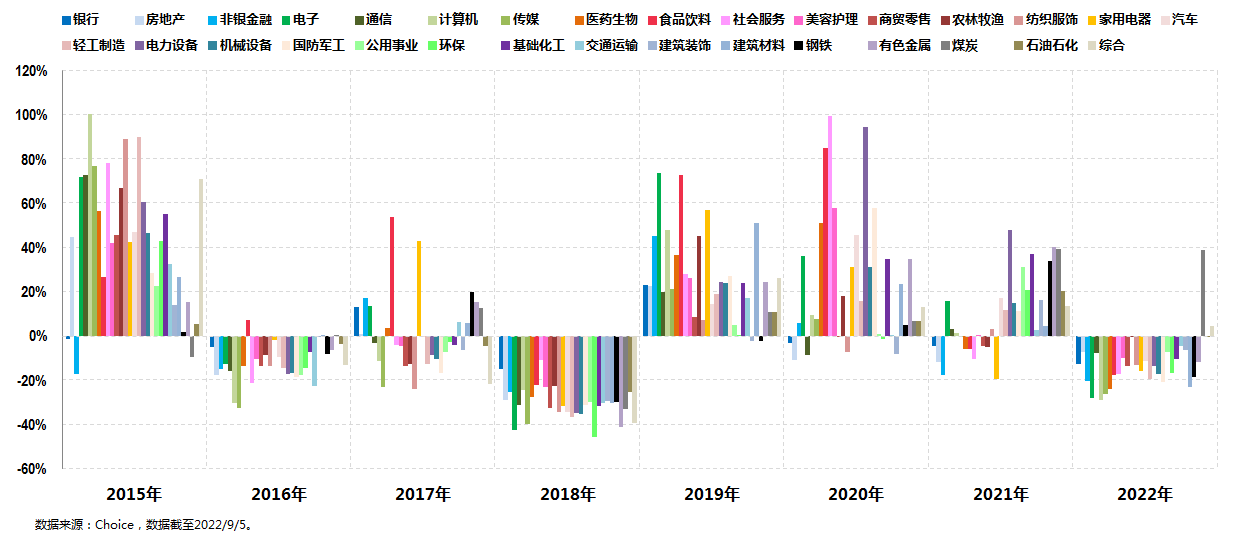

Although people say that investing is difficult every year (this is true, because investing itself is not easy), the difficulty of investing in 2022 is indeed relatively high. If you must give a quantitative indicator, it should be at least “one year in seven years” The last time such a differentiated market occurred was in 2016.

Some friends may say that it is more difficult to fall almost the whole year in 2018?

Really not, because 2018 is a year when all industries are “collectively lying flat”, even the most resilient banking sector has fallen by nearly 15%, so it is common for a sector to fall by 20%-30%. .

There are no finished eggs under the overturned nest, and it is not too difficult for people to have no finished eggs.

And the same is the differentiation market, 2022 will be more difficult than 2016.

This is because in 2016, although there was only one sector with positive returns, firstly, this sector with positive returns was called food and beverage (the sector’s annual income was 7.43%), and secondly, the conventional safe-haven sector of that year, the banking sector, was “only” “It fell -4.93%, so that even if a group of active funds in the mainstream market did not achieve positive returns, there were not many negative returns. After all, these two major sectors (mainly the banking sector) were the most important market center CSI 300 in that year. weight plate.

But 2022 will be completely different, and everyone has seen it. Except for the little-known coal sector, which has risen by nearly 40%, other sectors are not only “exhausted”, but also “inked” a bit miserably:

As of September 5, 2022, there are 8 sectors that have fallen close to or more than 20%, and even the big-eyed food and beverages and banks have fallen by more than 10%, so that the benchmark for conventional active funds The CSI 300 has collapsed, so there is such an embarrassing situation: the more familiar it is, the worse it falls, and the better it rises, the less familiar it is.

This can be seen from the figure below:

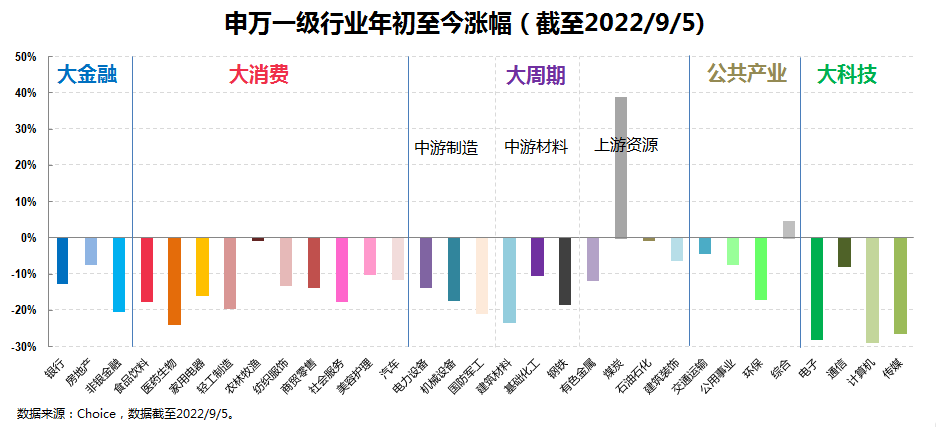

The picture above shows the rise and fall of the Shenwan primary industry this year. As can be seen from the figure:

On the one hand, the cyclical category, especially the upstream resources category, is the best. Except for the outstanding coal, petroleum, petrochemical, construction, etc. have hardly fallen. Similarly, the public utilities and transportation in the public industry have not declined much. Other small declines include real estate in big finance, agriculture, forestry, animal husbandry and fishery in big consumption, and communication in big technology.

In addition to being basically non-mainstream sectors, the above sectors can be roughly divided into two major themes: one is called “old energy power generation”, including coal, petroleum, petrochemical and public utilities (hydropower, wind power, etc.); the other is called “predicament reaction” “Transfer”, including transportation (aviation, etc.), real estate, agriculture, forestry, animal husbandry and fishery (pig and chicken breeding, etc.), and communications, etc.

On the other hand, the worst sector is undoubtedly the electronics, computers and media in big technology (and the China General Internet, which suffers from the same disease), plus a medical biology, the two parts add up to the technology sector in the broad concept.

Based on the above facts, we briefly discuss three topics in this issue:

The first topic: what is worth buying, why are these funds so popular

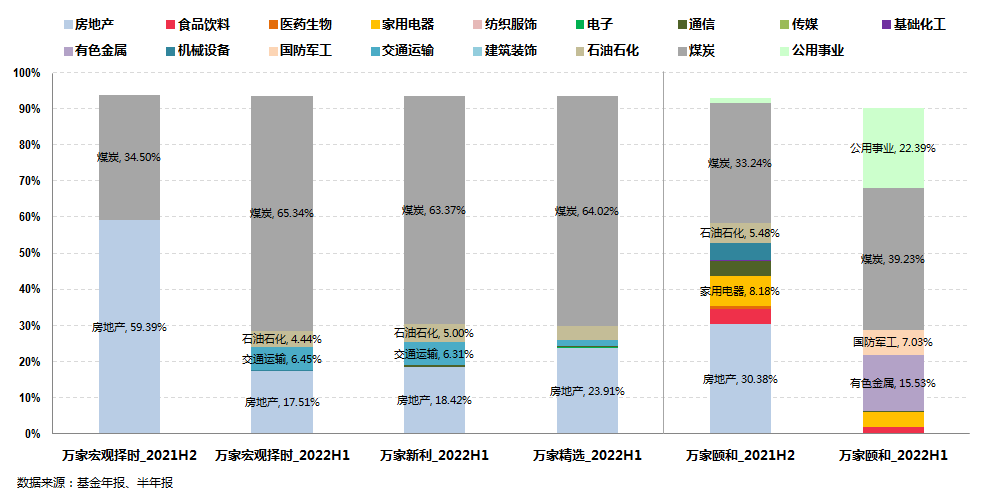

To say that this year’s most “hatred” fund manager is probably the “Shuanghai” combination of Wanjia. This is because the four funds they manage have almost always been at the forefront of the stock-biased active fund this year:

Among them, the three funds managed by Huanghai, Wanjia Macro Time, Wanjia Xinli, and Wanjia Select, which have the least income this year (as of September 5, the same below) have also achieved more than 50% of the income, and the most are fast The return is close to 70%. Since the beginning of this year, it is far ahead of other partial stocks and active bases, ranking the top three in the whole market.

On the other hand, Wanjia Yihe managed by Zhang Heng has competed for the fourth place for more than half a year with the most attractive fund this year, Jin Yuan Shun An Yuan Qi, and has not yet decided the winner.

I think most of you already know the reason for this:

From the perspective of the industry, the more heavily held the coal sector, the better the performance of the fund this year. The three products managed by Huanghai are enough to illustrate the problem: its industry allocation is basically from heavy holding of coal to more extreme heavy holding of coal.

Although Wanjia Yihe managed by Zhang Heng is not as heavy as Huanghai, its allocation ratio of close to 30%-40% is enough for a heavy position. It is understandable that the performance has been good this year.

The key question is: is the product of these two fund managers worth buying?

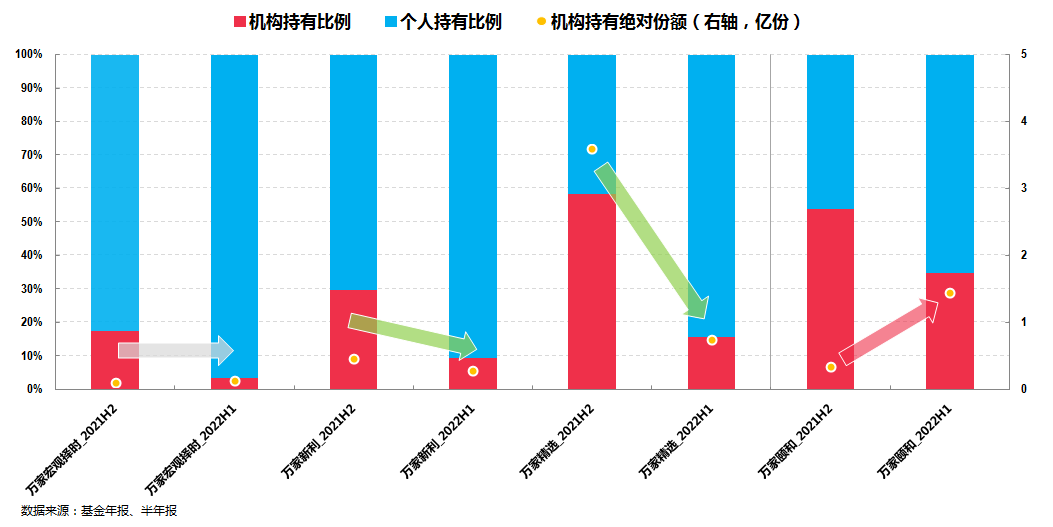

As the saying goes: peaches and plums do not speak, and they form their own paths. On this issue, we may refer to the choice of the following institutions:

Judging from the selection of institutions, Wanjia Yihe managed by Zhang Heng was significantly increased (the absolute share almost doubled by 4-5 times), but the three products managed by Huanghai were either slightly reduced or significantly reduced. It can be seen that the extreme style is always difficult to meet the aesthetics of institutions, which I think is very worth learning from our ordinary investors.

Speaking of institutional aesthetics, here are a few fund managers who are truly in line with institutional aesthetics and have performed better this year.

For convenience, here is an example of the representative fund they manage:

The first Zhonggeng Qiu Dongrong doesn’t need my introduction. I think many people are familiar with it. His PE-ROE investment framework was famous as early as the HSBC Jintrust Fund period. I don’t know if you still remember the “big chicken” ?

Since it is basically not a problem to buy him or not, I will only add one point here: the best choice for buying his products may not be the pilot of the value of Zhonggeng, but the quality of the value of Zhonggeng for one year, and the reason for this can be tasted by yourself. .

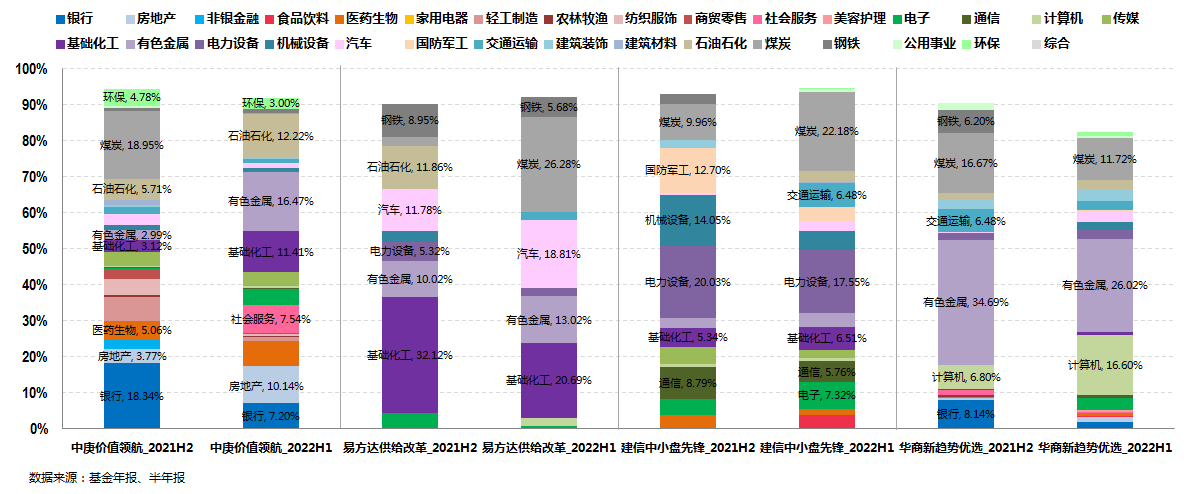

The second E Fund, Yang Zongchang , I once said when I was talking about industry-themed funds. Yang Zongchang, a Ph.D. in chemistry, has been taking a niche route to deeply cultivate the chemical sector since the management of the fund. Before the reform of E Fund’s supply, it can almost be regarded as a chemical-themed fund. .

However, since 2022 (based on 2021), its industry coverage has expanded, upstream resources (coal, petroleum and petrochemicals, nonferrous metals), midstream resources (chemicals, steel), midstream manufacturing (mechanical equipment, power equipment), downstream vehicles, etc. There are involved, the overall industry is more dispersed and balanced, and he has been favored by institutions since he managed products.

Although the third Zhou Zhishuo has managed funds for less than 2 years, his excellent industry allocation, rotation ability, and ability to select individual stocks have been fully demonstrated in the past two years. While achieving excellent performance, he has been highly recognized by institutions. Almost most of its tens of billions of dollars were bought by institutions in a short period of time, and it can be said that it is one of the most valuable new stars in the current market.

From the perspective of industry configuration, his latest positions can be said to be old energy (coal) and new energy (power equipment), the key is that both are still quite strong.

The fourth Zhou Haidong is actually a veteran. His investment is characterized by starting from a macro and meso perspective, picking stocks from the top down, and digging out companies that are in the boom cycle in the future and have an obvious upward inflection point. He is good at cycles and growth. Plate, investment is on the left side. The products it manages have also been favored by institutions in recent years.

Another point worth noting here is that in addition to upstream resources (nonferrous metals, coal), its latest industry configuration has also significantly increased its positions in the computer sector.

The second topic: the “fall” of big technology: the tragedy of TMT themed funds

Having seen the sectors and representative funds that have risen the best this year, I think it is also necessary for us to look at the sectors and representative funds that have fallen the worst this year.

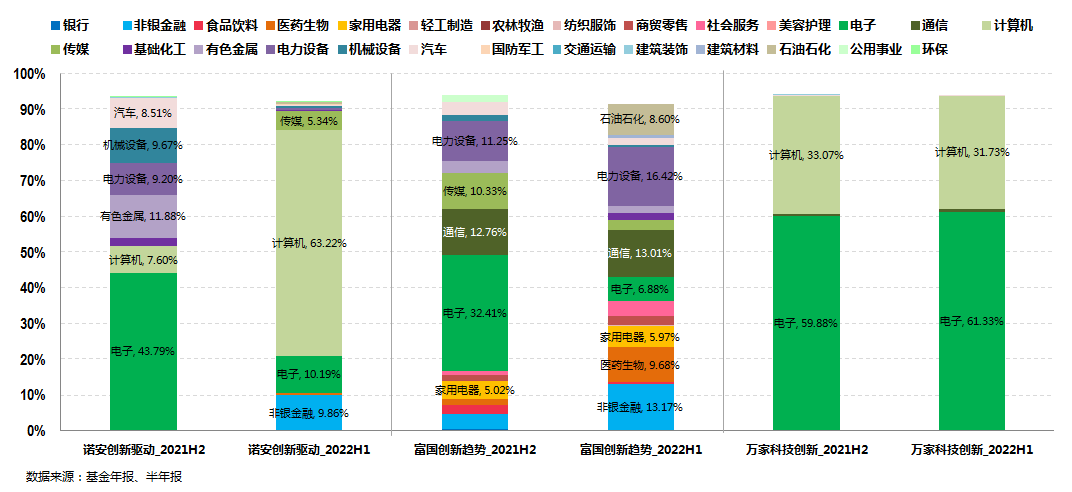

As the saying goes, the most beautiful is the red sunset, and the worst is TMT. This year’s TMT is really a bit miserable. I found a few familiar players on the bottom list to show you.

The eldest brother on the list is Cai Songsong, who has “become famous” with Lion’s growth . Here we choose Lion’s innovation-driven fund, which currently ranks at the bottom of the market. From the perspective of industry configuration, this base is not as “chip semiconductor” as Lion’s growth. Although it will also reconfigure the electronics sector in 2021, this product has begun to heavily store the computer sector since the first quarterly report in 2022. The 2022 interim report shows that its computer sector accounts for more than 60%, so now this is a computer-themed fund?

The name of the second Fuguo Li Yuanbo appears many times on the list. As a player whose investment is relatively focused on the TMT field, it is understandable that his performance is not good in the context of the overall decline of the TMT sector. Judging from the industry configuration changes from the annual report to the 2022 mid-year report, this product seems to be more balanced across the industry.

The third Wanjia Huang Xingliang is also well-known in the market for his investment in TMT. Since the beginning of this year, many products have also ranked low. From the perspective of their industry configuration, it is “rare” and extremely stable, and still maintains a heavy allocation of electronics and computers. The saving grace here is that once the TMT sector has rebounded, the tool-like nature of his management products has an advantage.

There are also a large number of pharmaceutical-themed funds named after medicine or medical treatment on the lower-ranked list, which is understandable, because in addition to TMT, there is a pharmaceutical and biological sector in all industries that has been miserable this year, but here I will not Expanded, we can focus on this sector in the discussion of valuation and investment in the future.

The third topic: the myth of industry equilibrium – is the balanced configuration really bad?

This topic comes from a question from a friend.

In fact, we can know from the industry comparison above that the performance of mainstream industries has not been good since the beginning of this year, and most of the industries that performed well are traditional niche industries, so even if the industry is balanced, the returns this year will not be too good. Therefore, if the balanced portfolio returns this year are around -15%, it is actually acceptable, and if it can be within -10%, it is considered an excellent performance.

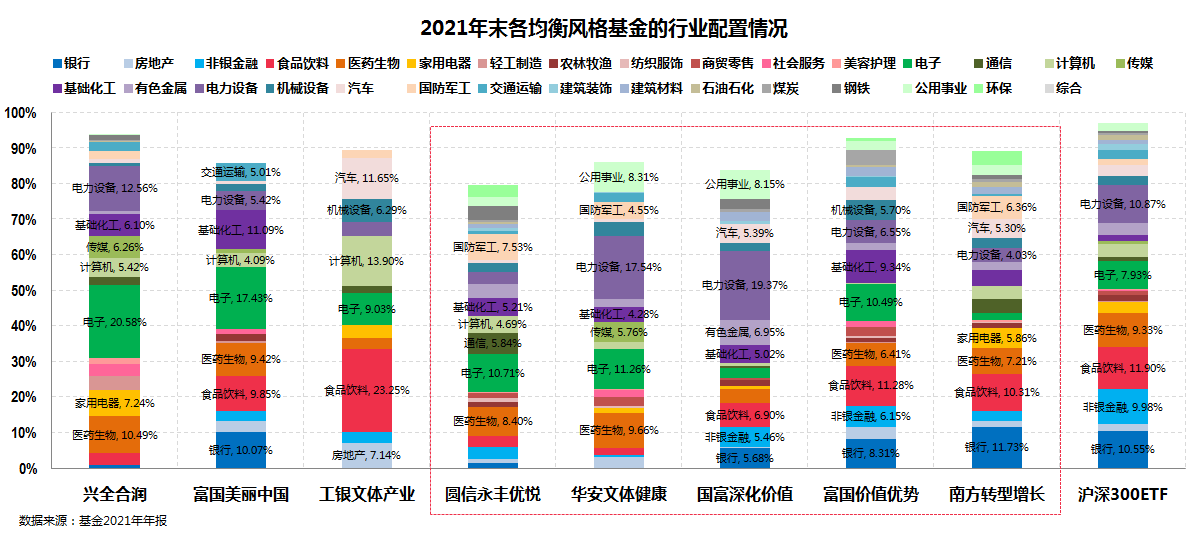

Based on this premise, here is a rough list of some typical balanced style funds.

Among them, the top three have obviously re-allocated TMT and large consumption, and almost do not allocate cyclical sectors, which is not only the reason for their good performance in the past few years, but also the reason for their relatively poor performance this year.

The performance of several balanced style funds in the red box is relatively good. From the perspective of the industry, the proportion of cyclical manufacturing allocation of these balanced style funds is significantly higher, and the overall TMT allocation is generally lower. The industry is also more fragmented.

Of course, there is another hidden point here. Under this kind of differentiation since the beginning of this year, it is also a balanced style. Fund managers with a certain industry mesoscopic perspective or cyclical thinking will be better than fund managers who purely select stocks from the bottom up. Slightly better.

For example, Yuanxin, Yongfeng Fanyan and Lin Lefeng from the south in the red box have a mesoscopic perspective on the investment of the industry, while Huaan Liu Changchang has a certain cyclical thinking despite bottom-up stock selection.

So far, the three topics are basically finished, but it seems that more of this is just a list of facts, corresponding to 1) which funds have risen well this year, 2) which funds have fallen a lot, and 3) balanced fund performance in a compromise, but It seems that there is no discussion about it, so we will briefly discuss it in the last part.

From a practical investment perspective:

First, if you want to follow the trend, perhaps the cyclical industries represented by coal, petroleum and petrochemicals, especially new energy represented by power equipment, etc., may still be the general direction of short- and medium-term investment.

This is both “maybe” and “maybe”, and it’s more like listening. Fortunately, we don’t have to make our own judgments in this part. After all, it’s easy to lose money with the strength of our ordinary investors, but we It is completely possible to use the funds of those players who are good at cycles or industry rotations in the first topic to do this part of the layout, especially in the current complex market background.

And, even if we can’t make sure they’re always accurate, we can at least make sure that they’re definitely a lot better than us.

Second, if you want to invest in a reverse direction, then the major themes of “dilemma reversal” may be the general direction of the next investment, and even the worst TMT (including the even worse China General Internet) and pharmaceutical biology are also not. Not that there are no opportunities for reverse layout.

Similarly, we do not need to do this industry-level “contrarian investment” ourselves, and we can still use the power of professional fund managers to do this part of the layout.

I recommend three contrarian investors who are my personal preference for reference: Lin Yingrui of GF Fund, Hu Yibin of Huaan Fund, and Mo Haibo of Wanjia Fund .

For specific investment methods, you can also refer to the article “Reverse of Reverse, a Low-Risk Dip-Buying Method” .

Third, if you want both, you still have to choose a balanced style.

Although the extreme market differentiation since the beginning of this year has devastated the balanced style, from the perspective of long-term investment, at least I personally prefer to choose the balanced style, even if I also have some funds of the two ideas mentioned above, but It is more configured as a satellite position, and the core position is still a balanced style fund.

Of course, if you have to dig out some small waves within the balanced style fund, especially in order to deal with the differentiation of the market this year (in fact, it started at the beginning of last year), it is also simple, as in the third topic As mentioned, we can choose some fund managers with industry mesoscopic perspective or cyclical thinking to deal with it.

above.

@Today’s topic @snowball fund @snowball creator center

This topic has 0 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/4354731086/230652390

This site is for inclusion only, and the copyright belongs to the original author.