In the second quarter, the average selling price of PepsiCo products rose by 12%, and the revenue in the quarter exceeded expectations by more than 5% year-on-year. Earnings for the quarter were also better than expected. PepsiCo raised its global organic revenue growth rate this year to 10% from 8%. On Tuesday, July 12, Eastern Time, snack and beverage giant PepsiCo announced its second-quarter earnings before the market, thanks to strong consumer demand for packaged food and beverages, its quarterly earnings and revenue were better than expected. , PepsiCo raised its revenue growth forecast for this year.

Author: Porridge Seven

PepsiCo’s U.S. stock rose more than 1% in pre-market trading, but the decline narrowed after the early opening in New York fell.

Specifically, its core financial indicators:

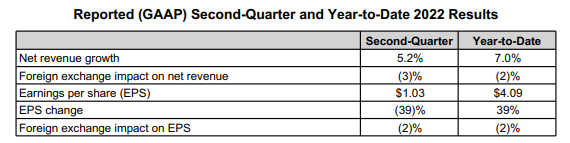

Second-quarter revenue of $20.23 billion was higher than the consensus estimate of $19.51 billion and a year-on-year increase of 5.2%. Second-quarter adjusted earnings per share of $1.86 beat analysts’ expectations of $1.74. Second-quarter profit was $1.43 billion, compared with $2.36 billion in the same period last year, down 39 percent year-on-year.

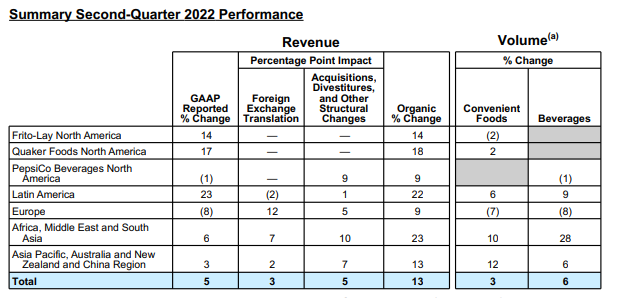

Specifically, look at the revenue performance of its product line in the North American market:

Frito-Lay North America’s organic revenue rose 14%, driven by sales growth at Cheetos and Doritos, but volume fell 2%, excluding the impact of pricing or currency fluctuations. Organic revenue in the North American beverage segment rose 9%, but its volume fell 1%, with Gatorade, Aquafina and Lifewtr recording double-digit growth in the quarter. PepsiCo sold its Tropicana juice business to private equity firm PAI Partners earlier this year, and the divestiture hit revenue. Quaker Foods was the only division in North America to post volume growth, with organic revenue climbing 18% and volume up 2%, helped by double-digit growth in rice and pasta, oatmeal and crackers.

In addition, PepsiCo also raised a key sales metric in its guidance, predicting a 10% increase in global organic revenue for the full year, up from an earlier forecast of 8% growth.

Chairman and CEO Ramon Laguarta said:

We are pleased with our second quarter results as we continued business momentum despite continued macroeconomic and geopolitical volatility and high levels of inflation in our markets.

Goldman Sachs analyst Bonnie Herzog believes that “the upward guidance is a good sign in a challenging environment and should be favored.”

We think the stock should outperform today on the back of better-than-expected Q2 results and a strong outlook. We reiterate our Buy (CL-based) rating on PepsiCo given its strong brand portfolio (especially Frito Lay) and long-term growth opportunities in beverages.

The soaring inflationary pressures facing companies still cannot be underestimated, said Bruce Richards, an analyst at Marathon Asset Management: “In terms of S&P 500 earnings, we believe we are heading for an earnings recession.”

Companies are squeezed in every way, they are squeezed in everything from the cost of goods, to wages, and to manufacturing goals or service inputs. On the other hand, we believe that corporate revenue growth will gradually slow and decline as interest rate costs rise. Due to the increase in fees, many corporate ratings will be downgraded, and the potential risk of systemic default will greatly increase.

Confronting Rising Cost Pressures: Raise Prices, Cut Volumes, and More

PepsiCo reported a 5.2% year-over-year increase in second-quarter revenue mainly due to a 12% increase in its average selling price. In recent months, PepsiCo has raised prices to help offset rising costs for trucking, packaging and agricultural commodities. Compared to the same period last year, prices rose 10% in the first quarter of this year and 7% in the fourth quarter of last year.

The global food and beverage giant also expects costs to rise even higher in the second half of the year, and in addition to raising prices to shift costs, PepsiCo said it plans to continue downsizing its products and deploy other ways to manage rising expenses.

Laguarta said PepsiCo and its retail partners are also continuing to pay attention to how inflation affects low-income shoppers, by making decisions on different categories of entry channels, such as in some communities, PepsiCo will offer more such as Santitas Cornflakes. Low price product.

In addition, Laguarta also warned that a recession is likely to come, saying that PepsiCo is preparing for different scenarios, with potential plans including reducing capital expenditures, increasing automation and shifting investment from growth to productivity.

Profits shrink, in addition to inflation and the blow from the Russian-Ukrainian conflict

An earlier article in Wall Street News mentioned that since the deterioration of the situation in Russia and Ukraine, there has been a rapid wave of “Russian withdrawal” among European and American companies. PepsiCo is no exception. PepsiCo, which has more than 20,000 employees in Russia, has suspended its global Sales of beverage brands in Russia, including its namesake Coke, continued, but continued sales of food and local brands, including a major dairy company.

Compared with the increase in costs brought about by inflation, which squeezed its profits, Pepsi has been hit harder by the Russia-Ukraine conflict. Judging from the financial report, expenses related to the Russian-Ukrainian conflict this quarter were $1.17 billion.

In midday trading on Tuesday, PepsiCo rose slightly, with PepsiCo down 1.3% year-to-date, outperforming the S&P 500’s decline of more than 19% over the same period.

media coverage

CNBeta

This article is reprinted from: https://readhub.cn/topic/8hAWUBhE9xi

This site is for inclusion only, and the copyright belongs to the original author.