The reform of medical insurance payment is undoubtedly the most variable factor for the medical industry in recent years. Especially in the past year or so after the sharp decline, market participants whose vital interests have been damaged often scatter most of their grievances on the issue of medical insurance payment, almost “the responsibility of the medical insurance bureau”, and even hear words such as “” The medical insurance cost control has completely subverted the logic of China’s medical industry ” conclusion.

This sounds easy to arouse a sense of recognition. After all, the price of innovative drugs has been really lowered, and in recent years, more than one industry has had its logic subverted or even directly destroyed because it does not conform to the direction of macro policies. In addition, the medical industry is widely considered to have some kind of “public welfare attribute”. However, these are all indirect associations. We still have to ask the most direct question: What logic does the medical insurance control cost subvert the medical industry ?

First, the conclusion is that the author clearly opposes the view that medical insurance control fees subvert the logic of the medical industry, and believes that the impact of medical insurance reform on the industry can be said to be planned ahead of time, unchanged from the beginning, as expected, and as it should be.

Before doing a detailed analysis, it is stated that this article will follow the following two default methodologies, and will not discuss their rationality: 1) The official data released by the relevant departments will be directly accepted without any verification; 2) The high-level The quantitative goals proposed in the level planning documents, in the absence of major macro-environmental changes, have been fully demonstrated rationality by default before formulating the plan, that is, they will be achieved with a high probability.

1. Plan ahead: Medicare reform is not because of no money now, but to save money for the future

“Medical insurance is out of money” seems to have become a self-evident consensus in the industry. After all, the logic of “because there is no money, so we have to save money” is very coherent, and factors such as epidemic prevention, the economic environment and financial constraints are also visible to the naked eye. This statement sounds reasonable.

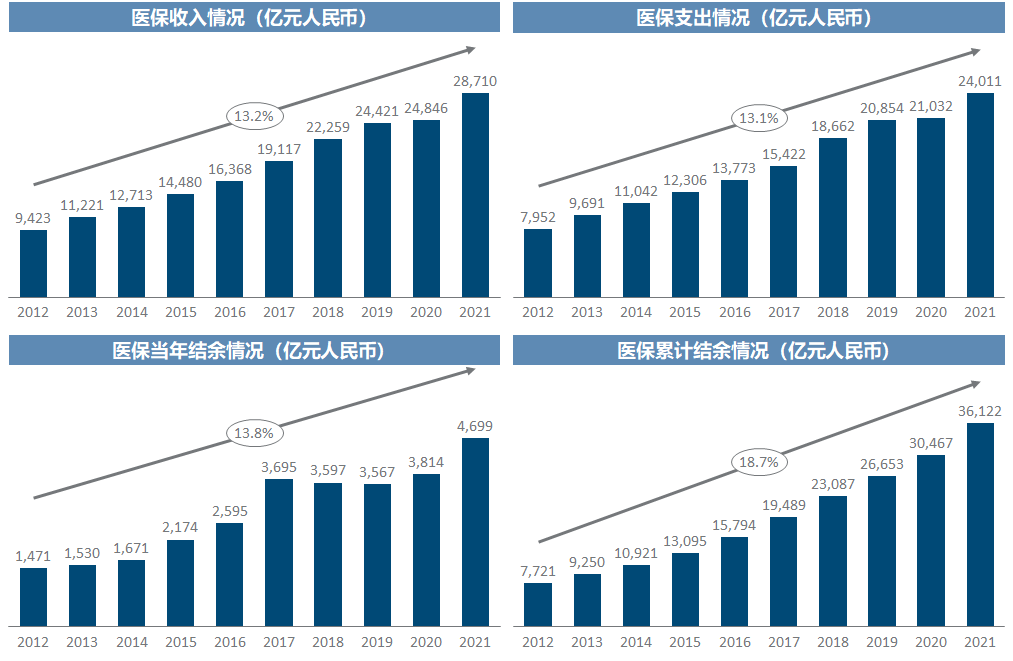

However, according to the medical insurance revenue and expenditure situation disclosed by the Medical Insurance Bureau, China’s medical insurance funds have not reached the bottom, and the health of the funds has continued to improve . In the past ten years, the cumulative balance has doubled by five times, especially after the 2017 document No. 55 and the establishment of the National Medical Insurance Bureau in 2018, the annual balance has jumped from one to two hundred billion to around 400 billion. Under the special circumstances of 2020/2021, although medical insurance payments fluctuated and epidemic prevention-related expenses increased, because the daily expenses of hospitals also decreased, the overall balance was still thickening, and even in 2021, whether it was the current year or the cumulative balance All hit new highs .

It should be noted that in addition to social financing, government financial subsidies are also an important source of medical insurance revenue, and the annual balance deducting subsidies is indeed a deficit (in 2020, the government health expenditure on medical security is 884.5 billion yuan). But this is two different things from “medical insurance” having no money, because every year the government finances have a budget for health expenditures. Unless there is evidence that the financial subsidies to medical insurance will be greatly reduced in the future, the medical insurance income will justify this part of the subsidy as a fixed amount. origin of.

The question is, since it seems that the landlord’s family has plenty of surplus food, why are they so stingy? Of course, there is no contradiction in this. A logic that is easy to understand for Chinese people with an incredible savings rate is that the driving force for saving money is either the lack of money now or the fear of lack of money in the future. The core starting point of China’s medical insurance fee control Just to make room for the difficult times that are coming .

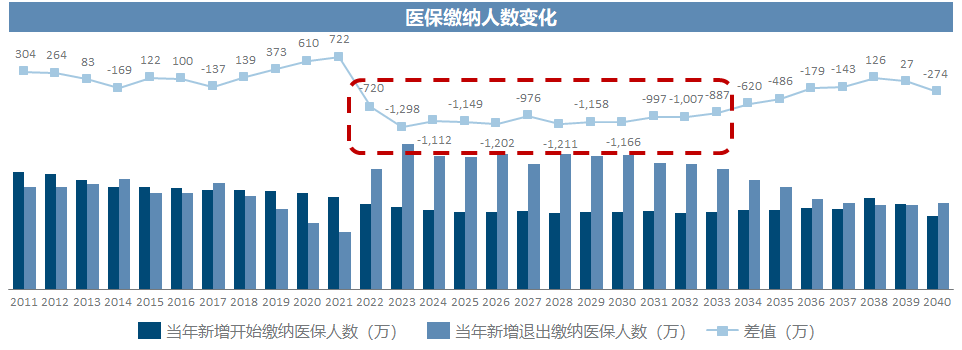

We can easily deduce the changes in medical insurance income and expenditure pressure from the number of births over the years. Assuming that the age of 22 begins to enter the scope of medical insurance payment, and the age of 60 leaves the scope of medical insurance payment, the difference between the two groups of people each year reflects the payment of medical insurance. The net change in the number of people (here is highly simplified, neither the effect of increasing medical expenses for people over 60 years old, nor the effect of reducing medical expenses caused by the death of elderly people). It can be clearly seen that the birth tide in the 1960s has begun to retire one after another, making 2022 exactly the beginning of the inversion of new retirements and new recruits in the next ten years or so. This will also be the decade when medical insurance faces the greatest pressure. After that, the pressure will decrease.

This explains why the drug review reform will start in 2015 and why the medical insurance bureau will be established in 2018. There must be a more comprehensive and complex picture in front of the decision-making level, but the principle is basically similar, in 2022 ” The five or six years before the start of “Upside Down” is the last window of time to save money for the difficult period of the next ten years. None of this information is dynamic, but a situation that was determined and predictable ten years ago. The decision-making level can see it, and you and I can basically see it. The information asymmetry is not obvious, that is, the so-called “” ” Bright cards “, both industry practitioners and investors should be able to make predictions in advance .

Here I would like to add a private message: the level of elite decision makers should never be underestimated. If you think that the decision is imperfect or unreasonable, it is indeed possible, because there may be a lot of off-site factors in the game process, and the balance formed after the joint action may not be the optimal result; but if you think the decision is stupid or even very It’s nonsense, it’s best not to question their IQ, and the priority must be to reflect on what you haven’t seen or understood. The more stupid it looks, the more essential information you’re missing.

2. It has not changed since the beginning: medical insurance cost control has not squeezed the scale of the industry

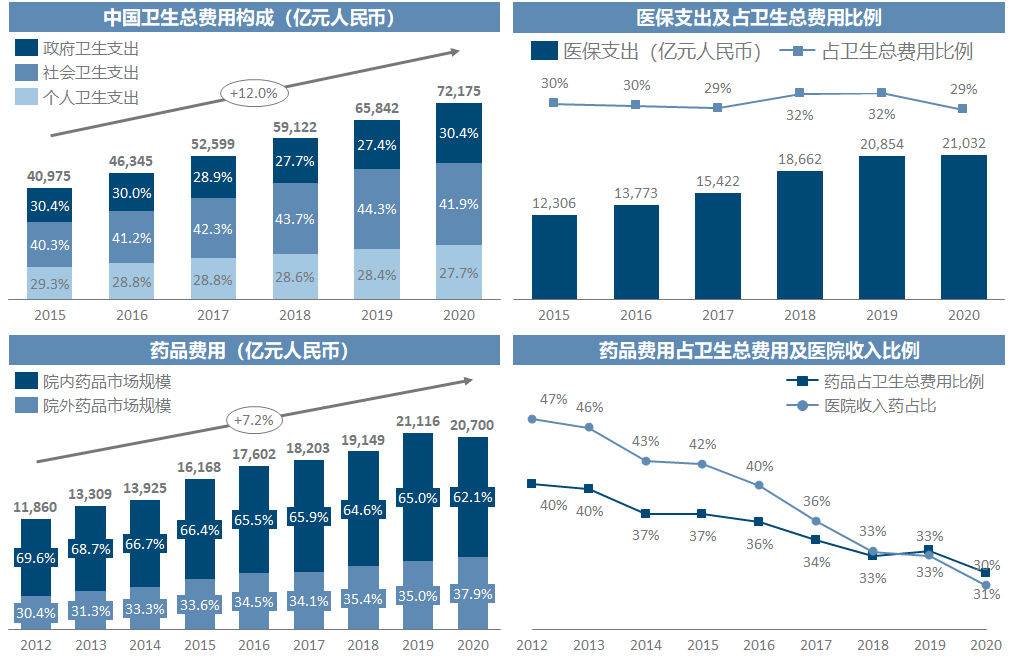

Whether medical insurance has money or not is just a foundation, the key is to see whether it continues to pay for medical and health activities. In addition to the continuous growth of the above-mentioned medical insurance expenditures, its proportion in the total health expenditure has basically remained at about 30%; at the same time, another perspective is that in the composition of the total health expenditure, the proportion of personal health expenditures has dropped significantly , from 30-40% in the early years to 27.7% in 2020, and it is clearly required in the “14th Five-Year Plan” to continue to drop below 27%, which means that medical insurance will be included in China’s medical and health payment system. continue to play a more important role .

If we focus specifically on the drug market, centralized procurement and medical insurance negotiations have been carried out for three or four years, and the size of the drug market has not shrunk due to cost control, but is still growing . It is far from the statement, and it is completely irrelevant to those industry scenes that are really “subverted”.

At the same time, we must also see that the payment structure is indeed undergoing adjustment. The growth rate of drugs is not as high as the total health expenditure, so the proportion of drugs has dropped significantly, and the growth rate of drugs in the hospital is not as good as that of the out-of-hospital, so the proportion of drugs in the hospital is also declining. This is the meaning of the medical insurance reform.

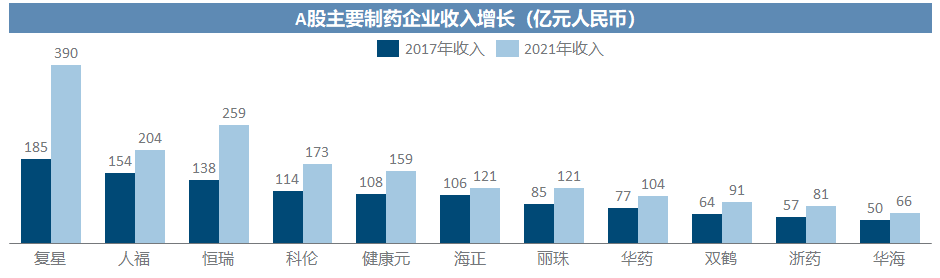

In addition to the overall macro data, it is not difficult to see from the income of even the so-called “traditional” pharmaceutical companies that since the implementation of the medical insurance reform and the cost control and price reduction driven by the implementation, there has not been a large-scale income decline . It’s a matter of how fast it rises.

Since the payment amount of medical insurance and the market size of medicines have not decreased, but after all, fee control and price reduction have really happened, there are only two explanations: one is the so-called ” price-for-volume “, that is, sales remain unchanged or even continue. Growth, but the decline in unit price means that pharmaceutical companies need to produce more volume to meet more demand (in response to inclusiveness), which will lead to increased costs and may dilute profits; ” Bird “, that is, the transfer of medical insurance funds according to the clinical value and the degree of innovation from low to high, including but not limited to from generic drugs to innovative drugs.

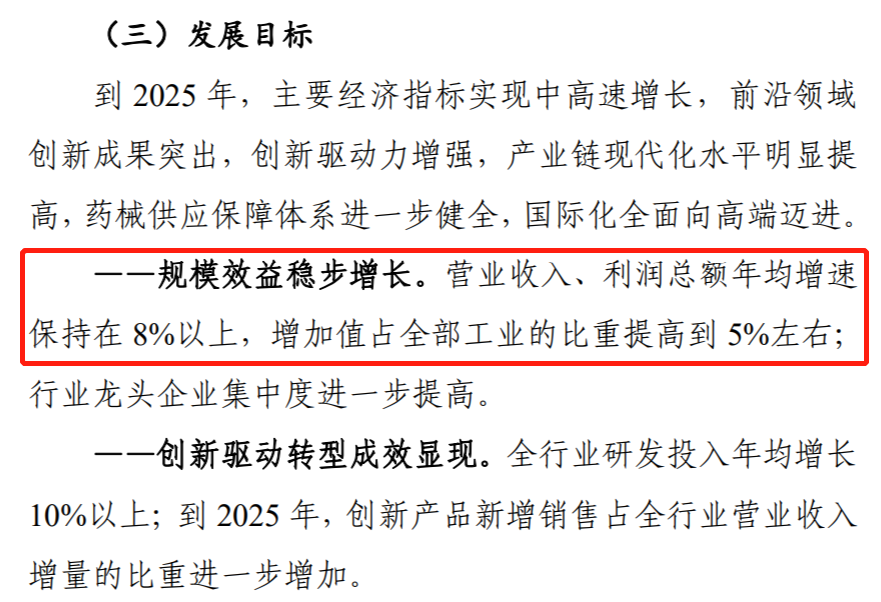

So even if the revenue does not decline, is it possible that there will be a serious shrinking of profits due to the price drop and the increase in volume? Please always keep in mind that the Medical Insurance Bureau is also the issuing unit of the “14th Five-Year Plan for the Pharmaceutical Industry”. It is written in black and white that both revenue and profit must maintain an average annual growth rate of 8%. This profit indicator is first proposed in the five-year plan. , which is still based on the premise of an average annual growth rate of 10%+ R&D investment. From the most realistic point of view, if any figure written in an important plan cannot be completed after five years, the relevant departments and the person in charge will be held accountable. Conversely, it means that these can be written down before the document is published. The quantitative indicators on paper have been carefully demonstrated and approved by all departments involved.

For details of the interpretation of the “14th Five-Year Plan”, please refer to: Yesterday, Today and Tomorrow——From the “12th Five-Year Plan” to the “14th Five-Year Plan” “Pharmaceutical Industry Development Plan” sentence reading

3. As expected: the relationship between supply and demand determines that a single payer will inevitably gain high bargaining power

There are always people who attribute the “violent” cost control of medical insurance to the so-called legacy of the planned economy, or even to be accused of being a backward system, but even according to the most classic Western economic theories, prices are closely related to supply and demand, while supply and demand in the Chinese pharmaceutical market In the relationship, the purchase decision on behalf of the demander is mainly medical insurance, which is a near-single payer. In a one-to-many situation, the supply is often excessive, which will inevitably lead to the demander having a great advantage in the price decision process. Frankly speaking, in the case that medical insurance accounts for a considerable proportion of the medical payment amount, the unrestricted bargaining of medical insurance is the most consistent with the principle of market economy .

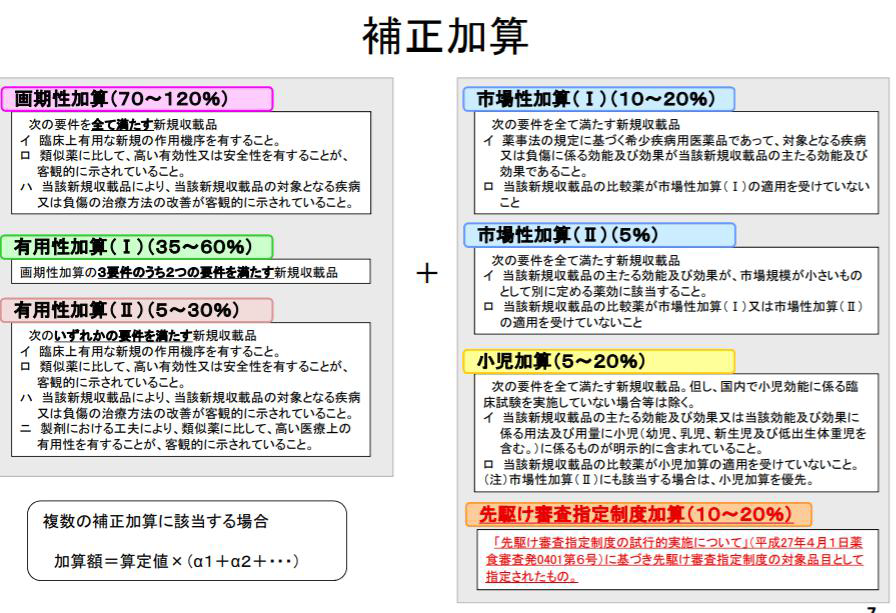

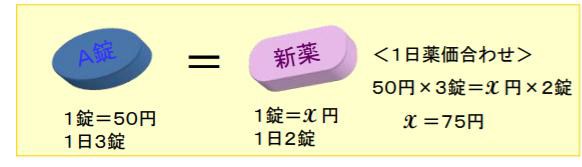

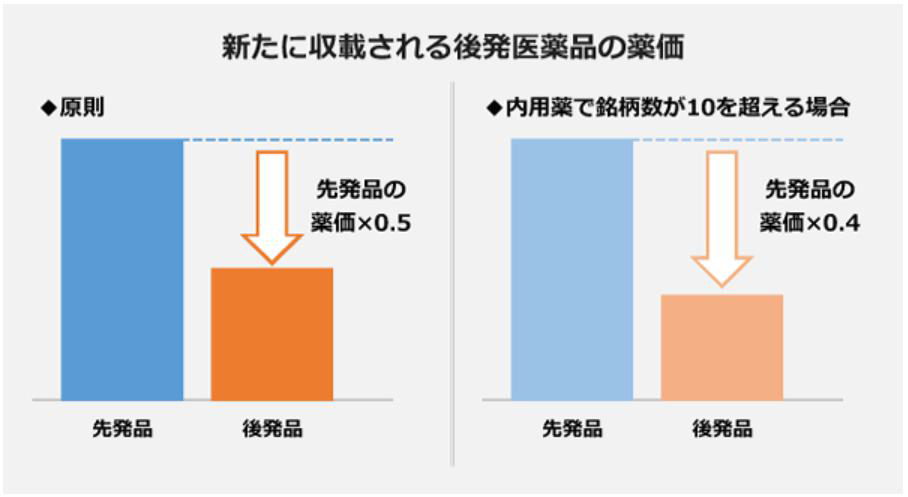

If we are always skeptical of our own system, let’s not look at Japan next door. Its medical insurance also adopts a centralized and unified payment led by the government, so the status of its pharmaceutical industry is also quite informative. For example, the first-in-class medicine (FIC) adopts cost-based pricing, and adds a certain percentage of sales, R&D, finance and other expenses and taxes to the manufacturing cost as the payment price for medical insurance, and this additional percentage is completely adjusted and determined by the Ministry of Health and Welfare; For Me-too products, the price of the original drug with the same efficacy shall be referred to, and the equivalent price shall be converted according to the efficacy; for generic drugs, if there are less than 10 brands approved to be marketed after the patent expires, the price of the original drug shall be 50%. % pricing, if more than 10, 40% of the original drug pricing. Does it sound shivering, more rigid and inflexible than the pricing set by the Chinese Medical Insurance Bureau? No space is right, this is the pricing method that best fits the rational person assumption as a single payer .

For details of the content of this section, please refer to Xinpu Investment Research Report Xinpu Investment Research Report

4. This should be the case: the medical insurance reform has actually promoted the benign adjustment of the industrial structure

Although the KPI of the Medical Insurance Bureau does not require any responsibility for the healthy development of China’s medical industry, the Medical Insurance Bureau does not exist in isolation. balance. In the process of the formation and adjustment of the balance, the means of controlling expenses by the Medical Insurance Bureau has precisely promoted the clearing of low-value forces in the pharmaceutical industry, and has in fact continued to help the benign adjustment of the industrial structure (although not necessarily entirely their subjective opinion). will).

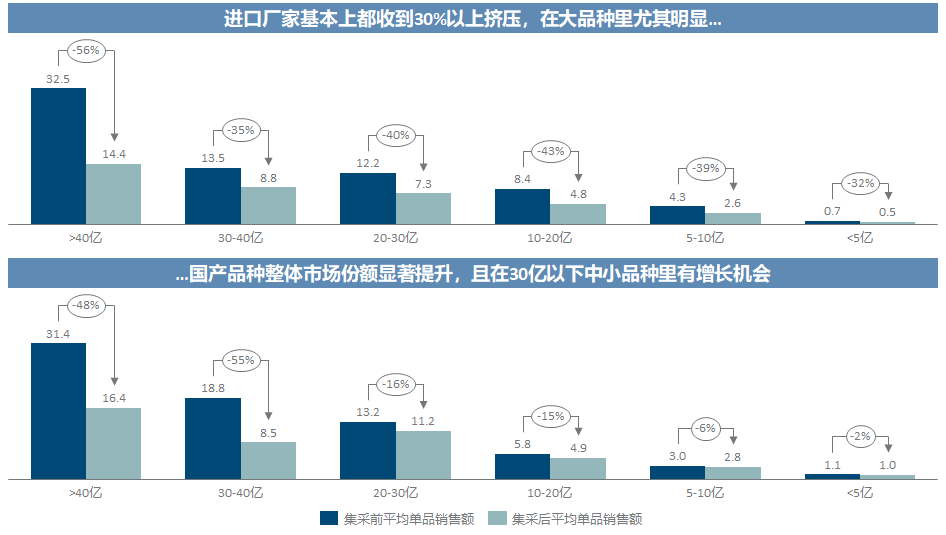

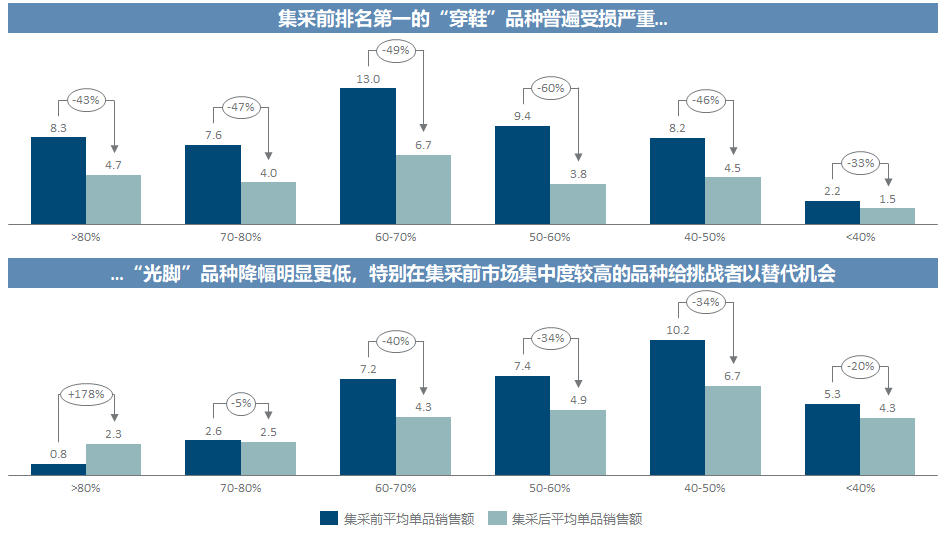

For example, for the centralized procurement of generic drugs (for details, please refer to ” The Real Impact of Centralized Drug Procurement on Sales “), while squeezing the total amount as a whole, there are also obvious priorities , such as varieties with low market concentration. , imported varieties, and varieties that are obviously suspected of abuse, etc., have more stringent price reduction measures, and in fact have brought about a more obvious sales shrinkage.

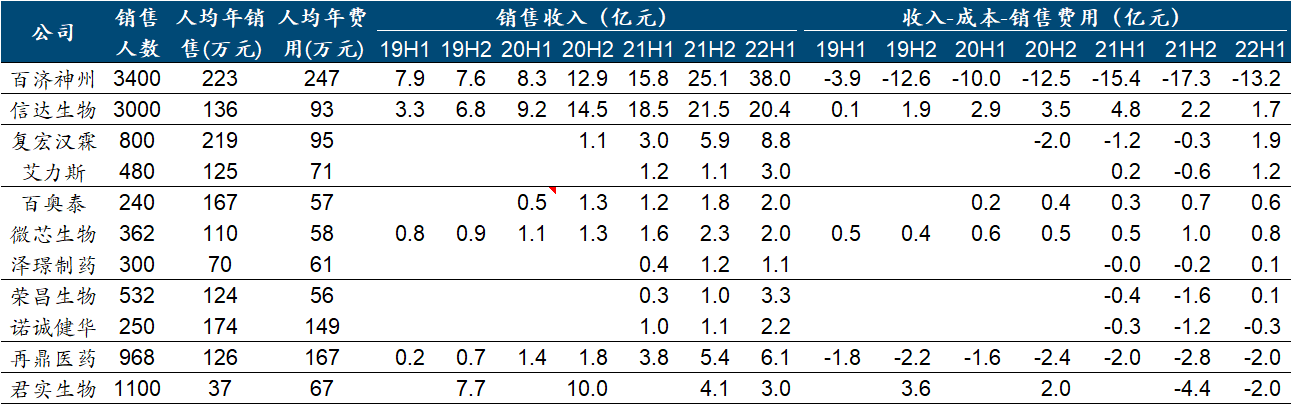

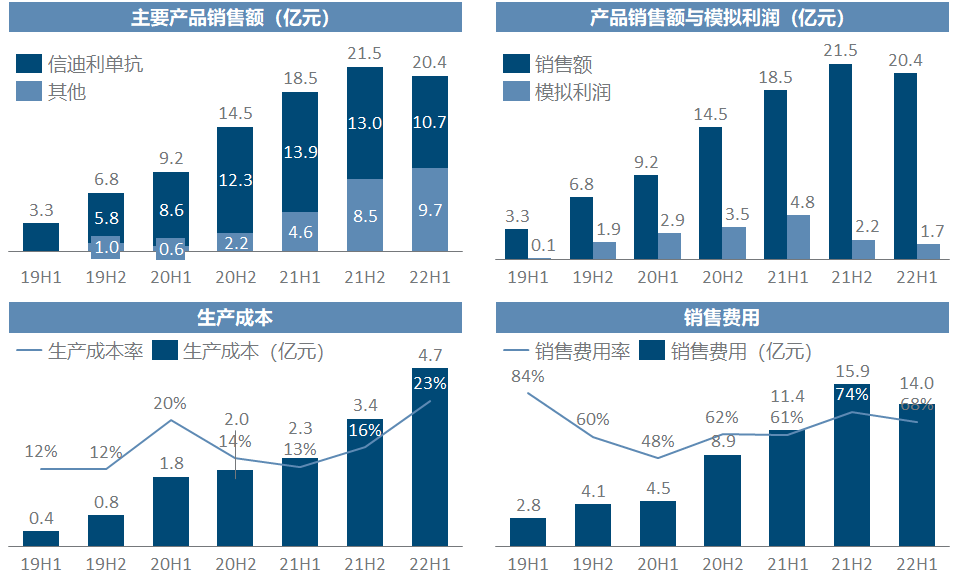

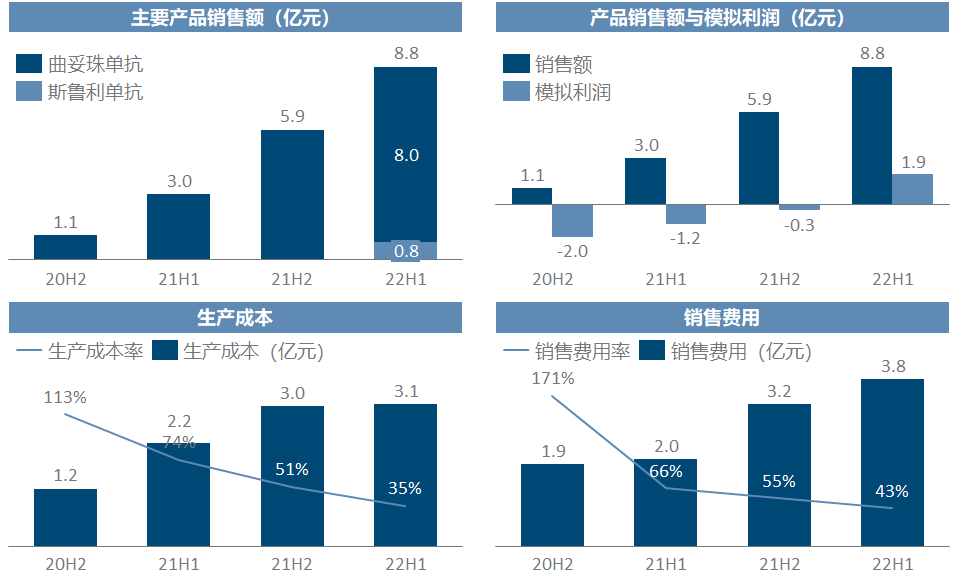

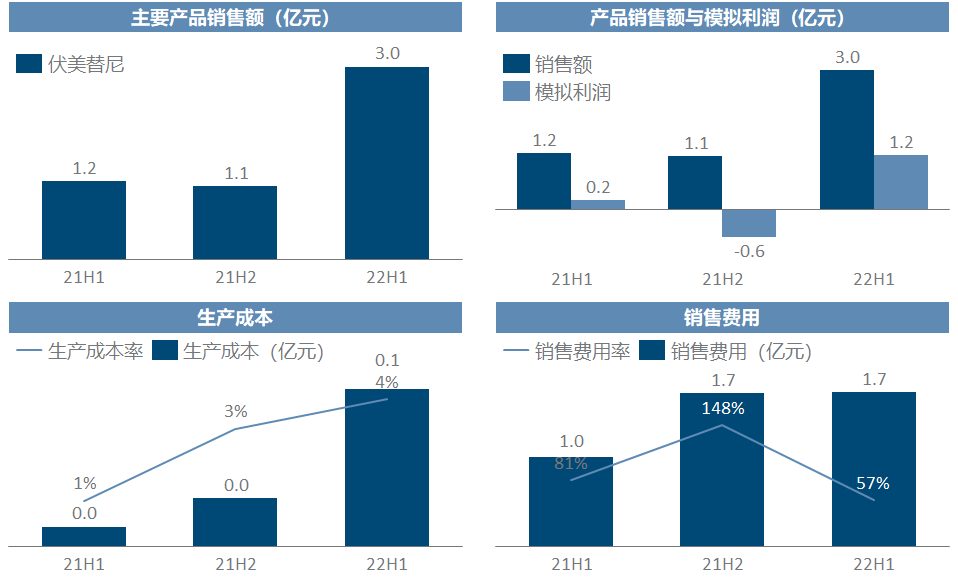

For another example, for innovative drugs (for details, please refer to ” Not all drugs sold are called commercialization “), accelerating their inclusion in the medical insurance list will allow even the re-rolling of the track (PD-1, EGFR T790M, Biosimilar), as long as it is a frontrunner. It is possible to obtain revenue and profits, and in just two or three years of commercialization attempts, several Chinese Biotechs can see the hope of making profits.

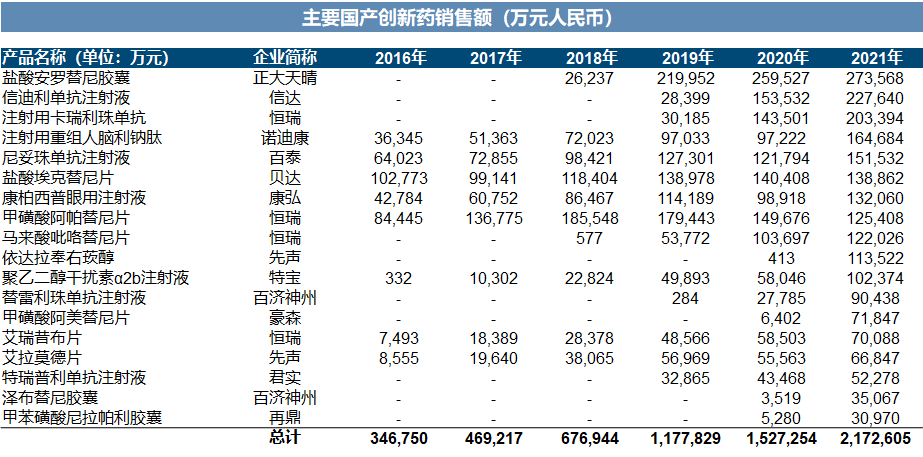

In more detail, we can perceive the transfer payment process from imitation to innovation, from inferior to superior, and from foreign to China from the changes in the sales data of specific varieties (data from Mi Nei).

So how big is this transfer space? We don’t need that exact answer, just a few very rough numbers to have an idea. By 2021, the sales of domestic innovative drugs will be about 30 billion to 40 billion (the table below shows the figures in Mine, considering a certain magnification), and the sales of imported drugs (mostly original drugs and expired patented drugs) will be about 170 billion . , the first six batches of centralized procurement save at least 100 billion medical insurance funds each year, and the future centralized procurement can save at least 200 billion or more space, and the total drug market size is 2 trillion .

In short, domestic innovative drugs are still in the order of tens of billions, the money saved by centralized procurement is already in the order of hundreds of billions, and the final target pool is in the order of trillions . This is what medical insurance is objectively doing.

Of course, the control of medical insurance fees has far-reaching effects on the industry, and it has really caused a lot of companies to suffer huge losses. However, before we try to make a grand conclusion such as “subverting the logic of the industry”, should we abandon the simple and crude emotional label? , Starting from the simplest common sense and logic, think about what it has subverted?

In fact, before and after the crash, the impact of medical insurance has not changed, and the industry’s logic has not been subverted, but some people have had unrealistic expectations about the medical industry. The recent crash is just a correction. post inertia. The medical insurance is the same medical insurance, and the medical treatment is the same medical treatment.

$Hengrui Medicine(SH600276)$ $Minray Medical(SZ300760)$ $Innovent Bio(01801)$

This topic has 35 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1335311504/231387300

This site is for inclusion only, and the copyright belongs to the original author.