Which company is more valuable?

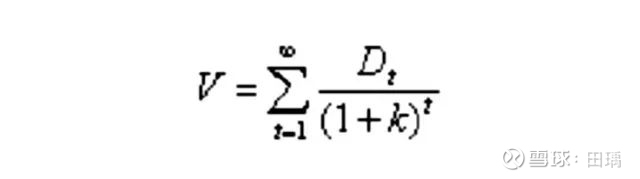

Let’s start with the definition of valuation. Tracing the source, both PE and PB can be unified in the pricing originator of asset pricing-the cash flow discount model. The specific incarnation in the stock is called DDM (dividend discount model). The basic formula is:

where V is the intrinsic value of each stock, Dt is the expected value of the dividend per stock in year t, and k is the expected return on the stock. The formula states that the intrinsic value of a stock is the sum of the present value of its expected dividends year over year. The numerator Dt can be replaced by net profit * dividend rate. We assume that the dividend rate is 100%, which can simplify the understanding. After simplification, the model becomes the well-known profit discount model. In fact, everyone will find a problem here: the application of the profit discount model actually has a scope, and we can discuss this issue later.

Suppose we have two companies on hand, one is growing by 30% for 3 consecutive years, and the other is growing by 15% for 10 consecutive years, which company should be more expensive (assuming that the two companies have maintained their net profit for the year after no growth , 6% discount rate)?

The answer is that the latter is 30% more expensive, that is, the two companies currently earn a dollar in profit. The PE multiple of the latter should be 1.3 times that of the former, and the yield will be the same after holding it all the time, which is what we mean Valuation premium.

As an investor, we should give a premium to the sustainability of reasonable growth, not to short-term high growth. Of course, it should be emphasized here that we are talking about as an investor, not the market. The market often likes to give short-term high growth. Paying a premium, rather than paying a premium to the sustainability of reasonable growth, often creates a lot of investment opportunities for long-term holdings of this type of company for pretty good returns.

Why does the market often prefer short-term high growth?

I guess this is closely related to the uncertainty of economic activity itself. For most companies, the situation facing the next 10 years may change dramatically, which is unpredictable for all analysts and investment managers. Therefore, a school of opinion widely circulated in the market is that there is no way to Look at the long-term, because the long-term is the most uncertain, so more people pursue short-term high growth.

As can be seen from the previous model, short-term extremely high growth can also rival long-term reasonable growth, but this may not be a cost-effective behavior in terms of fundamentals or game play. First, short-term extremely high growth, except for some companies with extremely high barriers and endowments, is not conducive to the development of the company. Rapid expansion will make it difficult for production, management, sales, and service levels to keep up. The hidden dangers left in the process of rapid growth will gradually emerge after the rapid growth period, sometimes destroying a business. This is like a small boat sailing on the sea with full sails. Although it can ride the wind and waves in a short time, the hull of the small boat may be damaged in the process of fast driving. Second, at the gaming level, since this is the choice of most people, it will not be cheap in terms of purchase price, and in the middle and late stages of growth, the game of “running fast” will eventually be played.

So, is it impossible to invest in sustainable, reasonable growth businesses?

I personally don’t think so, but the long-term uncertainty still needs to be resolved. My solution to this problem can be summed up in two principles: first, choose an industry with little industry change, and second, choose a company with high barriers. We don’t know what the iPhone will look like in 10 years, but we can probably judge that we will still eat bread in 10 years. As for the connotation of high barriers, there are many kinds, so I won’t repeat them here.

So for the long term, I chalk it up to barriers and change, and in my case only barriers should give a valuation premium.

Where are the barriers?

There are so many examples around, when you and your family and friends are constantly paying for a brand without hesitation, if you stop and think about it, you may find those barriers.

The above content is not intended as investment advice, please do not be impulsive.

@雪ball Fund @Today’s topic @中泰投資管理

#Invest Xiaoyuzhou

This topic has 14 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5833947526/220777114

This site is for inclusion only, and the copyright belongs to the original author.