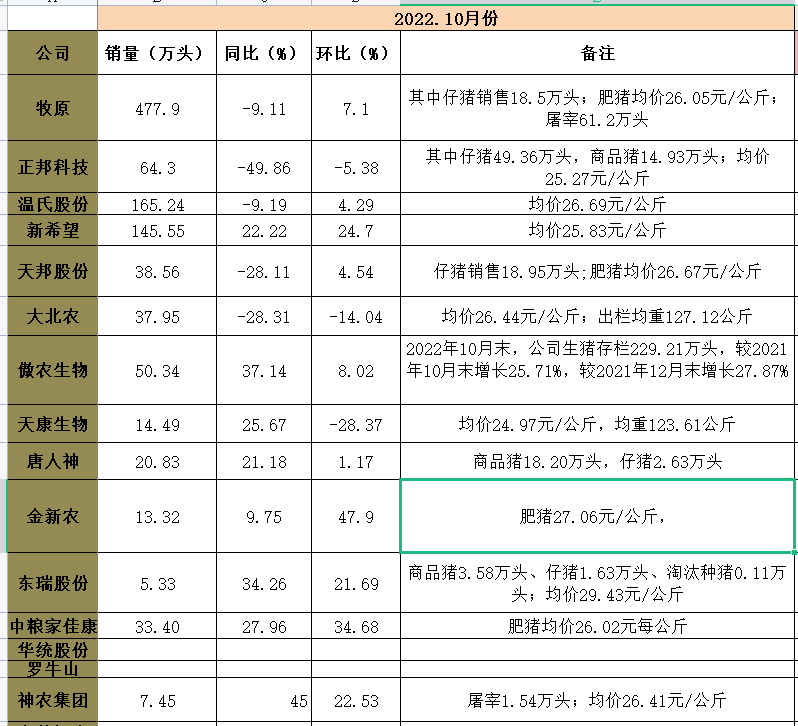

The pig fell in Pingyang and was bullied by the chicken. Pig stocks have always been the most worthy investment sub-sectors in the agriculture and animal husbandry industry. However, due to the pig cycle launched in July 2021, the amount of pig stocks has been greatly increased in advance, and due to the lack of understanding of the reversal of the pig cycle by various funds, the pig stocks have not been pushed up in the early stage. . After the cycle really reverses, all kinds of funds, including fund managers, will also take the attitude – I admit that I am wrong, but I am not very good at buying pig stocks. Makes this cycle a bit incomplete. We still organize the data of listed companies’ sales volume as always, as follows:

After entering October, the pig stocks with a year-on-year increase in slaughter volume are basically small stocks: Aonong Bio, Tiankang Bio, Tangrenshen, Jinxinnong, Dongrui, COFCO Jiajiakang, New Hope, Shennong Group.

The negative growth is $ Muyuan shares (SZ002714) $ $ $ Wen’s shares (SZ300498) $ , Zhengbang Technology, Tianbang shares, Dabeinong.

The positive month-on-month growth is also good, because the average price in October is higher than that in September, which means that the supply is less than that in September. Of course, there is a pressure factor, but the rhythm is also a reference dimension.

On the other hand, the white feather chicken has been going very strong recently. The cycle of white-feather chickens is short and the cycle is not strong. The only thing is that the breeding chickens are imported from overseas, and there will be a shortage of supply due to epidemics and customs closures, resulting in market conditions.

Analysts believe:

Since last year, the overseas avian influenza epidemics in countries represented by the United States and Europe have continued to ferment, and the current severity has hit a new high in recent years. An Weijie was also affected by the epidemic in Tennessee, the main producing area of the United States, in September. Alabama is currently the only state that can be introduced due to the avian flu epidemic.

Influenced by the avian influenza epidemic and superimposed flight problems, overseas introductions have continued to be low since May this year. In the short term, due to the inability to introduce avian influenza in Europe, the availability of breeders in the United States is reduced, and the probability of short-term flight restrictions is also low. In the first 10 months, the estimated number of new species introduced was 700,000, a year-on-year decrease of 33%. The estimated number of overseas species introduced in November was also 0.

The white chicken sector has been fluctuating at the bottom for nearly 2 years. The listed chicken seedling companies have been losing money for five consecutive quarters, and the industry’s production capacity has been partially reduced. We believe that the current industry bottom has passed, with low overseas introductions + reduced efficiency, parents in early 2023 Substitute supply may decrease, and the gap between chicken supply and demand may gradually expand in the second half of the year. It is recommended to focus on the development of Shengnong with independent and controllable seed sources, and Yisheng Shares/Minhe Shares of Chicken Miao Company. ![]()

This topic has 4 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1875334409/235023346

This site is for inclusion only, and the copyright belongs to the original author.