In real life, when you buy a fund in a bank, you find that the sales manager always strongly recommends newly issued funds and avoids talking about the existing funds. Why is this? Now let me talk about whether you should buy a new fund or an old fund.

The difference between the new fund and the old fund fee

Fund fees mainly include: subscription/subscription fee, management fee, custody fee and redemption fee.

During the subscription period of a new fund, there will generally be a subscription fee of 1-1.2%, and there is usually no discount. This fee fund company usually returns 100% to the sales channel.

When purchasing old funds, there is generally a subscription fee of 1.2-1.5%, and this fee is generally returned to the sales channel. However, due to competition factors, the subscription fee for old funds is usually discounted (10% discount for channels such as Egg Roll Fund, Tiantian Fund, Alipay, etc., and there are few discounts for banks and other channels, so it is generally not recommended to purchase funds directly from banks ), so the actual The discounted income of selling old funds is far less than that of selling new funds.

(The following is an example of Zhongtai Xingyuan’s flexible configuration of mixed A, and the rate comparison between a bank and an egg roll fund)

In addition to the subscription/subscription fee, the fund will also charge a 1-1.5%/year fund management fee, which is the main source of income for the fund company. Fund companies hope that customers will continue to hold the fund for a long time. In order to deeply bind with the interests of the channel, part of the management fee will be returned to the channel as a “trailing commission”, especially for new funds, the trailing commission ratio can reach 40-70%.

In today’s financial supermarket model, the sales channel is the strong party. Compared with selling old funds, not only is the trailing commission ratio low, the subscription fee is only 0.12-0.15% after discount; selling new funds is definitely more cost-effective, not only earning 40-70% trailing commission, the subscription fee of 1.2% is usually not discounted, so It’s no surprise that money managers are keen to market new funds.

From an investment point of view, which one is better for new and old funds?

In addition to the difference in fees, from an investment perspective, the new and old funds have the following differences:

1. Liquidity

New funds generally have a closed period of about 3-6 months, and cannot be sold during the closed period.

2. Transparency

The new fund will not announce its holdings during the closing period, so you don’t know what the manager will buy.

3. Position level

New funds generally build positions slowly within 6 months, and will gradually increase from 0 to 80-90% of the stock position. If the stock market rises during this period, the slow opening of the new fund will not catch up with the old fund’s rise. Of course, you would say that if the stock market falls and the new fund slowly builds a position, wouldn’t the loss be lower than the old fund? It does. But if the market is bad, why would you want to buy a fund all at once? Wouldn’t it be better to go short or make a fixed investment? (The new fund cannot be invested during the closed period)

4. Fund NAV

Some investors mistakenly believe that the net value of the new fund is 1, which is very cheap, so they are more inclined to buy the new fund. There is a big trap here, is the fund undervalued or overvalued? It does not depend on the size of the net worth of the fund. It does not mean that it is overvalued if it is worth three yuan, and it is undervalued if the net worth is more than one yuan. Net worth is just an accounting method, and the fund’s profit depends on the growth rate of net worth, not the absolute value of net worth.

5. Asset allocation

A very important principle of our investment is to achieve our own return expectations while matching our risk level. This requires good asset allocation, at least diversification of value and growth, large and small caps. However, when channels recommend new funds, they often focus on recommending the background and past performance of fund managers, or highlight current popular tracks, while ignoring other needs of customers. As for old funds, we can analyze their positions and styles, and choose different funds to make plans for decentralized allocation and investment ratios.

Is it right or wrong to “buy Laoji in a bull market and buy a new base in a bear market” when investing

There is a saying, “buy old bases in bull markets, new bases in bear markets”, and there is a certain truth to it. The old funds in the bull market are all running with high positions or full positions, which can maximize the dividends of the rise; while the new funds have a closed period. In the bear market, the proportion of losses can be reduced by adding positions step by step, and at the same time, it can avoid short-term sales by customers. , to reduce losses.

However, A-share bulls are short and bears are long, and the closed period of 3-6 months will generally not pass the bear market cycle. Like this bear market that has continued from 2021 to 2022, what is the use of such a short closing period? Will the cutting be more aggressive after the closed period ends?

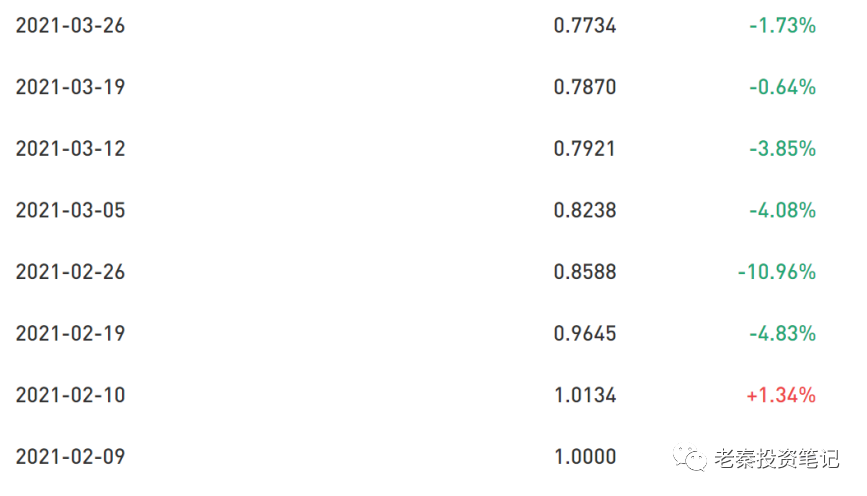

For example, Hui’an Balanced Preferred Hybrid Fund was established on February 9, 2021. It was too impatient to open positions. The net value on February 26 was 0.8588, down 14.12% in 9 trading days and 23% in one and a half months. The new fund cannot be sold during the opening period. Can you sleep well?

There is a saying in the fund marketing circle: a new foundation is created in a bull market, and a bear market is presumed to invest.

Investing is inhumane. Only the bull market has more new users, and the enthusiasm for buying cannot be stopped. Every bull market is a good time for fund companies to vigorously issue new funds. Especially for some relatively low-ranking fund companies, it is a good opportunity to overtake in the corner. If you seize it, the ranking can rise rapidly and bring more income.

Moreover, new funds often choose the current popular track, and short-term performance is more likely to attract attention. But it is a pity that after each round of the bull market, the Christians who are hurt by the new fund issued by the vertex are all chicken feathers.

Conclusion: For most people, it is better to buy old funds, at least according to past performance, ranking, style of fund managers, etc., to choose a variety that suits them. For new funds, long-term closed-end funds are more recommended, to avoid being unable to hold due to personal mentality. After all, most funds can achieve positive returns in the long run.

My real portfolio:

The opinions mentioned in this article only represent personal opinions, and the subject matter involved is not recommended. Buy and sell according to this at your own risk. If you feel that you have gained something, please like and retweet!

#The net value of the new fund has fallen by 20% after the rapid opening of the position# @雪ball creator center @today’s topic

This topic has 4 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8138265855/232097931

This site is for inclusion only, and the copyright belongs to the original author.