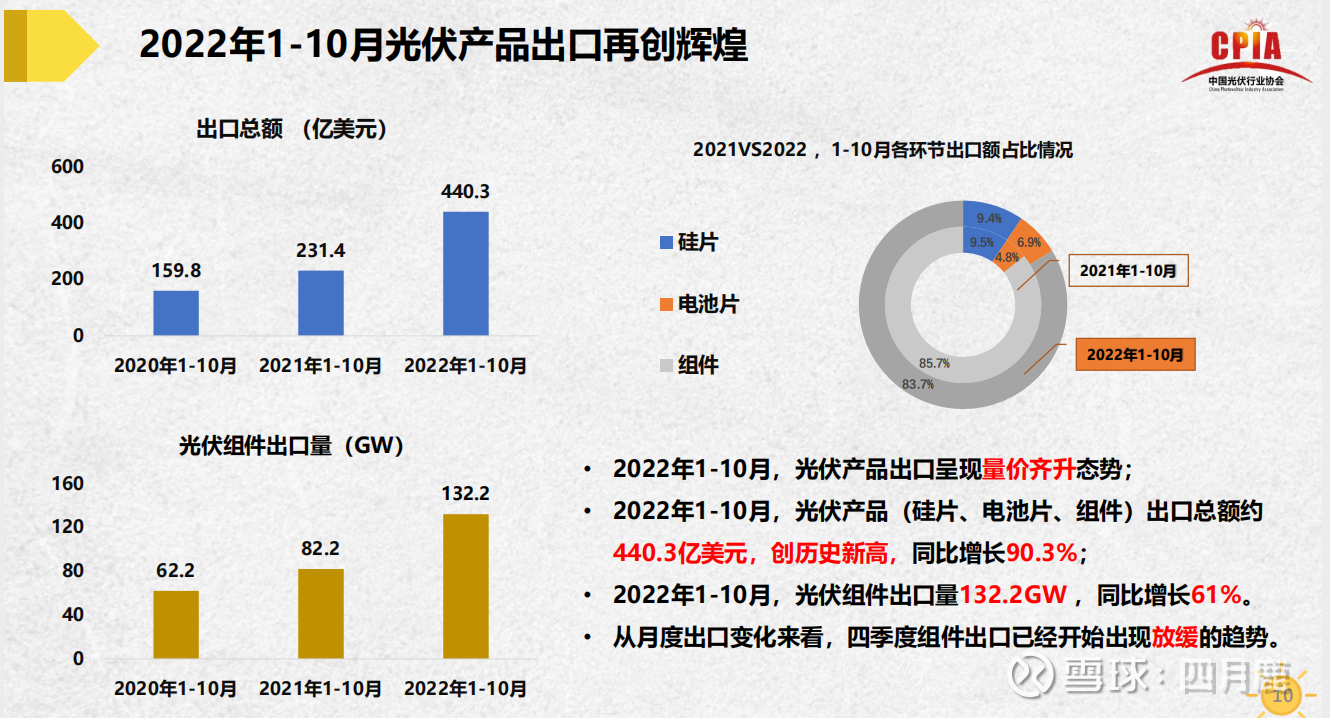

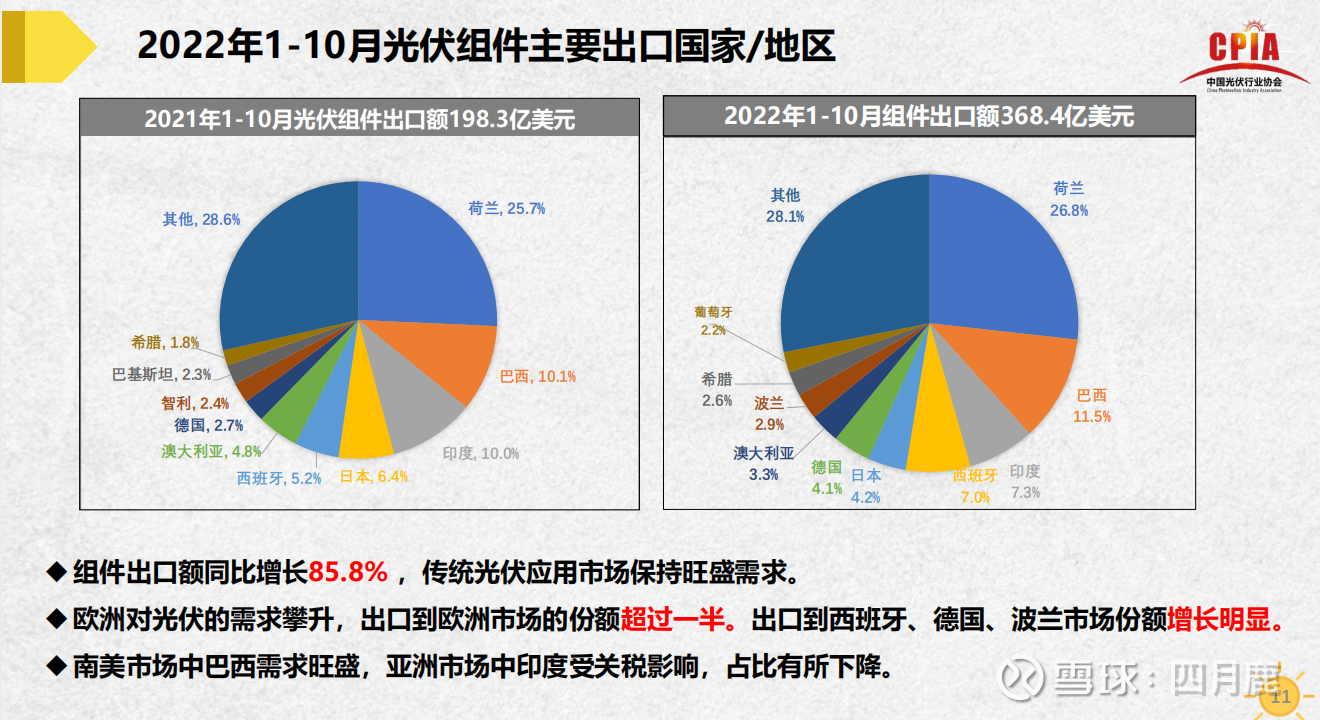

The above is the data of the annual meeting of the Photovoltaic Industry Association. As the world’s largest photovoltaic module transfer base, the Netherlands still ranks first. Followed by Brazil, as an important transit port in North and South America.

Regarding the issue of the Russia-Ukraine war, Macron began to mediate everywhere in early December, hoping that the war would end as soon as possible. I agree with Mr. Cao that if the war subsides sooner, then in the process of economic recovery, the chances of new energy installations will further increase instead of decline. After all, this war has made the world realize how important energy independence is.

Regarding energy storage, Mr. Cao introduced the situation of the energy storage market at the Chuzhou meeting. The analysis and hype of external capital is very enthusiastic, but the current status of energy storage is not optimistic. First of all, domestic energy storage has become a “shackle” for new energy development. Judging from this year’s energy storage, the actual utilization rate of energy storage is extremely low, even less than 10%. More than 90% of energy storage is idle, and the cost makes power stations corporate burden. The local government and the power grid did not follow the regulations to “receive all the electricity due to energy storage” at night, and the investment income of the power station was greatly discounted. Foreign energy storage is centralized and reverse storage at the same time. Due to the large area and sparse population, single household and single network, and time-sharing electricity price, the utilization rate is relatively high.

Since many of the 60+GW installed capacity in China are energy storage imposed by various provinces in the form of mandatory orders, it is more difficult to carry out centralized development, and many projects have been scrapped this year. In November, news broke out that wind power and photovoltaic power plants were gradually rebuilt and abandoned (no one has gold and silver mountains, and they cannot stand endless speculation). Therefore, the expected space for energy storage is large, and the difficulty of actual implementation is also a problem on the table. It may not be as good as brokerage stocks.

The [ Photovoltaic Competition ] series is my summary of some phased views on the competition between major component companies and leading companies in the sector. All are exclusively published on Snowball, welcome to reprint, please indicate “Snowball-April Deer”, thank you. @Today’s topic

$Sungrow(SZ300274)$ $LONGi Green Energy(SH601012)$ $Tongwei(SH600438)$

The original plan to write the 23rd article of the photovoltaic competition is based on the perception of this trip to Chuzhou. This year, the content of answering the sharp drop of Sungrow Power Supply is temporarily added, and the 24th article will be released this week.

There are 12 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/6322022770/237068228

This site is only for collection, and the copyright belongs to the original author.