Risk warning: The content involved in this article is the investment strategy sharing at that time. Shanying International has a large amount of goodwill impairment and operating losses in 2022. Netizens are reminded to pay attention to related investment risks.

On the evening of October 13, 2022, I saw Shanying International issued an announcement that the board of directors proposed to repair Shanying convertible bonds. I opened my mouth and stared at the screen for a long time, because I had a heavy position in the convertible bonds issued by Shanying International. Eagle 19 Convertible Bonds issued in 2019.

Very annoyed, this feeling is like a scheming girl trying her best to hook up with the handsome and young second son of a wealthy family. Just thinking that he has reached the pinnacle of his life since then, he suddenly saw the news that the second son was deprived of his inheritance rights and all his belongings were given to the eldest son. Thinking about losing his body and not getting any benefits, he was naturally sad and sad Angry. So for me, figuring out whether the second son’s inheritance rights may be reversed is the key to deciding whether to continue the love or ask for a breakup fee to leave.

Why did I buy Shanying convertible bonds?

In July 2022, hot money withdrew from the convertible bond sector, but the overall valuation of convertible bonds in the market was still high, and the price was too high to be bought everywhere. For horizontal comparison, I allocated some Shanying series convertible bonds with a not-too-long time to maturity, a fair premium, positive yield to maturity, and a rating of AA+.

I think that even if the subsequent convertible bond market weakens, the Shanying series with outstanding defensiveness should not fall much.

The Shanying series of convertible bonds also has a special profit point that most convertible bonds do not have, and that is the arbitrage value.

The first attribute: arbitrage

Shanying International issued a total of two convertible bonds:

For Shanying convertible bonds on November 21, 2018, the conversion price at the time point was 3.19 yuan, the maturity price was 113 yuan, and the unpaid two-year interest was 3.5 yuan. A total of 116.5 yuan.

For the Eagle 19 convertible bond on December 13, 2019, the conversion price at the time point was 3.15 yuan, the maturity price was 111 yuan, and the unpaid three-year interest was 4.4 yuan. A total of 115.4 yuan.

Both convertible bonds can be revised downward.

From the data, we will find that the conversion price of Eagle 19 is slightly lower than Shanying Convertible Bonds, so each Eagle 19 can transfer about 1.27% more shares than Shanying Convertible Bonds, and more than one year more options value.

However, the maturity principal and interest of Shanying Convertible Bonds is 0.9 yuan more than that of Eagle 19, and the time is shorter. With the same decline ratio, the rate of maturity increase will be higher than that of Eagle 19.

Therefore, the valuation of the Shanying series is very delicate. When the market is under attack, the reasonable valuation of Eagle 19 Convertible Bonds should be higher than that of Shanying Convertible Bonds. If the market is in a defensive state. The debt protection of Shanying convertible bonds is stronger, and the value will be higher than that of Eagle 19 convertible bonds.

Most of the time, the two convertible bonds of the Shanying series will rise and fall at the same time, but there will be differences in trends, resulting in a short-term gap in the prices of the two convertible bonds. I will set a certain threshold. Switching between, such an operation will have a little more profit than long-term holding. Because the underlying stock is the same, this kind of arbitrage will be very accurate, and it is less error-prone than arbitrage of convertible bonds in the same industry and demon-attributed convertible bonds.

This purchase of Shanying series is not the first time for me to operate them. Earlier, I used to do inter-industry convertible bond arbitrage between Shanying double bonds and Jingxing convertible bonds. Lee is out.

As the overall market weakens, the debt attributes of Shanying Convertible Bonds come into play, and the price difference between it and Eagle 19 Convertible Bonds is increasing. I have rotated to Eagle 19 early, and I can’t rotate to Eagle 19 after increasing my position. mountain eagle. I can only lie flat all the way, watching the two goods go down step by step.

On the evening of October 13, 2022, Shanying Convertible Bonds proposed a downward revision. I, who is full of Eagle 19 convertible bonds, need to think about whether Eagle 19 will also undergo downward revision at the same time. So as not to miss the more valuable convertible bonds in the future.

The second attribute: downward revision game

The downward adjustment terms of the two convertible bonds are very similar. When the closing price of the company’s stock is lower than 80% of the current conversion price for at least fifteen trading days out of any thirty consecutive trading days, the downward adjustment will be triggered, which can break through Net assets.

It is precisely because of the difference of 4 cents in the conversion price of the two convertible bonds that the Shanying convertible bonds were revised down in advance. The eagle 19 convertible bonds need to be two trading days earlier at the earliest, that is, on the evening of October 17 (with a weekend interval, 4 days later), the downward revision condition can be triggered.

The problem I am facing is:

If the Eagle 19 convertible bond, which has followed the trend, does not propose a downward revision on the 17th, it will face a compensatory decline. At the same time, if the Shanying Convertible Bonds are unilaterally revised down, its value will be greatly increased. Do I need to swap the uncertain Eagle 19 Convertible Bonds in advance to the already clear Shanying Convertible Bonds at an unclear time point in the market.

I made the following analysis:

The logic of promoting stock conversion (bearish):

There may be an out-of-synchronization revision, because Shanying convertible bonds mature one year earlier than Eagle 19, and the pressure to promote the conversion of Shanying convertible bonds into shares will be greater. It is more conducive to promoting the forced redemption of Shanying convertible bonds.

Historical attitude (favorable):

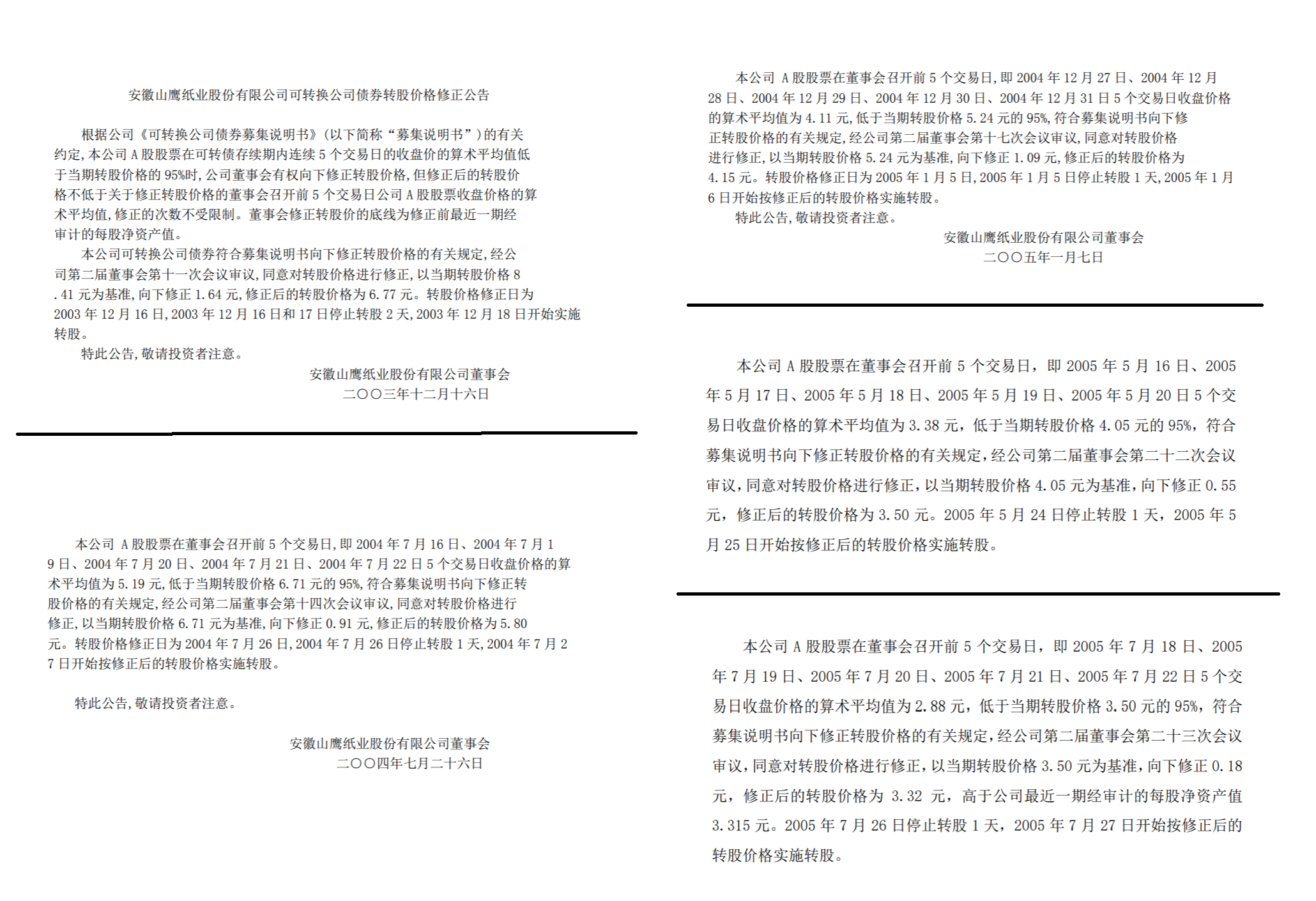

It is not the first time for Shanying International to issue convertible bonds. As early as 2003 and 2007, Shanying issued two tranches of convertible bonds, both of which lasted only two years before completing forced redemption. Both tranches of convertible bonds were revised down Record.

Among them, the downgrade clauses of Shanying Convertible Bonds in 2003 were astonishingly loose, and the downgrade could be triggered if it fell below 95% of the conversion price for five consecutive trading days. At that time, the downgrade could even be decided by the board of directors without going through the shareholders’ meeting The 2003 version of Shanying Convertible Bonds has been revised five times in two years, and the chairman of Shanying’s attitude towards convertible bonds is also comparable to that of directors, which can be called the ceiling of convertible bond directors. It’s just that nearly two decades have passed, and it’s unclear whether Shanying’s management can continue the original spirit.

Market trend (disk positive):

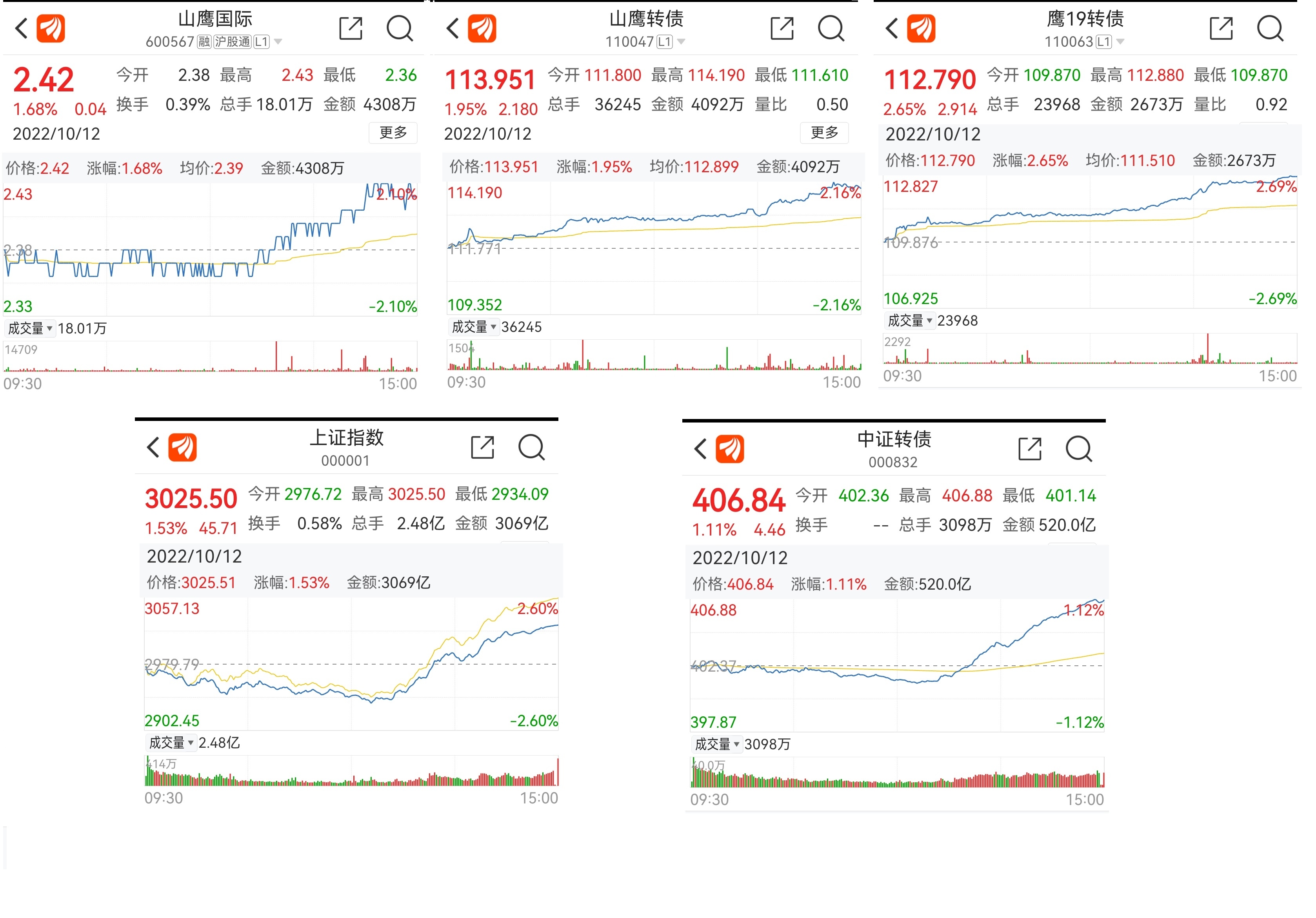

On October 12, 2022, just the day before Shanying’s convertible bonds announced a downward revision, Shanying and Ying 19 convertible bonds showed strange trends. Comparing the CSI Convertible Bond Index, Shanghai Composite Index, Shanying Positive Stock and the daily line of the two convertible bonds on October 12, the CSI Convertible Bond Index, Shanghai Composite Index, and Shanying Positive Stock all fell in the morning, hitting lows all the way After 1:30 p.m., it began to rise after 1:30 p.m. and continued until late trading. However, the two convertible bonds have risen against the market since the opening, which is not only different from Shanying International’s main stock, but also has nothing to do with the miserable green convertible bond market.

Such a trend in the market indicates that the result of the market judgment is that the two convertible bonds of Shanying may be revised down. Among the two convertible bonds, the low-priced Eagle 19 convertible bond is the leading one. This also shows the conclusion given to us by the market. It means that both convertible bonds will be revised down, not just Shanying convertible bonds. Because in the end, only the Shanying convertible bonds were revised down, then the Shanying convertible bonds should lead the rise, not the Eagle 19 convertible bonds.

This is a wild judgment call, but I believe markets are efficient.

Maximum Uncertainty (Maximum Bearishness)

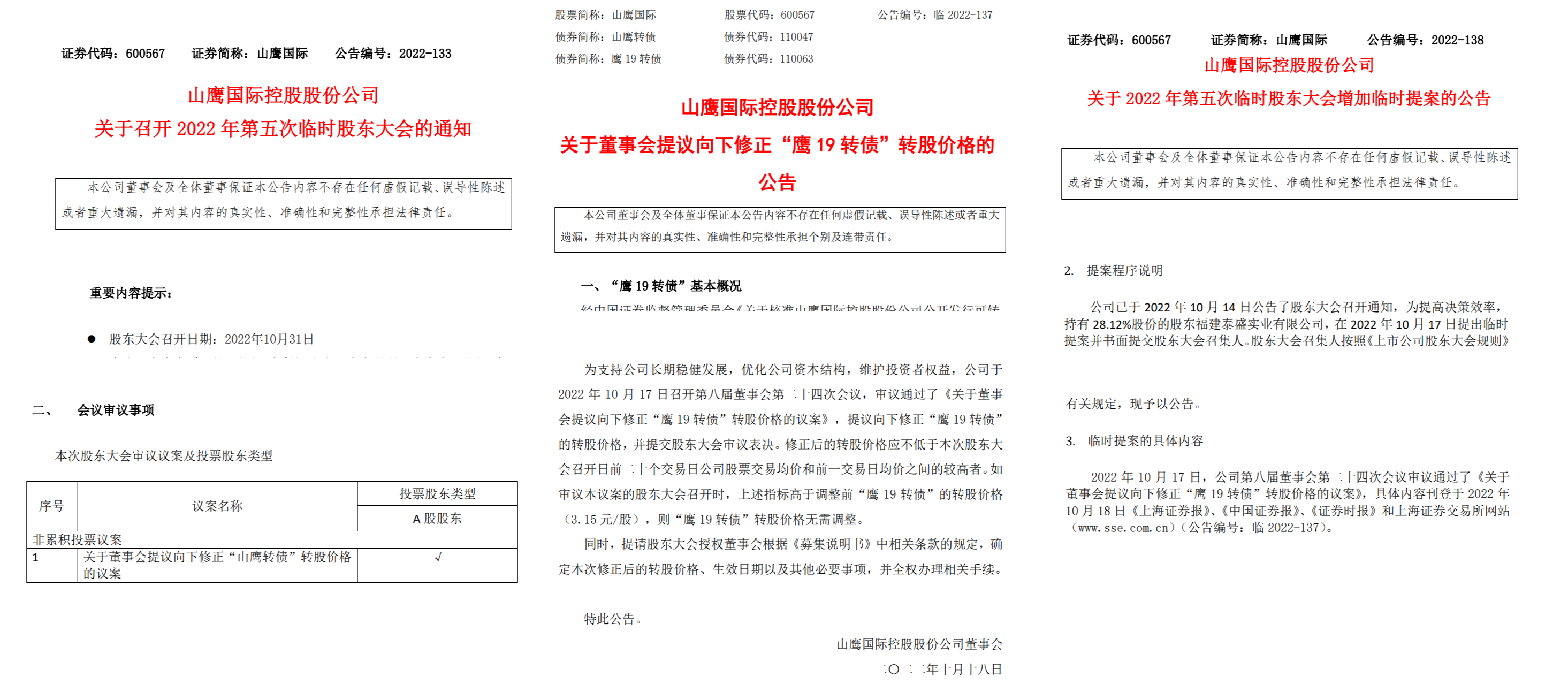

On the day when Shanying Convertible Bonds was to be revised and announced, Shanying International also issued a notice about holding the fifth extraordinary general meeting of shareholders. There was a detail that made me feel uneasy. The date of the extraordinary general meeting is October 31. According to the “Rules for the General Meeting of Shareholders of Listed Companies”, the extraordinary general meeting needs to be notified to ordinary shareholders 15 days in advance. The EGM was held more than 15 days after the Shanying Convertible Bonds proposal was announced, but the Eagle 19 Convertible Bonds were first triggered on the 17th and announced on the 18th. No matter which time is used, the proposed revision of the Eagle 19 convertible bond is less than 15 days away from the meeting.

Therefore, if Shanying International discusses the revision proposal for the Eagle 19 convertible bonds alone, it needs to hold another extraordinary shareholders meeting in early November. This is obviously against common sense.

I think that perhaps at the moment when this extraordinary shareholders meeting was confirmed, the company’s board of directors finalized the principle, that is, the proposal for this downward revision is only for Shanying Convertible Bonds.

However, it is not difficult for me, Uncle Ka, to figure out whether the board of directors does not want to issue Xiuying 19 convertible bonds or something else is hidden about the timing of the meeting. Because researching listed companies has always been my biggest advantage.

The solution to a problem cannot be guesswork.

I had a communication with the securities department of Shanying International, listed a series of questions of concern and asked them all the way, and finally asked the core questions.

I asked directly: “I have observed that the earliest triggering revision of the Eagle 19 Convertible Bonds is less than 15 days away from the EGM. It is obviously inappropriate to hold two EGMs in a row. Does this indicate that the company’s Didn’t you consider the revision of the Eagle 19 convertible bond?”

The staff replied: “For the two convertible bonds, the company will currently consider the work of promoting the conversion of shares. However, the specific resolution needs to be decided by the company’s board of directors. If the Eagle 19 convertible bonds are also proposed to be revised, we will not hold a separate interim shareholder meeting.” General meeting. We will add this proposal to the general meeting of shareholders on the 31st as a temporary proposal for resolution.”

At this moment, a golden light enveloped Uncle Ka, and a pure white angel floated out of Uncle Ka’s body shining with loving brilliance.

It said: “According to the requirements of Article 15 of the “Rules for Shareholders’ General Meetings of Listed Companies”, the extraordinary general meeting of shareholders needs to notify investors at least 15 days in advance. The rights and interests of small and medium-sized investors need to be notified in sufficient time to make it easy for small and medium-sized investors to organize and think about whether to exercise their veto power. Such a way of filling temporary proposals is to take advantage of policy loopholes, which is not appropriate.”

Immediately afterwards a black figure flashed past, and another black little devil flew up from Uncle Ka’s body. It took off its shoes and knocked down the angel at once. It’s a bond investor.”

So Uncle Ka’s mouth showed a sly smile, and I said to the other end of the phone: “Well, the company made a temporary proposal in accordance with Article 14 of the “Rules for Shareholders’ Meetings of Listed Companies”, which improved the efficiency of decision-making. It is reasonable, legal, very appropriate and considerate. We applaud the listed company for the decision-making of the rights and interests of all parties.”

Put the phone down, according to all the research and analysis.

I think there is a very high probability that the Eagle 19 convertible bond will be revised down in a few days. The board of directors of the company actively proposes such a proposal, and important shareholders do not need to avoid investment, then it is very likely that this resolution will be passed by an overwhelming advantage. Shanying double debt, before the revision, the premium is not very high, and the revision has no net assets If there are no restrictions, then the probability of this downgrade to the end is quite high.

On the evening of October 17, the Eagle 19 convertible bond was proposed to be revised down. After that, everything was carried out in accordance with normal procedures. The conversion price of the two convertible bonds was unified at 2.4 yuan. Everything is back on track, but after this revision, the conversion value of Shanying Convertible Bonds has increased a little bit more.

Since the price of Eagle 19 was always lower than that of Shanying by more than 1 yuan during the warehouse building period, the two convertible bonds returned to the parity stage in the later period. So in this downward revision game, I actually completed this round of investment in a more cost-effective way.

The third attribute: ex-dividend grabbing power

Synchronous downward revision, it seems that the two convertible bonds have returned to the daily threshold switching state. But at this point in time, there are some differences from the past. Because the annual ex-dividend date of Shanying convertible bonds is November 21, and the ex-dividend date of Eagle 19 convertible bonds is December 13, 22 days later.

The interest paid on Shanying Convertible Bonds in the fourth year is 1.5 yuan before tax per piece, while the interest paid on Eagle 19 Convertible Bonds is 0.9 yuan per piece before tax in the third year. There is an interest rate difference of 0.6 yuan per ticket before tax and 0.48 yuan after tax.

Therefore, the arbitrage of convertible bonds with the underlying shares can actually be divided into two time points. For most of the time period, we can switch the arbitrage according to the threshold set by ourselves, but at the time point of ex-dividend, we need to pay extra in this cycle. Consider the fluctuation caused by the ex-dividend factor, and at the same time, you can use this fluctuation to earn an extra income.

The investment in Shanying double debt is not a high-yield investment case, but it has great particularity. It contains multiple investment strategies of convertible bonds, quantitative analysis, excess arbitrage income, and The all-dimensional thinking of the lower revision of the game, so I deliberately share this case, hoping to be helpful to everyone’s future investment.

Finally, I wish netizens a happy Year of the Rabbit, good health in the New Year, and stable asset appreciation.

There are 13 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/9508203182/240488595

This site is only for collection, and the copyright belongs to the original author.