Today, I will summarize the annual gains of some dividend value price indexes and total return indexes, as well as the annual excess returns of tracked ETFs. The data is only counted for the past 14 years. It is considered to have gone through two rounds of bulls and bears, which has certain reference value.

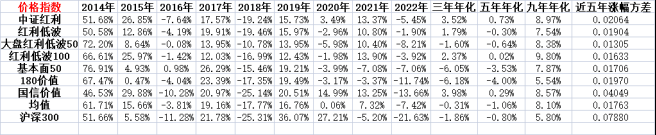

First look at the annual increase in the price index:

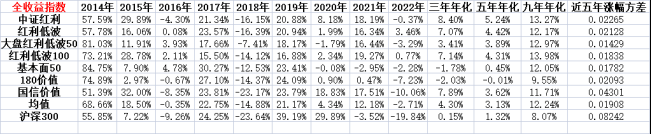

Let’s look at the annual increase in the total return index:

A few conclusions and thoughts:

1. China Securities Dividend is an underestimated good index. It only uses the simplest dividend rate weighting to achieve the best results. Among the several dividend value indexes concerned, it has been in the past three years, the past five years, and the past nine years The rate of return is almost always the best. Whether it is adding low volatility factors, value factors, fundamental factors, or ROE factors to dividends, it is not as good as the original dividend rate factor. Pure dividend rate enjoy pure benefits;

2. The volatility of the dividend value index is lower, and the holding experience is better. Here I simply use the variance of the increase in the past five years to measure the volatility. It can be seen that the variance of the dividend value index is much smaller than that of the CSI 300 index. However, There are two points worth noting. One is the value of Guosen, which is a small-cap style value index. The volatility is significantly higher than other dividend value indexes. The second is that the volatility of the index that uses a low volatility factor is also significantly lower than other dividend values. class index;

3. The dividend value strategy has steadily outperformed the CSI 300 Index in the past. The average total return of the value dividend index has outperformed the CSI 300 in six of the past nine years, and the nine-year average annualized outperformed by 4.17 %, even the worst value of 180 outperformed by 1.48%. Long-term holding of the dividend value index can provide a return that exceeds the market average;

4. There is a phenomenon that the dividend value index cannot beat the market average in the short and medium term. In 2019 and 2020, the dividend value index generally underperformed the Shanghai and Shenzhen 300 by a large margin. Taking the best performing CSI dividend as an example, the total return index was 19 Underperformed by 18.31% in 2019 and 21.71% in 20 years, you need to have enough patience to hold dividend value indexes;

5. Fundamentals 50 and 180, the two price indices that represent the value of the market, have fallen for three consecutive years. Will this year be extremely prosperous? Will it provide more excess returns than other dividend value indices? I think it is possible, and these two indices deserve more attention.

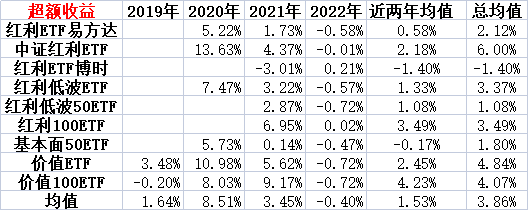

The following is a summary of the data tracking the excess returns of ETFs. For the convenience of calculation, the excess returns here are equal to the actual increase in the ETF minus the increase in the corresponding total return index, and the excess returns are simply identified as new returns:

A few conclusions and thoughts:

1. The 20th and 21st years are the new golden age, and these two years are also the period when the market is relatively good in recent years. When the market is good, small-scale ETF funds can provide substantial excess returns;

2. The income from new games is unstable, and when the market was bad in 22 years, the income from new games also dropped sharply;

3. Scale expansion will reduce the income from new launches. Also tracking the dividends of China Securities, the smaller China Merchants has significantly outperformed the larger E Fund;

4. Value 100 ETFs, Value ETFs, Bonus 100 ETFs, and Bonus Low-Volume ETFs have performed well in the past, and there is a high probability that they will provide good new earnings when the market recovers in the future, and there is a high probability that the bonus ETFs will be able to do so after the scale of the dividend ETF stabilizes;

5. Relying on the income of the dividend value index plus the income of the corresponding ETF, the long-term dispersed holding of small-scale dividend value ETFs has a high probability of continuing to outperform the market and on the basis of enjoying lower volatility. Nice payoff.

A few additional notes:

1. There are so many dividend value indexes, here are only a few dividend value indexes of personal concern, the conclusion may be partial;

2. The past rate of return does not represent the future, and the data is for reference only;

3. It is inaccurate to simply consider the excess returns from new investments as new returns. In fact, not only new returns can provide excess returns, but the calculation of new returns also ignores the overall operating expenses of the fund. $Dividend Index(SH000015)$ $CSI Dividend(SH000922)$ $CSI Dividend ETF(SH515080)$

There are 22 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/6828304753/239661234

This site is only for collection, and the copyright belongs to the original author.