In the past two days, I took the time to read all the announcements issued by Watson Zhongbao, and summarized and extracted some key points of the company’s changes, from the company’s performance in the first half of the year to the company’s project progress, to the company’s convertible bond issuance, and the company’s ongoing I made a brief summary of what I have done and what I will do in the future. The content is only for personal sharing, and does not make investment decision suggestions!

1. The company’s performance is developing steadily

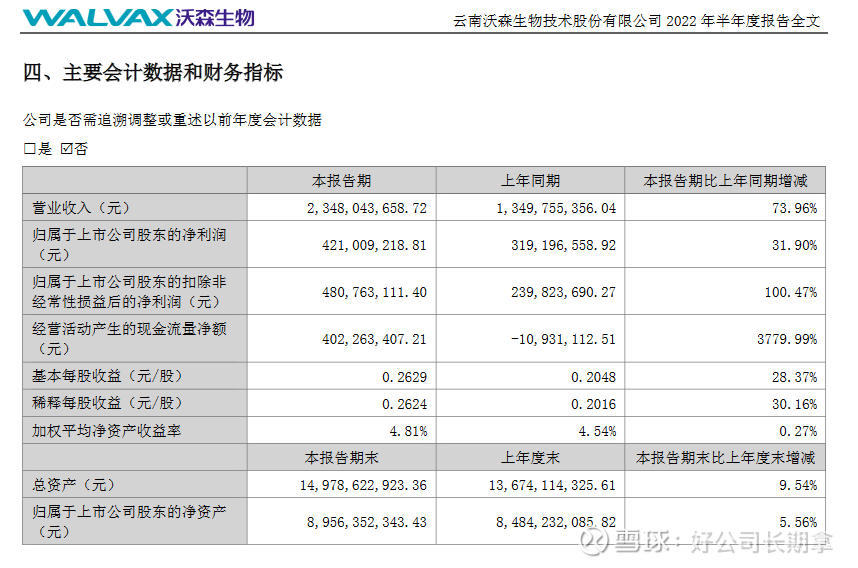

In the first half of the year, the operating income was 2.348 billion yuan, an increase of 73.96% year-on-year and a month-on-month increase of 157.99%. Among them, 3.7315 million doses of 13-valent pneumonia vaccine were issued in batches, a year-on-year increase of 39.68%. Vaccines accounted for 85.62% of revenue. Bivalent HPV obtained a registration certificate in March this year, and 884,000 doses of bivalent HPV were approved in the first half of the year. The launch of bivalent HPV is a very important milestone for Watson, which is also the second half of the performance. A point to watch.

In the first half of the profit, the net profit was 421 million, an increase of 31.9% year-on-year, and an increase of about 890% month-on-month; non-net profit was 481 million, a year-on-year increase of 100% and a month-on-month increase of 293%, mainly due to the company’s holdings in Jiahe Biotechnology. – More than 88 million.

The company’s R&D investment in new products and new projects continued to increase, mainly in the clinical trials of the new crown mRAN vaccine at home and abroad. In the first half of the year, the R&D investment was 478 million, an increase of 84.1% year-on-year, and the R&D expenditure was 400 million, mainly in the new crown. Revenue increased by 3.16% year-on-year. The new crown is mainly due to higher expenses in the past two years, so it has a greater impact on single-period profits.

The total amount of the company’s construction in progress is 1.489 billion, of which the investment in the construction in progress in the first half of the year is 375 million, and the single-phase conversion of fixed assets of the construction in progress is 389 million. The company is making every effort to promote the industrialization of Jiangsu, Yuxi, Sichuan and Beijing. In the future, a rapid transformation of vaccines from research and development to industrialization will be realized.

The company’s fixed assets were 1.435 billion, an increase of about 34.06% compared with the end of last year, and then the intangible assets were 1.11 billion, an increase of about 155% compared with the end of last year. While the company accelerated its investment in product research and development and industrialization, the company’s cash flow on the account Abundant, monetary capital is 3.75 billion, the sales cash flow rate has reached 74.09%, and the net cash flow from operating activities is 402 million. The current cash flow is relatively good.

Overall, Watson’s performance is growing steadily. Whether it is revenue, profit, fixed assets, total assets, construction in progress and the company’s book cash, they have maintained a good growth rate, and all of these have maintained a good growth rate. Only the 13-valent pneumonia vaccine is being promoted, and the bivalent has not contributed much. The new crown vaccine is still in the stage of dragging its expenses. If you compare the new crown provision of Kangtai Bio, then Watson’s performance is very good. The bivalent HPV will be released in half a year, and the new crown mRAN vaccine will be approved for marketing in Indonesia or the fourth injection in China, and the performance will have a qualitative leap.

2. The company’s product pipeline, R&D strength and production requirements are all leading in the industry

Watson has come along with more and more vaccine products, and the company has become more and more competitive at home and abroad. For more than 20 years, it has a very rich product pipeline, including 12 products under development, and the company and its subsidiaries still have a nine-valent HPV vaccine. , ACYW135 group meningococcal polysaccharide conjugate vaccine, 4-valent influenza virus split vaccine, recombinant new coronavirus vaccine (CHO cells), recombinant new coronavirus variant vaccine (CHO cells), DTaP-Hib quadruple vaccine and the company and partners The joint research and development of new crown mRNA vaccine, recombinant new coronavirus vaccine (chimpanzee adenovirus vector), herpes zoster mRNA vaccine, respiratory syncytial virus mRNA vaccine, influenza virus mRNA vaccine and new crown variant mRNA vaccine and other vaccine products are in clinical trials Different stages of research or preclinical research. There are 8 listed products (12 product specifications), and it is in an industry-leading position in the field of biotech medicines represented by new vaccines.

The company is the first manufacturer in China and the second manufacturer in the world to independently develop and successfully market 13-valent pneumonia conjugate vaccine, and is currently the only manufacturer in the world that has both 13-valent pneumonia conjugate vaccine and HPV vaccine. The company has built a domestic leading vaccine research and development and industrialization technology platform, gathered a large number of professional technical and management talents combining Chinese and Western, and obtained a group of national “863 Plan” and “Major New Drug Creation” scientific and technological major special projects. It has established close cooperative relations with many scientific research institutes, universities (Tsinghua University) and internationally renowned institutions such as WHO and Gates Foundation.

It can be seen from the announcement “Feasibility Study Report of Yuxi Watson’s Integration of Industrialization and Industrialization Project” that the company is also a domestic leading enterprise in vaccine production and inspection equipment. Yuxi Watson has 6 GMP certified production lines and is building A world-class high-end vaccine production base has become a large-scale supplier for the procurement of international vaccine organizations. This is something the company is doing and has been planning for a long time.

And the company has been paying attention to digital transformation in the past two years. Watson signed a cooperation with Honeywell , an international enterprise, to realize the transformation of vaccine digital production. This is in line with the national planning goals and in line with the standards of international vaccine companies, and from the company’s perspective, it can reduce costs and increase efficiency in the long run. It is expected that through the integration of industrialization and industrialization in about five years, Yuxi Watson will build the country’s leading advanced intelligent manufacturing demonstration workshop and operation management model, and create a new model of low-risk, high-quality, high-efficiency, and low-cost human vaccine intelligent manufacturing.

It is expected that the production efficiency will be increased by more than 20%, the operating cost will be reduced by more than 20%, the product upgrade cycle will be shortened by more than 28%, the energy consumption per unit output value will be reduced by more than 10%, the automatic generation rate of production plans under complex working conditions is not less than 90%, and the efficiency of enterprise resource allocation It has been increased by more than 30%, and the precise service capability has been increased by more than 50%. Therefore, whether it is the new crown vaccine factory or the improvement of other vaccine factories, the production environment is advanced in China, and the construction period is about two years. Therefore, if you want to become an international vaccine enterprise, none of these steps can be taken. few.

3. Issuance of convertible bonds, do a good job of vaccines in a down-to-earth manner, and have forward-looking future plans

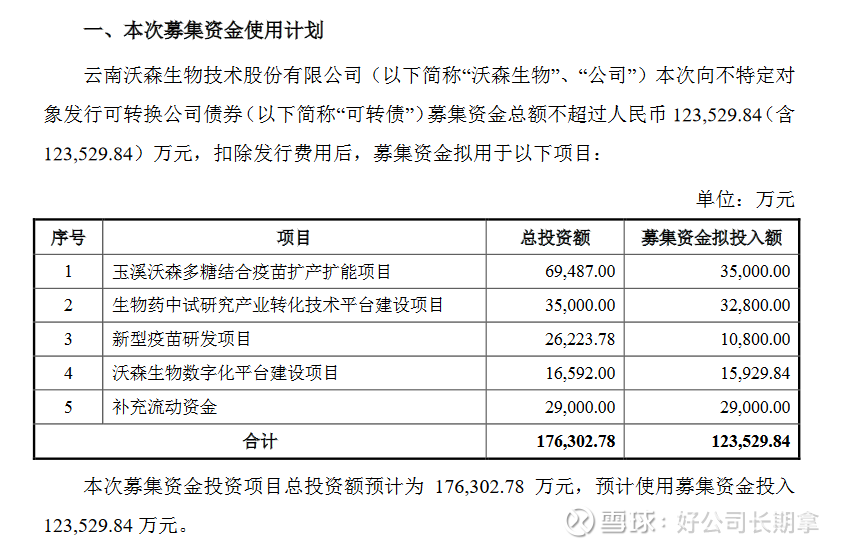

At the same time, Watson Bio also released a convertible bond issuance plan. You can read the “Feasibility Analysis Report on the Use of Funds Raised by Issuing Convertible Corporate Bonds to Unspecified Objects” . The funds raised this time are mainly used for Yuxi Watson Polysaccharide . Combined with the vaccine production and capacity expansion project, the biopharmaceutical pilot research industry transformation technology platform construction project, the new vaccine research and development project, the Watson Bio digital platform construction project and supplementary working capital. It is mainly the company’s layout in the vaccine industry. It is the future development trend to attach importance to informatization construction and the development of new vaccines, multivalent vaccines and combined vaccines. It emphasizes enhancing industrial innovation capabilities and improving the level of international competition.

(1) Yuxi Watson Polysaccharide Conjugate Vaccine Production and Capacity Expansion Project. Construction of ACYW135 group meningococcal polysaccharide conjugate vaccine (hereinafter referred to as “tetravalent meningococcal conjugate vaccine”) stock solution production workshop, CRM197 carrier protein workshop and preparation sub-packaging workshop. After the completion of the project, it will be able to produce 30 million doses/year of tetravalent meningitis conjugate vaccine stock solution, 6000g/year of CRM197 carrier protein, and a preparation workshop with a production capacity of 100 million doses/year.

(2) The construction project of the industrial transformation technology platform for biopharmaceutical pilot research. In order to strengthen the pilot-scale research and industrial transformation capabilities of the four technology platforms of polysaccharide/polysaccharide-protein conjugate vaccines, recombinant protein vaccines and drugs, nucleic acid vaccines and drugs, and adenovirus vector vaccines that the company has built, relying on the recently built and put into use Watson Biotechnology The innovation center will be equipped with basic facilities, and implement the construction project of the industrial transformation technology platform for biopharmaceutical pilot research.

(3) New vaccine research and development projects. A clinical trial study was conducted on the ACYW135 meningococcal polysaccharide conjugate vaccine (“quadric meningococcal conjugate vaccine”) and the adsorbed acellular DTP/Haemophilus influenzae type b combined vaccine.

(4) Watson Bio-Digital Platform Construction Project. In order to integrate the internal resources of the enterprise, improve the level of business operation and management, and help the company to achieve digitalization and intelligence, it is planned to pass the Yunnan Watson R&D and management digital project, Beijing Watson digital project, Yuxi Watson production quality digital project and Guangzhou Watson marketing digital project Project, build a digital platform for R&D, production, sales, and enterprise management.

(5) Supplementary working capital. In recent years, the company’s business has continued to develop rapidly. With the rapid expansion of business scale, it is difficult for the company to meet the demand for funds for sustained and rapid business expansion only by relying on internal operation accumulation and indirect financing. This time, the company plans to use the 290 million yuan of the raised funds to supplement working capital, which is in line with the development status of the company’s industry and the company’s business development needs.

In fact, some gossip about convertible bonds was known in advance, but the construction content was wrong. Some said that the layout of 24-valent, some said that the blue magpie variant was deployed, and some said that the layout of 9-valent HPV, the results were all. No, it’s a little embarrassing! There are also friends who have complained about the company because of this. If convertible bonds are replaced by popular tracks, such as lithium batteries, new energy vehicles, and photovoltaics, the issuance will definitely rise sharply, and the pharmaceutical industry has adjusted a lot in the past two years. I think It is a periodical low valuation, and it belongs to the bottom area. They are all waiting for a fuse to ignite the track. Just like the chip track, the mood will rise quickly.

Fourth, the vaccine industry has broad market prospects and high technical thresholds

Vaccination is the most economical and effective means of preventing and controlling infectious diseases. The social cost of effective disease prevention is far lower than that of disease treatment, and the development and application of vaccines is considered to be one of the investment methods with extremely high returns. According to the data released by the US CDC in December 2021, considering the treatment costs and productivity decline caused by the disease, the annual immunization of 4 million newborns in the United States can directly save nearly 13.5 billion US dollars in net costs and save 70 billion US dollars in total social costs. If the cost/benefit ratio (CBR) is used to accurately measure the economic value brought by vaccines, the CBR of the vaccine industry can reach 1:16~44, that is, if you invest 1 yuan, you can get 16~44 yuan of benefits.

Although my country’s vaccine market has great potential, my country’s vaccine industry still has problems such as low concentration, high product homogeneity, and weak vaccine innovation capability. According to the 2021 data from the China Inspection and Quarantine Institute, there are currently more than 40 domestic vaccine manufacturers in China, only 5 companies that have issued batches of 4 or more vaccine products, accounting for only 16%, and only 1 of the 19 vaccine companies. Vaccine varieties, accounting for 59%. The implementation of the “Vaccine Administration Law” will further accelerate the overall progress of the vaccine industry in a better and safer direction. In addition, although my country’s vaccine industry has accumulated many years of technology, most companies are still at the bottom of the technological innovation pyramid, mainly relying on the improvement of traditional vaccines. Such vaccines (such as hepatitis B, rabies, pertussis and Japanese encephalitis, etc.) have serious homogenization. and fierce competition. New vaccines such as polyvalent multivalent vaccines, polysaccharide conjugate vaccines, and HPV vaccines have been approved for marketing abroad for many years, but there are still many varieties that have not been localized in my country.

Fifth, talk about other

In terms of company cooperation, Beijing Weida Biotechnology Co., Ltd. actually incurred a cost of 110 million yuan, indicating that the chimpanzee vaccine cooperation with Professor Zhang and Tsinghua University should have made great progress. At the same time, the company has also made a lot of moves in the mRNA vaccine industrialization cooperation recently. We can look forward to the launch of the mRNA new crown vaccine in Indonesia!

In terms of public welfare, it is mainly to pave the way for HPV. While paying attention to its own development, the company still actively participates in social public welfare undertakings and contributes its own strength to social development. The company signed two Donation Agreements with the China Women’s Development Foundation, and will donate a total of 11.5 million yuan in cash to the China Women’s Development Foundation to support/establish the “‘Rose Action’ Adolescent Health Education Public Welfare Project” and “Heart-to-Heart”. Angels in White Charity Project”. Subsidiaries donate no more than 700,000 doses of 23-valent pneumonia vaccine nationwide through third-party organizations (such as the Red Cross, charitable fund organizations, etc.). So far, Yuxi Watson has donated about 550,000 doses of 23-valent pneumonia vaccine.

In terms of shareholder returns, this cake is okay, and there is hope. The company has issued the “Shareholder Return Plan for the Next Three Years (2022-2024)” . You can see that cash dividends are preferred, and the company’s cumulative distribution of profits in cash is not less than 10% of the distributable profits realized in the year, or The accumulated profits distributed in cash in the last three years shall not be less than 30% of the average annual distributable profits realized in the last three years. If the company’s net profit maintains a sustained and rapid growth in the next three years, the company can increase the proportion of cash dividends, or implement stock dividend distribution under the conditions of issuing stock dividends to increase returns to shareholders.

In the future performance expectations, mainly the 13-valent pneumonia vaccine goes overseas and the batch of 2-valent HPV is released in large quantities. In the medium and long term, there is also the approval of the mRNA new crown vaccine and the supply of 2-valent HPV to WHO. Watson is exporting these things internationally. The annual revenue growth rate is also obvious. The company’s products have been exported to 18 countries in total, and the follow-up meningococcal series vaccines will also be exported. Moreover, the company is the first company to lay out the mRNA track in China. Now there are many companies on the track investing heavily in the layout. It is foreseeable that the importance of the mRNA platform has a relatively large expectation difference, whether it is an overseas Indonesian mRNA new crown vaccine or a domestic new crown vaccine. Approval will bring good performance to Watson, and the market obviously did not give Watson this valuation.

In terms of the company’s share price, the biopharmaceutical industry sector as a whole is in a stage of low valuation and high cost performance. Vaccines and biomedicine have recently raised many ETF funds, and biomedicine belongs to the national key support track. Although there is a certain gap with the advanced pharmaceutical companies in the United States, our market is large enough and we are catching up! At the same time, Watson’s R&D, production, testing and other requirements are strictly implemented in accordance with international standards. In conjunction with the WHO and the Gates Foundation, they are highly deploying internationalization and moving forward steadily as a whole. It is worth looking forward to!

Okay! The alchemy of the content of the mid-term report is here. Thank you for your patience to read it. I hope it will help you understand Watson Bio. As for whether Watson Bio is real gold, you need to use your eyes to identify it.

If you want to know more about Watson, you can take a look at my other article: “Watson Biological Alchemy, a Lone Walker in the Vaccine Industry” is written in more detail! Like a friend remember to like! Thanks for the support!

$ Watson Bio (SZ300142)$ $ Shanghai Index (SH000001)$ $ ChiNext Index (SZ399006)$

@Today’s topic @Investment alchemy season @snowball interview #Investment alchemy season in mid-2022# #Investment alchemy season# #shareholder’s daily#

This topic has 91 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3537625901/227970129

This site is for inclusion only, and the copyright belongs to the original author.