foreword

The purpose of posting is to find colleagues. I don’t mind those who have no research ability for nothing, but please figure out your contribution and value. Don’t mistakenly think that others are working for you for free, and don’t mistakenly think that others are yours. Cheap parents.

Warmly welcome colleagues to go down together! Make up for each other and make progress together!

text

1. Historical overview

The role of tin as a metal is mainly welding, and silver can replace this role, and it also has a small amount of chemical effect.

As we enter a huge electrified and electronic society, there is no need to say more about the demand for “welding”.

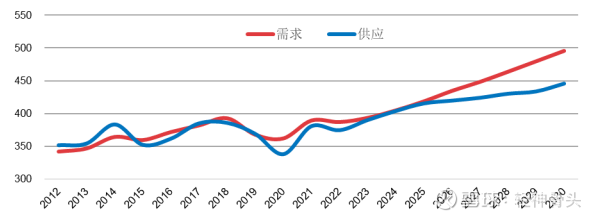

Tin, a metal with many fates, should have surfaced a long time ago, but in 2015, a super-high-grade mine appeared in Myanmar, and it was not until 2018 that the super-high-grade mine was dug with a grade of 10%, and the supply increased greatly. In 2020, but experienced the blow of the epidemic again, the demand fell accordingly. As shown below (this picture only looks at the history):

Second, the status quo

More than 70% of tin demand is in Asia, and 47% is in China. The supply is also similar, the duopoly structure of Indonesia and China, and the 50% oligarch structure of Yunxi in China. Indonesia’s policy is to gradually tighten export supply, and there may be further restrictions in January.

Twenty-five years ago, there were more than 20 new mining projects in the world, but only 6 of them could have a better increase. African Tin and First Tin ranked first, and the projects of African Tin increased by about 700 tons per year.

The existing mines are basically in a state of obvious decline in grade, digging deeper and further away from the coast.

3. Downstream situation

The downstream is mainly electronics (the largest head, electric vehicles are classified into this category), photovoltaics, tinplate, and tin chemicals (lead-acid batteries account for 8% and are classified into this category). Except for electronics that have shrunk in recent years, the others are growing significantly.

Consumer electronics has actually reduced demand by 20% in 22 years. Home appliances decreased by about 3%, and integrated circuits decreased by 13%. Semiconductors grew about 4.5%. A very miserable year.

Photovoltaic has increased by about 70% in 22 years. The amount of tin used by photovoltaics is 71.4 tons/GW. This was calculated in detail by me and the knight. Later, I found that it was almost the same as the market statistics. If other welding requirements for photovoltaics are added, the photovoltaic industry may pull 74 tons. /GW. Then the 450GW demand for photovoltaics for tin in 23 years is 33,300 tons, which is 22,900 tons more than the demand in 21 years, accounting for 6% of the global total and 12% of my country’s.

That’s why I started paying attention to tin.

I have seen the figures of tin used in electric vehicles before, but I have not verified it. Looking at the big figures in the industry, it is about 12,600 tons added in 25 years, accounting for 3% of the current global total demand.

Both tinplate and lead-acid batteries have improved significantly. As an aside, lead-acid batteries may be thought to be replaced by lithium batteries, but the reality is the opposite, which is interesting.

So how much is the total? China’s production fell by 5.3%, ex-China increased by 2%, and global production fell by only 1.5%. China’s consumption fell by 2.9%, and excluding China, it fell by 0.5%, and the global total demand fell by only 1.6%. In 23 years, photovoltaics and electric vehicles will have a greater increase. If electronics can pick up, then the demand situation in 23 years will be very exciting. With the loosening of the real estate policy, home appliances are still bright. I am not familiar with the consumer electronics industry, but the results of the inquiries, it is generally believed that this year will pick up in the second quarter.

Fourth, the upstream situation

in stock. In the past two decades, the inventory has been decreasing. In 2022, the global inventory was 27,000 tons, but I found a very interesting thing: I counted the tin ore and tin ingots imported by my country. This year, the net import increase is exactly 3 About 10,000 tons, that is, it is useless to buy 30,000 tons more, and it is saved. What does it mean? This means that taking advantage of the sharp drop in tin prices this year, the global inventory may have been transferred to China. Check the imports of mines in Myanmar and refined tin in Indonesia this year. The volumes are indeed very large. Do you understand what this means?

mine. As mentioned above, the grade of all existing mines has declined, mining is difficult, and the increment of new mines is small. Due to the war in Myanmar, only about one-tenth of the stock was sold. Now the mines are all of low-grade mines, and the mining cost is estimated to be more than 190,000. Our country should have a mining cost of more than 180,000.

In the past six months, it has become more and more difficult to purchase raw materials for smelters, and now it is almost impossible to buy mines. This phenomenon is also very interesting. It is impossible to stop mining. Our country has bought so many mines and has not consumed them. The increase is about 50%. Why can’t smelters buy mines now? Where did the mine go? I think the only answer is that mines are hoarded.

Question: 1. After the epidemic in 23 years has passed, if electronics returns to the level of 21 years, who can provide the additional demand gap?

2. There must be a surplus of tin now, and the downstream has not started work during the Spring Festival. Why are the spot and futures of tin soaring, and it is still on the rise?

5. Enterprise

I will not write the detailed analysis of Yunxi, but only the key points.

Yunxi digs about 24,000 tons of tin by itself, but smelts more than 50,000 tons of tin, and ships 80,000 tons of tin in total. At the industry conference just held, it also said that it will ship 30,000 tons of tin in 23 years. It also set the target at 30,000 tons before, but it has not been realized. Now it is estimated that it may be able to achieve it by stocking up.

The cost may be tens of thousands lower than the domestic 180,000 per ton. I don’t know who has a reliable analysis in this regard.

In addition, there are tens of thousands of tons of copper and zinc. I have carefully looked at them before, but I am too lazy to look at them now.

Yunxi is a company that has been mining tin for more than a hundred years. Under the current background of the rise of state-owned enterprises, I don’t think its management can be so bad. Some people point out the hedging loss in 21 years and the one billion inventory provision in 22 years to say that the management is poor. In fact, I think both hedging and inventory provision are normal, especially the inventory provision is just a matter of numbers. .

It’s just that Yunnan State-owned Assets has never been very famous. It is inevitable that we must pay attention to that in the future.

It is very likely that the profit of Tin Industry Co., Ltd. will be maintained at more than 5 billion in the future, and I am not surprised to reach 15 billion. The time may not be 23 years.

$Gold Molybdenum Share(SH601958)$ $Tin Industry Share(SZ000960)$

There are 113 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/7590109814/239513155

This site is only for collection, and the copyright belongs to the original author.