“Yin-yang contracts”, bundled sales, and price increases in disguise, there are still irregularities in the signing of medium and long-term contracts for power coal

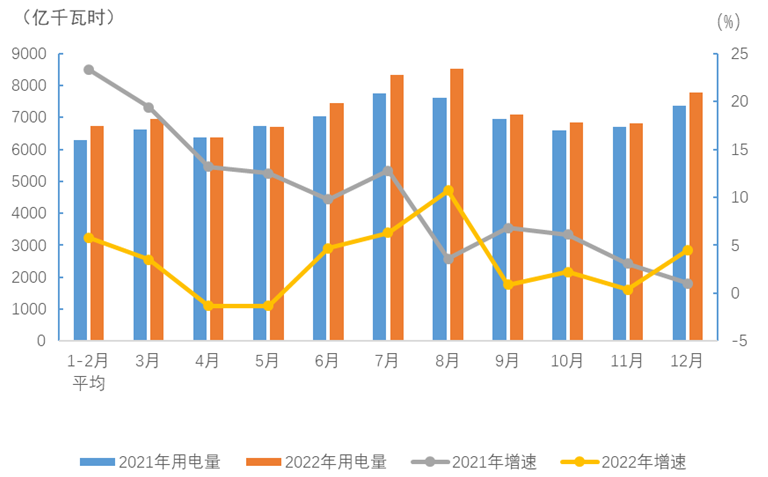

After experiencing the impact of the epidemic, China’s electricity growth rate in 2022 is lower than expected.

On January 19, the China Electricity Council released the “National Electricity Supply and Demand Situation Analysis and Forecast Report in 2023”. The report data shows that in 2022, the electricity consumption of the whole society will be 8.64 trillion kwh, a year-on-year increase of 3.6%. At the beginning of 2022, the China Electricity Council predicts that the growth rate of electricity consumption in that year will be 5%-6%.

Both new installed capacity and non-fossil energy installed capacity hit record highs

For the whole year, due to the impact of the epidemic and other factors, the growth rate of electricity consumption in the second and fourth quarters was 0.8% and 2.5% respectively, and the growth rate in the first and third quarters was 5% and 6% respectively, which was within the forecast range of the China Electricity Council .

2021 and 2022 Monthly Electricity Consumption and Growth Rate of the Whole Society Source: China Electricity Council

In terms of industries, the electricity consumption of the primary industry was 114.6 billion kwh, a year-on-year increase of 10.4%, and the electricity consumption of urban and rural residents was 1.34 trillion kwh, a year-on-year increase of 13.8%, a relatively high growth rate. Weather factors have a significant impact on residents’ electricity consumption. In August 2022, there will be large-scale continuous high-temperature weather across the country. The national average temperature will reach the highest level in the same period of history since 1961. Residents’ domestic electricity consumption will increase by 33.5% that month. In December 2022, four times of cold air will affect China. The national average temperature will be the lowest in the same period in the past ten years. Residents’ domestic electricity consumption will increase by 35% in that month.

Electricity growth rate is a barometer of economic development. The electricity consumption of the secondary industry, which accounts for the largest proportion, was 5.7 trillion kWh, an increase of only 1.2% year-on-year. Specific to different industries, the power growth rate also reflects the prosperity of the industry. For example, the electricity consumption of new energy vehicle manufacturing increased by 71.1%, while the electricity consumption of the cement industry in building materials fell by 15.9% year-on-year, and the electricity consumption of the consumer goods manufacturing industry A year-on-year decrease of 1.7%.

In terms of power installed capacity, although the competent authorities have emphasized the role of coal power as a guarantee after experiencing the power shortage in 2021, and the approval of coal power projects will also rebound in 2022, the overall trend of low-carbon transformation has not been affected, and the process is accelerating. trend.

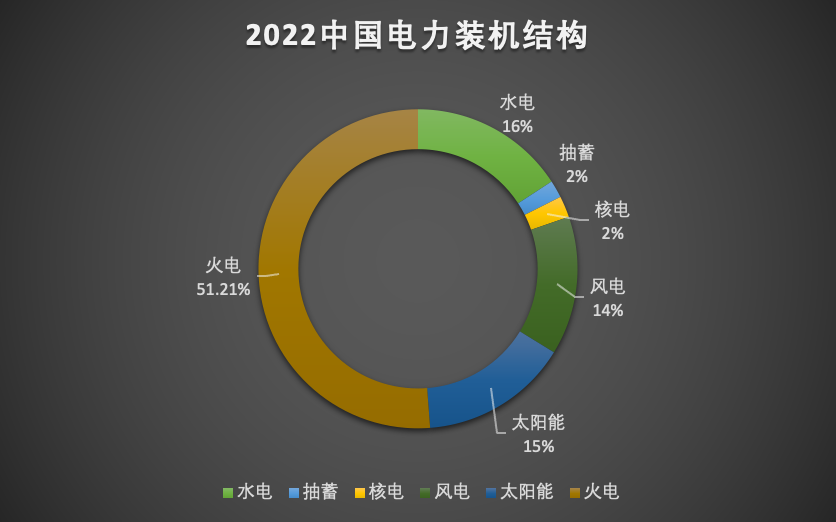

In 2022, China’s new power generation installed capacity will be 200 million kilowatts, of which non-fossil energy installed capacity will be 160 million kilowatts, accounting for 80%. By the end of 2022, China’s full-caliber power generation installed capacity will reach 2.56 billion kilowatts, and non-fossil energy installed capacity will reach 1.27 billion kilowatts, accounting for 49.6%, an increase of 2.6 percentage points year-on-year. The total installed capacity of newly commissioned power generation and the installed capacity of non-fossil energy both hit record highs.

2022 China’s power installed capacity structure data source: China Electricity Council (thermal power mainly includes coal power, gas power and biomass power generation, of which coal power accounts for 43.8%)

In terms of electricity, the trend of low-carbon transformation has also continued. In 2022, the full-caliber non-fossil energy power generation will increase by 8.7% year-on-year, accounting for 36.2% of the total power generation, an increase of 1.7 percentage points. The power generation of coal power increased by 0.7% year-on-year, and the power generation ratio was 58.4%, a year-on-year decrease of 1.7 percentage points. And when the incoming water was dry in the third quarter, coal power generation increased by 9.2% year-on-year, playing a role in ensuring supply.

It is also worth mentioning that China’s electricity market reform continues to deepen. In 2022, the power trading centers across the country will accumulatively organize and complete 5,254.3 billion kilowatt-hours of market transaction electricity, a substantial increase of 39% year-on-year, and market-oriented electricity will account for 60.8% of the total electricity consumption of the society, a substantial increase of 15.4 percentage points year-on-year.

2023 supply and demand tight balance

Regarding the power supply and demand situation in 2023, the China Electricity Council expects that China’s economic operation is expected to rebound in general, driving the growth rate of power consumption demand to increase compared with 2022. Under normal weather conditions, it is estimated that the electricity consumption of the whole society in 2023 will be 9.15 trillion kWh, an increase of about 6% over 2022.

Jiang Debin, deputy director of the Statistics and Data Center of the China Electricity Council, said at the press conference that the growth rate of electricity consumption in the secondary industry will gradually pick up in 2023. Under the influence of favorable policies, the gradual recovery of the real estate market will promote the recovery of electricity consumption in industries such as steel and building materials; The optimization and adjustment of epidemic prevention and control measures will create conditions for the recovery of service consumption and offline consumption in 2023. Electricity consumption in contact industries such as accommodation and catering, transportation, and cultural tourism will become an important factor for the recovery of the growth rate of electricity consumption in tertiary industries. driving force.

In terms of power installed capacity, the China Electricity Council expects that the new installed capacity will reach 250 million kilowatts in 2023, and the total installed capacity will reach 2.81 billion kilowatts, of which non-fossil energy will reach 1.48 billion kilowatts, accounting for more than half of the total installed capacity and reaching 52.5%. Specifically: 420 million kilowatts of hydropower, 430 million kilowatts of grid-connected wind power, 490 million kilowatts of grid-connected solar power, 58.46 million kilowatts of nuclear power, and about 45 million kilowatts of biomass power generation. The installed capacity of hydropower.

Under multiple factors, the China Electricity Council predicts that in 2023, the national power supply and demand will be in an overall tight balance, and power supply and demand will be tight during peak hours in some regions. During the peak summer season, the power supply and demand situation in East China, Central China, and South China is tight; the power supply and demand in North China, Northeast China, and Northwest China are basically balanced. During the peak winter season, the power supply and demand in East China, Central China, South, and Northwest regions are tight; the power supply and demand in North China are tightly balanced; and the power supply and demand in Northeast China are basically balanced.

In terms of factors affecting supply, the report also mentions that coal-fired power continues to lose money, which has led to insufficient investment in technical renovation and maintenance, which has led to increased hidden dangers of equipment and increased uncertainty in power production and supply.

In the report, the China Electricity Council suggested that the cost of coal-fired power generation should be eased, and the role of coal power supply should be fully guaranteed. Scientifically set up a linkage mechanism between fuel costs and coal power benchmark prices, relax the fluctuation range of coal power mid- and long-term transaction prices, and reflect and guide changes in fuel costs in a timely manner. Promote the construction of a capacity guarantee mechanism, increase compensation for paid peak shaving, make up for the gap in the recovery of fixed costs of coal power companies, and further improve the sustainable survival of coal power and the ability to guarantee supply. Strengthen unit operation and maintenance and safety risk prevention and control work, increase equipment health status monitoring and evaluation, and ensure safe and reliable operation of units.

There are still irregular and unreasonable phenomena in the signing of power coal contracts

After experiencing the electricity shortage in 2021, the role of coal power supply protection has attracted renewed attention, and the stable supply of coal power is the key guarantee for maintaining the role of coal power as the “ballast stone” of the power system.

To this end, the competent department will start research in October 2021 and issue relevant documents by early 2022 to complete the adjustment of the long-term coal price mechanism, promote the full coverage of medium- and long-term coal contracts for power generation and heating, and the number of medium- and long-term contracts for coal enterprises to reach their own The amount of resources is more than 80%, the benchmark price of the long-term association is raised to 675 yuan/ton, and a new floating range is set to 570 yuan/ton to 770 yuan/ton.

One year on, how is the implementation? Ye Chun, deputy director of the Planning and Development Department of the China Electricity Council, answered a question from a reporter from Caijing at the press conference. He said that the operation of medium and long-term power coal contracts in 2022 will be better than in previous years, which will play an important role in ensuring the safety of power coal and power supply. The performance rate of medium and long-term contracts in the first half of 2022 exceeded 96%, and the annual data has not yet been released. Judging from the performance of each specific contract, the proportion of contracts that can achieve 100% performance in the total contract volume is still not high, and there are uneven Case. In addition, there are still problems such as the obvious decline of coal quality and the confusion of the price mechanism.

The 2023 medium and long-term power coal contract is still in the process of signing.

The National Development and Reform Commission previously issued in October 2022 the “2023 Mid- and Long-Term Coal Contract Signing and Performance Work Plan” clearly stated that in principle, each coal company’s mid- and long-term contract tasks for thermal coal should not be less than 80% of its own resources. For 75% of thermal coal resources, medium and long-term contracts have been signed for the part of nuclear capacity increase since September 2021; coal companies that have not signed in full will be restricted in terms of new project approval, new capacity increase, railway capacity and financial support.

The “Plan” also requires that the contract must specify the coal quality requirements for the type of coal supplied and the quality inspection agencies recognized by both parties, and include “one owed and three supplements” into the contract terms, and a letter of commitment for honest performance should be signed.

Ye Chun, deputy director of the Development and Planning Department of the China Electricity Council, said in response to a reporter from Caijing that under the current situation, signing medium and long-term contracts with coal and electric power companies is an effective means to ensure supply and stabilize prices. At the same time, the increase in the proportion of long-term cooperative coal and the realization of high quality can also largely relieve the fuel cost pressure of coal power companies. However, in order to fully exert the role of “ballast stone” and “stabilizer” in ensuring supply and stabilizing prices of medium and long-term contracts, it is necessary not only to achieve the quantity of contracts signed, but also to ensure the quality of contracts signed, to avoid obscurity and violation, and to ensure the smooth performance of subsequent medium and long-term contracts .

At present, there are still problems in the actual signing work.

Ye Chun introduced that major power generation groups have made great progress in the signing of medium and long-term contracts, but there is still a certain gap from the goal of 100% full coverage. It is understood that mainly due to the lack of willingness of some coal companies to sign contracts, and even the fluke mentality of waiting and waiting, it is difficult for some coal companies to propose unreasonable quality and price terms to reach agreement, and it is difficult to further connect and communicate.

Ye Chun further introduced that there are still irregularities and unreasonable situations in the signing of mid-to-long-term power coal contracts: some coal mines have proposed bundling sales with market coal at a ratio of 3:7 or even 1:3, and this situation has spread from certain regions to various regions. It exists in major coal-producing regions;

Signing “yin and yang contracts” in a disguised form, for example, although the contract signed and entered into the system is divided according to the task, it is clearly stated that only a certain proportion of reduced cash will be cashed offline; Carry out calorific value assessment, etc.;

It is required to reduce the requirements for indicators such as sulfur content, moisture content, ash content, and volatile content, and increase the incentive clause, and increase the price in a disguised form when the contract is fulfilled, reaching 100-150 yuan/ton;

Some traders have high service fees in the circulation link, and some agency service fees exceed 50% of the coal price; and there are irregular requirements such as increasing the proportion of advance payment and setting deposits or guarantee deposits.

In response to these problems, Ye Chun said that it is currently in a critical period for the signing of medium and long-term power coal contracts in 2023 to fully cover the “hard bones”. While further promoting the signing of long-term agreements, strengthen contract review and timely correct irregular signing behaviors. Only by maintaining the seriousness of medium and long-term contracts for thermal coal can we effectively lay the foundation for ensuring the supply and price of thermal coal in 2023.

The China Electricity Council also suggested in the analysis and forecast report that the signing of contracts should be strictly regulated, and all kinds of illegal profit-making behaviors such as price increases in disguise and lowering the calorific value of redemption should be stopped, and a strong signal for stabilizing market prices should be released.

This article is from the WeChat public account “Finance and Economics Eleven” (ID: caijingEleven) , author: Han Shulin, 36 Krypton is authorized to publish.

media reports

36Kr Sina Sina interface

related events

- The China Electricity Council predicts that electricity demand will increase by 6% in 2023, and the supply and demand will be tightly balanced throughout the year2023-01-20

- National Energy Administration: From January to June, the electricity consumption of the whole society increased by 2.9% year-on-year 2022-07-14

- National Energy Administration: The electricity consumption of the whole society will increase by 10.3% year-on-year in 2021 2022-01-18

- In June, the electricity consumption of the whole society increased by 9.8% year-on-year 2021-07-15

This article is transferred from: https://readhub.cn/topic/8mIyVsaFUdK

This site is only for collection, and the copyright belongs to the original author.