Among the many foreign stories in the pharmaceutical industry, a mature and effective trading market is a very attractive one, especially when Chinese companies go out to the sea to look around, they are all admirable pictures, both greedy for multinational drugs Qi’s bottomless pockets are also jealous of the ingenious products of biotechnology companies, which is a lively scene of win-win business and guest-host enjoyment. Turning his head to look at the shabby family, the purchases are not worth the money, and the sales are not good, why not make people feel disappointed?

Of course, we must admit the development gap in the field of medicine, assets and capital, quantity and quality, concept and operation, we still have huge deficiencies compared with the international market. However, when others play well, how well, how well, and whether they have been good all the time, we always have to have a spectrum in our hearts, and only by imitating and catching up can we get ahead. Knowing what to buy and what to sell is also a necessary preparation.

Therefore, the starting point of this article is to comprehensively analyze the major asset transactions of international pharmaceutical companies in the field of innovative drugs in history, and establish a connection between various conditions and indicators during the transaction and whether the underlying assets can ultimately generate commercial value. The core intention is to quantitatively answer a question: Have international pharmaceutical companies made any money in innovative drug transactions?

0. Data Declaration

This paper analyzes all overseas innovative drug asset transactions from 2000 to the present , including two categories: first, merger and acquisition transactions, which require a total transaction value of more than 1 billion US dollars; second, authorization (referring to handing over all rights to the transferee) and cooperation (referring to the joint development of both parties) type transactions, the total transaction value is more than 1 billion US dollars, and the down payment is not less than 30 million US dollars. Mergers and acquisitions between large pharmaceutical companies (such as the acquisition of Celgene by BMS) are not included because it is difficult to consider their impact.

A total of 203 transactions were included in the final analysis. Transaction-level data, including transaction time, transferor, transferee, down payment, milestones, total transaction value, etc., the main data comes from listed company announcements, media reports and Capital IQ database statistics, etc. It must be explained that the amounts here are all The amount paid by the transferee is different from the overall valuation of the target in the M&A transaction; transaction target-level data, including drug name or code (use generic name if possible), target, disease area, drug type or technology path, transaction The current development stage, the latest development stage, peak sales, etc., the main data comes from the medical cube database, announcements of listed companies, and media reports. If there is no public disclosure, leave it blank. It must be explained. The one with the highest total sales of traditional Chinese medicines (if it is still climbing, take the last year), simply consider the quality of the underlying assets of the transaction, without considering the scope and proportion of the transferee’s rights (for example, only holding some regional rights or only sharing part of the revenue profit).

A summary table of information on all transactions and underlying assets is attached at the end of the article.

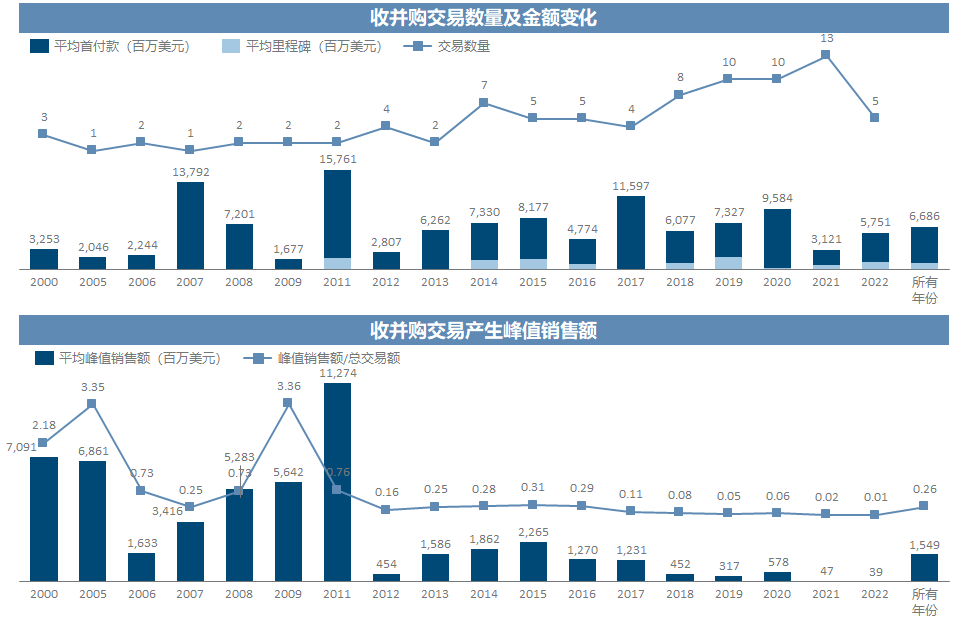

1. Overall trend

The popularity of M&A transactions has increased significantly in the past ten years , but in the past two years, it has tended to be “miniaturized”, and the frequency of tens of billions of transactions has been significantly reduced. However, while the number of M&A transactions has surged, the asset quality of M&A transactions can be said to be not as good as it used to be . From 2000 to 2011, each transaction generated an average of billions of peak sales, which is basically equivalent to the total transaction value. From 2012 to present Not only did peak sales of traded assets drop rapidly, but the “return” became very ugly as the total traded value increased. For all M&A transactions, the transferee spends an average of nearly 7 billion per transaction, but can only recover peak annual sales of 1.5 billion .

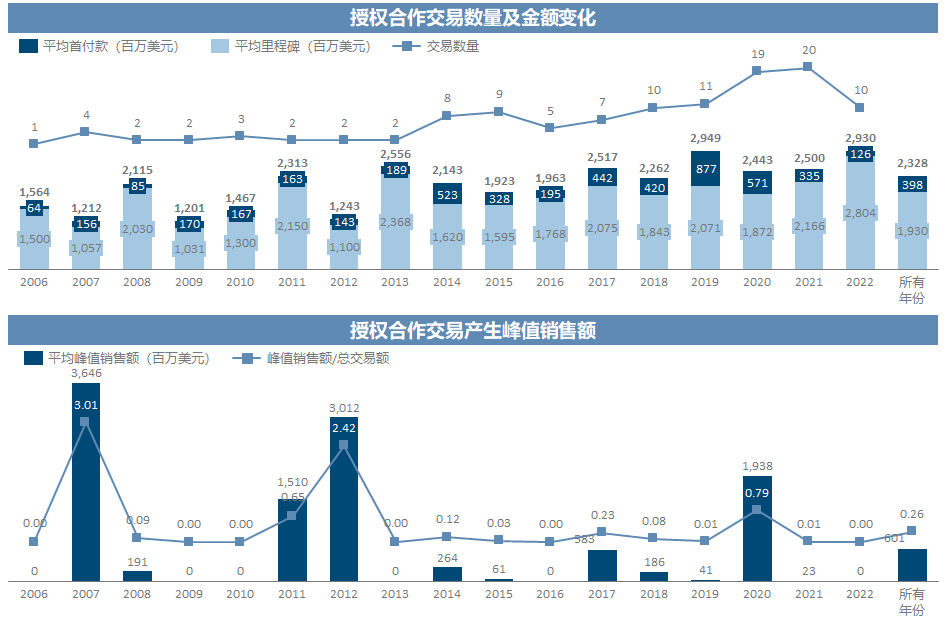

The trend of licensing cooperation transactions is similar to that of mergers and acquisitions, and even the growth of transaction frequency and amount is more aggressive, especially in 20/21, which doubled compared to 18/19. Among so many transactions, the proportion of high-quality assets is much lower than that of M&A transactions. Most of the transactions cannot even produce approved varieties, let alone sales. Only a few “God transactions” that have produced super-heavy bombs have been created. The increase in average peak sales objectively reflects the great uncertainty of authorized cooperation transactions (even if the amount threshold is more than 1 billion), which is far greater than that of M&A transactions.

Before starting the analysis, although I often ridiculed the vision of international pharmaceutical companies, I did not expect that the commercial value generated by these transactions as a whole could be so low. We can simply assume that since the product is launched, it will generate revenue at the peak sales level for 5 consecutive years, and the net interest rate will be 40%. Without considering the cost of capital time, if the peak sales/total transaction volume is less than 0.5, Basically, it is difficult to recover the investment cost . Considering that the peak sales here are not all attributable to the transferee (but the transaction amount must be paid out), and the peak level is often difficult to last for many years, so the probability of the break-even point of this ratio should be only high. Not low; of course, taking into account the definition of peak sales here, it is possible that the actual peak will be higher for some products that are still climbing. Therefore, it can be seen from the specific analysis of various companies and transactions here and later that only a few transactions with the right time and place can make money, and they have made many times the money, while the vast majority of the remaining transactions are losses. Yes , M&A transactions are more mature, with high certainty, but the transaction volume is also large and it is not easy to make money, and the authorized cooperation transactions with smaller amounts, earlier stages, and weaker endorsement by big pharmaceutical companies are even more outrageous.

The inspiration this gives us is that overseas asset transactions are certainly a very important development tool for innovative drug companies, but both companies and investors should have more calm expectations for even large-scale transactions. Assets endorsed by the best buyers in the international market may not be able to bring benefits, and the persuasiveness that other transactions with less certainty can provide is even more conceivable .

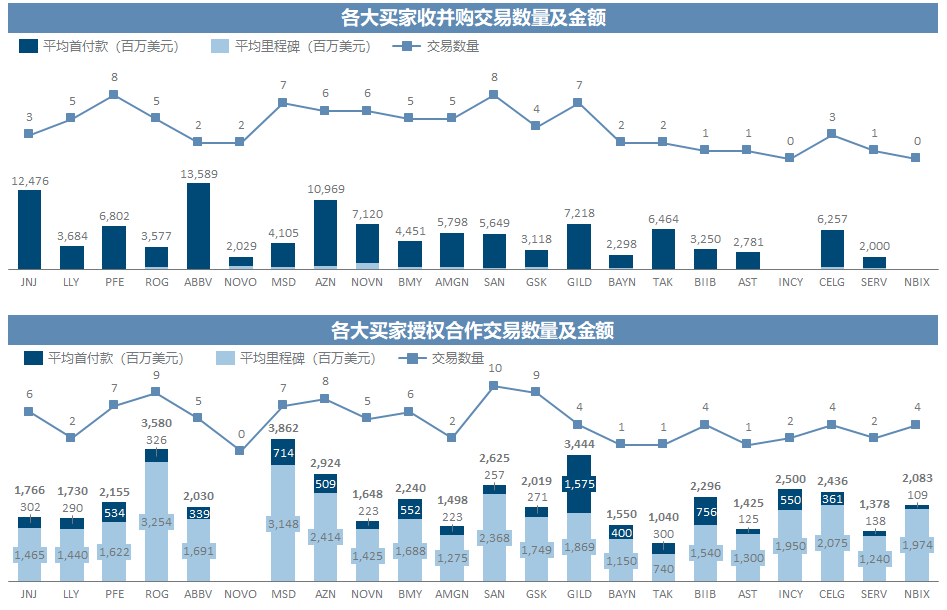

2. Buyer activity

Among the 203 transactions, only 9 active buyers have made ten or more shots. All buyers who have made no less than two shots are sorted by market value as follows, and they will be analyzed and ridiculed one by one later.

Big Pharma’s overall shot is more generous. Sanofi actually has the most ties in the audience. Pfizer is also a worthy buyer. J&J, Abbvie and AZ have made many billion-dollar deals. Roche They don’t play big, but they like to play small. Novo Nordisk is the most silent; the new talents who have grown up in Biotech have much shallower pockets, mainly Gilead and Celgene.

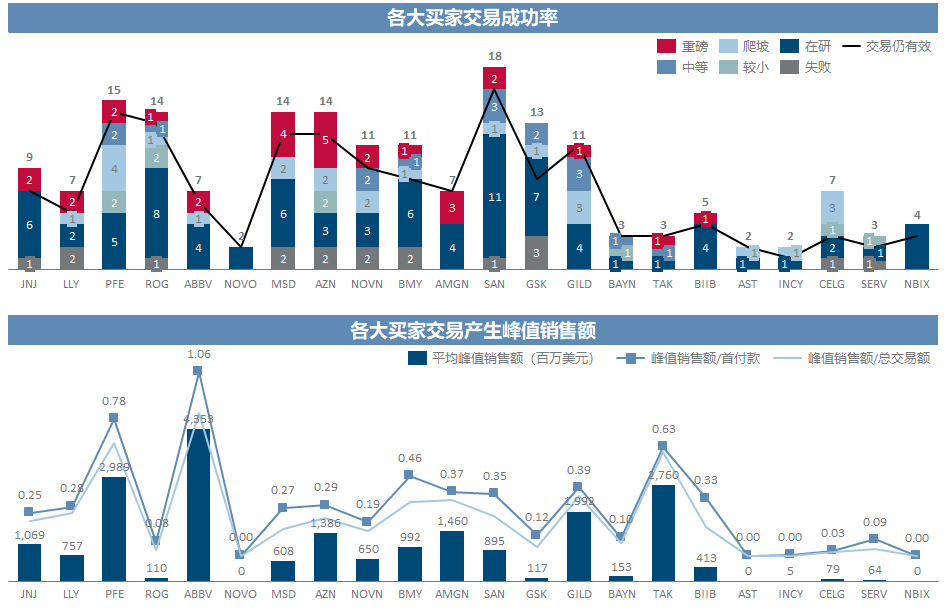

3. Buyer Success Rate and Peak Sales

The subsequent trends of all the underlying assets of the transaction are divided into six categories, including heavyweight category (products with peak sales exceeding 1 billion), medium category (products listed for more than 3 years and peak sales of 200-1000 million), climbing Category (products listed within 3 years and more likely to continue to climb), smaller category (products listed for more than 3 years and peak sales less than 200 million), research category (products have not been approved but at least no public information shows that they have been Termination of development), failure category (product development has been terminated); in addition, whether the transaction is still valid or not is also marked (as mentioned above, there is a situation where the transaction is terminated but the product development has not failed).

It can be seen that although AZ, MSD and Amgen are the best blockbuster hunters, due to the lack of super heavy prey, the peak sales brought by the transaction are mediocre; Abbvie, Pfizer, Gilead and Takeda basically rely on each other. One or two super heavyweights supported the average sales; Roche sold too many early assets, GSK hung up the most projects, and Celgene did not even get mature products after listing. Among the more active buyers The three brothers had the worst asset sales.

4. Representative Buyers

Before the official fire of mockery, I still have to make a statement: the amount of data is large and all manually extracted and entered from different channels. The omission and rudeness of basic data are inevitable, and the products that I am relatively familiar with have been taught based on memory as much as possible. Yes, but there may still be a few product information that is incorrect, and the understanding of the company and products in the comments is more likely to be superficial and unexplored, please do not hesitate to correct and Haihan.

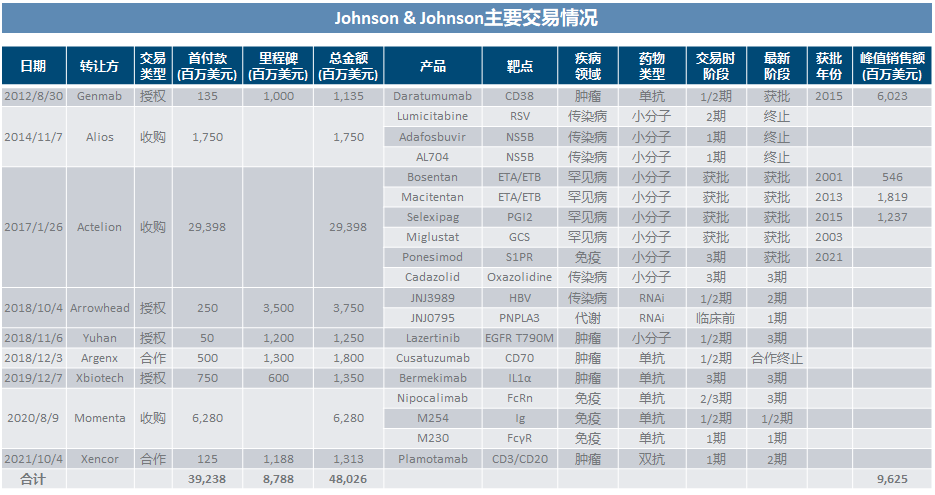

4.1 Johnson & Johnson

Since J&J bought Daratumumab ten years ago, it has been lackluster in terms of transactions. The biggest bet of 30 billion to buy Actelion is really too cost-effective. At present, if JNJ3989 can regain its advantages in the race with ASO, there is still hope to rank among them. heavyweight.

4.2 Eli Lilly

Eli Lilly has been a large pharmaceutical company with relatively high self-research efficiency for a long time. It seems a little sloppy in terms of transactions. In the early years, the two assets of Tadalafil and Cetuximab were basically bought as cash cows. The largest Loxo has not been seen at least yet. For the money back, it might also be worth looking forward to Lebrikizumab from Dermira.

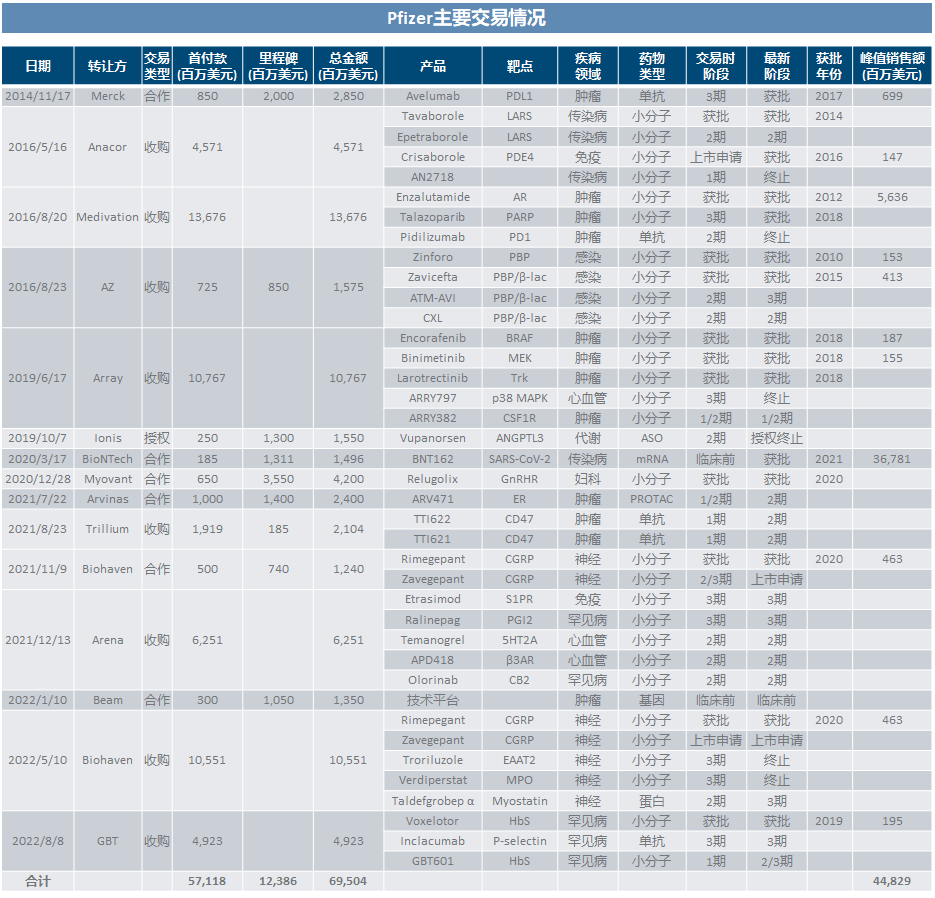

4.3 Pfizer

In addition to the windfall of BioNTech, the “return” of Pfizer’s other transactions is actually not good. With a down payment of 57 billion, it can only get a peak sales of 8 billion. If you remove Enzalutamide, the purchase time As for the products that have been approved for many years and the follow-up plot has not been right, then Pfizer’s vision as a big buyer for more than 20 years is really a question mark (after all, Lipitor has long been a memory). Forgive me for not being able to know the true God. From this list of trading assets, the intuitive feeling is that there is a hammer in the east and a hammer in the west. Various disease areas and drug types are synchronizing and evenly pouring money, especially after the windfall is visible to the naked eye. unrestrained. At present, among these products, it seems that Biohaven’s two migraine drugs should still have some points of interest (although they have kneeled on other projects just after receiving the company), Arvinas’ PROTAC is a small future, and Beam may have a big future.

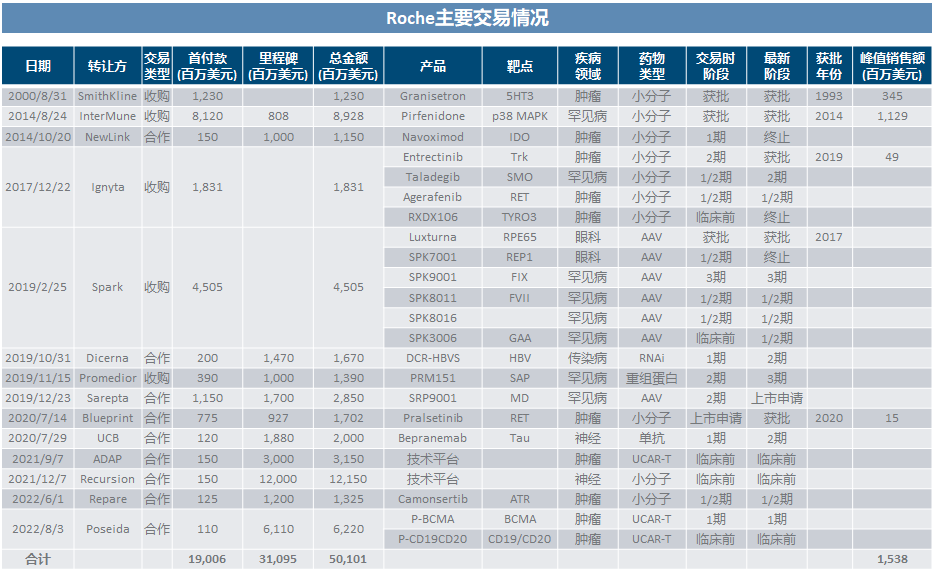

4.4 Roche

I don’t know if it’s because the history of self-research is too glorious (regarding Genentech as the body), Roche is obviously not interested in spending a lot of money to buy products. It is even more relegated to the “small scattered” projects that only make a down payment of more than 100 million, especially for the so-called next-generation technologies such as genes, cells, and nucleic acids. The one with the fewest peak sales.

4.5 Abbvie

Abbvie is the only player in the audience who hit two overweight prey (the King of Medicine should have extra points), and he can really blow for a lifetime with just these two hits. Of course, the 63 billion purchase of Allergan (not in the scope of this analysis), which I haven’t been able to understand so far, may be the “outrageous” one.

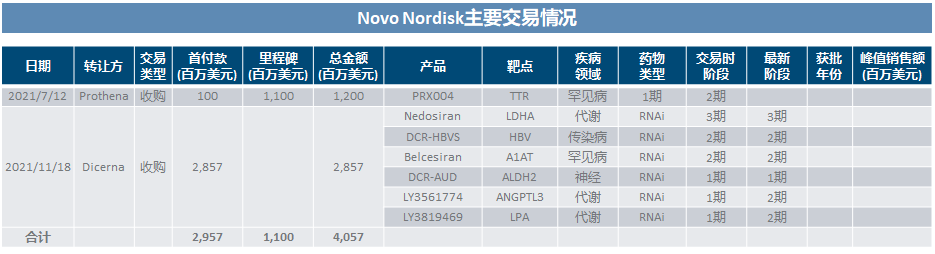

4.6 Novo Nordisk

Novo Nordisk is definitely the most conservative big pharmaceutical company in terms of transactions. Not only is it willing to show its money for metabolic diseases with its old business, but even if it buys game changers like RNAi, it only buys Dicerna, the cheapest among the three brothers. Sexual mentality comes to the fore.

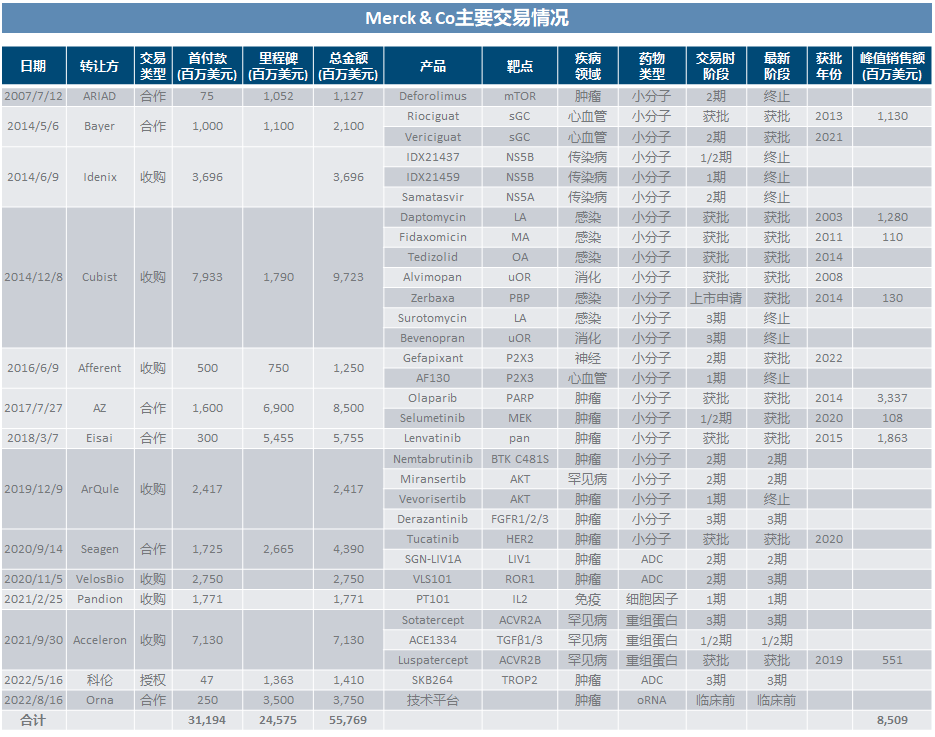

4.7 Merck & Co.

MSD lost blood in the field of infection/infection in the early years. In recent years, it is at least remarkable. It focuses on tumors and rare diseases. If Acceleron can make some gains, the transaction results can be explained in the past.

4.8 AstraZeneca

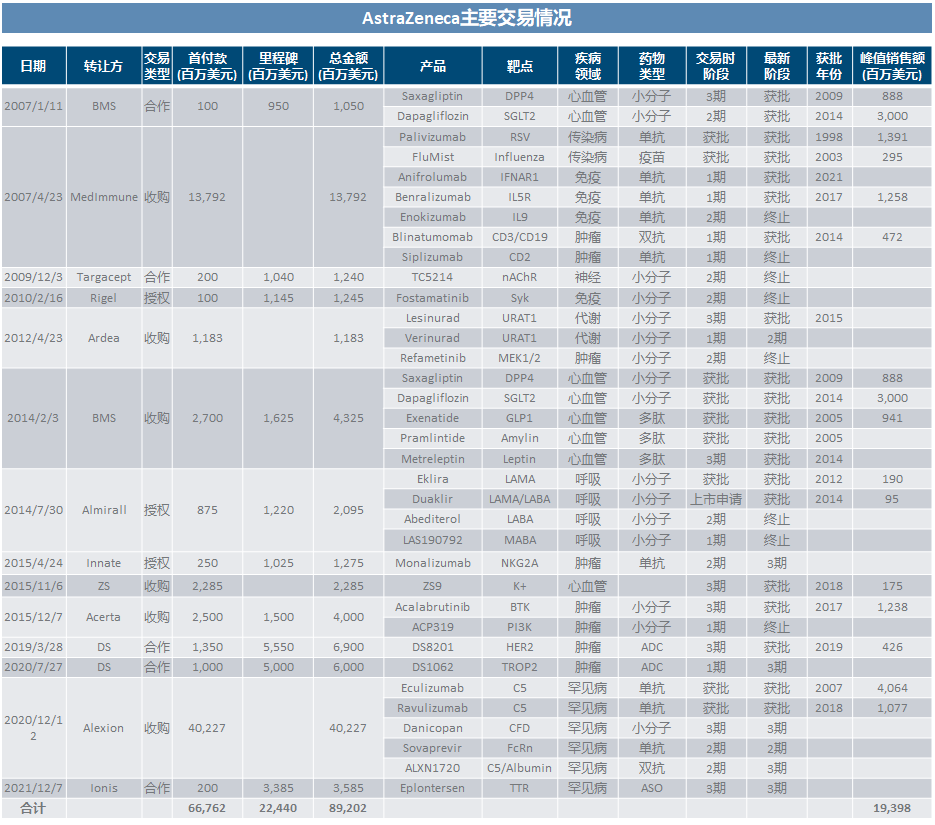

Before 2019, AZ might be the dragging role of the buyer industry. After all, MedImmune spent too much money; by the end of 2020, by holding Daiichi Sankyo’s thigh tightly, DS8201 will block the killing Buddha, and AZ will stop killing the Buddha. He jumped into the most handsome boy in the whole street; then with the Alexion merger case, the 40 billion amount made the weight of other transactions instantly meaningless, and the current sales of the C5 series of 4 to 5 billion are not enough to fill this hole. .

4.9 Novartis

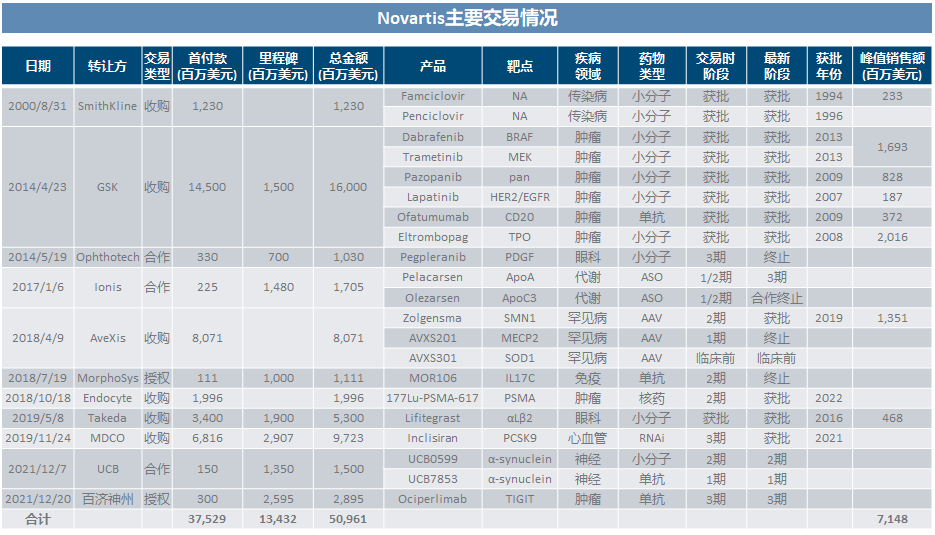

Among the big pharmaceutical companies, Novartis undoubtedly spends a lot of time in the transaction, and the idea of buying the head of each track is relatively clear. Inclisiran in RNAi, Zolgensma in AAV, 177Lu-PSMA in nuclear medicine, plus China BeiGene, a pharmaceutical company, has good assets, but none of them are cheap.

4.10 Bristol-Myers Squibb

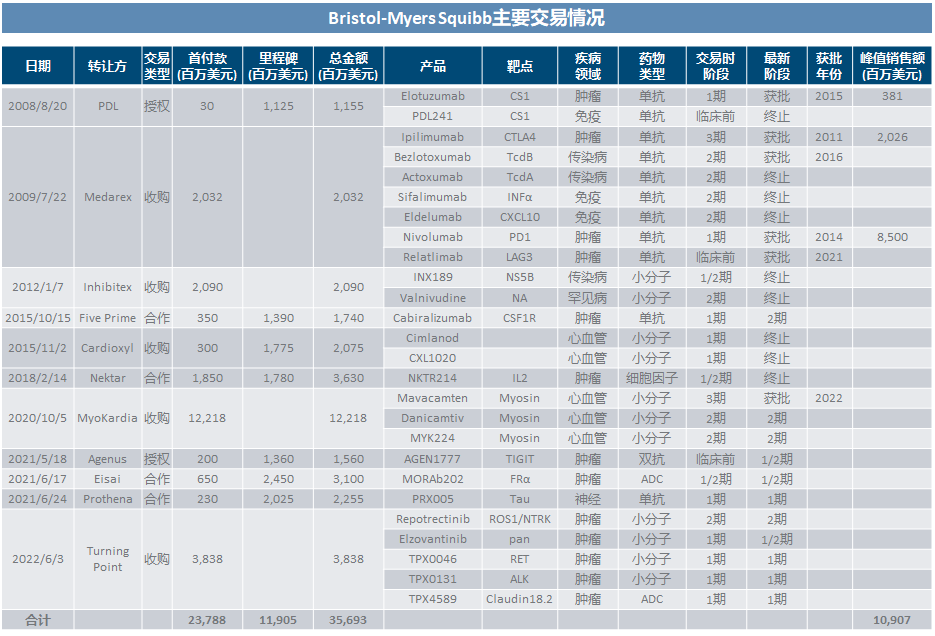

Relying on a Medarex antibody platform, BMS has not been able to consume it until now, and after Nektar’s dream is broken, the heavy task of filling the O drug pit is probably going to fall on MyoKardia’s cardiomyopathy drug series.

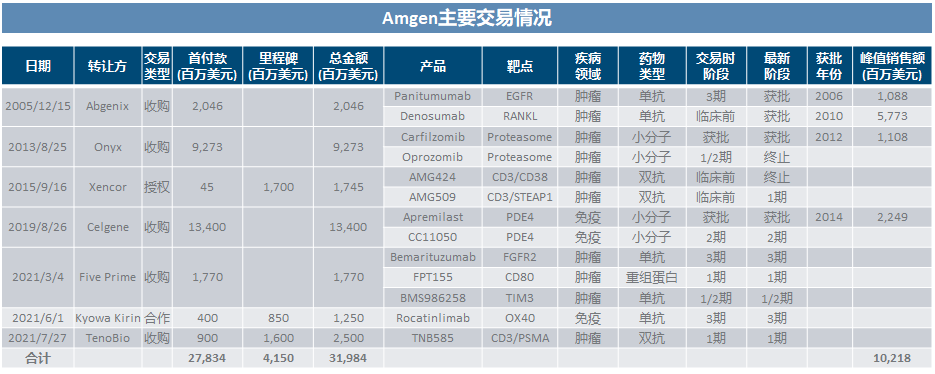

4.11 Amgen

After the successful acquisition of Abgenix in the early years, Amgen seems to have lost its inspiration in the transaction. Although Carfilzomib and Apremilast are heavyweights, in front of the price of 9 billion/13 billion, the small and heavy price-performance ratio of more than ten or two billion sales Very suspicious.

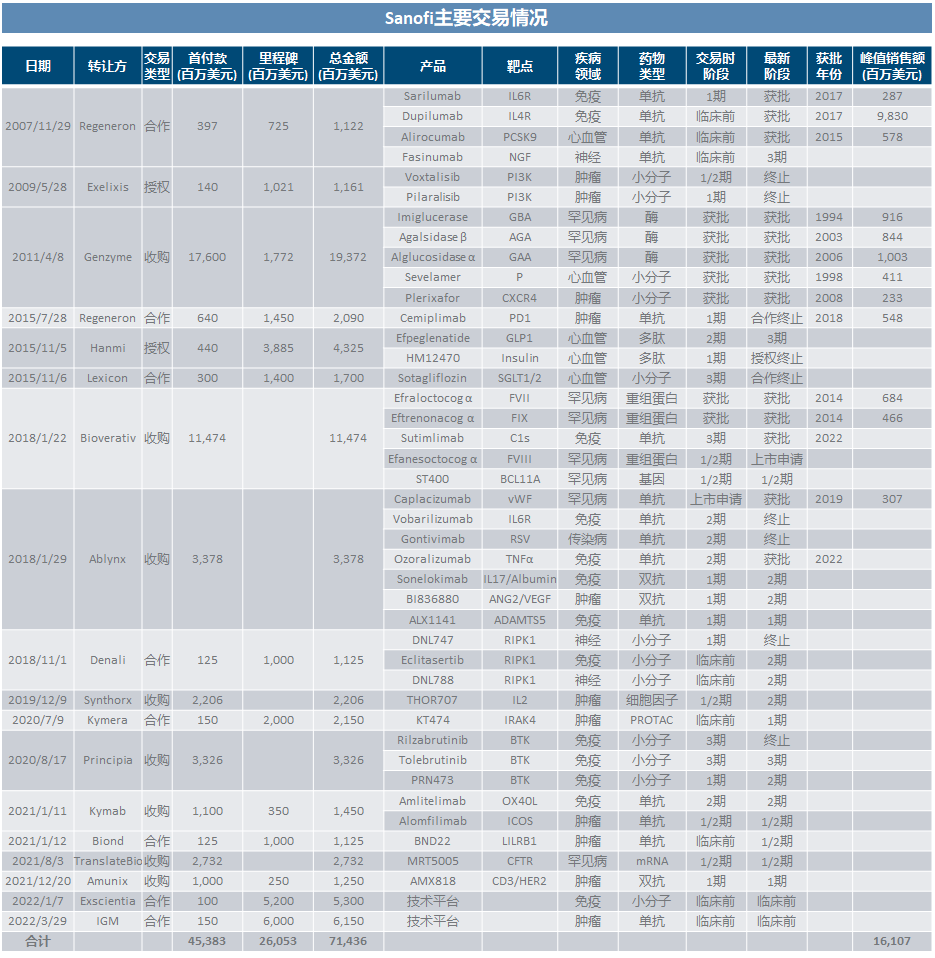

4.12 Sanofi

As soon as Sanofi appeared on the stage, the atmosphere gradually became joyful. For details, you can also refer to ” Sanofi Folding Arm SERD “Meat Grinder” and ” Sanofi or Twice Breaking Halberd BTK “. Finding Regeneron was a miracle, although it was a bit unclear who was the father; Genzyme supported the company through the time before Regeneron exploded, although it was not cheap; the rest of the deal, except for the name of the target, was spelled quite a lot. Apart from the features, it is difficult to figure out any reliable aesthetics (today’s milk method), Bioverativ, Ablynx, Principia, Denali and possibly Synthorx, kneeling out of posture, kneeling out of level; so much so that in the past two years, more It was quickly approaching the path of Translate Bio, Exscientia, and IGM. . . (Sorry I can’t really appreciate this genre)

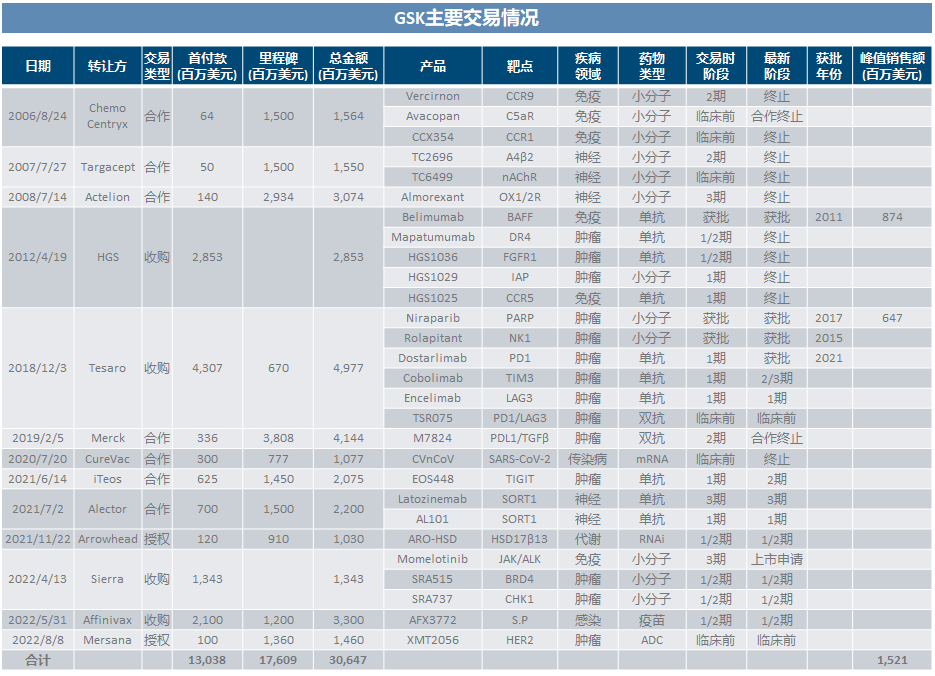

4.13 GSK

Before I started writing, I was just thinking about the milk method, but I found out that the big old GSK is the biggest cup. After all, Sanofi is also backed by Regeneron. I didn’t mention the miserable death in the early years. When I bought Tesaro, I felt like my fortune had turned around. However, although PARP was good, it was obviously not worth the price of 5 billion; people made money playing PD1 and dual resistance, and it played with Merck. It’s a dead end. People play mRNA vaccines to make money, and it’s dead when playing with CureVac. It has a cancerous temperament. The recent 3.3 billion purchase of high-priced pneumonia vaccines is a bit mysterious, and the deal with Mersana is even more confusing.

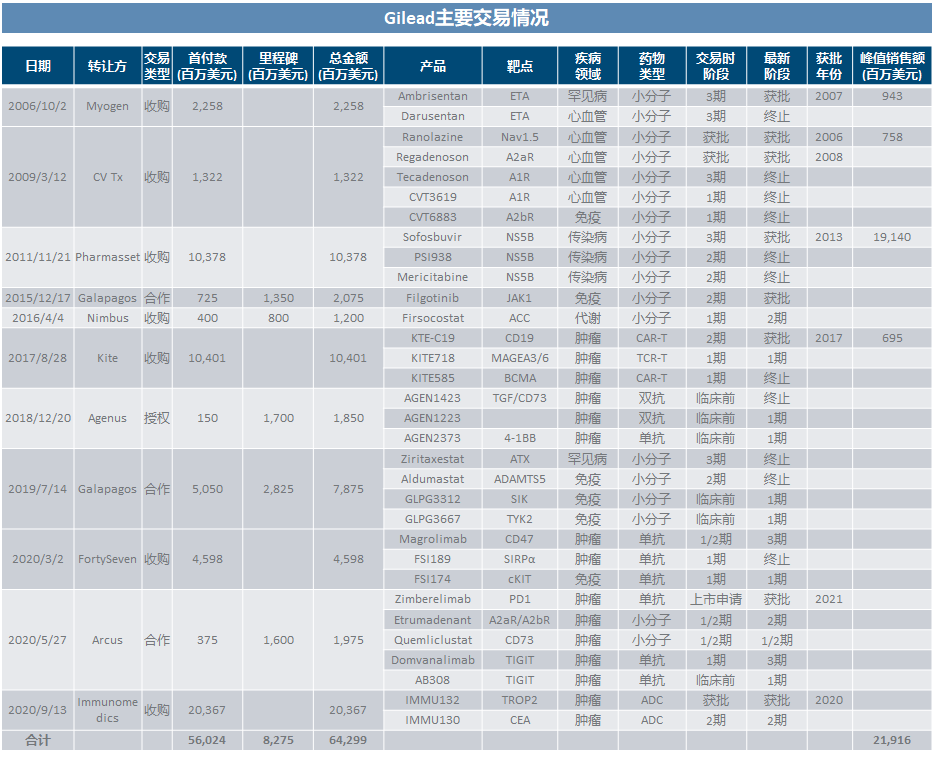

4.14 Gilead

Just look at Gilead to know what it means to be a god in the first battle; if it is difficult to obtain a victory after being conferred, you may also have to look at Gilead. Back then, he spent tens of billions to buy back the hepatitis C series led by Sofosbuvir, which brought tens of billions of cash, and then the operation was simply unbearable. Kite was completely ignorant, Galapagos was a bunch of bulls and ghosts, and CD47 had a bad fate. It seems that the only thing looking at assets is The relatively normal IMMU132 itself is priced at 20 billion. . . From Gilead, I can fully feel that pharmaceutical companies also pay attention to their heritage. Although the old-fashioned aristocrats will also make a lot of confusion, they rarely see a series of unbelievable big pits like the number one upstart. .

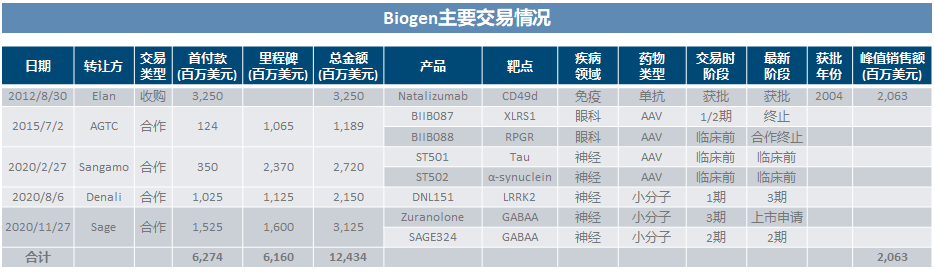

4.15 Biogen

In recent years, the topic of Biogen has been concentrated on AD, and the transaction level has been calm.

4.16 Celgene

The last place on the list is undoubtedly the worst. Among the 7 major transactions, 3 failed, 1 voluntarily terminated, and 3 products were approved but the sales compared with the transaction pricing can be said to see little hope. . . However, although people are not good at buying, they are good at selling; how tiring is it to make money after buying assets, isn’t it sweet to sell yourself at a good price and focus on counting money 🙂

5. Postscript

Unknowingly, the whole combing turned out to be a miserable conference. It seems that in the two keynotes of miserable and especially miserable, there are only a few lucky people enjoying the dividends of the whole industry. In fact, this is neither arrogant (from China’s standpoint) nor self-defeating (from the standpoint of medicine), but the characteristics of the innovative drug industry chain itself, which are highly risk-intensive and highly concentrated, and are just projections in the transaction. The simplest explanation is that if it is so easy to make money by buying, buying, buying, and buying, why would anyone spend time on self-study?

Since pure asset trading is not a shortcut to making money anywhere, let’s focus on the product itself, let technology and R&D drive clinical benefits, and accumulate enough value for the assets in your hands. Trading is only about realizing value. At the same time, with awe and distance from the market, buying and selling itself does not generate value, and who will buy what price will not increase or decrease the certainty of the product itself.

After all, who can have a melon that is guaranteed to be ripe?

Attachment: List of major innovative drug transactions since 2000

$BeiGene(BGNE)$ $Innovent Bio(01801)$ $Hengrui Medicine(SH600276)$

This topic has 13 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1335311504/232299097

This site is for inclusion only, and the copyright belongs to the original author.