The decline of Hong Kong stocks in 2019-2022 does not seem to be as large as the decline of US stocks in 1929-1932. However, the degree of loss of investment confidence caused by the simultaneous occurrence of multiple low-probability events may be similar (small-cap stocks with a price-earnings ratio of 4 times and 5 times abound). Compare for a long time:

In 1932, the Dow Jones was at a low of more than 40 points, down 44% from the 70 points at the end of 1917. However, in 1932, the US GDP after the recession was 59.5 billion, which is almost the same as that of 59.7 billion fifteen years ago. What’s worse is investor confidence.

China’s GDP behind the Hang Seng Index in 2022 is estimated to have increased by more than 400% compared with the US$3.5 trillion in 2007, but the Hang Seng Index has also fallen by 34% in the past 15 years. The worst is also investment. confidence.

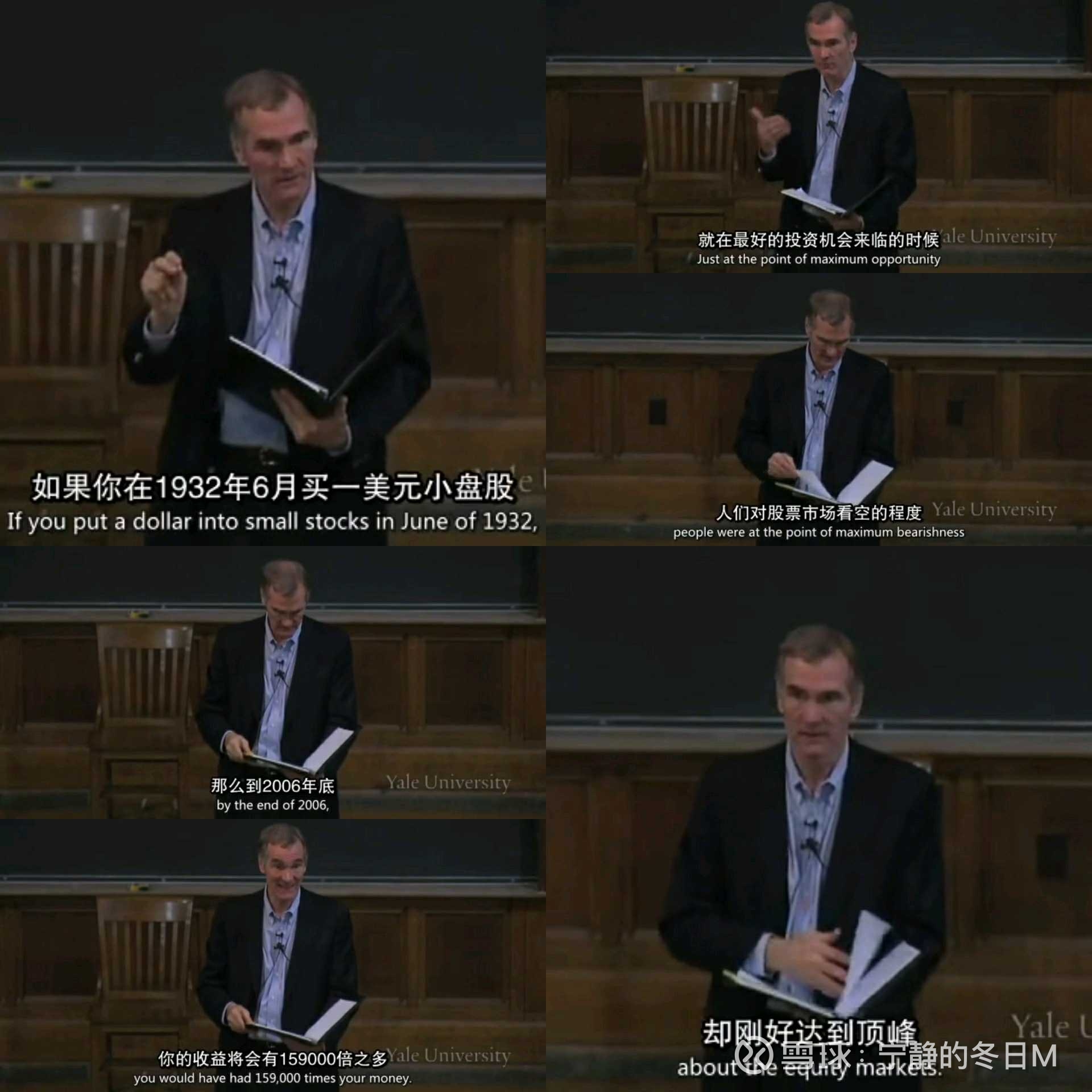

Looking at this point in 1932, if you ever thought that stocks were the asset with the highest long-term return in 1929, it must have been a regrettable miscalculation. You’d think it would have been nice to have bought Treasuries instead of stocks three years ago. . . But in the real long-term dimension, such as 2006, your judgment is actually correct. During this period, stock assets accumulated a return of more than 1,000 times (including dividend reinvestment), which is still the highest return. Far more than the bonds of the same period – the latter is only more than 70 times.

Stocks are the assets with the highest long-term returns, which are determined by the continuous creation of value by the economic organization behind them. People’s high and low confidence in investing in stocks has never changed this fact. Of course, if people had lost their confidence in investing in 1932, and they were particularly regretful about buying stocks instead of bonds, taking a portfolio of small-cap stocks as an example, the return would have been 159,000 times by the end of 2006. . .

Both the 1929 market and the 1932 market were ineffective by the long-term returns of large classes of assets. Stocks are all undervalued (the difference is that 1932 was more undervalued). This undervaluation has proven unexplainable by differences in risk indicators such as volatility.

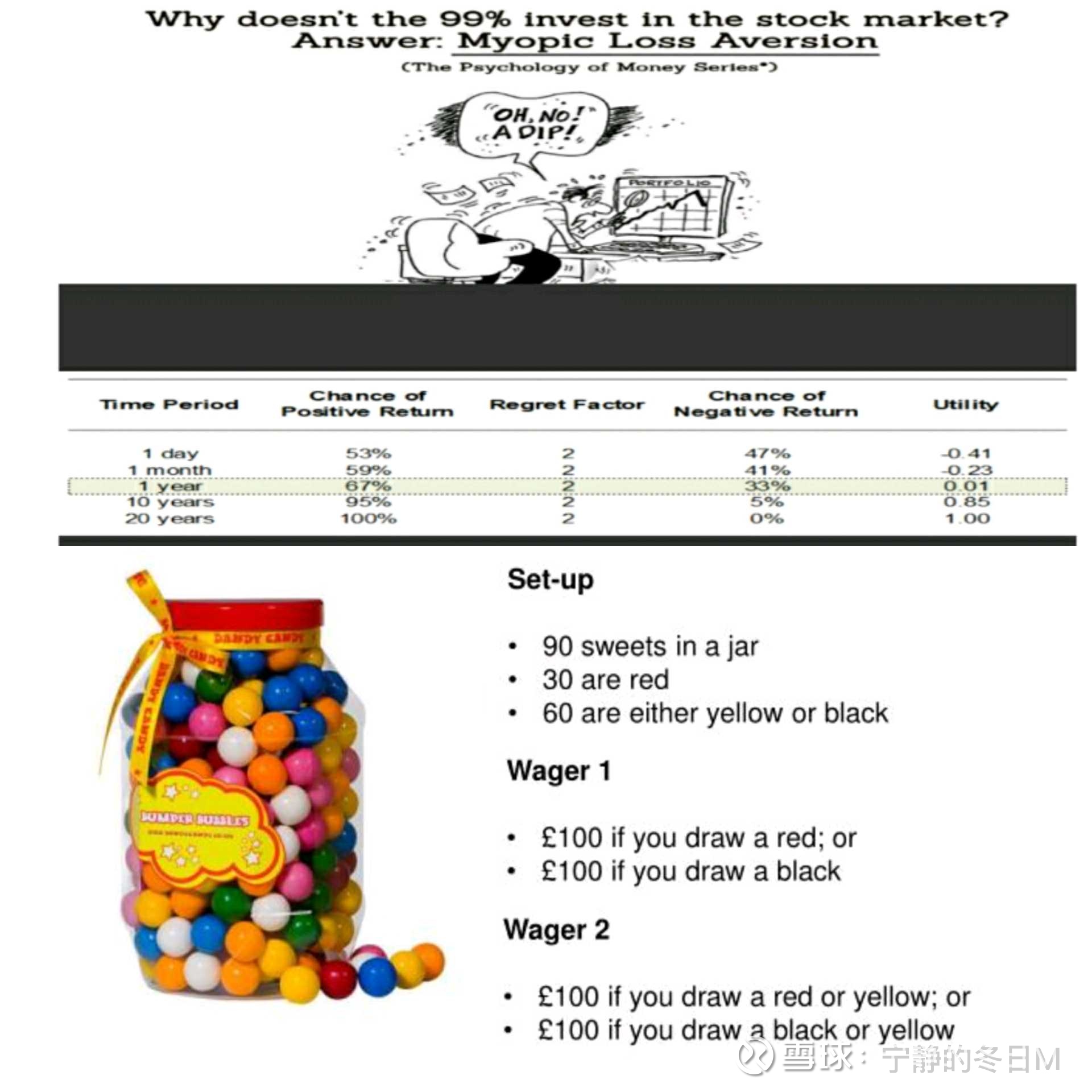

However, based on the psychological needs of users, both of them may be effective ~ stock assets are at a significant disadvantage compared to bonds and gold when faced with psychological laws such as fuzzy aversion and frequent evaluation. Only the smart, accomplished, socially sought after ones experienced in bull markets like 1929. . . can be partially offset. The 1932 bear market experienced doubt, anxiety, and remorse. . . The gap between the two has led to a huge price difference – business returns can be calculated to a certain extent, and it is difficult to calculate how much difference people are willing to pay for their life experience.

Aversion to stocks just peaked at the best of historical opportunities. The reason behind this phenomenon observed by David Swenson is that if people’s investment is based on the most intuitive statistics, then a certain asset is counted for three years, five years, and fifteen years. . . When there is always a negative return, how can everyone not worry about the next fifteen years, not doubt, worry, and regret?

Some people say that investing is against human nature. I personally think that if this is the case, if you need to give up ordinary human nature, give up the joy of life, and make yourself a god who suffers every day, in order to make a good investment, then I would rather not do such an investment.

Fortunately, what we really need to give up in investing is not human nature, but a little stick to the rules. As long as we take a step forward, look through statistical data to see the causal relationship behind it, and use the first principles of physics to find the real source of returns , it is easy to find that intuitive statistics may lead us into misunderstandings:

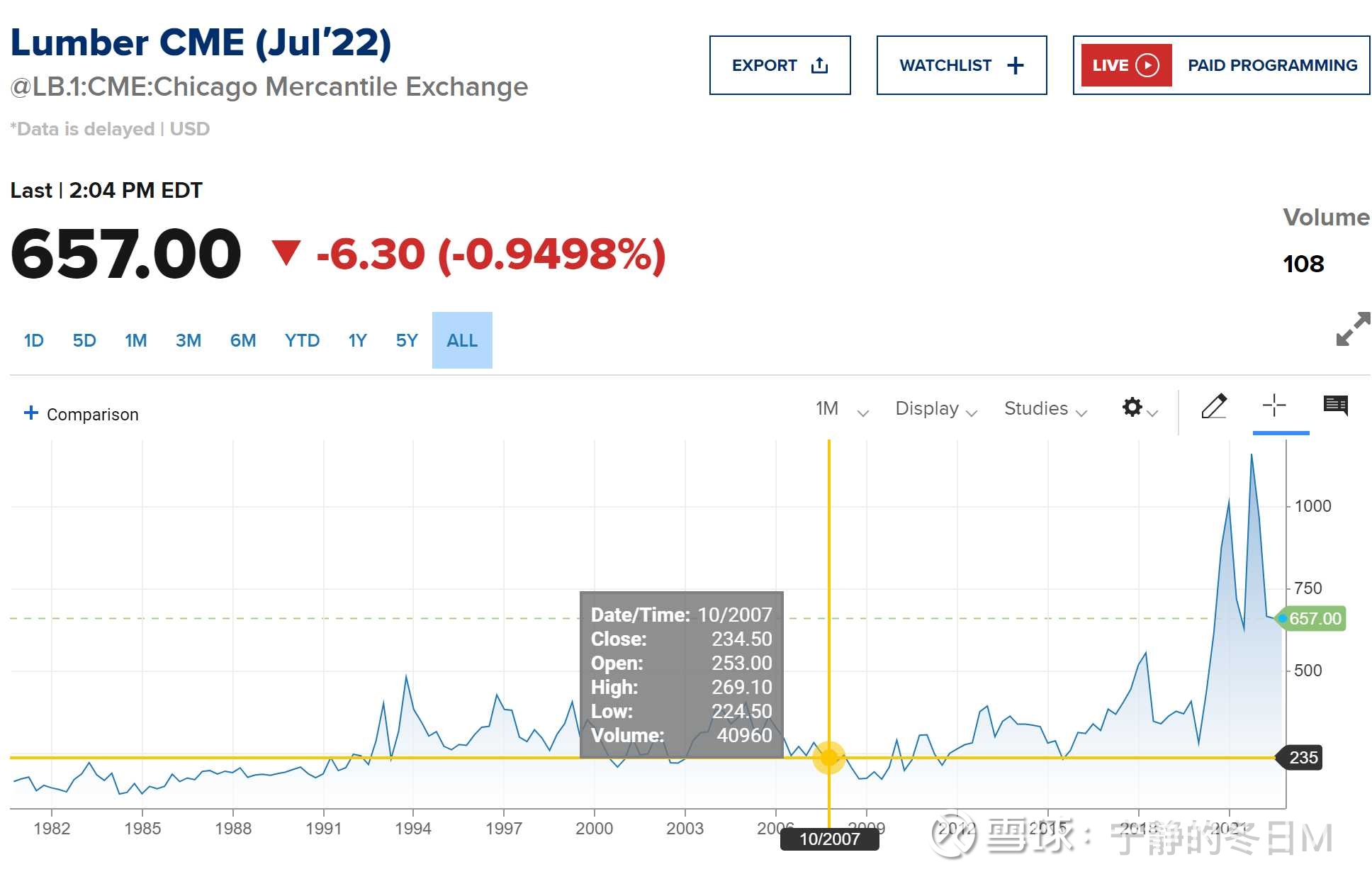

A plantation that can produce 10,000 tons of wood per year, if it is cheaper than 10,000 tons of wood, which one should we buy more cost-effectively? From the point of view of causality, this is a thing that does not need to be considered at all. But statistics are likely to tell us that assets should be allocated to the latter ~ because the price of the latter has more than tripled in the past fifteen years, and the price of the former has fallen (mainly because the price-earnings ratio has dropped from twenty times to several times), Configuring the latter can not only spread the risk, but also “increase the rate of return”. . .

According to this way of looking at statistics and making investments, the most important thing to increase the allocation ratio last year is various virtual currencies (this is no longer a joke, but what many asset management institutions actually do with investors’ money). . .

In fact, as our risk control @ Mujiu said, the real risk comes from not penetrating to the bottom, not figuring out how the money is generated ~ Statistics will not tell us that reliable business keeps generating money , and the money generated by the popular spontaneous Ponzi games, in terms of long-term returns. But from a causal point of view, the difference between the two is essentially:

The latter is gone when it falls. The former is that the more you fall, the more you earn~ If our investment is only based on statistics, it may be based on the latter. Under this background of thinking, when the best stock investment opportunity comes , it is normal to just hate stocks the most (just looking at the statistics in 1932, the experience is still very good, it can only be sick). If our investments are based on causality behind statistics, root in the former. It would probably be found that there were actually more good opportunities in 1932.

However, once we start looking for cause and effect, we need to dive into the real world of business. It’s full of challenges here. Making money doesn’t seem to be an easy keystroke anymore, it’s getting harder. But we have less anxiety and more happiness in our investment life. A while ago, my beautiful colleague @秋瑞8 taught me: “There is no perfect investment, only perfection through continuous learning”.

I think this sentence makes a lot of sense.

Therefore, if you find yourself in 2022 with a 5x price-earnings ratio of Hong Kong stocks and a lot of losses from the stock price, it may be the same as the 5x price-earnings ratio of US stocks in 1932. In the long run, they are only on the road of high returns. But the premise is: your business portfolio can make money in the long-term in the future ~ looking at statistics is not the point of investment. The main point is: understand the causal relationship behind the data, make money happily, and live happily.

There are 48 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1556808774/224418195

This site is for inclusion only, and the copyright belongs to the original author.