Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Xu Jue

Source/Zero State LT (ID: LingTai_LT)

The “going overseas” of China’s new energy vehicles is accelerating.

According to data from the China Automobile Association, from January to August 2022, China exported 1.817 million vehicles, a year-on-year increase of 53%. Among them, new energy vehicles are the core growth point of China’s auto exports. In the first eight months of this year, the export volume of new energy vehicles reached 593,000 units, exceeding the total of 2021 (588,000 units), accounting for 31% of the total vehicle exports. In 2020, the annual export volume of new energy vehicles was only 223,000.

On September 2, the 10,000th new energy vehicle of Great Wall Motor’s Rayong New Energy Plant in Thailand rolled off the assembly line; on September 8, BYD signed a contract with WHA Weihua Group Volkswagen Co., Ltd. to formally sign the agreement on land subscription and plant construction. Prior to this, BYD and local partner RÊVER held a brand conference in Bangkok, announcing its official entry into the Thai passenger car market.

On September 16, Nezha Auto signed a comprehensive strategic cooperation agreement with PTT, the largest petrochemical manufacturer and trader in Thailand. The two parties will work together to develop the new energy vehicle market in Thailand. Prior to this, the right-hand drive version of Nezha V was launched in Thailand, and the first overseas 3.0 image experience space opened in Thailand.

Behind the dazzling achievements, the international competitiveness of Chinese new energy vehicle companies has been continuously strengthened. With the increasing momentum of Southeast Asia’s undertaking of industrial chain transfer, Chinese new energy vehicle companies are also targeting this emerging market with a population of nearly 700 million. Thailand has become the first stop for Chinese car companies to go overseas to Southeast Asia.

01

Japanese hegemony in the era of fuel vehicles

China and Southeast Asia are connected by mountains and rivers. Since ancient times, it has been a major channel for trade and cultural exchanges between the East and the West, and it is also the main destination for people from the southeast coast to migrate overseas in history. As early as the Qin and Han dynasties, there were records of maritime merchants entering Southeast Asia. During the Tang and Song Dynasties, Chinese maritime merchants spread all over the coastal areas of Southeast Asia, and population and economic exchanges became more and more frequent.

However, Southeast Asia, which should be the most familiar market for Chinese companies, is not the main export destination for Chinese cars.

According to customs monitoring data, the top five markets for China’s auto exports in 2021 are Chile, Saudi Arabia, Russia, Belgium and Australia. Li Chunrong, CEO of Proton Motors, once said: “In the Southeast Asian market, there were Chinese companies making layouts more than ten years ago, but they were all trade-oriented. After a short period of glory, almost all the previous Chinese brands withdrew from the local market.”

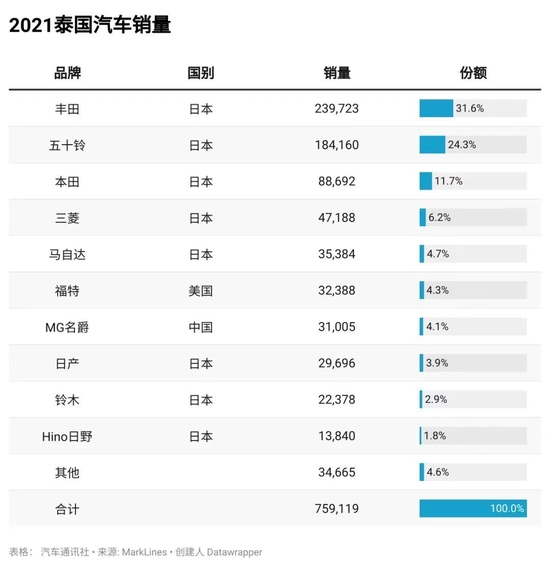

In 2021, Japanese vehicles will dominate all areas of the Thai passenger car segment.

Although sales of Toyota (including Lexus) with the largest market share fell by 1.9% to 239,700 units, due to the launch of the Corola Cross model in the Thai market in 2020, the sales of Toyota SUV products not only increased, but also promoted Toyota’s overall market share in Thailand. 0.8% to 31.6%. Although Honda’s sales in Thailand fell 4.7% to 89,000 units, the situation continued to improve in 2020.

The reason for such a large share is the strong barriers that Japanese car companies have built locally over the past decades. In 1990, Japanese car companies and auto parts manufacturers led by Toyota expanded their investment in Thailand, thus forming a relatively complete skilled labor market in Thailand and bringing technical support to local car manufacturers. Coupled with a 98% local parts procurement rate, Japanese cars can monopolize the market at a very low cost. Therefore, Southeast Asia has long been the back garden of Japanese cars.

On the other hand, most Southeast Asian countries have not developed local brands. Even Thailand and Indonesia, known as “Detroit in Southeast Asia”, are Japanese car kingdoms where Japanese car companies hold about 90% of the share.

This has also led to the fact that local companies in Thailand can only set foot in the low-end field, and cannot make core components such as engines and gearboxes. The situation in Indonesia is similar. Japanese cars not only occupy 95% of the market, but also firmly control the local market. Automotive industry chain, dealer channels, upstream and downstream parts suppliers, etc.

It is also extremely difficult for other countries to enter. If they want to enter, they will inevitably be constrained by the supply chain, and their products will also be surrounded and suppressed by Japanese brands. If it is all imported, then the freight and so on will be a lot of expenses, which will directly affect the product pricing, which may eventually lead to the inability to open the market. German, French and American cars have all tried to crack the Southeast Asian market, but most of them ended in failure.

02

why at this time

why thailand

Although Japanese car companies have deep roots in Thailand, this does not mean that Chinese new energy car companies have no chance. From a domestic point of view, this year is a year of accelerated restructuring of the auto industry. Even in the new energy vehicle field, which is in the limelight, factors such as fierce competition, tight supply chains, and rising raw material prices have all caused serious “involution”, and the speed of survival of the fittest in the industry is accelerating. It continues to accelerate, so it is logical to go overseas to find a new growth curve.

So why Thailand?

At present, there are more than ten electric vehicle brands in Thailand’s new energy vehicle market, and SAIC MG, which has a weak domestic presence, is the top one. In 2019, SAIC MG launched its first electric model MG ZS EV in Thailand, followed by MG EP. The two models accounted for over 90% of the sales of electric vehicles in Thailand, and their strength should not be underestimated. Great Wall Motor also launched the Haomao model in Thailand in October last year, and received 6,000 orders within two days of its launch.

Behind the dazzling achievements, Chinese car companies have a deep insight into the needs of the local people. Taking the economically developed Chiang Mai as an example, in addition to pickups, the most used passenger cars are small cars with a displacement of about 1.5L. The most common ones are Toyota’s Vios series, Honda JAZZ and CITY Fengfan. Even the Mazda 2, which is not popular in China, is quite popular in Thailand. And this choice is based on realistic considerations: according to Thailand’s official data, Thailand’s per capita monthly income is about 2,700 yuan. At this level of income, the price, durability and practicality of the vehicle are more important considerations than all kinds of cool technology.

Therefore, when SAIC entered the Thai market, it catered to the local demand with the entry-level boutique family sedan MG 3, and won SAIC’s best-selling model of the year. So successful, the most important point is that the price of MG 3 is relatively low. The starting price in Thailand is 479,000 baht (about 96,300 yuan). If you pay in installments, you can own it with a minimum down payment of 15%, which is much lower than The competing Mazda3 is 969,000 baht. Secondly, the MG 3 model provides a two-color body, and the novel color matching also makes the MG3 popular among young consumers in Thailand.

With the test of MG 3, SAIC’s first pure electric model MG ZS EV launched in Thailand adopts the same idea. At that time, the new energy vehicle market in Thailand was a blank piece of paper, and the MG ZS EV was positioned as a compact pure electric SUV. The 44.5kWh battery pack WLTP has a comprehensive range of 263km. Electric heated seats, car play, panoramic sunroof are all available, the E-NCAP crash test has 5 stars, and it also provides a seven-year unlimited mileage warranty, so it is sought after by the middle class in Thailand.

Not only MG adopts a low-price strategy, but Great Wall Motors, which just entered the Thai market last year, has also lowered the prices of all three pure electric vehicles. The lowest price is about 830,000 baht, which is 16% lower than the original price. This month, the price of BYD’s first pure electric passenger car in the Thai market is only 1,199,900 baht without subsidies.

In addition to the cost-effective strategy based on price, localized production is also the consensus of domestic car companies. SAIC MG owned its first assembly plant as early as 2013. Since then, it has established SAIC CP Co., Ltd. as a joint venture with Thailand’s CP Group, and spent 10 billion baht to build a second, more intelligent plant in Chonburi Province. Great Wall Motors immediately carried out intelligent transformation and upgrading after acquiring the Rayong Automobile Manufacturing Plant and Powertrain Plant in Thailand. On September 8, BYD also announced that it would buy land to build a factory in Rayong.

If localized production has given Chinese car companies a “ticket” to the Thai market, then localized R&D has given them more confidence to challenge Japanese hegemony.

MG (Thailand) relies on SAIC’s technology accumulation. In addition to developing the i-Smart system that can understand Thai language, making MG ZS the world’s first car that can control the vehicle in Thai language, it also relies on a high degree of modularity. The SAIC platform for overseas travel has created popular smart hardware such as ai assistant, thus establishing a brand image of “black technology”, “Internet” and “younger” in the hearts of Thai consumers. Great Wall Motors introduces advanced technologies into factories, cooperates with local parts manufacturers to develop new products, shares professional technical knowledge of automobile production, and accelerates the reserve and training of local talents.

In order to draw a blueprint on the “white paper” of Thailand’s new energy, Chinese car companies have also jointly held electric vehicle forums with relevant Thai government departments for many times, promoted the formulation of relevant standards, called for the introduction of industrial policies, vigorously built infrastructure, and actively promoted The electrification process of Thai cars.

Thai officials have also begun to formulate a series of incentives for the development of new energy vehicles.

In terms of taxation, the Board of Investment (BOI) of Thailand provides up to 8 years of corporate income tax exemption for suppliers of various types of electric vehicles. In terms of financial subsidies, it is in line with the policy issued by the National Electric Vehicle Policy Committee of Thailand. In the plan to transition to zero emissions, the Thai Ministry of Finance has also spent 2.923 billion baht as a car purchase subsidy to encourage consumers to buy and use electric vehicles. In terms of the battery industry chain, Thailand currently has 18 projects under construction, involving battery production, module production, and module assembly.

“The supply chain advantages of China’s new energy vehicles and the current mature business model can start from Thailand and quickly radiate to other surrounding areas.” An industry insider told Zero State LT (ID: LingTai_LT). “And this is also the key to whether Chinese car companies can use this to break the Japanese car series.”

Of course, the ambitions of Chinese new energy vehicle companies will not stop in Thailand. From the current layout of various companies, Thailand is just a starting point, and the ultimate goal is to radiate the entire Southeast Asia.

03

From point to area

Can you take over Southeast Asia?

If you win Thailand, can you win the entire Southeast Asia?

From a geographical point of view, Thailand is bordered by Myanmar in the west and northwest, Laos in the northeast, Cambodia in the east, and Malaysia in the south, which can be said to be able to completely cover Southeast Asia. If Chinese car companies can gain a foothold in the Thai market, radiate to Southeast Asia, and then increase their global market share, it can be said that it will not be a problem at all.

For the current Chinese new energy going abroad, the size of the population directly determines the future development space. At present, the total population of the ten Southeast Asian countries has exceeded 660 million, and the potential demand for automobiles is huge. In terms of economy, in recent years, the economy of Southeast Asia has developed rapidly, and residents’ income has continued to increase. The total GDP of the ten Southeast Asian countries has exceeded 3.2 trillion US dollars, and it has jumped to the fifth largest economy in the world.

More importantly, Southeast Asia is also one of the regions with the fastest average annual growth rate of carbon emissions in the past decade. According to the Southeast Asia Energy Outlook (2019), carbon emissions in the region will climb from 1.4 billion tons in 2018 to 2040. nearly 2.4 billion tons per year. Therefore, the requirements of coping with global climate change and promoting the realization of green travel are also forcing Southeast Asian countries to promote the popularization and development of new energy vehicles.

Compared with the monopoly of Japanese cars in the traditional automobile market in Southeast Asia, new energy can be said to be still in its infancy. According to data from the Southeast Asian Automobile Federation, total vehicle sales in Southeast Asia will reach 2.79 million units in 2021, a year-on-year increase of 14%. It is expected that by 2035, the sales of electric vehicles in Southeast Asia will completely exceed that of fuel vehicles. According to the Bangkok Post report, Thailand has reduced the tax rate of pure electric vehicles from 8% to 2% since June this year, and each pure electric vehicle still has 150,000 baht to buy a car subsidy.

Indonesia has also set a goal of making pure electric vehicles account for 20% of its total vehicle production by 2025; the Philippines is also vigorously purchasing electric buses, and requires domestic public transport companies to increase the proportion of their pure electric vehicles to more than 5%. . In addition, the Southeast Asian auto industry has benefited from the advantages of trade agreements with various countries, and is now a key operating area for global automakers and parts factories. In the future, it is expected to replicate the growth model of the Chinese auto market and become the next development focus of the global auto industry.

Looking back at the “going overseas” process of Chinese car companies, from the simple export of vehicles in the past, to going overseas with the industrial chain and technology now, Chinese automobiles going overseas have ushered in structural changes. Although the “sinicization” of the automobile industry chain cannot be fully realized in a short period of time, in the new wave of electrification, Chinese car companies have pressed the accelerator button for hunting Japanese cars in Southeast Asia.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-10-14/doc-imqmmthc0847285.shtml

This site is for inclusion only, and the copyright belongs to the original author.