Qiu Dongrong’s recent investment roadshow is undoubtedly the hottest topic in the fund industry.

On the one hand, Qiu Dongrong’s 65.16% return on the small-cap value of Zhonggeng last year, and this year’s excellent performance of Zhonggeng’s value-leading still positive earnings, naturally aroused the attention of chasing rankers; on the other hand, he was clearly bullish on the stock market and even shouted ” The most conservative investors should buy stock assets now “, which is also a stimulant in the recent sluggish market environment.

For the essence of Qiu Dongrong’s roadshow, you can read the full text of Xiaoya’s “Qiu Dongrong in the most enthusiastic onlookers, giving the most optimistic market judgment at present: very conservative investors should buy stocks now! “We will definitely not keep cash!” Dingge bought Hong Kong stocks! , very detailed.

Here, I will do some derivative discussions, mainly on how to use index funds to reproduce this investment idea – after all, Qiu Dongrong’s fund does not discount, the 1.5% subscription fee is quite expensive, and the previous purchase limit is also a risk point.

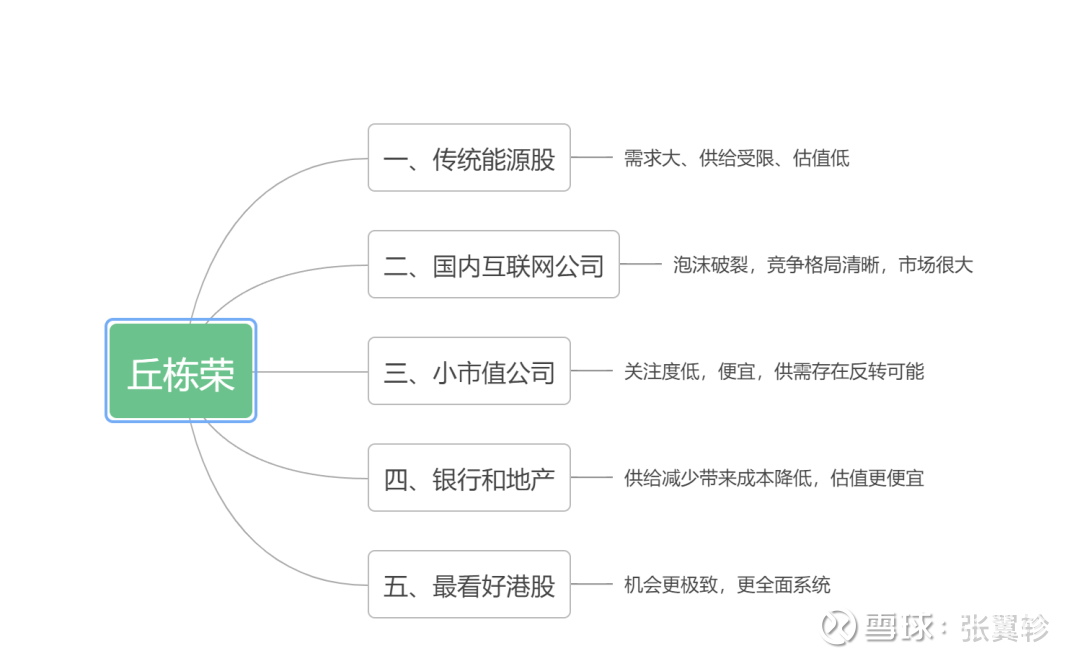

First, let’s take a mind map, based on the arrangement and production of Teacher Xiaoya, you can see the five opportunities mentioned by Qiu Dongrong.

1. Traditional energy stocks

Qiu Dongrong loves coal, which is a major feature of him. In October last year, I wrote an article “Qiu Dongrong, who has made a profit of 73.59% this year, continues to be optimistic about coal, and at the same time increases financial real estate.”

There are three main reasons why Qiu Dongrong is optimistic about coal:

With the recovery of the global economy, especially the recovery of economies represented by the United States, downstream demand is accelerating in the short term;

In traditional oil, natural gas, coal and other industries, the most important feature in terms of supply is that capital expenditure peaked around 2012 and continued to decline;

In such an industry, the remaining companies are very large and leading companies with very large resource endowments and corporate barriers. It is very difficult for latecomers to enter this field and gain an advantage.

You can actually keep these three reasons of Qiu Dongrong in mind. This is not only the investment logic of coal stocks, but also the fundamental logic of traditional value investors . A few days ago, I listened to the roadshow of another in-depth value-producing gold manager, Zhongtai Xingyuan Jiang Cheng, which is also of similar logic. Jiang Cheng took the US tobacco stock as an example, emphasizing that the competition pattern is more important than the growth of total market revenue. Sales have been shrinking for a long time, but because there is no strong competition, Philip Morris shares have been doing well all year round.

Of course, one of the better things about coal is that demand may still rise. This point, the author in “Value Investing Is Dead? In the article, the key to citing GMO Fund’s Jeremy Grantham is similar. Jeremy Grantham believes that the expansion of new energy sources may actually be good for demand for old energy and materials.

Tracking energy stocks, the main force at the index fund level is naturally the coal ETF (151220), and the corresponding OTC connections are: A share 008279 and C share 008280.

2. Domestic Internet

Qiu Dongrong is optimistic about the logic of the domestic Internet, in fact, it is similar to being optimistic about coal.

After the anti-monopoly crackdown, the Internet giants are no longer in a money-burning competition pattern. In this regard, Qiu Dongrong analyzed this:

In the past year, very important changes have taken place in their fundamentals: very strong constraints from national industrial policy, which include preventing capital expansion, restricting competition and anti-monopoly.

From an investor’s point of view, we think this is a very good policy, and they strictly limit the urge of the giants to expand. This is a very good supply-side reform measure for the entire Internet ecosystem.

Under these measures, the major giants have strictly contracted their fronts, without further crazy expansion, without making more radical and additional capital expenditures, but focusing more on the main business.

Regarding this logic, as early as December 12, 2020, I expressed similar expectations and visions in the push of “Friday’s meeting, a lot of information, my thoughts”.

At that time, I emphasized that anti-monopoly policy is definitely a short-term negative for Internet giants, but it will become a positive in the long-term.

Today, the giants do seem to have entered such a pattern.

It’s just that in the past year or so, the stock prices of Chinese stocks have fallen by 2/3, which is indeed unexpected. But it is precisely because of this that Internet companies will enter Qiu Dongrong’s vision, which is a bit like Buffett was optimistic about Apple back then.

To track this group of companies, there are too many index products to choose from, such as China Concept Internet ETF, various Hang Seng Technology ETFs, and Hang Seng Internet ETFs.

3. Small-cap companies

For small-cap companies, Qiu Dongrong pursues sinking:

We have the opportunity to buy companies with low valuation, low risk, and sustained high growth. Companies are generally distributed in CSI 500, CSI 1000, and even small companies below CSI 1000. We need to find them from the bottom up.

In this regard, active funds do have advantages and can choose the best.

For index investors, at the level of the CSI 1000 Index, there are very few options, let alone further down.

The optional main force may still be in the field of the CSI 500 Index.

For example, Pengyang CSI 500 Index Quality Growth (007593/007594) tracks the 500 Quality Index. As can be seen from the table below, the 500 Quality Index has passed the optimization of the CSI 500 Index. Except for the 2020 Young Micro underperforming the CSI 500 Index, other years have significant excess returns compared to the CSI 500 Index.

As for the quality growth of Pengyang CSI 500, because of its small scale and new bonuses, historically there can be more excess returns.

4. Banks, real estate

When I first mentioned Qiu Dongrong, it was because he did not buy a house, but only bought real estate stocks.

In terms of his optimism about banks and real estate, Qiu Dongrong is indeed a relatively clear-cut person:

The opportunity lies in the reduction of risks under the background of stable growth, especially those leading companies in banks and real estate.

As a value investor, if you want to bet on banks and real estate, the main force is obviously to go to Hong Kong stocks.

For banks, CSI has launched the HK Bank Index Tracker, and there are two corresponding index products.

Penghua Hong Kong Stock Connect China Securities Hong Kong Bank (LOF) (501025), which can be traded on the market, although the daily trading scale is less than one million, you need to buy slowly;

Of course, Penghua is only LOF, so it can also be purchased off-site. In addition, HK Bank also has a Taikang Hong Kong Stock Connect CSI Hong Kong Bank Index (006809) on the off-site, which performs slightly better in the long run.

In the real estate sector, if you focus on A shares, you can naturally consider the real estate ETF fund (515060), and the corresponding feeder fund: A share: 008088 C share: 008089, this previous “Buying real estate stocks now, is it too late?” “Introduced in the scale is relatively small, there are still new thickening.

Of course, in the real estate sector, the valuation depression is in Hong Kong stocks.

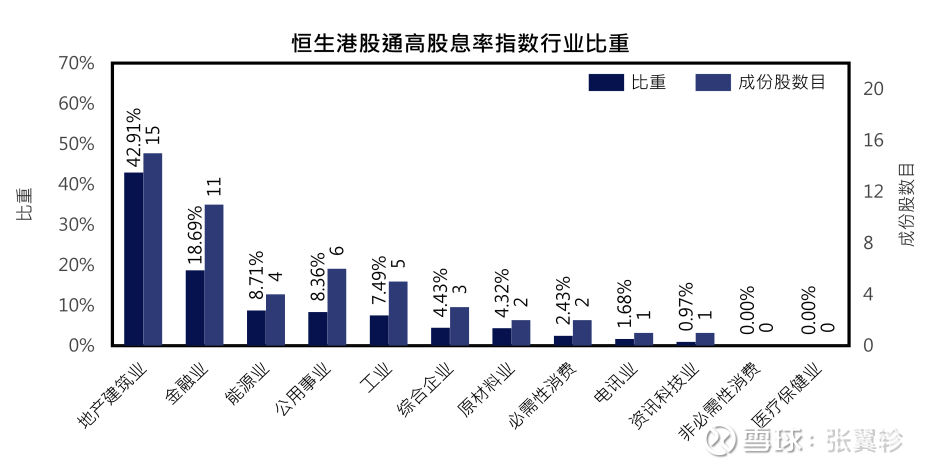

If it is considered from a package, in fact, two Hang Seng High Dividend Funds can be considered.

One is the Bosera High Dividend ETF (513690) and the corresponding link: A share 014519 C share 014520, I have so many high dividend funds in Hong Kong stocks, which one do I love the most? “introduced. It is almost 40% real estate plus nearly 20% banks and nearly 10% energy.

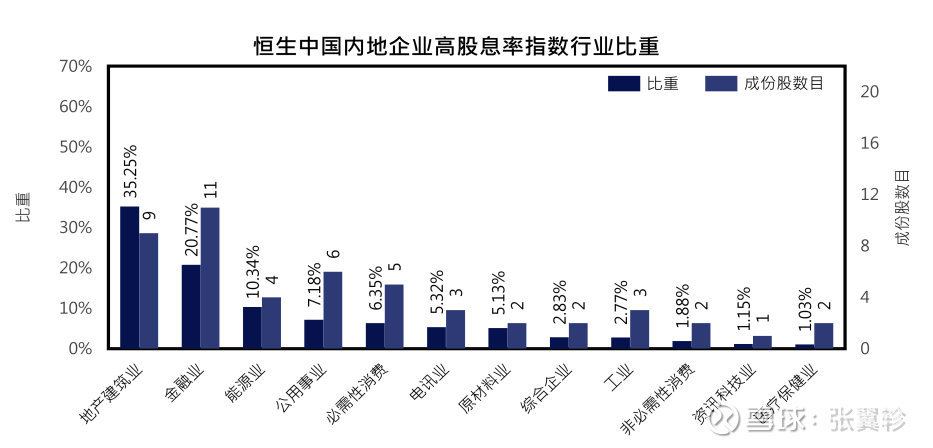

The other is China AMC Hang Seng Mainland China Enterprise High Dividend ETF (159726), which has no feeder fund. This only focuses on high-dividend mainland companies listed in Hong Kong, with a lower proportion of real estate and a slightly higher proportion of finance and energy.

Qiu Dongrong’s fifth point is about Hong Kong stocks. In this regard, he is extremely optimistic:

We have actually raised the proportion of Hong Kong stocks to a relatively high level this year, close to the upper limit. The upper limit is 50% of the stock ratio. We think this is a very, very good opportunity.

In fact, judging from the funds we selected in the previous modules, the Internet and bank real estate are actually mainly Hong Kong stock funds, which is the embodiment of this idea.

Referring to Qiu Dongrong’s holdings, let me make a fictitious ratio that focuses on financial real estate and see how much difference will there be in the future compared to Qiu Dongrong’s Zhonggeng value pilot:

15% Bosera High Dividend ETF + 15% China AMC High Dividend ETF + 15% Taikang Hong Kong Bank + 30% Pengyang CSI 500 Quality Growth + 5% Coal ETF + 20% Hang Seng Internet ETF.

This topic has 4 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3559889031/220082286

This site is for inclusion only, and the copyright belongs to the original author.