This is an article on the “Snowball Special Issue” in November. It is mainly a collection of my previous posts, and it is used to popularize the rough points of coal investment. Since the “Reference” has been published, I will share it with you here. The article is relatively superficial, and it is strongly recommended that friends who study coal study a few articles by @沙林子洲.

text

Energy, information, and organization are the core elements that drive human progress, and energy is the most important. The history of human civilization is a history of the use of high-efficiency energy. Energy itself is scarce, and people’s wars for energy abound. The prosperity or decline of enterprises, the rise or fall of national status, all of these depend on energy.

Since the founding of the People’s Republic of China, in order to ensure energy security, my country has built an energy system with coal as the ballast stone. The mining and utilization of coal has provided sufficient power guarantee for the rise of a large country with a population of 1.4 billion.

In 2021, my country’s large-scale enterprises will produce 4.07 billion tons of raw coal, accounting for more than 50% of global coal production. The continuously growing demand for coal has brought environmental pressure and public opinion pressure on carbon emissions both domestically and internationally. In this context, my country has promised to achieve “carbon peak” by 2030 and “carbon neutrality” by 2060. At the same time, vigorously promote the capital investment of wind and solar storage, in order to build a new energy system with words and deeds.

Specific to the investment of coal enterprises, the opinions of the group are quite divided. On the one hand, the coal mining sector index has risen by 42.3% and 26.8% respectively in the past two years, showing stable and excellent performance in the uncertain environment of A-shares, and coal companies generally make real money after earning high profits. High dividends; on the other hand, the “Development and Reform Commission” continues to regulate the price of coal, especially thermal coal, and the capital investment is gradually increasing with wind and light. Many investors think that coal is a thing of the past. Regarding whether the coal industry is currently suitable for investment, the two voices are quite different.

From my personal point of view, for coal investment, we need to pay attention to two big logics and four small details.

Logic 1: Before the realization of “carbon neutrality”, coal will occupy a key position in my country’s energy system for a long time.

First, demand for coal remains strong and supply remains in a tight balance.

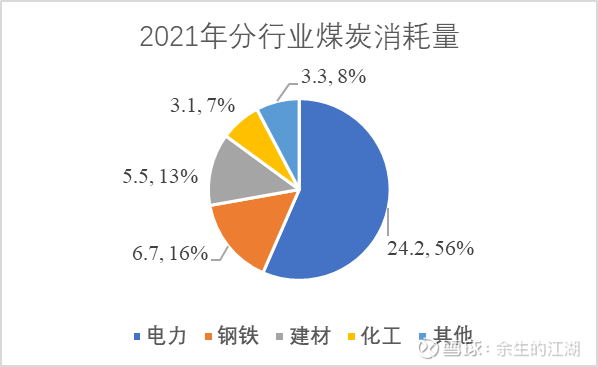

In 2021, my country will consume a total of 4.27 billion tons of commercial coal, accounting for 56% of the total energy consumption. Although the proportion has dropped by 0.8 percentage points, the absolute amount of coal consumption has increased by 5% (or 230 million tons) year-on-year. In terms of industries, electric power, iron and steel, building materials, chemicals and other industries consumed 2.42 billion tons, 670 million tons, 550 million tons, 310 million tons and 330 million tons of commercial coal respectively, a year-on-year increase of 8.9%, -1.9% and 1.1% respectively , 3.6% and 0.8%, of which coal consumption accounted for 56.7%, a year-on-year increase of 2 percentage points, as shown in Figure 1.

Figure 1. Classification of China’s coal demand in 2021

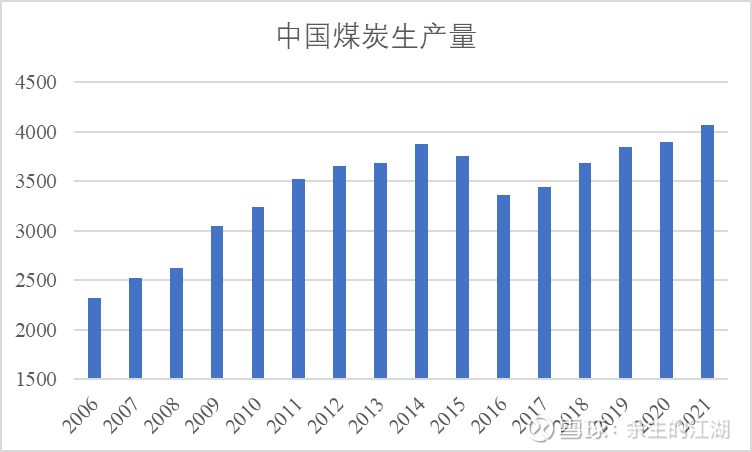

Continued growth in demand will put pressure on supply. Figure 2 is the trend chart of raw coal production in my country in the last 15 years. It can be seen from the figure that the production of raw coal of enterprises above designated size tended to grow steadily before 2014. After a short-term decline, in 2016, the production started to grow again and fell Reaching a staggering 4.07 billion tons in 2021.

Figure 2. China’s coal production trend in the past 15 years (unit: million tons)

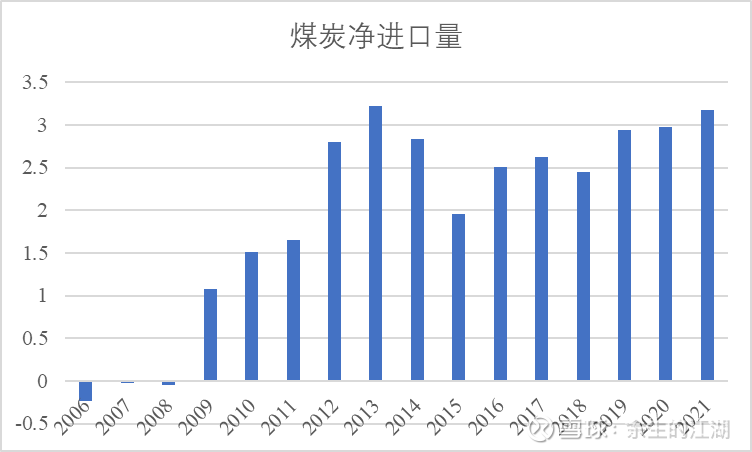

Due to the gap in demand, the demand for scarce coal types and the price difference between domestic and foreign coal, some coal needs to be supplemented by imports. Figure 2 shows the net import data of raw coal in my country. Since 2009, my country has completely changed the net export of raw coal, and the net import volume has rapidly increased from 100 million tons to 300 million tons, and has remained at 200 million tons in the following eight years. In 2021, the net import will be 320 million tons.

Figure 3. The trend of China’s imported coal quantity in the past 15 years (unit: 100 million tons)

So, is there an opportunity to increase domestic production capacity?

During the “13th Five-Year Plan” period, due to relatively low coal prices and “supply-side reforms”, my country has withdrawn nearly 1 billion tons of coal production capacity. Mengxi is concentrated, and in the foreseeable next 10 years, the coal mines in the central and eastern regions will be depleted at an accelerated rate.

In the same period, the newly increased and approved production capacity was less than 600 million tons, and the approved number decreased year by year. According to personal statistics, from 2020 to the end of 2021, my country has approved a total of 64 million tons of new coal mine production capacity, and half of the production capacity is located in Xinjiang, far away from major coal consumption areas. The coal industry as a whole is in short supply.

As a result, since 2021, my country has experienced a shortage of coal, especially thermal coal. For two consecutive years, there have been unavoidable measures such as power cuts and production restrictions. The price of coal continues to rise. Starting from September 2021, coal The supply guarantee policy has not been withdrawn, and the existing production capacity continues to be produced at full capacity under high pressure.

In order to alleviate the shortage of supply, a series of measures have been introduced to ensure supply growth, mainly including: legalization of off-balance-sheet production capacity, approval of land use for open-pit coal mines, increase of existing coal mines or reconstruction and expansion to increase production capacity, speeding up the progress of coal mines under construction and approval of exploration rights, etc. As of August 2022, my country’s coal output is 2.93 billion tons, an increase of 11% year-on-year. However, the supply and demand of coal still maintain a tight balance, coupled with insufficient water in the rainy season. In August, large areas of the country once again restricted enterprises and high energy consumption.

Due to the gradual completion of the construction of coal mines with relatively low comprehensive costs, according to the “China Mineral Resources Report” in 2022, by the end of 2021, my country’s coal resource proven reserves and credible reserves totaled 207.9 billion tons, according to the reserve coefficient of 1.3 and the 2021 According to the production calculation, it can be mined for 40 years, but 25% of the production capacity is located in Xinjiang, and the transportation cost is high.

Secondly, in terms of industries, the substitution of coal is a long-term process.

Coal is mainly used in power generation, heat supply, steel, building materials, and chemical industries. In terms of actual functions, it is mainly divided into steam coal as power raw material, coking coal used as smelting principle, and chemical coal used as chemical raw material. Are there other raw materials that can replace coal?

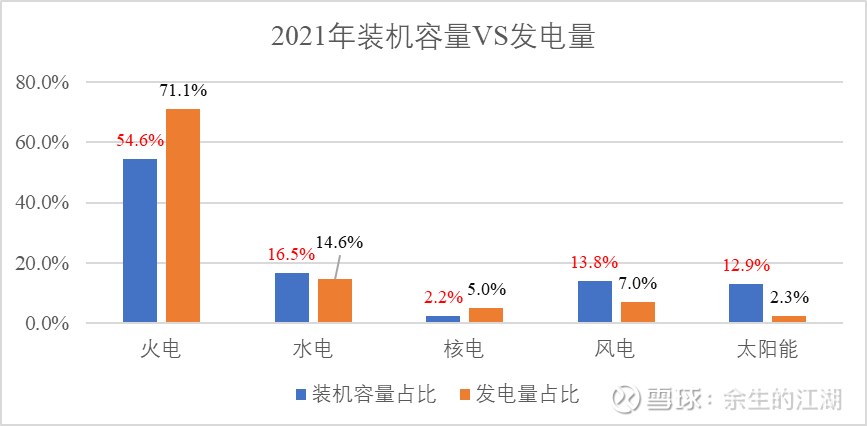

Let’s first look at the power generation business, which accounts for 56.7% of the total coal consumption. Figure 4 shows the installed capacity and actual power generation of various types of power generation in my country by the end of 2021. Among them, thermal power (including a small part of other fuels) produces 71% of the electricity with 54.6% of the installed capacity. Thermal power still occupies an absolute dominant position in terms of output, and its power generation efficiency is second only to nuclear power.

As a substitute, hydropower produces 14.6% of electricity with 16.5% of its installed capacity, and its efficiency is acceptable. However, my country’s economically developable hydropower installed capacity is about 400 million kilowatts, and the development of major rivers has basically been completed, and the future increment will be limited.

Due to issues such as safety, public opinion and site selection, the installed capacity of nuclear power in my country is only 2%, and the alternative power provided is only 5% and the growth rate is slow.

Therefore, wind power generation and photovoltaic power generation are expected to be high as clean energy sources. However, the efficiency of wind power and photovoltaics is very limited. By the end of 2021, the installed capacity of wind power and photovoltaics will reach 26.7%, reaching 630 million kilowatts, but only less than 10% of the electricity (about 750 billion kilowatt-hours) will be produced.

Figure 4. China’s power energy structure and proportion of power generation

The low efficiency means that to replace coal power, wind and photovoltaics still need a long time for infrastructure construction, including the construction of power transmission facilities. Constraining the progress of infrastructure In addition to cost, wind power and photovoltaic power generation are intermittent, uncontrollable, and inconsistent with demand. The grid needs energy storage facilities to ensure the grid connection of intermittent energy. The construction of energy storage facilities will take decades time and high capital expenditure. Take the more economical pumped storage as an example. At present, the installed capacity of pumped storage in my country is only 30 million kilowatts, which is far from enough for peak regulation and frequency regulation for unstable energy sources. Therefore, the country issued Document No. 633 to further promote capital investment in pumped storage. However, the construction cycle of pumped storage power stations is relatively long. The current plan is to reach 60 million kilowatts during the “14th Five-Year Plan” and 120 million kilowatts during the “15th Five-Year Plan”.

Therefore, for a long period of time in the future, it is difficult to fundamentally change the status quo of coal power as the main power generation method in my country and coal as the main power generation fuel.

As a metallurgical raw material, my country consumes nearly 600 million tons of coking coal every year. In the “Carbon Neutral Roadmap of China’s Energy System”, it is hoped that through technological changes, hydrogen will be used as a reducing agent to replace coking coal. However, the cost of this process is very high. Both the production and storage of hydrogen, as well as the hydrogen reduction scheme itself are still in the demonstration stage, and there is still a long way to go before commercialization.

Although my country’s large-scale infrastructure has entered a plateau, the demand for coking coal may decline in the future, but as “panda coal”, the supply of coking coal will decline faster.

In terms of chemical coal, under the resource background of “rich coal, low oil, and poor gas” in my country, coal chemical industry has always been the direction of coal use supported by policies, and it can better reflect the commercial value of coal. Modern coal chemical industry can realize clean and efficient utilization of coal, which is an important way to promote the structural adjustment of the coal industry. Therefore, the demand for chemical coal will continue to increase in the future, and there is no substitution problem.

Based on the above, the huge coal demand base caused by the resource structure, the continuous pressure on economic coal supply and the long-term replacement cycle constitute the first logic of coal investment.

Logic 2: The low cost that is difficult to replicate is the core advantage of coal enterprises

Under the same use, coal, as an undifferentiated product, has no brand premium. Therefore, it is the comprehensive cost of coal that builds the core competitive advantage of the enterprise, including the comprehensive cost of mining and transportation cost. The coal mining industry is a typical pre-expense industry, that is, the main cost and resource endowment have been formed when the coal mine construction is completed, and depreciation and amortization are the main costs on the future profit and loss statement. Transportation costs depend on the location of the coal mine. This means that although there is no difference in products between coal mines, resource endowments are inherently different and cannot be compensated through acquired efforts, and the cost per ton of coal is very different.

The impact of the resource endowment of coal mines on cost includes:

1. The depth of the coal seam.

The depth of the coal seam determines whether the development method is open-pit mining or mine mining, and whether the mine is constructed with a vertical shaft or an inclined shaft. The cost of open-pit mining is the lowest. Generally, the cost per ton of coal is only 70-90 yuan/ton, but the calorific value of coal in open-pit mines is relatively low; the cost of coal per ton in inclined shafts is lower than that of vertical shafts. Coal and gangue are more expensive than mines with shallow coal seams. At present, coal burial depths in Shaanxi, Shaanxi, and western Inner Mongolia are lower than those in the central and eastern regions.

2. The thickness of the coal seam.

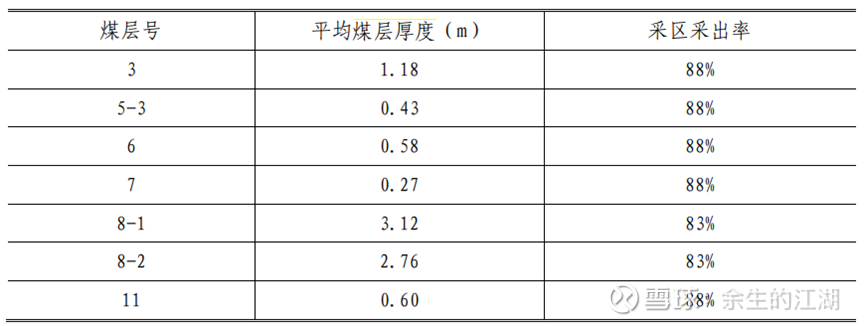

The thickness of the coal seam affects the efficiency of coal mining, thereby affecting the cost per ton of coal. Take the Xinhu Mine of Huaibei Mining Co., Ltd., which will be put into production in 2021, as an example. As shown in Figure 5, only the No. 8 coal seam has an average thickness of 3 meters, and the other coal seams are thin coal seams. 6 meters.

Figure 5. The coal seam thickness table of Xinhu Coal Mine (data comes from the public report of the coal mine)

1. Coal seam inclination.

The mining cost increases with the increase of the coal seam inclination, and the excessive increase of the coal seam inclination may even change the mining method of the coal mine.

2. The stability of the coal seam

In addition, complex underground conditions, such as drainage and gas disaster management, also directly affect the production capacity of coal mines. For example, the coal mines of Huaibei Mining generally have complicated geological conditions, and basically the output is difficult to reach the approved production capacity.

Therefore, low-cost coal mines have a competitive advantage that cannot be replicated, and the cost per ton of coal in a coal mine directly depends on resource endowment and geographical location. Therefore, the necessary homework for investing in coal is to understand the resource endowment and location of the coal mines under the company one by one. The main reason why coal is often regarded as a “cyclical stock” is that the unpredictable demand side makes the future price of coal difficult to predict. But no matter how the coal price changes, low-cost coal mines will always remain invincible. Just as the entire coal industry lost money in 2015, China Shenhua is still profitable.

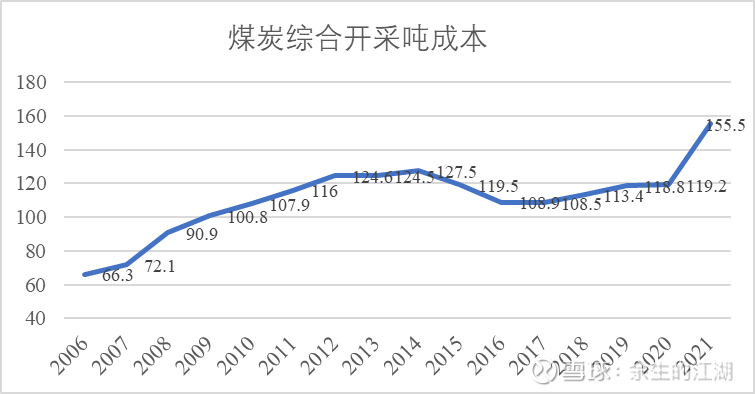

Of course, in addition to geographical location and resource endowment, the cost of coal will rise to a certain extent with the mining progress of coal mines, rising labor costs and other reasons. Taking Shenhua as an example, the figure below shows the trend of Shenhua’s cost per ton of coal in the past 15 years.

Figure 6. Change trend of China Shenhua’s coal cost per ton

It can be seen from the figure that Shenhua’s cost per ton of coal has gradually increased with the rise of coal prices, from 66 yuan to 127 yuan in 2014; after the coal price fell, Shenhua’s cost per ton of coal gradually dropped to 108 yuan, but the cost The bottom price is much higher than the 66 yuan in 2006. Later, as coal prices stabilized, the cost per ton of coal did not change much until 2021 when coal prices rose sharply, and the cost per ton of coal increased to 155 yuan.

The factors driving the increase in the cost of ton of coal the day after tomorrow are: first, the increase in labor costs, which increased from 8.5 yuan to 36.6 yuan; , the cost of raw materials, fuel and so on has increased to a certain extent.

The above two logics, the first logic solves the problem of how to view the future development of the coal industry, and the second problem solves the problem of how to view specific coal companies, which are issues that must be considered when investing in coal stocks.

In addition, in the process of understanding the coal industry, we should also pay attention to the following details:

Detail 1: The relationship between production and reserves

Output is one of the two major factors that determine a company’s revenue. Generally, coal companies will disclose the output of the year in their reports.

First of all, we should pay attention to the caliber of enterprise disclosure. Some enterprises disclose the output of raw coal, and most of them disclose the output of commercial coal. Especially for coking coal enterprises, the washout rate of coking coal is only about 50%, so the quantity of raw coal and commercial coal varies greatly.

Secondly, we should pay attention to the product structure and the proportion of sales and self-use. Taking Huaibei Mining as an example, it will produce 22.58 million tons in 2021, but only 19.76 million tons will be used for sales, and the rest will be used for the production of coke; 10,000 tons is coking coal, and the others are more than 6 million tons of steam coal, medium coal and coal slime. For thermal coal-based enterprises, some high-quality coal will also be sold as chemical coal in order to obtain higher sales prices.

Finally, pay attention to the output trend, especially when you find that the output of the company is gradually declining, you need to pay attention to whether the reason behind it is long-term. For example, China Coal’s Pingshuo has a decline in production and an increase in coal costs per ton due to the Luzigou anticline.

The output affects the current profit of the enterprise, while the reserves determine how long the profit of the enterprise can last.

When an enterprise discloses reserves, it generally discloses the economic reserves of the Chinese standard and the reserves of the JORC standard. The Chinese standard originated from the former Soviet Union. Although it has been updated several times, it is not recognized by international counterparts. Coal companies listed abroad must disclose reserves under the JORC standard. The JORC standard originated from Australia and is an internationally recognized mineral classification standard. Conservatively, it is recommended to use the JORC standard to measure the coal reserves of enterprises.

In the process of coal mining, losses will inevitably occur. Therefore, when evaluating the mining life of a coal mine, it is necessary to use a resource reserve factor based on the mining conditions of the coal mine. Generally, 1.3 is used for coal mines with simple geological conditions, 1.4 is used for moderate geological conditions, and 1.5 is used for complex mines.

The mining life of the coal mine = coal reserves / (reserve factor * output)

Detail 2: Coal price mechanism

The price of coal is complicated, and can be divided into pit mouth price, vehicle board price, sewage price and so on according to the sales form. Among them, the common pit-mouth price is also called the ex-factory price, which refers to the price at which coal leaves the mine. Launched water price refers to the price of coal reaching the waterway through various connection transportation. Generally, 5,500 kcal of Bohai Rim thermal coal is used as the standard product of launched water coal.

As mentioned earlier, coal is mainly used for electricity, building materials, steel and chemicals. Since my country’s current electricity price is planned electricity, and electricity and winter heating directly affect people’s livelihood, the price of this part of thermal coal is strictly regulated. The price exists in the form of “long-term contract price” for thermal coal, and the pricing form of “long-term contract price” will also change with the game of coal and electricity.

In May 2022, the National Development and Reform Commission issued the “Notice on Further Improving the Coal Market Price Formation Mechanism”, which stipulates that starting from May 1, the reasonable price range for water coal (5,500 kcal) at Qinhuangdao Port is 570 yuan per ton ~770 yuan, Shanxi, Shaanxi, and Mengxi coal (5,500 kcal) reasonable price ranges for the mining link are 370 to 570 yuan per ton, 320 to 520 yuan, 260 to 460 yuan per ton, and Mengdong coal (3,500 kcal) card) The reasonable price range for the mining link is 200 to 300 yuan per ton. After the implementation of the policy, the “long-term agreement price” of seaborne coal in Qinhuangdao Port has been maintained at 719 yuan/ton.

As for coal for other purposes, it is basically sold at the market price, and the price control is not strict. However, due to the existence of the supply guarantee policy, more thermal coal is sold to power plants at the “long-term contract price”. In the case of little change in the total amount, the supply for other purposes will become more scarce, and the price of this part of coal will soar. At present, the spot quotation of 5,500 kcal in ports around the Bohai Sea exceeds 1,500 yuan/ton, far exceeding the “long-term agreement price”, and the operating profits of building materials and chemicals in the downstream of the industry generally decline.

The price of coking coal is not under price control. In order to alleviate the large fluctuations in coking coal prices, some coking coal companies negotiate with downstream customers and sell in the form of “long-term contract prices”, generally based on “annual lock-in volume and quarterly lock-in prices”. Form, the coking coal sales price of the quarter is determined at the beginning of each quarter.

In addition, different coal companies have different sales ratios between “long-term contract price” and “spot price”, which directly affect the sales amount and flexibility of the company. For example, about 90% of China Shenhua’s coal is sold in the form of “annual long-term agreement”. Therefore, no matter how the spot price fluctuates, as long as the “long-term agreement price” remains unchanged, the change in Shenhua’s sales is very limited. The “long-term association” ratio of Shaanxi Coal Industry is about 50%, so in the case of rising spot prices, sales are more flexible.

Detail 3: Taxes affect profits

In addition to mining cost per ton of coal and transportation cost, taxation is also one of the main elements of cost composition. The main types of taxes in coal mines include value-added tax, urban maintenance and construction tax, resource tax and corporate income tax. The resource tax and corporate income tax deserve attention.

Resource tax is a kind of land tax. It is “ad valorem” for raw coal or processed coal. The tax rate is generally between 2% and 10%. Because it is a land tax, provinces with net coal exports tend to increase tax rates, while coal net imports Provinces tend to have lower tax rates. For example, the “Three West” regions continue to increase the tax rate of resource tax. Inner Mongolia will increase the tax rate from 9% to 10% in 2020, while Anhui will maintain the coal resource tax rate at 2%. With the rise of coal prices, this part The impact on cost is more prominent.

In 2007, China Shenhua’s resource tax per ton of coal was about 3.2 yuan. With changes in tax calculation methods, tax rate increases, and rising coal prices, the resource tax per ton of coal in 2021 will be equivalent to 40 yuan. During the same period, the resource tax per ton of coal in Huaibei, Anhui was below 15 yuan.

The corporate income tax also has a relatively large impact on the profits of coal mines. Generally speaking, the corporate income tax rate is 25%, but the tax rate for coal mines that enjoy the “Western Development” preference is 15%. At the same time, some coal mines with complex geology enjoy the preferential tax rate for “high-tech enterprises” due to their high R&D expenses . Changes in tax policy can have a significant impact on corporate profits.

Detail 4: Historical baggage

The historical burden deposited in each coal mine may be heavy or light, and the personnel are the direct embodiment of the historical burden. Therefore, although the historical construction cost of some old mines is relatively low, they have a relatively large surplus of personnel, while the pressure on personnel in new mines is relatively light.

A typical case is Huaibei Mining. Most of its coal mines have a relatively long history. Although the coal production is only 22 million tons, it bears the salary of 73,000 people. The cumulative salary expenditure in 2021 is 7.8 billion, accounting for 27.2% of the main business income. (excluding trade coal). As a reorganized listed company, Shaanxi Coal Industry has left the historical burden at the group level. The listed company has achieved 140 million tons of coal production, and the number of employees to be borne is only about 38,000. In 2021, the salary expenditure is 8.5 billion, accounting for only Self-produced coal accounted for 10.8% of operating income, and employee efficiency was much higher than that of Huaibei Mining.

In general, the factors affecting the profit of coal mines are relatively complex, and resource endowment, sales structure, price structure, location differences, taxation, and personnel burden have different impacts on coal mines. The price of coking coal is higher but the cost of mining is higher. The cost of mining in the “Three West” area is lower but the transportation cost and resource tax rate are significantly higher. Although the coal mines in the central and eastern regions are close to the coal consumption area, the mining cost is generally high and the labor burden is heavy. Therefore, specific analysis of specific coal mines is required to achieve “one discussion per case”.

the future of coal

Does coal have a future? This is an era when words must talk about “double carbon”. This is a bad era for the coal industry, but it is also a good era for the coal industry.

After the “double carbon” was proposed, firstly, the wind power and photovoltaic power generation sectors ushered in explosive growth, and wind and light equipment companies experienced a sharp rise in both operating performance and stock prices. Then the wind came to the operation of wind and photovoltaics. In 2021, the share price increase of operating companies will be far greater than the performance growth, and energy storage, electric vehicles, etc. will also fluctuate in the wind. Surprisingly, the coal industry, which is regarded as a sunset industry by the public and is extremely undervalued before 2021, has also ushered in an explosion in operations and stock prices.

There is no other reason: the increase in demand for coal is greater than the increase in supply.

These were bad years for the coal industry.

In the next few years, with China’s economic restructuring and transformation, coal demand will peak and decline slowly. The economic structure that relied too much on investment in the past will gradually tilt towards consumption, and industries such as building materials and steel that have entered a plateau will gradually decline in demand for coal in the future.

The upgrading and transformation of the industrial structure will also improve the efficiency of energy utilization. In the power sector, although the trend of power electrification will bring about an increase in electricity consumption, there is room for growth in the primary industry, the tertiary industry, and residential electricity consumption, but the secondary industry, which accounts for 67% of the total electricity consumption, has a significant impact on electricity consumption. Demand will gradually stabilize, and industries with high energy-consuming demands may be restrained to a certain extent in the future.

In addition, with the advancement of technology, capital investment and gradual improvement of infrastructure, the increase in demand and a part of the stock will be gradually replaced by other raw materials and energy forms, which is the only way to “carbon neutrality”.

This was also a good age for the coal industry.

Coal production capacity in the central and eastern provinces with large energy consumption is rapidly depleting, and the capital expenditure of coal under the “double carbon” is suppressed, which affects the supply of coal. At the same time, under the relatively low coal price, the construction of coal mines with low comprehensive cost has been basically completed, and the competition pattern of coal supply has become clear. For low-cost coal mines, future operating profits will be more secure.

The capital expenditures of China’s three largest coal companies also reflect the fact that low-cost coal mines have decreased: China Shenhua’s new capital expenditures in coal are only newly launched Xinjie Project, the profits earned in the past few years, or in the form of cash Exist or invest in thermal power and railway sectors, and new energy operations have gradually begun to test the water. With the commissioning of Dahaize Coal Mine, China Coal’s coal capital expenditure is also coming to an end, and the asset-liability ratio has steadily declined. The 2021 performance communication meeting disclosed that it will carry out certain new energy operations in the future. After the “Xiao Bao Dang” project, Shaanxi Coal Industry has no new coal mine expenditure in the short term, and has also invested surplus funds in new energy and new materials in recent years.

Therefore, in the context of the gradual reduction of capital expenditures, more profits generated by coal mines will be fed back to shareholders in the form of dividends. For example, China Shenhua’s dividend rate in 2021 has reached 100%, and there is still a large amount of cash on the books.

Is the current price suitable for investment? This is a matter of opinion. The answer depends on one’s perception of the business and risk appetite (discount rate). The value of an enterprise does not depend on the four-fold increase in the stock price in the past, nor does it depend on the current static dividend rate exceeding 10%, but only on the discounted free cash flow during the duration. Due to different cognitions, each person’s free cash flow assessment of the company is very different, and the discount rate is different for different risk preferences, and the final value is also a very personal number.

I firmly believe that although the demand for coal will peak in the short term, coal companies with excellent resource endowments still have a bright future and good investment opportunities.

The above text only represents personal understanding and cognition of the coal industry, and the cases listed in the article are used to demonstrate the arguments. At the same time, individuals who hold coal shares are inevitably biased in cognition. Please think rationally. Any opinions and cases in this article are not considered as investment advice.

There are 72 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/8745459979/237590829

This site is only for collection, and the copyright belongs to the original author.