Three years of 3.6 billion losses

Three years of 3.6 billion lossesWelcome to the WeChat subscription number of “Sina Technology”: techsina

Text / Chiron

Source/Value Planet Planet (ID: ValuePlanet)

Another Chinese concept stock opted for dual primary listing.

A few days ago, Kingsoft Cloud officially submitted an IPO listing application to the Hong Kong Stock Exchange, applying for dual primary listing of Hong Kong stocks. After the news was announced, Kingsoft Cloud’s U.S. stock price also rose. On the evening of the 27th, Kingsoft Cloud US stocks closed at $3.47 per share, a single-day increase of 2.66%.

However, the single-day increase cannot hide the big trend of the company’s stock price. At the beginning of May 2020, Kingsoft Cloud landed on Nasdaq at an issue price of US$17 per share. In the following year or so, Kingsoft Cloud’s share price continued to climb, reaching a high of US$70.35 per share on February 12, 2021. point.

But then, the share price of Kingsoft Cloud “falls endlessly”. As of the close on August 2, 2022, Eastern Time, Kingsoft Cloud’s US stock price was only $3.18 per share, 95.48% evaporated from the highest point and 81.29% lower than the issue price. It can be seen that Kingsoft Cloud is not as attractive to US stock investors as it used to be.

It is true that the decline of Kingsoft Cloud’s share price has a certain relationship with the overall market, but it is also inseparable from the company’s performance. Last year, Kingsoft Cloud had a net loss of 6.789 billion and a net profit margin of -35%. On May 11, 2022, the SEC also included Kingsoft Cloud in the “pre-delisting list”.

Therefore, the “crux” of Kingsoft Cloud may not be solved by changing the listing location.

“Strategic losses” have become the norm

In fact, from the perspective of revenue, Kingsoft Cloud still shows strong vitality. The prospectus shows that from 2019 to 2021, Kingsoft Cloud’s revenue will be 3.956 billion yuan, 6.577 billion yuan and 9.061 billion yuan respectively, with a compound annual growth rate of 51.3%.

More importantly, the scale of China’s cloud computing market is also expanding. According to data from the Prospective Industry Research Institute, from 2019 to 2021, the scale of China’s cloud computing market will be 133.4 billion yuan, 209.1 billion yuan and 310.2 billion yuan respectively, up 56.7% and 48.4% year-on-year respectively.

Considering that Kingsoft Cloud’s revenue growth rate is very close to the industry growth rate, it can be seen that the company has not been “fallen” by the industry. The capital market should have believed Kingsoft Cloud’s “cloud computing story”, but as mentioned above, its performance in the secondary market is not ideal, which may be related to Kingsoft Cloud’s continuous loss.

According to the prospectus, from 2019 to 2021, the net losses of Kingsoft Cloud will be 1.111 billion yuan, 962 million yuan and 1.592 billion yuan respectively. In Q1 2022, Kingsoft Cloud’s revenue was 2.174 billion yuan, a year-on-year increase of 19.9%, but the net loss was as high as 555 million yuan, a year-on-year increase of 45%.

It can be found that although Kingsoft Cloud’s revenue is growing steadily, its losses are also continuing to expand.

The core problem of Kingsoft Cloud’s losses is that cloud computing is a “heavy asset” business, and at this stage, it has to continue “blood transfusion” in terms of “infrastructure”. In the past three years, Kingsoft Cloud’s operating costs reached 3.949 billion yuan, 6.220 billion yuan and 8.71 billion yuan, accounting for 99.8%, 94.6% and 96.1% of total revenue, respectively.

Source: prospectus

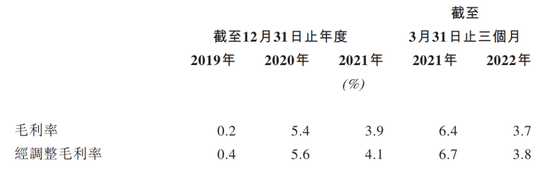

Source: prospectusOperating costs remain high, which has seriously affected Kingsoft Cloud’s gross profit margin. According to the prospectus, from 2019 to 2021, the adjusted gross profit margin of Kingsoft Cloud will be 0.4%, 5.6% and 4.1% respectively. Considering that the gross profit rate of traditional Internet business is often in double digits, Kingsoft Cloud’s single-digit gross profit rate is indeed difficult to attract investors’ attention.

However, it cannot be ignored that the cloud computing industry is inherently characterized by a long construction period and a large investment. At present, in China’s cloud computing industry, except for Alibaba Cloud, most cloud computing-related companies are in a loss-making stage.

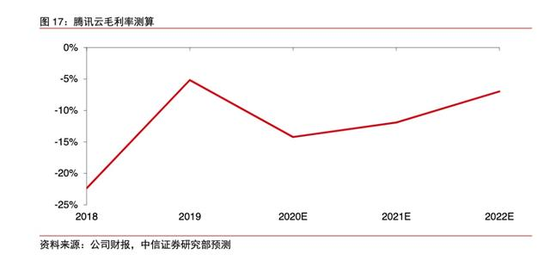

Source: CITIC Securities

Taking Tencent Cloud as an example, CITIC Securities has calculated that from 2020 to 2022, its gross profit margin will be -14%, -7% and -7% respectively. In mid-2020, Tang Daosheng, president of Tencent Cloud and Smart Industry Business Group, said that Tencent plans to invest 500 billion in the next five years for “infrastructure” such as cloud computing and servers.

From this perspective, “strategic losses” are actually the norm for cloud computing players at this stage.

The “big customerization strategy” has been challenged

Kingsoft Cloud’s continued losses are actually just the appearance of causing investors to flee.

On top of this, most investors dare not continue to bet on Kingsoft Cloud, mainly because the latter’s influence in the market is shrinking.

Although Kingsoft Cloud declared itself as “China’s largest independent cloud service provider” in its prospectus, based on market research data, Kingsoft Cloud is no longer as brave as it used to be.

According to IDC data, in the first half of 2017, Kingsoft Cloud accounted for about 6.5% of the market share in China’s public cloud IaaS, ranking third after Alibaba Cloud and Tencent Cloud; in Q3 2021, Kingsoft Cloud’s market share is only 2.89%, ranking eighth. At the same time, Alibaba Cloud, Huawei Cloud, Tencent Cloud and other five major players also shared more than 70% of the market share.

At the end of 2014, when the cloud computing business was just laid out, Lei Jun, chairman of Kingsoft Cloud, once said: “Cloud services are different from the Internet. As a basic service, China needs three to five companies. We (Kingsoft Cloud) are not necessarily the first, but we must. Stay in the top three, top five.”

Now nearly 8 years have passed, and Jinshan Cloud has fallen out of the “top five” red line drawn by Lei Jun.

But it is worth noting that cloud computing business is ultimately connected with customers. Kingsoft Cloud’s market influence is gradually shrinking, which is also related to its long-standing adherence to the “big customer-oriented strategy”. In this regard, Lei Jun once said, “Giants do cloud services because they are very strong, and they are willing to be big and comprehensive. We select some leading companies, and then strive to serve these customers well.”

Source: prospectus

Source: prospectusAccording to the prospectus, from 2019 to 2021, Kingsoft Cloud will have 243, 322 and 597 high-quality customers, respectively, contributing 97.4%, 98.1% and 98.2% of the revenue to the former.

At the same time, the top five customers contributed 65.7%, 61.5% and 50.5% of the revenue to Kingsoft Cloud respectively. Horizontal comparison shows that Kingsoft Cloud relies heavily on the top five customers.

With the development of enterprises, more and more enterprises begin to have clear cloud service requirements, and most of these large and medium-sized enterprises choose to build their own cloud platforms. This makes some of Kingsoft Cloud’s partners directly change from the previous “customers” to the current “adversaries”.

The prospectus shows that in 2020, ByteDance will become Kingsoft Cloud’s largest customer, contributing 28% of the latter’s revenue. However, it was also in the middle of 2020 that ByteDance launched the Volcano Engine and began to enter the cloud computing market.

At the end of 2021, Yang Zhenyuan, vice president of ByteDance, revealed that 95% of ByteDance’s domestic business runs on self-built cloud services, and Douyin, Toutiao, and Understanding Chedi are all major customers of Volcano Engine Cloud.

The loss of bytes not only means a reduction in the company’s future revenue, but also means that the original “big customerization strategy” may be at risk. Regarding the above risks, Kingsoft Cloud stated: Most of our revenue comes from a limited number of customers, and the loss of one or more high-quality customers or a significant reduction in their usage will lead to a decrease in our revenue and may damage our business.

The new “story” of industry cloud

In order to balance the high operating costs and capture the new generation of customers, Kingsoft Cloud has been constantly exploring new development paths in the past two years.

Source: prospectus

At present, Kingsoft Cloud’s main focus has shifted from “public cloud + enterprise cloud” to “public cloud + industry cloud”.

According to the prospectus, from 2019 to 2021, Kingsoft Cloud’s revenue from public cloud business accounted for 87.4%, 78.5% and 68% respectively; the revenue from industry cloud business accounted for 12.3%, 20.9% and 32% respectively. Horizontal comparison shows that Kingsoft Cloud’s industry cloud business has a clear upward trend.

Kingsoft Cloud’s efforts in the industry cloud are likely because it sees that in the public cloud industry, it is increasingly difficult for small and medium-sized enterprises to form economies of scale in order to overtake giants. Taking Youkete, which is also on the public cloud track, as an example, the financial report shows that in Q1 2022, its net profit attributable to its parent company was negative, and its revenue plummeted by 25.73% year-on-year.

In contrast, in the prospectus, Kingsoft Cloud stated, “Industry cloud services have the advantage of lowering our capital expenditure requirements, because customers are usually responsible for the cost of underlying equipment and cloud resources (such as Internet data center services and servers).”

From an industry point of view, with the gradual saturation of the market, it is difficult to nourish more cloud computing companies by simply helping Internet companies “go to the cloud”. Enterprises in government, industry, and other fields may indeed become the next “virgin land” in the cloud computing market. “.

In this regard, Yu Baicheng, Dean of Zero One Research Institute, said: “At present, the public cloud market structure has been initially completed… The cloud computing market is still in the process of high demand growth. Therefore, other players such as Kingsoft Cloud provide services through industry clouds. Shen, form differentiated competition and seek market space.”

However, there are not many players in this field, and Kingsoft Cloud has to face the competition from the giants.

Source: IDC

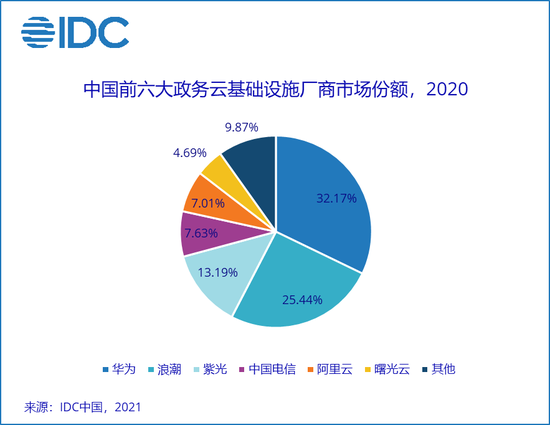

Source: IDCFor example, in the field of government affairs, HUAWEI CLOUD has become the first. IDC data shows that in 2020, in China’s government cloud infrastructure market, Huawei Cloud, Inspur and Tsinghua University will occupy 32.2%, 25.44% and 13.19% of the market share, ranking among the top three. HUAWEI CLOUD has occupied the top position in China’s government cloud infrastructure market share for four consecutive years.

For government-level customers, Huawei has built a closed-loop cloud technology ecosystem and omni-channel sales capabilities. According to official data, through the HUAWEI CLOUD Stack system, HUAWEI CLOUD can help enterprise-level customers achieve unified management of multi-cloud and multi-resource pools. In order to serve government-level customers more conveniently, Huawei has also set up representative offices in more than 30 provincial-level administrative regions across the country, reducing the time for customers to go back and forth.

At present, Kingsoft Cloud mainly provides services for games, finance and other fields, and its customers include Bilibili, Zhihu, Giant Network, etc.

For example, in the financial industry, Kingsoft Cloud serves nearly half of large state-owned banks and joint-stock banks, and six of the top 10 banks are the company’s customers. These customers can become classic cases of Kingsoft Cloud’s external publicity, and with the deepening of cooperation, they can also help Kingsoft Cloud to establish an industry position.

It should be noted that the more such a big “gold master” is, the more likely it is to be “pried away” by opponents, which also makes Jinshan Cloud have to face more intense competition.

Paypal founder Peter Thiel said in his book “From 0 to 1: The Secret to Unlocking Business and the Future”, “Any big market is the wrong choice, and there are already other competitors. The big markets that exist are worse. That’s why entrepreneurs trying to get 1% of a $100 billion market always don’t work.”

Therefore, it is not easy to survive in the cracks of large cloud factories. The difficulty of Kingsoft Cloud, which has been squeezed into the “second echelon”, lies in reducing costs, in how to turn losses, and in expanding scale.

*This article is based on public information and is only for information exchange and does not constitute any investment advice

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-09/doc-imizmscv5482744.shtml

This site is for inclusion only, and the copyright belongs to the original author.