The main assets of CYPC have already been calculated, but the company’s equity investment has not been calculated. Now, after looking at the stocks of five large, medium and small hydropower companies, let’s take a look at what CYPC’s investment assets are. looks like.

As of the 2022 Q3 financial report, the investment income is 4.18 billion yuan, and the net profit is 19.22 billion yuan, which has accounted for more than 21% of the net profit. Since 2016, the investment income has increased every year, accounting for 6% of the net profit. It has increased to 21% of the current level, and the long-term equity investment of foreign investment has increased from 13 billion yuan in 2016 to the current 55.3 billion yuan.

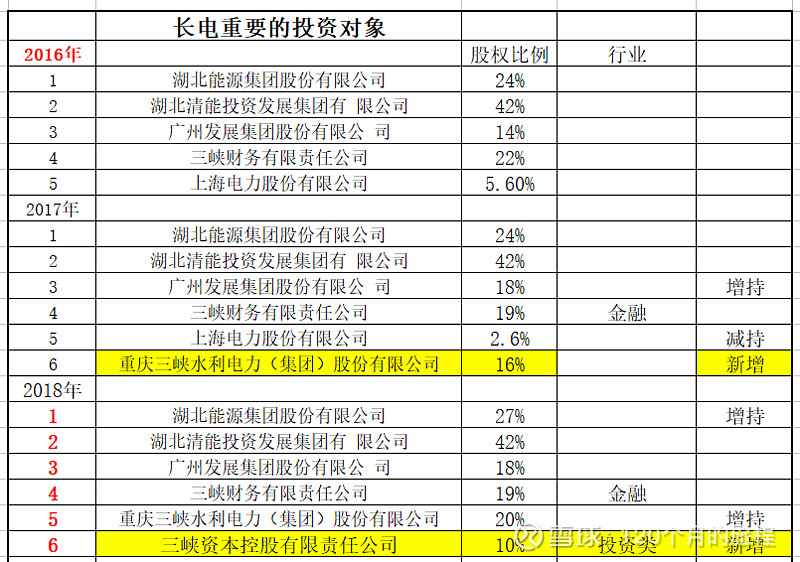

From 2016, the list is as follows:

From 2016 to 2018, Three Gorges Power and Three Gorges Capital were added, and Shanghai Electric Power was liquidated. I don’t understand how to operate equity investment for this purpose, maybe it’s a whim.

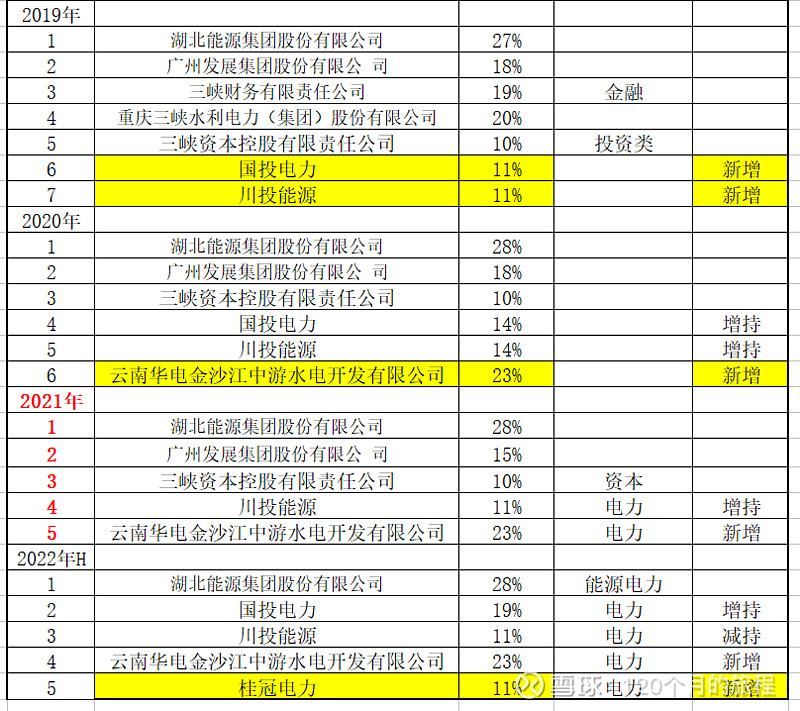

From 2019 to the first half of 2022, this context will become clear, with key investments in SDIC, Sichuan Investment, Hubei Energy, Huaneng Jinsha River Middle Reaches and Guiguan Power, taking down all the hydropower companies ranked first, second, third and fourth in the country. Among them, in 2021, SDIC Power was excluded from the statement of an important joint venture, which led to a crazy increase in SDIC Power in 2022. Now the shareholding has reached 19%, which is quite a lot for this big SDIC Power , This should be very optimistic about the hydropower assets of SDIC Power.

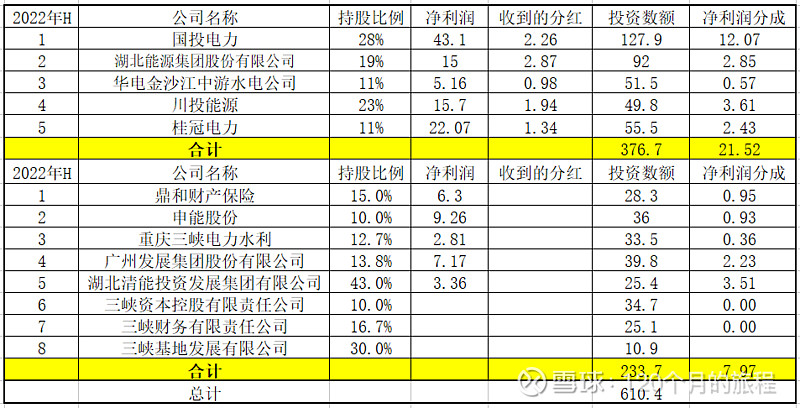

As of the first half of 2022, the company has a total of 64 shareholding companies with a total investment of 64.5 billion yuan. The companies with investment exceeding 1 billion yuan are mainly listed in the table below:

As can be seen from the above table, these 13 companies accounted for 61 billion yuan of the total investment of 64.5 billion yuan, and the other 50 companies shared the remaining 3.5 billion yuan investment. The top five of these companies are controlled by Huaneng, which has the second largest installed capacity. Jinsha River Midstream Company, Yalong River Hydropower and Guiguan Power, which rank third in installed capacity, and Hubei Energy Company of Hubei Small Hydropower Company of Three Gorges Group, have a proper hydropower platter. The stakes range from 11% to 28%.

The following non-important large equity investment companies include three listed companies, namely Shenergy, Guangzhou Development and Chongqing Water Conservancy. They are listed companies in Shanghai in East China, South China and Chongqing, all of which are relatively high-quality. In addition, there are brother companies of the group The three companies are Three Gorges Capital, Three Gorges Finance, and Three Gorges Base (it seems to be the logistics company of the Three Gorges Group). The brothers, the finance company and the capital company are definitely the main force of the Three Gorges Group. Dinghe Property & Casualty Insurance is an insurance company related to China Southern Power Grid. It does more business in the power grid. The company Hubei Qingneng is a company that Yangtze Power has always wanted to sell but has not. In October 2022, it was put on the label of selling again. The selling price was 4.6 billion yuan, corresponding to a cost of 2.54 billion yuan. , basically if you can make a deal, you can earn 90%, which is still possible.

Looking at these 13 long-term equity investment companies, they are basically state-owned enterprises, 8 power companies (5 water and 3 fire), hydropower companies, especially hydropower, are the big ones, 1 financial company, investment company 1 company, 1 insurance company, 1 company listed for sale, and 1 logistics company within the group, with very clear intentions and strategic positioning, low risk, and stable cash flow, only Hubei Qingneng has a little The ones that don’t match up are ready to be sold, and the company’s management is praised.

The company’s long-term equity investment uses the equity method to calculate the investment income of Yangtze Power. Except for 8 power-related companies, the 13 major companies are not very friendly in terms of financial, investment and logistics information, and the insurance company’s operation is relatively relatively stable. Therefore, focus on the big and let go of the small, and don’t measure the ones that are not accurate. We only focus on the analysis of the remaining 8 power-related companies, and see how much stable income these companies generate in a year.

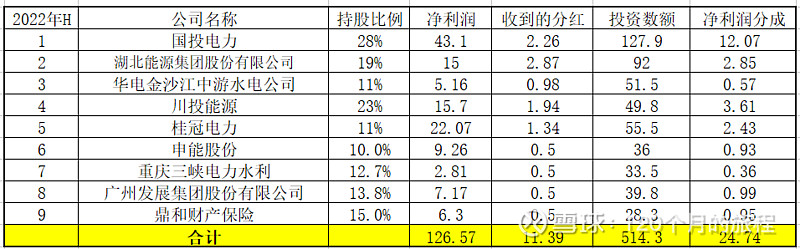

Dinghe is excluded from these 9 companies, but their performance should be quite stable, and they will not make big losses. Except for Huaneng Jinsha River Midstream, which is not listed, the rest are all listed companies, and it is easier to predict their performance, especially Guiguan, Jinsha River, SDIC, Sichuan Investment, Three Gorges Water Conservancy and Hubei Energy. Basically, the annual change is very small, and they are all hydropower-based companies, which can be roughly predicted according to the installed capacity or basically reliable according to the proportion of annual profit.

Among them, the most important asset of Guiguan is the Hongshui River, with a total installed capacity of about 10 million kilowatts of hydropower. The equity installed capacity of Changdian Power is 1.1 million kilowatts. The main asset of SDIC and Sichuan Investment is the Yalong River hydropower, with a total installed capacity of about 20 million kilowatts. Kilowatts, and eventually about 29 million kilowatts can be installed. Now Changdian’s equity installed capacity in the two investment projects is 2000×0.52×0.28+2000×0.48×0.23=5.12 million kilowatts. The installed capacity of hydropower in Hubei Energy is about 4.66 million kilowatts, and the equity installed capacity of Changjiang Power is 880,000 kilowatts. By the end of 2021, Jinshajiang Midstream Company will have a total installed capacity of 14 million kilowatts, and the final planned installed capacity will be 20 million kilowatts, of which Changdian will account for 11%. Equity installed capacity is 1.54 million kilowatts, and the Three Gorges Water Conservancy and others are negligible. In this way, the equity hydropower installed capacity of Changjiang Electric Power Co., Ltd. is 110 (laurel crown) + Yalong River (513) + Hubei Energy (88) + middle reaches of Jinsha River ( 154) = 8.65 million kilowatts. If the long-term installed capacity is counted, it will properly exceed 10 million kilowatts.

If you value the 10 million kilowatts of hydropower assets that you don’t need to invest in yourself, how should you value them? Compared with the six giant power stations including the Three Gorges, is this asset a high-quality asset or a relatively inferior asset?

Then there are the photovoltaic, thermal power, new energy and other assets of the above-mentioned companies, which will not be counted in detail. Now let’s review the main assets of Changdian, the six giant hydropower stations.

Then we can estimate the approximate market value of Changdian. The median price-earnings ratio is 18. Changdian’s investment assets can generate more than 5 billion yuan in income every year, and it will increase more and more with time. , then the net profit after Wubai injection is about 37-40 billion yuan, the market value is about 666-720 billion yuan, and the reasonable buying range is 0.6-0.8 percent off.

The current market value of Changdian Electric is 470 billion yuan, and the discount corresponding to the minimum 660 billion yuan (2023 or 2024) is 0.71 percent. Considering the dividend rate of 70%, the dividend is about 26 billion yuan, and the total share capital is 23 billion yuan. One share is 1 It’s about 1 yuan, so it’s not too expensive. If you want to hold it for a long time, JCET has a certain investment value at this moment. As for the risks of JCEP, such as unstable water supply, northward movement of the precipitation line, and earthquakes, etc. In my opinion, none of them are risks. The risks in my eyes are random investment, cross-industry, and cross-professional investment.

Summary of valuations of hydropower stocks such as Changdian, Huaneng, Guiguan, Qianyuan, and Nanwang Energy Storage #水电投资#

$Yangtze River Power(SH600900)$ $Huaneng Hydropower(SH600025)$ $Guiguan Power(SH600236)$

There are 10 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/6442372442/237839809

This site is only for collection, and the copyright belongs to the original author.