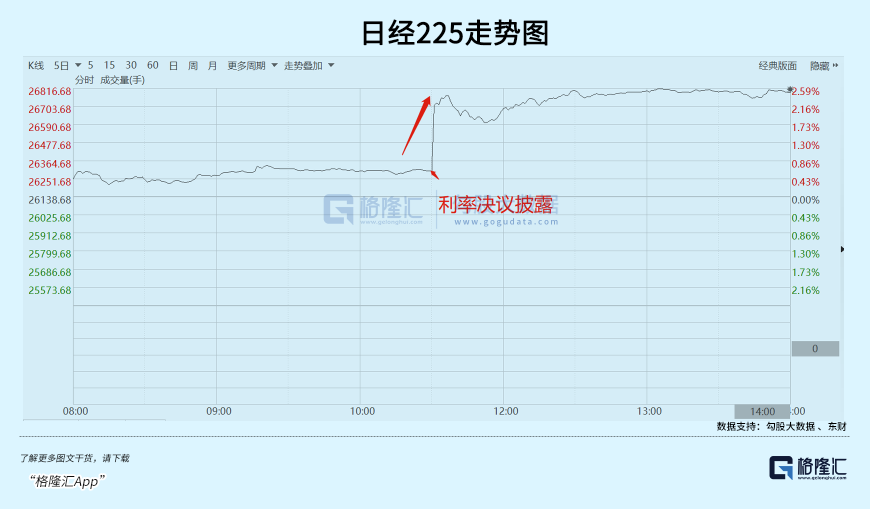

At about 10:30 am on January 18, the Bank of Japan announced the latest interest rate decision.

The result was quite unexpected. The Bank of Japan passed the interest rate decision with a 9:0 vote, keeping the benchmark interest rate at a historical low of -0.1%, unanimously passed the yield curve control (YCC) decision, and kept the 10-year government bond yield target at around 0%. Continue to allow the 10-year Treasury yield to fluctuate within a range of about 50 basis points above and below the target level.

This caused a “false alarm” in the global financial market, neither raising the YCC by 25 basis points as the market had previously feared, nor abandoning the YCC framework.

The Bank of Japan held its fire and boosted risk appetite for global assets. The Nikkei 225 jumped 2%, and the yen quickly depreciated from 128.4 to 131 against the US dollar, a drop of more than 2%. At the same time, the 10-year U.S. bond yield fell sharply by 2%, and the three major U.S. index futures briefly rose rapidly.

If you look at the time a little longer, the gray rhinoceros in Japan has not lifted the threat to the world.

The Mystery of Monetary Policy

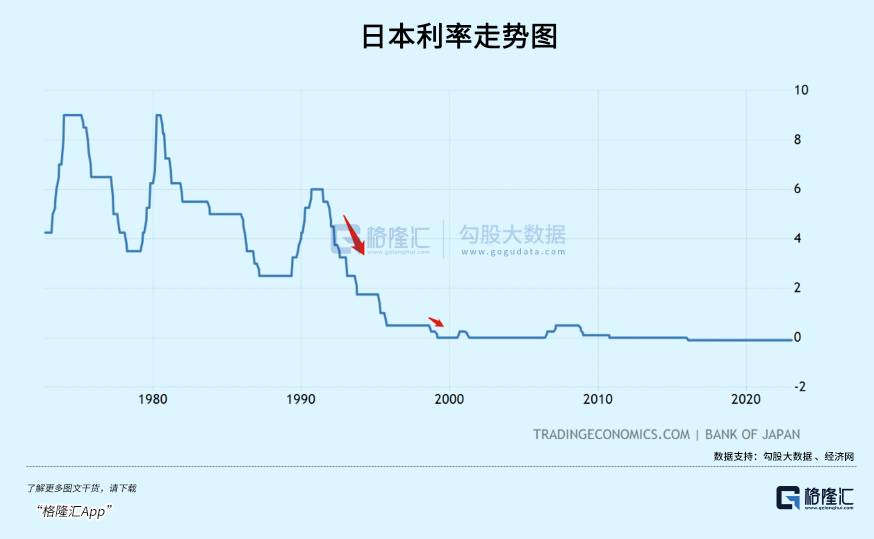

In 1988, the Federal Reserve raised interest rates very accurately and sharply, which finally burst the bubble in the Japanese stock market and property market, and reaped huge wealth in Japan. Since then, Japan has sharply cut interest rates to stimulate the economy, but the economy has not improved and has been in a slump.

In 1997, the financial crisis swept across Asia, and the Japanese economy was hit hard again. In the second year, Japan took the lead in entering the era of zero interest rates. Since then, Japan has not raised interest rates for more than 20 years, except for a small increase in 2007.

In 2008, the subprime mortgage crisis broke out, which did great harm to Japan. The effectiveness of the past QE policy is no longer enough to face the real dilemma. In 2012, Abe came to power, and Abenomics was born—three arrows plan, including quantitative easing policy, expanding fiscal expenditure, and structural reform.

In 2013, the Bank of Japan practiced Abenomics and officially launched the Quantitative and Qualitative Easing Policy (QQE), announcing that Japan has entered an indefinite, open-ended ultra-loose policy period.

The biggest difference between QQE and QE is that in addition to buying corporate bonds such as government bonds and real estate mortgage bonds, Japan also directly buys Japanese stocks. QQE releases base currency of up to 80 trillion yen per year.

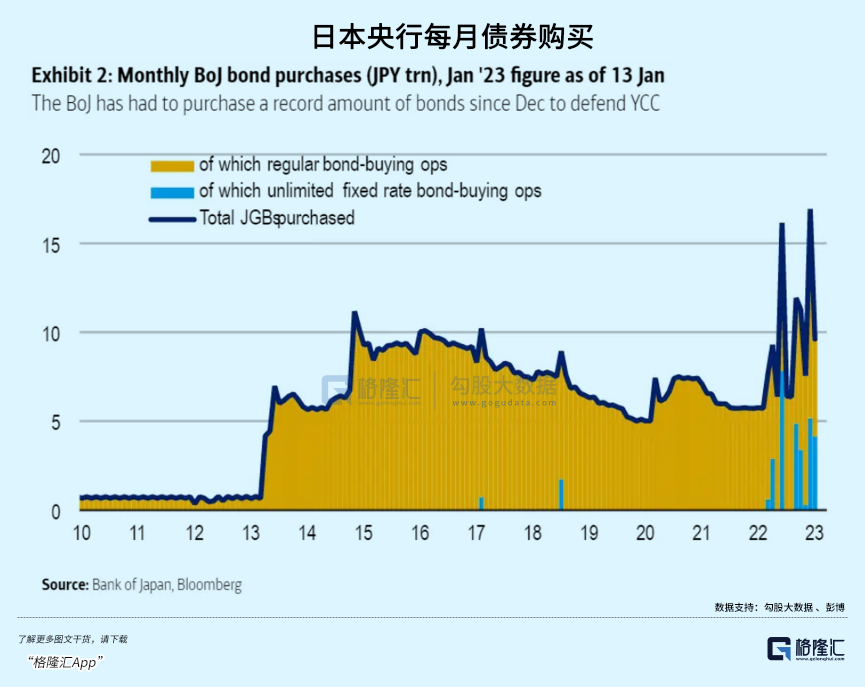

The Bank of Japan bought and bought all the way, and became the largest shareholder in the Japanese stock market and national debt market. As of November 2020, the Bank of Japan has a market value of 45.1 trillion yen in stocks, officially surpassing the 44.8 trillion yen in government pensions. In the government bond market, the Bank of Japan holds more than 50% of the shares. In October 2022, a large-scale purchase of national debt will be made, and 70% of the share will be in the bag.

Japan insists on loosening and not relaxing, and has practiced the MTT currency debt theory all the way. In September 2016, the new QQE policy was released, which mainly consists of two parts – Yield Curve Control (YCC), which adjusts the short-term and long-term; the second part is the commitment to overshoot inflation, which promises to expand the base currency level until it exceeds 2%. Target, and stable above 2%. This monetary policy has continued to this day.

The most important prerequisite for the QQE policy to continue to play is that inflation cannot get out of control. This is the same risk as the QE policies practiced by the Federal Reserve and the European Central Bank.

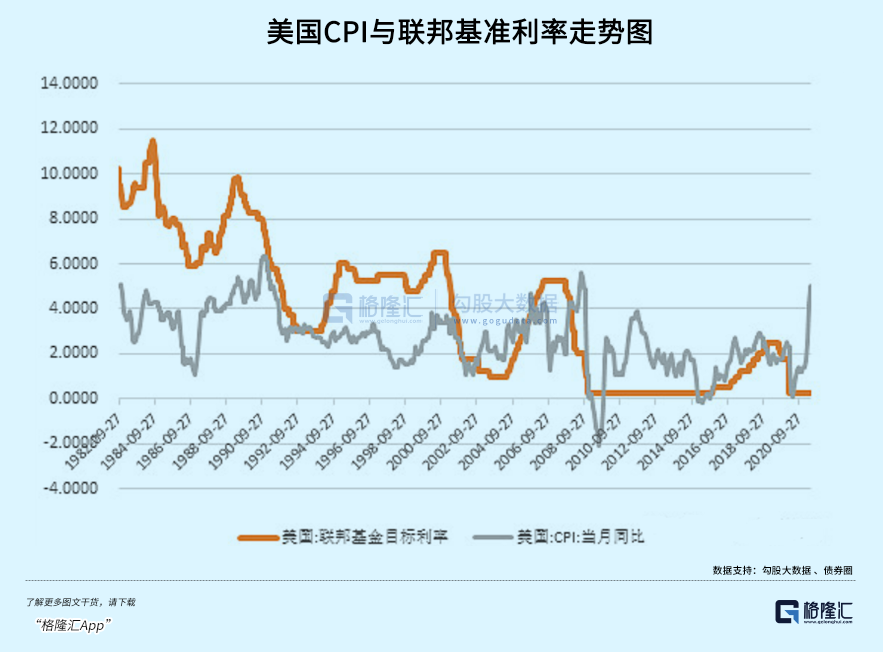

But now Japan’s inflation is getting out of control. In December 2022, the CPI excluding fresh food in Tokyo’s 23 districts rose by 4% year-on-year, exceeding market expectations of 3.8%. This has been the seventh consecutive month that Tokyo has exceeded the Bank of Japan’s 2% target, while Tokyo’s average CPI in the past year was 2.2%, the highest level in 30 years. The Jingdong price index is a leading indicator of Japan’s national CPI, and Japan’s overall CPI reached 3.8% in November last year, a 41-year high.

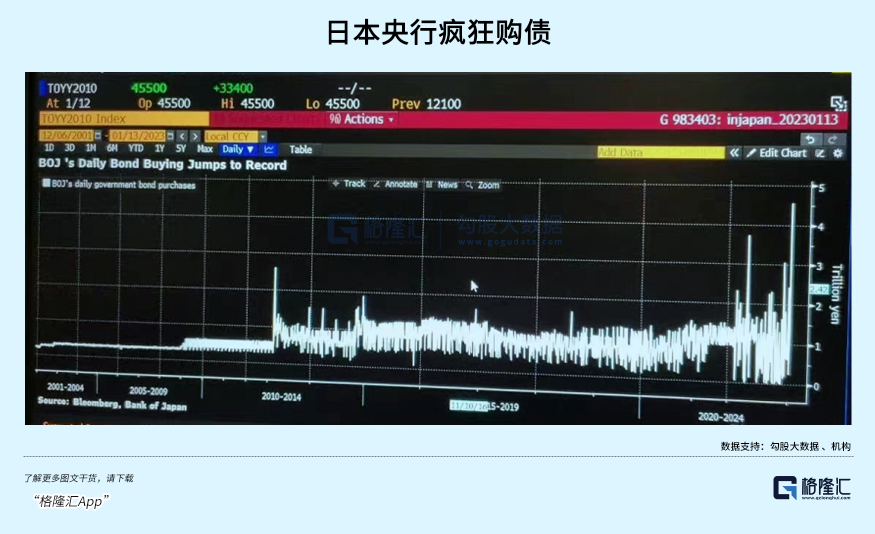

In addition, the Bank of Japan’s crazy bond purchases have crazily suppressed the endogenous momentum of rising interest rates in the market, completely distorting the national bond market.

In the first 15 days of 2023, the Bank of Japan held 53% of the entire government bond market, a rapid increase of 1% from the end of last year. If this crazy behavior continues, it will only take 33 weeks before the Bank of Japan will have no bond purchases to buy, and the entire market will take it into its pocket. The problem of liquidity depletion has also become more prominent. In October last year, there was a rare scene of zero transactions for three consecutive trading days, and the market function became more and more dysfunctional. It is important to know that Japan is the second largest sovereign debt market in the world.

The monetary policy of the Bank of Japan seems to have reached the point where everything must be reversed. On December 20, the Bank of Japan adjusted the YCC target from ±0.25% to ±0.5%, raising interest rates by 25 basis points in disguise, which shocked the global market.

Today, the Bank of Japan kept its policy unchanged, but it does not mean that the next monetary meeting will not take action. Bank of Japan Governor Haruhiko Kuroda is about to step down from March to April this year, and the market is also worried that the new governor will start the process of normalizing Japan’s monetary policy.

Extremes must be reversed

In the more than 20 years before 2020, Japan has released such a large amount of currency, why has there not been a deep and long-term depreciation of the yen exchange rate?

In my opinion, in addition to the substantial release of overseas mainstream currencies, an important factor for the relative stability of the yen exchange rate is that Japan has a huge amount of net assets overseas.

In the past few decades, globalization has been deeply integrated, and the global economy has maintained a good momentum of long-term growth. Although there were crises such as those in 2001 and 2008, they did not damage the core growth momentum. Whether it is the official government or private enterprises and individuals in Japan, they use the extremely cheap domestic yen to continue to increase investment overseas, earn a steady stream of profits, and return them to Japan, which supports the yen exchange market to a considerable extent.

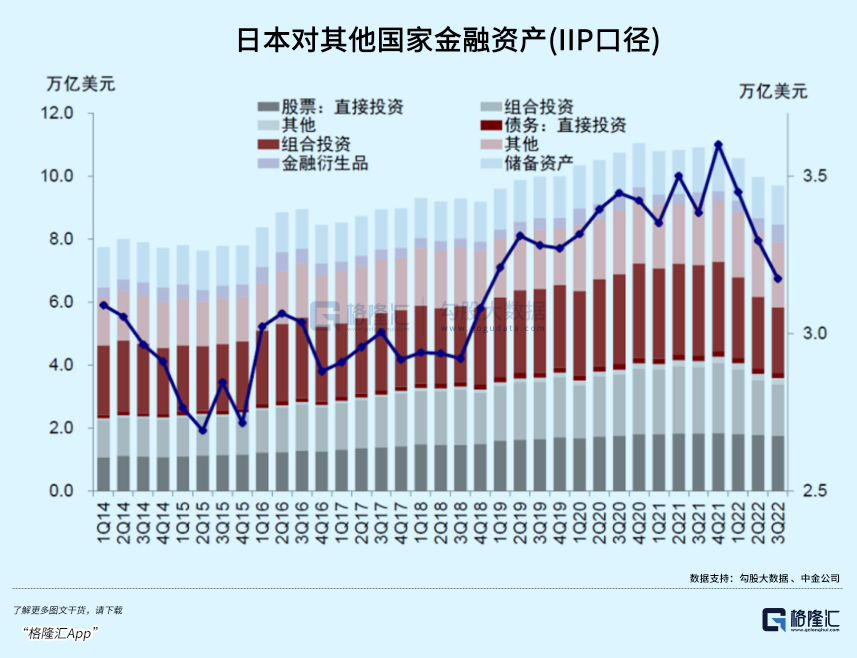

Japan has been the world’s largest creditor country for 30 consecutive years. As of the end of 2020, the balance of overseas assets owned by the Japanese government, enterprises, and individuals has increased by 5.1% compared with the end of 2019, reaching 67.35 trillion yuan, setting a new record for 9 consecutive years. Among them, the balance of direct investment increased by 0.9%, to 12.1 trillion yuan, accounting for 18% of the total foreign investment. It can be seen that in 2020, when the new crown is raging, Japanese companies’ investment activities such as overseas mergers and acquisitions are still growing.

As of the end of June 2022, Japan’s net international investment position—the difference between its stock of assets held abroad and the stock of Japanese assets held by foreigners—was $3.29 trillion. This scale is equivalent to 2/3 of Japan’s 2021 GDP ($4.93 trillion). This is the biggest background of Japan’s economic development model and the maintenance of QE policy.

However, the outbreak of the new crown epidemic and the outbreak of the Russia-Ukraine war have interrupted the backbone of the global economy’s good growth momentum. In particular, the war has become regionalized and two camps have been formed, which has greatly accelerated the speed of the reversal of globalization.

From 2020 to 2022, the exchange rate of the yen against the US dollar plummeted from the lowest of 101 to 151.9, a deep depreciation of 50%. Such an exaggeration, in addition to the similarities and differences in the monetary policies of Japan and the United States, there is also an underlying logic that the Japanese economy’s model of relying on overseas investment to feed back the country has been reversed, accelerating the depreciation of the exchange rate.

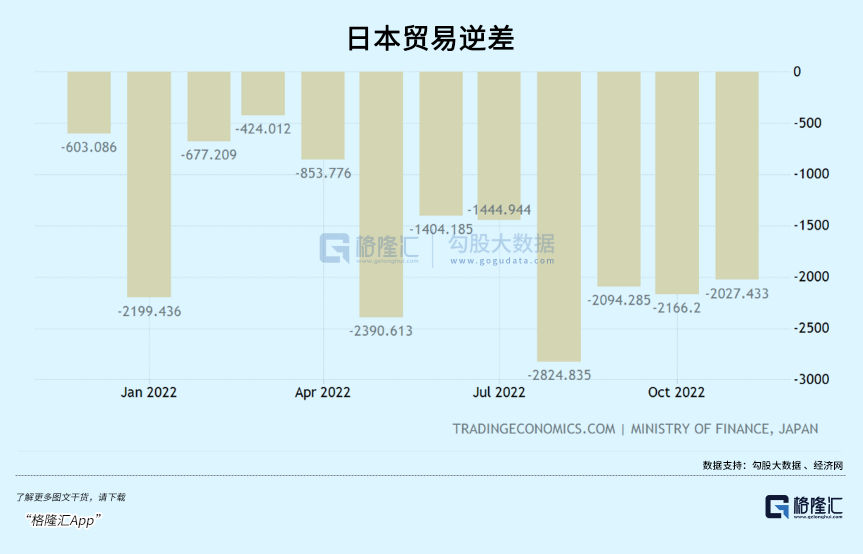

The yen depreciated sharply, and the price was extremely tragic. Japan’s economy is extremely dependent on foreign trade, and now this carriage has deteriorated severely. From June 2021, Japan will have a trade deficit for 16 consecutive months. In November last year, the deficit hit a new high in November since 1979, when comparable data was available. The deterioration of foreign trade impacted the Japanese economy.

Second, the sharp depreciation of the yen has brought about huge imported inflationary pressures from raw material imports. At present, Japan’s inflation has hit a 41-year high, far exceeding the Bank of Japan’s 2% policy target. But now the Bank of Japan continues to maintain an extremely loose monetary policy, and inflation is heading out of control.

In addition, there is a global macro background – inflation is easy to rise, but difficult to come down. From 1970 to 1980, the world experienced hyperinflation for more than 10 years. Later, Volcker raised interest rates frantically to 19.1% before he began to tame inflation. From 1980 to 2000, the federal benchmark interest rate was higher than the CPI for a long time, which finally solved the problem of inflation. Now, whether it is the United States or Europe, inflation has fallen, but then there may be a dive like in 1970. After monetary easing, high inflation returned.

Global inflation may not be temporary, and it will face a structured and long-term high situation. The underlying logic is that deglobalization is intensifying, supply chain reorganization, trade regionalization, and currency diversification lead to higher transaction costs and lower productivity.

The 2% global inflation in the past was based on cheap energy led by Russia and cheap manufactured goods led by China. In the future, as the world moves towards deglobalization, it may be a luxury to return to maintaining 2% inflation for a long time.

Whether it is the pressure of high inflation, exchange rate depreciation, and bond market distortion in the short to medium term, or the pressure of global inflation and structurally high interest rates in the medium and long term, the Bank of Japan may be imminent in normalizing its monetary policy.

end

This year, it is possible for the Bank of Japan to continue to raise the YCC policy interest rate range, or to abandon the YCC framework, but this may be a super gray rhinoceros for the global financial market.

If Japan continues to raise interest rates, tighten the last faucet of “cheap money” in the world, and attract the return of overseas yen, it will have an impact on global currency liquidity, and its power will be greater than Switzerland’s overseas shrinking balance sheet. On the one hand, the global carry trade reversed, with positions as high as 12.9 trillion yen. On the other hand, Japan holds US$9.7 trillion in assets abroad, including US$4.3 trillion in bond assets and US$36,000 in stock assets.

In the short term, the Bank of Japan will continue to choose to stay on the sidelines and leverage the market hard. But the situation is stronger than others. In the next few months, before Haruhiko Kuroda’s last monetary interest rate meeting arrives, the market will not give up, and will once again have a fierce game and confrontation with the central bank.

This article is from the WeChat public account “Gelonghui APP” (ID: hkguruclub) , author: Moyu Fengxiang, 36 Krypton is authorized to publish.

media reports

36Kr The Paper News Sina Sina Sina Sina Sina Sina Tencent Technology Sina

related events

- Japan, this super gray rhino 2023-01-18

- The Bank of Japan unexpectedly adjusted the interest rate policy, shocking the global market2022-12-20

This article is transferred from: https://readhub.cn/topic/8mFJy1gWK60

This site is only for collection, and the copyright belongs to the original author.