Multi-asset strategy index generally achieves higher returns at lower risk levels through dynamic portfolio management of multiple low-correlation assets.

There are many multi-asset index issuers, including banks, securities companies, and China Securities and other index compilation institutions. Minsheng Bank, China CITIC Bank, Shanghai Pudong Development Bank and other institutions publish these indices in order to issue embedded option wealth management products linked to these indices. Brokerage companies have also released such indices, such as CITIC and CICC. They release these indices as the underlying assets of the OTC derivatives business. The indexes they publish have a feature, many of which are related to stock index futures, which is convenient for hedging and leverage.

In addition, CSI will also independently or cooperate with other institutions to compile relevant indexes as performance benchmarks for some products or to issue index tracking products.

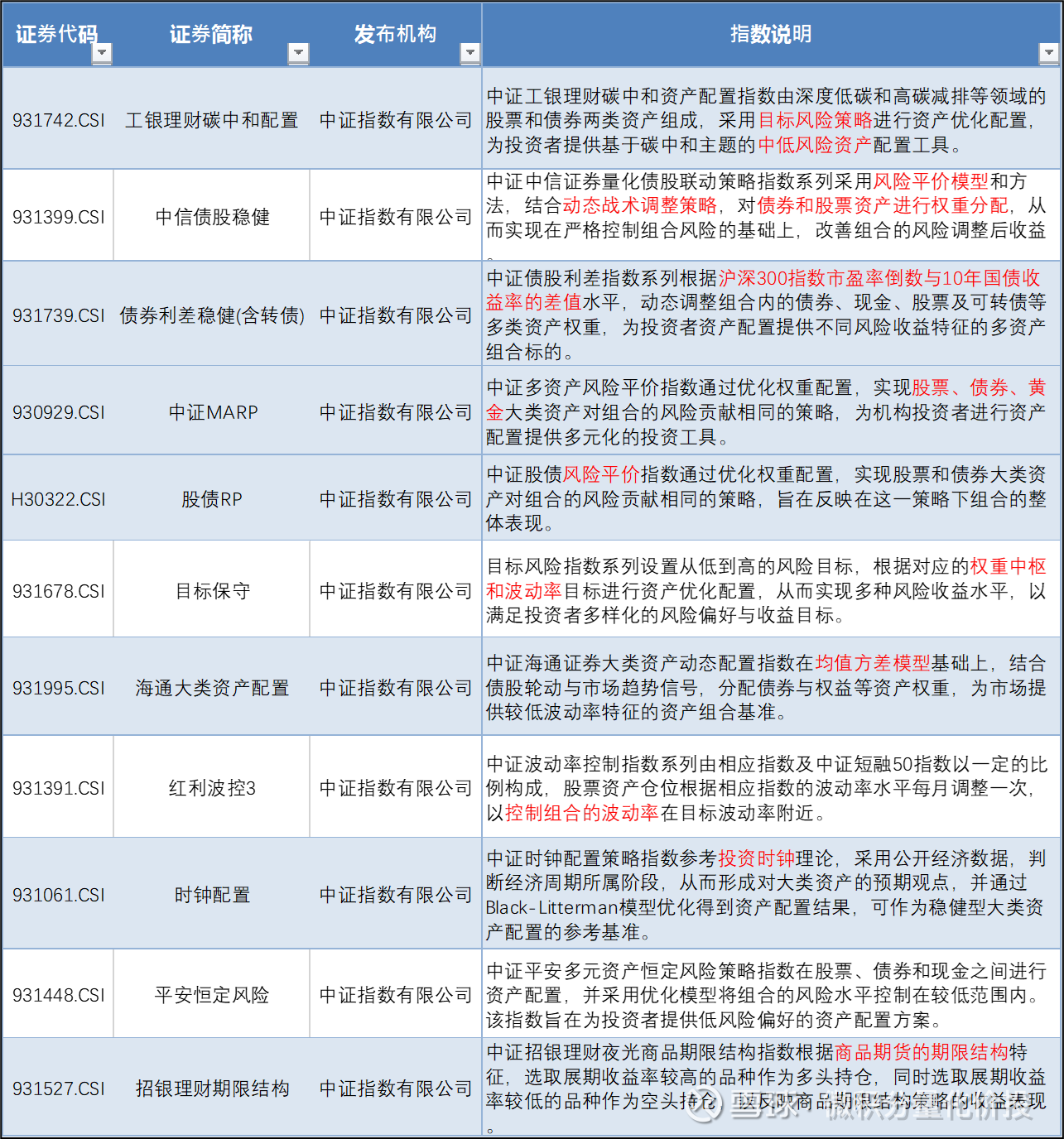

Through the following table of several common multi-asset indices, you can probably understand the characteristics of these indices.

In terms of assets involved, mainly stocks, bonds, gold and futures, and quantitative risk management methods will be used to control the risk of the portfolio, such as risk parity, mean-variance model, etc. Among them, there are indexes with pure quantitative strategies, and there are also multi-asset indexes with subjective judgments, such as clock allocation strategies.

Robust strategy

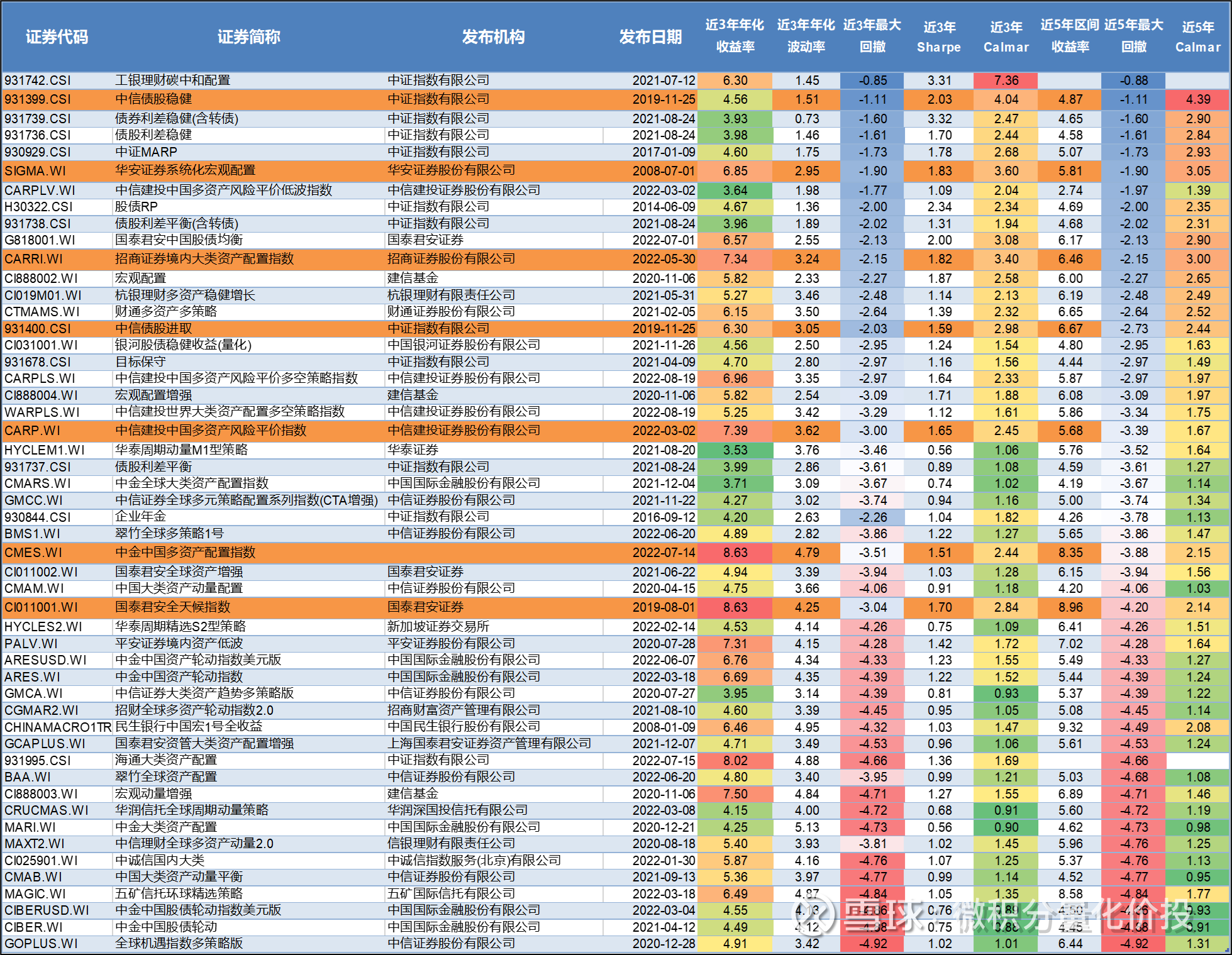

A robust strategy is defined as a maximum drawdown of no more than 5% over the last 5 years. The following performance statistics deadline: 2022-08-23.

Among them, there is a multi-asset index: Haitong Hedging Select. Select a hedge fund index with better performance (market neutral strategy). The historical performance of this index must be very good, because the best-performing private equity hedging strategies are selected, but because these products are basically restricted, you cannot copy this index, so this index is deleted from the table.

From the perspective of historical data statistics, the major asset categories with relatively good historical performance are:

ICBC Wealth Management’s carbon neutral allocation (mainly carbon neutral stocks contribute income, and the future sustainability may be average)

CITIC bond stocks are stable (the Calmar ratio is quite high, but the yield is a little lower)

CITIC Bonds and Stocks Progress

Huaan Securities Systematic Macro Allocation

China Merchants Securities Domestic Asset Allocation Index (Compiled in May 2022, too little out-of-sample data)

CSC China Multi-Asset Risk Parity Index (too little out-of-sample data)

CICC China Multi-Asset Allocation Index (too little out-of-sample data)

Guotai Junan All Weather Index (compiled in 2019, relatively speaking, there are more out-of-sample data, and it is relatively stable)

After the overall screening, there are two indicators to focus on:

CITIC bond stocks are stable, CITIC bond stocks are aggressive (there is currently no tracking product, you may need to build it yourself)

Guotai Junan All Weather Index (The index can be directly invested in through OTC options, swaps, etc.)

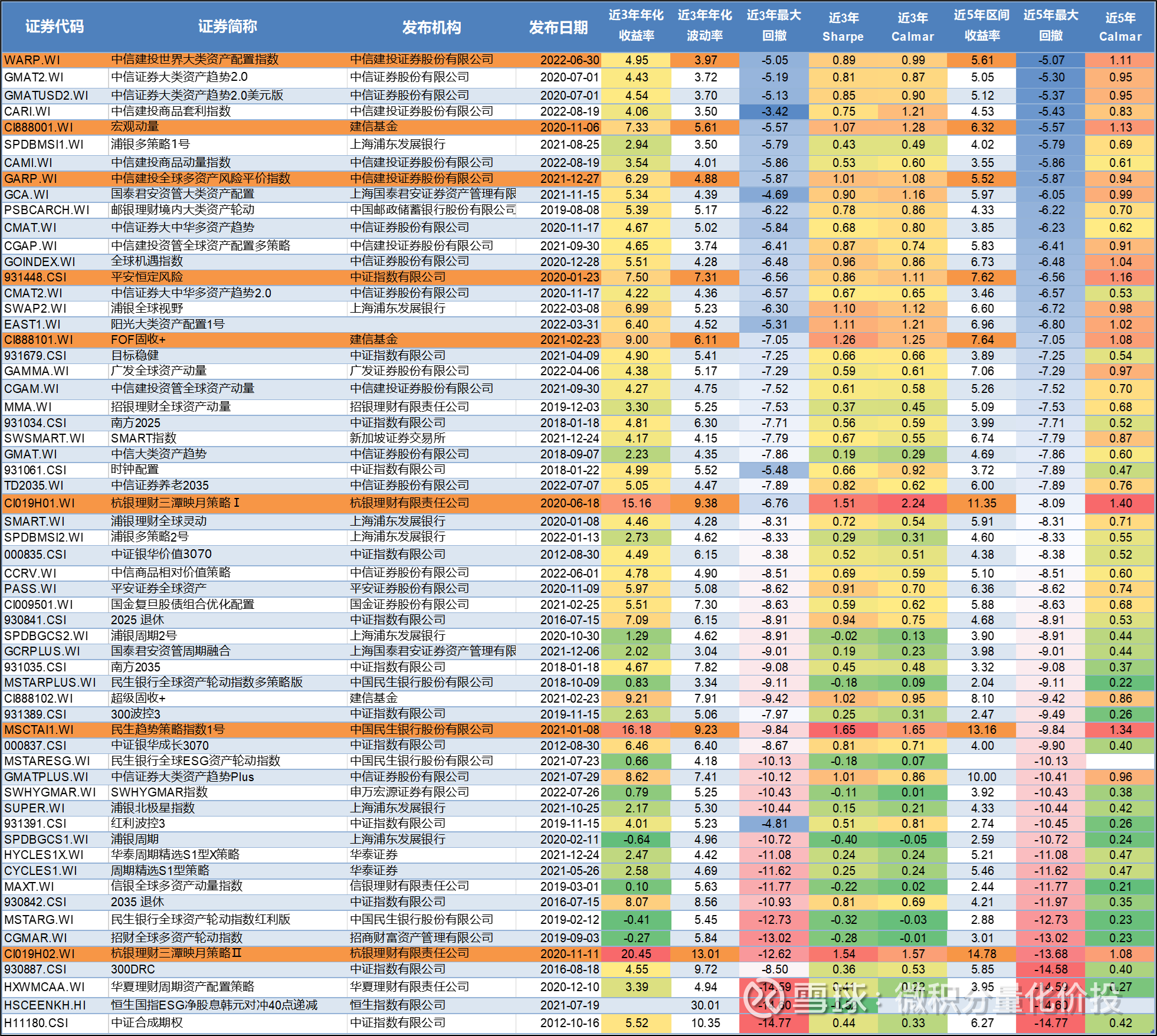

Balance strategy

A balanced strategy is defined as a maximum drawdown between 5% and 15% in the last 5 years.

From the perspective of balancing strategies, the compilation time of many indices is relatively short, and the out-of-sample data is insufficient. Relatively noteworthy are:

Macro Momentum (CCB Fund)

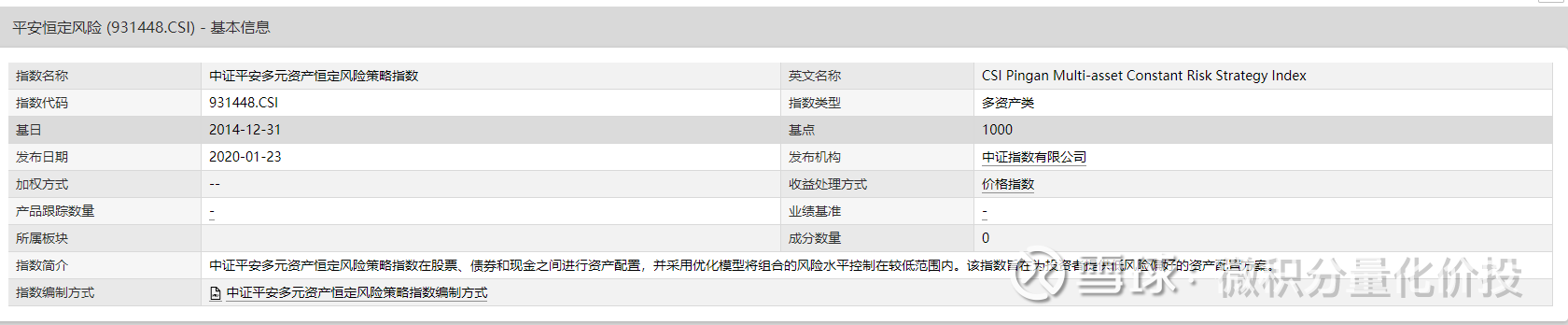

Ping An constant risk

FOF Fixed Income+ (CCB Fund)

People’s Livelihood Trend Strategy Index No. 1

Among them, Ping An’s constant risk information is relatively more:

From the perspective of the compilation rules, it is not a purely quantitative strategy, which combines expected returns, and the estimated time window lengths for annualized volatility and correlation coefficients are inconsistent. The reproducibility of this index is more difficult,

CCB Fund Macro Momentum Strategy:

The macro factor momentum strategy index adopts the idea of trend tracking, which is different from the existing momentum strategy index. The macro factor momentum strategy index aims to track the macro factor trend. Compared with asset prices, macro trends tend to last longer and are more stable. The macro factor momentum strategy index is based on a stock, bond, and commodity ratio of 25:70:5, and dynamically adjusts the allocation ratio to improve risk-adjusted returns. From the point of view of this compilation rule, it is also more difficult to replicate.

aggressive strategy

An aggressive strategy is defined as a maximum drawdown of more than 15% in the last 5 years.

Aggressive strategies can be given less attention. Generally, the best performances are the global allocations, including US stocks and so on. But the overall performance has been poor in the past 1-2 years, because US stocks, European stocks and other stocks are all falling.

There is little information about the major asset trends of CITIC Securities, but the content of the CITIC Securities research report can be speculated about the general principle.

summary

The ideal of a multi-asset strategy is better, but from a practical point of view, the overall investment value is not high. Due to the demand for over-the-counter derivatives, many brokerages have recently issued multi-asset allocation indexes, but these allocation indexes are released relatively late, and there may be over-fitting, and the extreme market conditions in the past two years are just the best test for these strategies. gold stone. After screening, only the Guotai Junan All-weather Index of the monarch has relatively investment value, and the others still need to be verified.

In addition, it is worth noting that the two indexes of CITIC bond stocks and CITIC bond stocks are both stable and aggressive. These two indexes have actually been introduced in previous articles.

These two products do not have tracking products, but the compilation principle and the underlying assets involved are relatively simple, and you can consider implementing this index yourself.

At this point, the full text is over, thank you for reading.

If you find any mistakes or omissions in my analysis, your corrections and additions are welcome.

The above content is only used as a personal investment analysis record, and only represents personal opinions. The analysis content is based on historical data. Historical performance does not indicate its future performance. It does not serve as a basis for buying and selling, and does not constitute investment advice.

Like and watch, investment makes more ¥

#雪ball star plan public offering talent# #ETF star push officer# #calculus quantitative price investment#

@ Egg Roll Index Fund Research Institute @ Today’s topic @ Snow Ball Creator Center @ Egg Roll Fund @ golfer welfare

Quickly retrieve historical articles

$CSI 300(SH000300)$ $CSI 500(SH000905)$ $Hang Seng Technology Index(HKHSTECH)$

This topic has 1 discussion in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/4778574435/232600790

This site is for inclusion only, and the copyright belongs to the original author.