From the stage high on August 19, the photovoltaic concept index (CN: BK0478) has dropped by 20%. For PV investors who have been accustomed to eating meat in the past three years, such a callback is unavoidable: Is the cycle turning point of China’s PV industry already approaching?

In order to clarify this problem, we have carried out a detailed review of the development of the photovoltaic industry, hoping to achieve a vision of the future development of the industry through awe of history.

The strength of the photovoltaic industry does not always end. The most recent calamity in the market’s memory is that because the cost of power generation has always been high, after the industrial subsidies have declined (531 New Deal), the market was once full of doubts about the future of the photovoltaic industry. , the overall valuation of listed companies fell to historical lows.

Figure: Photovoltaic Concept Index (CN:BK0478) Weekly Trend, Source: Snowball

However, with the continuous improvement of industrial technology, the continuous improvement of photovoltaic power generation efficiency, and the huge demand released by the energy reform, the growth rate of the photovoltaic industry has been released rapidly. Behind the fruitful harvest of photovoltaics, technological maturity is a prerequisite, and demand release is the direct driving force. Under the resonance of technology and the times, investors’ expectations have been completely reshaped.

Looking at the overall situation, the rise of new energy is only the beginning, especially in the case of the continuous tension of overseas geopolitical situation, it has increased the certainty of the global market’s demand for the photovoltaic industry. The fall in the valuation of related companies is more like the fading investor confidence caused by external factors, and the core driving force of the industry is still there, indicating that photovoltaic companies are far from over, and there are still stories to tell.

After photovoltaic power generation achieves grid parity, the competitiveness of photovoltaics compared with traditional energy sources begins to emerge, and the impact of technical factors on the photovoltaic industry will be reduced. However, the so-called “parity” is not the end. Cheaper and cleaner electricity is still the eternal pursuit of people. How the industry will evolve in the future to meet the growth in demand.

In this context, we believe that the photovoltaic industry will enter the era of 2.0: the era of vertical integration.

01 Industrial trend: integration becomes inevitable

First of all, we need to take everyone to think about it: what is the first principle of photovoltaics? In fact, the answer is very simple, that is, cost reduction. Because the final commodity produced by all power generation methods is electricity, and electricity is the most typical standard product. No one will care whether the electricity I charge for my mobile phone today comes from thermal power, hydropower, photovoltaic, wind power or nuclear power. The lower price is the ultimate standard. The only law of competition for products.

Therefore, the history of photovoltaic development is a history of price reduction. However, the core driver of price reduction is gradually migrating, and it is precisely this turning point that we see, so we divide the development stage of PV into 1.0 and 2.0.

1) Technological innovation is the main theme of the photovoltaic 1.0 era

Since the establishment of Suntech in Wuxi in 2001, China’s photovoltaic industry has experienced at least 20 years of great waves and sand era, and finally formed a strong supply chain system with detailed division of labor. Whether it is upstream polysilicon, midstream cells, or downstream components, the main market share is firmly occupied by Chinese companies.

Looking back at the rise of China’s photovoltaic industry, the new technology driven by innovation is the key to success. The story of the latecomers catching up and surpassing has become a business story that everyone talks about.

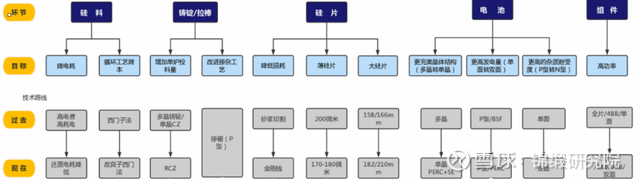

Figure: Technological progress in each link of the photovoltaic industry chain, source: Industrial Securities

For example, after LONGi introduced the diamond wire cutting technology into the field of single crystal silicon wafer cutting, the entire cutting rate was increased by 2-3 times, and the cost was greatly reduced. In 2015, my country issued the “Energy Efficiency Leader System Implementation Plan”, which clearly defined the main tone of promoting the application of advanced photovoltaic technology products and industrial upgrading. Monocrystalline silicon technology with higher conversion efficiency has become a breakthrough technology, subverting the previous market dominated by polycrystalline silicon. pattern. Today, monocrystalline silicon wafers with higher power generation efficiency and lower cost per watt have achieved overtake and become the mainstream.

For another example, Tongwei began to optimize and verify the polysilicon production process and equipment in 2007. By 2014, it has carried out four technical transformations, and its comprehensive energy consumption has dropped from the initial 180-200 degrees per kilogram to 2015. The annual temperature is about 60 degrees per kilogram. With the continuous innovation of technology, the comprehensive power consumption, steam consumption, silicon powder consumption and other production indicators have continued to decline. At present, the production cost of Tongwei polysilicon has dropped to 30,000-40,000/ton (excluding the impact of industrial silicon market price factors, at constant price) calculation), equivalent to 1/3 of the mainstream market price in 2015.

In addition, the application of new technologies such as cold hydrogenation, anti-disproportionation, high-boiling cracking, continuous Czochralski technology, RCZ single crystal growth, single crystal PERC, double-sided power generation, and multi-busbars has made the cost of photovoltaic power generation continue to drop, promoting With China’s photovoltaic industry to the forefront of the industry.

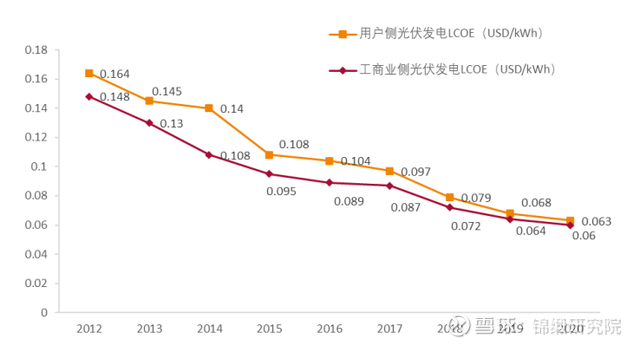

Figure: 2012-2020 PV power generation cost decline trend, source: Tianfeng Securities

It is not difficult to understand that the reason why China’s photovoltaic industry has been able to catch up all the way to lead the world is due to the technological changes in the past two decades. New technologies have driven the industry to continue to reduce costs and increase efficiency. technology R & D. It can be said that this is the 1.0 era of the photovoltaic industry.

In an era when technology is king, what is the most efficient business model is that each enterprise concentrates all its strengths on one point to tackle tough problems, and finally completes the innovation of the industrial chain together. This model is still vigorously performed in the field of semiconductors and innovative drugs today.

2) Vertical integration has become the keyword of the photovoltaic 2.0 era

Although future technological development will still serve as the core driving force of the photovoltaic industry, the technical route of each link except for cells is relatively clear, and the technological momentum has begun to show fatigue. This is why, in the photovoltaic industry, which used to change frequently, in recent years, the industry leaders are always a few old faces.

The pursuit of cost reduction is endless. We see that after the rapid technological iteration kinetic energy decays, the vertical integration strategy driven by leading enterprises has gradually become a new trend in the development of the industry in recent years.

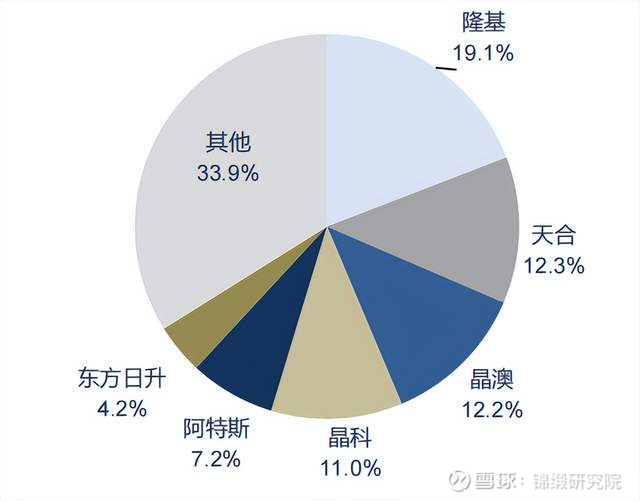

Talk to the data. According to Solarzoom data, LONGi Green Energy, Trina Solar, JA Solar, JinkoSolar, and Canadian Solar will be the top five companies in global PV module shipments in 2021, with a combined market share of 61.8%, and all other manufacturers accounted for only 38.2%.

Figure: 2021 module industry landscape (by shipments, GW), source: Solarzoom, Soochow Securities Research Institute

Among these five component leaders, without exception, the vertical integration strategy is regarded as the focus of future development.

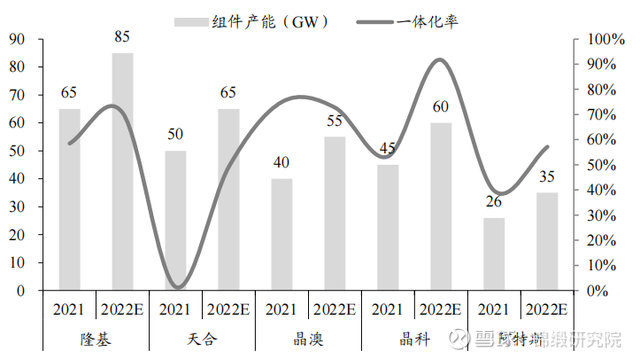

LONGi Green Energy, JA Solar, and JinkoSolar have made an early integration layout. The current integration rate is over 50%, and the proportion of external mining has successfully dropped significantly. Originally, Trina Solar was the only professional component leader without integrated layout, but on June 17 this year, it announced a high-profile investment in the construction of Qinghai (Xining) Zero-Carbon Industrial Park, fully embracing vertical integration.

Moreover, Trina Solar’s “integration” is very thorough, not only laying out silicon wafers upwards, but also covering polysilicon and its raw material industrial silicon, and laying out components and auxiliary materials downwards. It is reported that Trina Solar will invest in Qinghai with an annual output of 300,000 tons of industrial silicon, 150,000 tons of high-purity polysilicon, 35GW of monocrystalline silicon, 10GW of chips, 10GW of cells, and 10GW of modules. 15GW module auxiliary material production line.

In a sense, Trina Solar’s transformation is a landmark event in the acceleration period of the photovoltaic industry 2.0 era.

Figure: Comparison of leading module production capacity and integration rate (GW, %), source: CPIA, Soochow Securities Research Institute

Through the vertical integration strategy, the strategic autonomy of the enterprise will be significantly improved, which will not only effectively control the terminal cost, but also further ensure the timely delivery of orders, which is of positive significance to the company’s production capacity planning and business development.

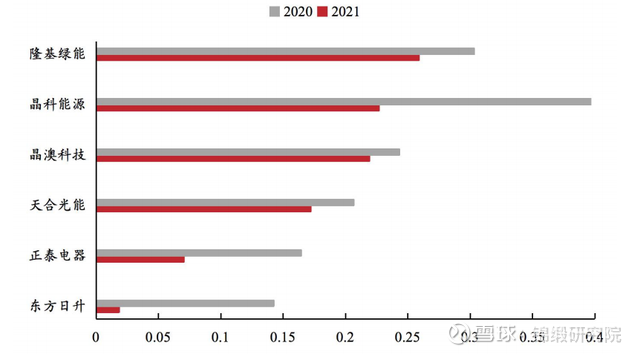

More importantly, vertical integration can effectively guarantee the company’s position in the industry and future income stability. From the current results data, module companies with a high integration rate have significantly stronger profitability per watt of their module business than companies with a low integration rate.

Figure: 2020-2021 module business profitability per watt (yuan/W), source: Wind, East Asia Qianhai Securities Research Institute

02 Enterprise response: how to deal with yourself in the 2.0 era?

1) Shift in strategic adaptation

The wheels of industry development are rolling forward, and achieving strategic adaptive transformation in the 2.0 era is a topic that every enterprise needs to face.

Taking Tongwei as an example, since the integrated layout has not yet been completed, although it has made a lot of money in the past two years, its business layout must consider two issues:

Single pressure brings naturally high volatility. Many investors saw the boom in silicon materials in the past two years and thought it was a lucrative industry, but in fact, in the past ten years, silicon materials were not very profitable business, and even fell into serious losses for a time. among. Tongwei’s high profitability is due to bold counter-cyclical investments. For example, from February to March 2020, due to the impact of the epidemic, domestic polysilicon prices fell to the lowest point in nearly 10 years; however, Tongwei made counter-cyclical expansion of production capacity at that time. The decision to build “Baoshan Phase I” 37,500 tons and “Yongxiang Phase II” 50,000 tons of silicon material projects. Essentially, it is a highly volatile industry, similar to lithium mines in the lithium battery industry.

Long-term concerns about excess silicon material. What is currently lacking in the photovoltaic industry is silicon material. Now that there is too much talk, it is estimated that some people think it is unfounded. In fact, it is not. With the unstoppable trend of photovoltaic industry integration, this will lead to an ending – many upstream silicon companies may not have so many buyers for their new production capacity.

Figure: Silicon material quotation: super dense material (yuan/kg), source: Solarzoom, China Galaxy Securities Research Institute

How to adapt to the industry 2.0 trend? Preemptive strikes, and later strikes are made by people. Since downstream components are integrated upstream, upstream companies can also extend downstream. It is precisely driven by this underlying logic that Tongwei, still guarding the “gold mine”, began to actively enter the component market. We believe that in the future, we will see more and more news of this kind.

2) Discussion of strategic rationality: starting from the high threshold of components

Extending to the upstream or downstream of the industrial chain is easier said than done. With the direction, photovoltaic companies need to do feasibility research. An analogy is, is it easier for Huawei to make cars, or is it easier for Weilai to make chips?

For the photovoltaic industry chain discussed in this article, we discuss the most controversial component segment in the market.

As the only industrial link dealing with end customers, components were not taken seriously at the beginning, and were once considered by the market to have strong user stickiness and brand power. Before Tongwei entered the component business, the short-term consensus finally formed in the market was this A field has a very high entry barrier (so the capital market has also given a high valuation).

But what investors didn’t expect was that Tongwei’s full entry into the module business immediately triggered a continuous decline in the share prices of module companies, and the market’s belief in the module’s leading moat was instantly wiped out.

On August 17 this year, Tongwei became the first bid-winning candidate for China Resources Power’s 3GW centralized procurement order, less than a month later. On September 6, Tongwei won the bid for Guangdong Electric Power Development Co., Ltd. as the first bid-winning candidate. A large order of 400 million yuan of components.

Picture: Tongwei’s photovoltaic modules won the bid, source: Soochow Securities

This makes people wonder, is the threshold for components high?

As we all know, photovoltaics mainly rely on cells to generate electricity, but the output voltage of a single cell is too low to be used independently, and must go through a certain number of series and parallel connections; at the same time, the cells are easily corroded by the external environment and have poor tolerance. , prone to recession. In order to ensure the normal production of the cells, it is necessary to ensure the smooth operation of the cells through the packaging process.

The module is not only the smallest unit that can provide direct current output and is inseparable, but also the direct carrier of the downstream terminal, so it is regarded as the core of the entire photovoltaic power generation system.

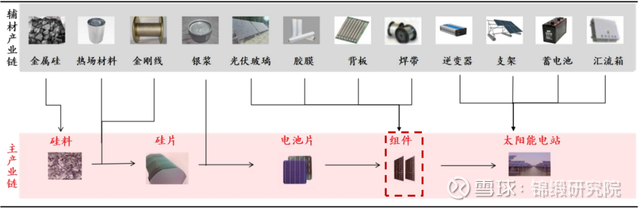

Splitting the photovoltaic module structure, it is not difficult to find that it is mainly composed of cells, photovoltaic glass, adhesive film, backplane, welding tape and other components. Different from the efficiency competition between silicon wafers and cells, the core purpose of modules is to ensure the stability of power generation efficiency of cells through packaging, so it will test the engineering process of enterprises.

Figure: Schematic diagram of photovoltaic main and auxiliary materials industry chain, source: Haiyou New Materials prospectus, East Asia Qianhai Securities Research Institute

Looking at the entire photovoltaic industry chain, the module segment is one of the few asset-light businesses, and the core business is mainly packaging. Therefore, the traditional business model mostly relies on outsourcing. Although its own profit margin is not high, it has a high asset turnover. Rate. In view of such industry characteristics, the core competitiveness of component companies mainly includes three aspects: engineering capabilities, brand effects, and supply chain capabilities.

Tongwei is a latecomer in the industry and does not have the brand premium advantage of traditional module manufacturers. However, for many years of silicon material production, it has accumulated mature engineering capabilities, technical reserve capabilities, recognized industry-leading corporate management style, etc. The strong upstream supply chain capability brings Tongwei sufficient capital to grab the module market.

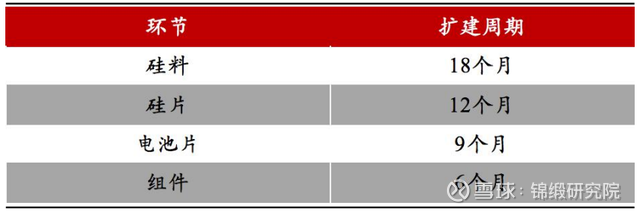

In addition, in the entire photovoltaic industry chain, the shortest expansion cycle of modules is only 6 months, and the longer the industry upstream, the longer the expansion cycle. Although component manufacturers have already started vertical integration, Tongwei’s top-to-bottom layout is significantly faster and more efficient.

Figure: Production expansion cycle of each link in the main photovoltaic industry chain, source: announcements of various companies, East Asia Qianhai Securities Research Institute

In general, although photovoltaic modules have certain barriers to entry, for veteran players like Tongwei who have strong supply chain advantages, and Tongwei’s 40-year strong brand building, building and dissemination integration capabilities, it does not need to spend too much time and The cost investment can catch up or even surpass. That is to say, for Tongwei, the barriers to modules are not high, which is why the market is bullish on new entrants Tongwei and bears on traditional module companies.

Back to the company’s strategic choices, we believe that integration is the correct strategic direction, and at the same time, we must ensure that our extended tentacles are still within the scope of the circle of competence, both of which are indispensable.

03 Future stories are still worth looking forward to

1) The industry value of the whole chain that the market will eventually recognize

After completing the incubation from 0 to 1 and from 1 to 10, the photovoltaic industry will actually face a growth process from 10 to 100 in the future. With the continuous deepening of the vertical integration process of the industry chain, the future competition target of the photovoltaic industry chain has actually changed quietly.

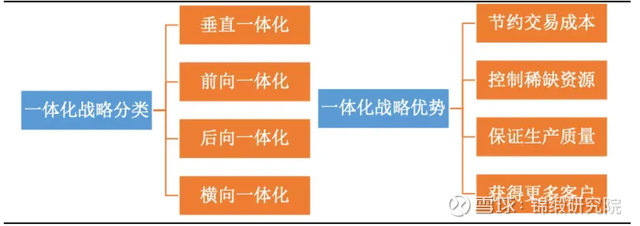

The integration theory was first put forward by American economist Paul Krugman in 1981, and its emphasis is on the internalization of all aspects of production and operation of multinational corporations.

That is to say, from the production of raw materials and parts to the final product pricing, etc. are all incorporated into the enterprise, and then by dispersing all aspects of production in different countries and regions around the world, using the combination of comparative advantages and convenient means of communication and transportation, to achieve each production. The purpose of lower cost of link intermediate products.

Vertical integration has the ability to improve the organization of internal control and coordination, and save the economy of transaction costs. In many cases, through vertical integration, the development of technology can be accelerated, the core competitiveness of enterprises can be improved, and the purpose of defense is to prevent them from being excluded by other enterprises. In essence, vertical integration is not only a way to improve economic efficiency, but also a means to cultivate one’s own competitiveness, enhance the ability to resist risks, and carry out active strategic planning.

Figure: Classification and advantages of integrated strategies, source: Industrial Securities

We might as well look at two examples of new energy vehicles, perhaps to better understand the importance of “vertical integration”.

The first example is the national car benchmark BYD. In the automotive “chip shortage” in 2021, why did BYD’s sales not be affected by the lack of cores, but instead hit a new high. The reason is that BYD is the company with the highest rate of autonomy – battery, motor, electric drive, electric control, battery BMS system, and even some automotive chips are designed and produced by itself, and even car seats are also produced by joint ventures. .

Figure: BYD’s new energy industry chain layout, source: Orient Securities

The second example is the smart car benchmark Tesla. Tesla not only conducts self-research in the field of intelligent driving, but also builds 4680 batteries in person, and extends its tentacles to battery recycling. It even plans to make a fuss at the most upstream of the industry chain: optimizing the mining and refining process of minerals. In Musk’s eyes, only in this way can we better control the cost of the entire vehicle and have more full competitiveness.

In a nutshell, BYD and Tesla, which are developing rapidly today, are ostensibly due to policy-driven and marketing efforts, but in fact they are both models of vertical integration. This success is inseparable from their layout of many core technologies such as batteries and electronic controls, as well as accurate research and judgment on industry trends.

However, CATL, which is also an industry leader, handed over a report card in the first quarter of this year that “revenue doubled but net profit fell by more than 20%”. The answer is also well known, the sharp rise in upstream raw material costs is the main reason. In the face of the extreme situation where the price of lithium carbonate has skyrocketed to 500,000/ton, even “Ning Wang” is powerless.

Having said that, the Ningde era is actually a supporter of vertical integration. After all, Ningde’s industrial chain has been deployed in the fields of cathode precursors and lithium battery equipment, but the layout of the upstream is insufficient, and it will eventually affect the whole body. Other second-tier power battery companies that are weaker in vertical integration are even more mourning. For example, Guoxuan Hi-Tech’s revenue in the first half of 2022 hit a record high, but its net profit hit a three-year low.

Figure: Guoxuan Hi-Tech was forced to fall into the dilemma of “increasing revenue without increasing profits”, source: the company’s 2022 semi-annual report

Focusing on the photovoltaic track, under the general trend of vertical integration in the future, the core of competition among enterprises will change from focusing on profits in the past to the layout and control of the value of the entire industry chain.

The payment ability of terminal power station customers is certain, which means that the entire profit of the entire photovoltaic industry chain is fixed. In the past, this part of the profit was divided by silicon material, silicon wafer, cell, and module companies. This forces the upstream and downstream of the industry chain to become the objects of mutual competition. Everyone wants to maximize the benefits, but the local excessive competition is not necessarily the overall optimal solution, which aggravates the periodic fluctuation of the photovoltaic industry chain to a certain extent.

After vertical integration, the profits of silicon materials, silicon wafers, and cells will all be reflected in the final module profits, which will make the company’s performance more stable and allow different industrial divisions of labor in each link of the industry chain. Doing so can not only enhance synergy, but also reduce disorderly competition, which will be more conducive to the development of the photovoltaic industry.

2) The story of cost reduction is unfinished to be continued

On August 24 this year, the General Office of the Ministry of Industry and Information Technology, the General Office of the State Administration for Market Regulation and the General Department of the National Energy Administration issued the “Notice of the Three Departments on Promoting the Coordinated Development of the PV Industry Chain Supply Chain”. It is proposed that the three departments should effectively use the domestic photovoltaic market, guide the upstream and downstream enterprises in the industry chain to communicate in depth, and promote the improvement of industrial quality, cost reduction and efficiency increase.

The policy guidance direction and the industry law have achieved an accurate fit. In the 2.0 era mentioned above, we clearly proposed that vertical integration will replace technological progress and become a relatively more important factor.

Further systematic attribution, it is not difficult to find that the future competition of the photovoltaic industry chain will be upgraded from the profit competition of a single business to the comprehensive competition of the strategic layout of the enterprise. The test is the overall competitiveness of the enterprise in the core field and the strategic aspect. decision-making power.

All changes are inseparable from the original, all walks of life are the survival of the fittest. The trend of vertical integration is not only the result of industrial upgrading, but also the essential law of the market. In fact, the final industrial pattern has already begun to emerge. In the future, integrated leaders such as Tongwei and LONGi will continue to write the next chapter.

$LONGi Green Energy(SH601012)$ $Tongwei Co., Ltd.(SH600438)$ $YiJing Optoelectronics(SH600537)$ #PV#

@Today’s topic @Prophet Church @houbinghoping @oriental sunrise @arts

There are 21 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/6217310837/232470439

This site is for inclusion only, and the copyright belongs to the original author.