@lianghong posted that he bought energy and metal stocks, and this time coincided with a big drop in the Fed’s interest rate hike, and the commenters below were basically one-sided cynicism.

In fact, many times people have different opinions, and it may be because of differences in cognition or concept of different people. In the end, no one can convince anyone. Let me list a few simple facts that are easy to verify.

.

.

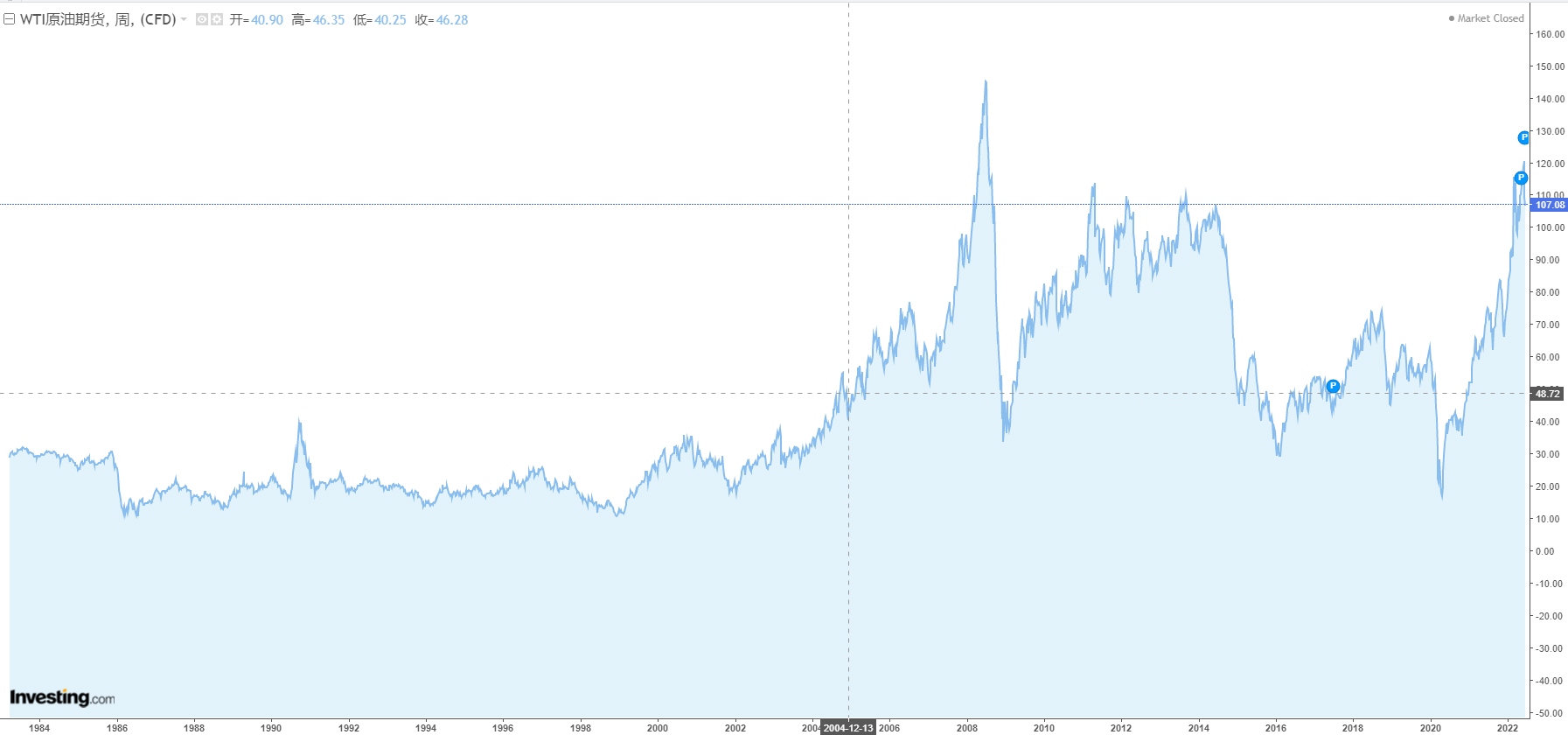

First, about the cyclicality of commodity prices.

[Oil] After two oil crises in the 1970s, it finally hit the all-time high price of crude oil in 1981, which was $39 per barrel. For the next 20 years, crude oil prices peaked near $40. So with this historical experience, and then looking at crude oil with a “cycle” mentality, then you will most likely think that oil prices peaked when crude oil reached $40 again in 2004, and at the same time, it was accompanied by the global central bank raising interest rates. However, in the nearly 20 years that followed, crude oil was below $40 for only 10 months.

.

.

[Copper] Like crude oil, we go back to 2004. The copper price doubled rapidly in a short period of time and was close to the highest price in history. At that time, the Shanghai copper price was 3w/ton. What would have happened if the copper price had peaked at the time? It is a pity that in the following nearly 20 years, the monthly closing price of copper was lower than 3w for only 4 months.

.

.

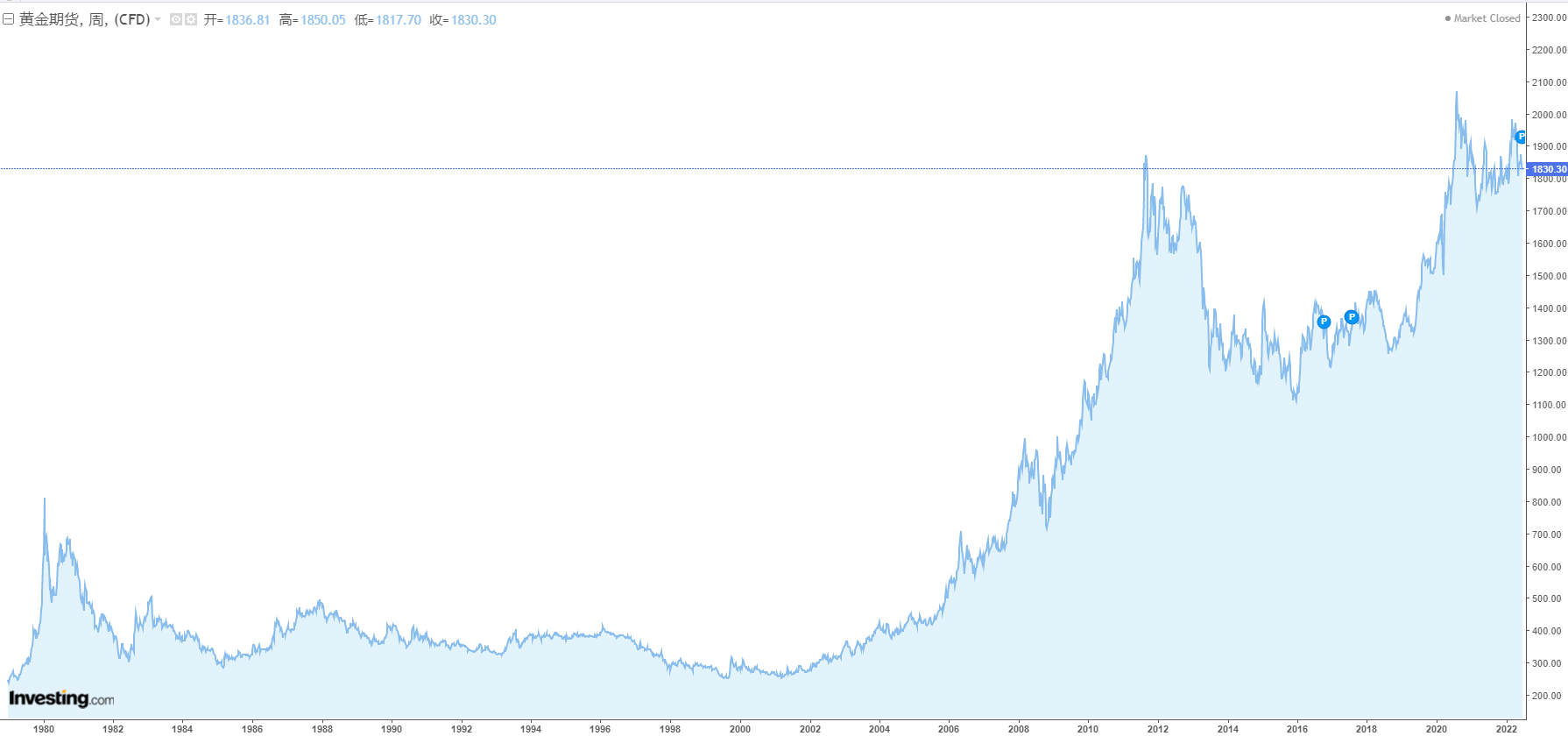

[Gold] Of course, as a quasi-currency, its cyclicality is much weaker than that of general commodities. Therefore, the price-earnings ratio of gold stocks is actually much higher than that of cyclical stocks.

.

Therefore, the high of the previous cycle turned out to be the bottom of the next cycle. This conclusion is easy to draw.

.

.

Second, on the company’s performance.

Of course, for the industry, strong cyclicality is the mortal enemy of many companies. We often see cyclical stocks continue to lose money in the down period, and I also think this phenomenon is too normal. why? Because expansion and mergers and acquisitions are commonplace in the industry during the most prosperous years of a cycle, few companies can resist the splendid temptation of the peak of the cycle. It should be understood, however, that commodity price volatility is not the reason for cyclical losses. And investment in high-cost mines and high-priced mergers and acquisitions in the industry are the culprits of their losses. So when we look at the cyclical industry as a whole, most companies are destroying value in rounds of cycles. But from another angle, since the expansion at the top of the industry is the root cause of value destruction, don’t companies that can expand and M&A at the bottom of the industry have a growth that far exceeds the industry?

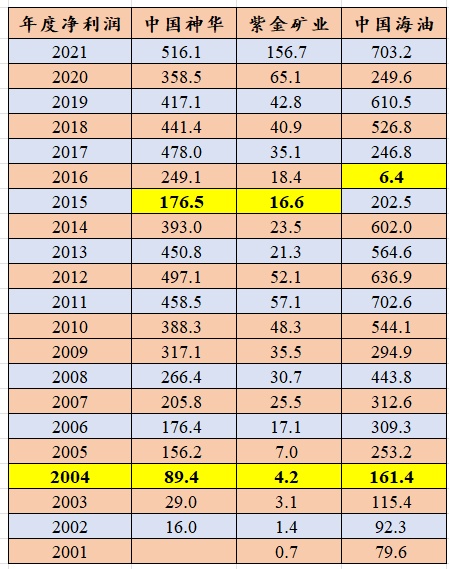

Also, why is 2004 a good year to watch? Because looking back in 2004, commodity prices were at the highest level in history, but looking back in 2004, commodity prices were in the bottom range again. In addition, 2004 was also the starting point for the Fed to start its interest rate hike cycle.

.

China Shenhua, Zijin Mining, CNOOC, the three most representative resource stocks, their performance in 2004 is basically “the highest in the past and the lowest in the future”. For example, China Shenhua and Zijin Mining, the worst performance years after 2004, the net profit is far greater than 2004. Therefore, if you only see the cyclicality of commodities without seeing a long-term upward trend, then in 2004, it was a big joke to think that the so-called cyclical stocks were at a cycle high, both in terms of performance and stock prices. .

.

.

Therefore, if the apex of the previous cycle is the bottom of the next cycle, then our commodity cycle has not really begun. Because the prices of crude oil, coal and copper have not broken through the peak of the previous round.

This topic has 109 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9794771369/223620818

This site is for inclusion only, and the copyright belongs to the original author.