Welcome to the WeChat subscription number of “Sina Technology”: techsina

Text | He Jinyi Edited by Zhang Ranran | Fu Xiaoling, Cao Binling, Zhou Xiao

Data Support | Insight Data Research Institute

Source: inside and outside the table (iD: excel-ers)

A report by the Grizzlies against Weilai came down, and the market was restless – the new energy vehicle sector was green as a whole.

The report accuses NIO of using unmerged related party entity Wuhan Weineng to inflate revenue and profits by 10% and 95%, respectively, by over-supplying Weineng batteries and prepaying revenue in advance (subscription revenue is converted into immediate revenue recognition).

To this end, in addition to calculations and various research data discussions, it also specifically emphasized in the report that NIO executives are also closely related to Ruixing Coffee, which was accused of financial fraud two years ago.

This really messed up “a lake of water”, and Weilai’s “toxic” has overwhelmed many voices.

But looking at Weilai after the turmoil, what should be explored more is: why does such a false accusation occur? This article will restore the truth.

Don’t panic, it’s just basic accounting of listed companies

To explain this clearly, let’s first build a small scenario model:

Enterprise: outside and inside

Attribute: Electric Vehicle Company

Business model: vehicle sales

In the first year, the price of an electric car on the outside of the watch was 100,000, and the cost of producing the car was 70,000. The company sold 100 cars that year, and earned 3 million on the outside. The specific profit statement is as follows:

However, during the year-end review, it was found on the outside that the price of 100,000 yuan was too high, causing some intended users to finally give up the purchase.

In order to solve this problem, in the second year, the exterior and interior of the watch adjusted the car sales plan – the battery was sold for rent, and users did not need to pay the battery in full when buying a car, as long as they paid a certain amount of rent on time.

As a result, the purchase price of the car will be reduced by 30,000 (the price of the battery), and the user can buy a car for 70,000, which greatly reduces the threshold for purchasing a car.

Based on this, 10 more electric vehicles were sold on the surface of the calendar this year, and sales increased to 110.

However, at the end of the year, it was found on the outside of the watch that the more the car was sold, the less money it made—the net profit was only 2.42 million, down from 3 million the previous year.

The reason for this is that after the battery is sold for rent, the rent is paid monthly, 500 yuan per month, and repaid in 5 years. Therefore, only the rent of the year can be received on the outside of the table: 660,000 yuan.

You must know that last year’s battery sales revenue was 3 million, and the profit gap should be here.

Not only will the income be reduced, but the battery rental plan will also carry a large amount of non-current assets on the outside and outside of the watch, reducing the liquidity of the asset, and the asset will generate additional depreciation expenses every year.

This is comprehensively reflected in the financial statements, that is, the income statement and the balance sheet, which are much inferior to last year.

At the end of the year, although the boss was very satisfied with the increase in sales, the two unsatisfactory tables made him feel very unhappy, and told everyone to solve it as soon as possible.

The salesman Xiao A boldly suggested that he could set up a subsidiary and sell the batteries to them, not only to get rid of the rent-collecting work, but also to sell at a higher price-for example, if it is sold to users for 30,000 yuan, it can be sold to Subsidiaries can be 35,000, after all, the source of customers is in our hands.

However, this strategy was strongly protested by the Ministry of Finance.

The boss of the finance department said that from the perspective of business operation, selling batteries to subsidiaries, we can receive higher battery sales revenue at one time, which is indeed a good plan.

But from the financial dimension, subsidiaries are to be consolidated with the parent company, and their performance will eventually be reflected in our financial statements.

Take this year as an example, according to this strategy, after the subsidiaries are consolidated, the income and costs generated by internal transactions will be offset, and the income statement will not be optimized much.

At the same time, large illiquid assets will also be merged back, and because of high prices, the amount will also increase. Not as Xiao A said, was thrown out.

Of course, after refuting Xiao A, the boss of the finance department gave a better solution:

Since the problem lies in the consolidation, then simply sell the battery to a non-actually controlled affiliate, so that consolidation is not required, and this is also a common handling technique for listed companies.

According to this method, also in this year’s situation, the sale of batteries to non-actually controlled affiliates can not only confirm the battery sales revenue at one time, but also get rid of the burden of large non-current assets.

Under such beautification, not only has the revenue and profit increased, but the balance sheet has become “beautiful” again.

Based on the above four scenarios, Weilai’s current accounting treatment method is obviously the fourth one, a must for an excellent CFO.

In other words, NIO’s current financial disclosures are “formally” compliant.

Of course, people who understand finance can still capture this basic operation, which is not enough to cause market turmoil. What investors are more afraid of is that the company has something to hide.

Investors shout to Weilai: Don’t hide anything from me

As mentioned above, the premise of non-consolidation is that the affiliated company is not actually controlled. In the disclosure of NIO’s 2021 annual report, it is indeed said that: the shareholding ratio of the battery asset company (Weineng) is only 19.8%, Accounting using the equity method.

The financial report also mentioned that NIO has the right to appoint one of NIO’s nine board members. That is, the director may only be an ordinary member of the board of directors and will not control the affiliated company.

But the actual situation is that the person who decides the operation of the affiliated company is the “people of Weilai”.

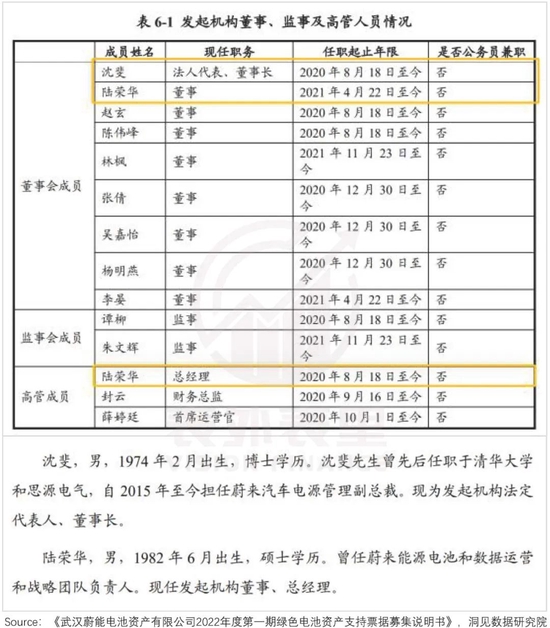

According to information disclosed by Wei Neng, the director appointed by Wei Lai is actually Shen Fei, chairman and legal representative of Wei Neng.

At the same time, Lu Ronghua, the general manager, was also a manager of Weilai, which Weilai has not officially disclosed.

The two “NIO background” personnel have the power to make decisions on the production and operation of the enterprise, and may even have a significant impact on the resolutions of the shareholders’ meeting to achieve control over the enterprise.

According to the accounting standard of substance over form, this situation should be regarded as “actual control”, and it is necessary to disclose or partially disclose the details of related party transactions in accordance with the corresponding requirements.

But Weilai obviously did not do this, which made the relevant personnel have room for “discretion” in the transaction between Wei Neng and Wei Lai.

This is also the most criticized point of Weilai: Weilai may sell at a high price to achieve high income on the report, and whether Wuhan Wei can accept this price is decided by the management related to Weilai.

Taking NIO’s 2021 financial report disclosure as an example, its transaction method with NIO can only be described as follows:

When NIO sells vehicles to BaaS users, it sells battery packs to NIO on a back-to-back basis. When the vehicle (along with the battery pack) is delivered to the BaaS user, NIO recognizes revenue from the sale of the battery pack to the battery asset company.

That is to say, only the time of recognition of transaction revenue and the number of transactions (the number of cars purchased by users using the BaaS solution) are disclosed, but the specific pricing is not mentioned.

Such unclear disclosure of related party transactions will inevitably make investors doubtful, especially if the transaction amount is relatively large.

Taking the first nine months of 2019 as an example, NIO’s battery revenue from sales to Nion was 2.79 billion, and its total revenue during the same period was 26.2 billion, accounting for more than 10%.

And with NIO’s promotion of BaaS services, this proportion still has room to rise, and its importance is getting higher and higher.

In this way, information such as how it is priced and its impact on NIO’s performance, if not fully disclosed, will mislead investors.

No one cares about cue profits, the market sees sales

It can be seen that although Weilai was exposed, the capital market seemed to have a mediocre response, and the stock price only fell by more than two points “politely”.

The reason is that the Grizzlies’ shorting did not hurt the fundamentals. In fact, as an emerging industry company, at this stage, the market is more concerned about whether the company can open up sales, rather than whether it can make a profit.

For example, in the product pipeline of NIO in 2021, it will only rely on ES8, ES6, and EC6 SUV models that have been on the market for a long time. The products on sale are “old” as a whole, making the delivery volume hit record lows. In 2021H2, Xiaopeng and Ideal will catch up. overtake.

The decline in sales has disappointed investors, and the market value has fallen from the vanguard of the new forces.

However, the anxious situation of “no new cars to sell” may be broken this year-in 2022, the delivery of new models will enter a blowout stage.

The ET7 was delivered in March; the just-released ES7 and the facelift of the old three 866 will be delivered in August; the ET5 will be delivered in September.

However, with such a “crazy output”, investors are even more worried:

“Will the arrival of ES7 have an impact on the 866?”

“The similarity between the ET7 and ET5 is extremely high. Will the delivery of the ET5 affect the sales of the ET7?”

In other words, intensive launch may lead to confusion in positioning, resulting in an embarrassing situation of competing products, and the certainty of sales is doubtful.

Perhaps compared with a “chaotic fist”, if you want to boost sales, you need a more popular model. At present, NIO seems to be betting on the relatively cost-effective model ET5.

For example, its management has mentioned many times: ET5 is the car with the largest number of reservations within 24 hours after its release. At present, the sales performance of models in the price range of more than 200,000 is very good. I believe this market can still accommodate another monthly model. More than 10,000 cars sold.

Based on this, rather than cue Weilai’s profits, it is more important to track sales and market feedback of new models.

summary

Things are already very clear, the key to the problem is not the accounting treatment of NIO’s current BaaS business, because although it is convenient, it is “formally” compliant after all.

Investors are more concerned about the fuller disclosure of BaaS related transactions – with the promotion of BaaS services, this part of information will have an increasingly significant impact on investors’ decision-making.

However, given that new energy is still an emerging track, in fact, the players in the capital market are anchored, and they pay more attention to sales.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-07-01/doc-imizirav1427452.shtml

This site is for inclusion only, and the copyright belongs to the original author.