Abundance is harder for us to handle than scarcity.

– Taleb

1. Business segment and development stage

Alibaba is huge, and it is necessary to straighten out the business first. After completing the organizational structure adjustment at the end of last year, Ali is roughly divided into Chinese digital commerce (Taobao, Tmall, Alimama, Taocaicai, Taote, Sun Art Retail, Hema, etc.), overseas digital commerce (lazada, global AliExpress, international trade, etc.), cloud business (Alibaba Cloud, DingTalk), local life (Ele.me, Koubei, AutoNavi, Fliggy), Cainiao Network, Big Entertainment (Alibaba Entertainment), innovative business. Others are unconsolidated holdings and investments, such as Ant.

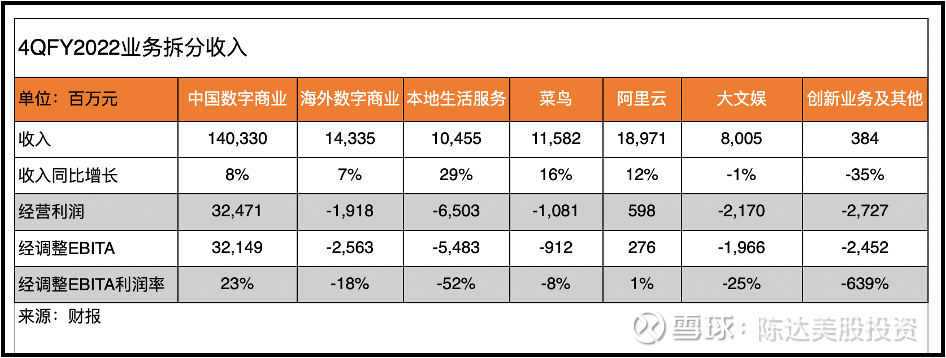

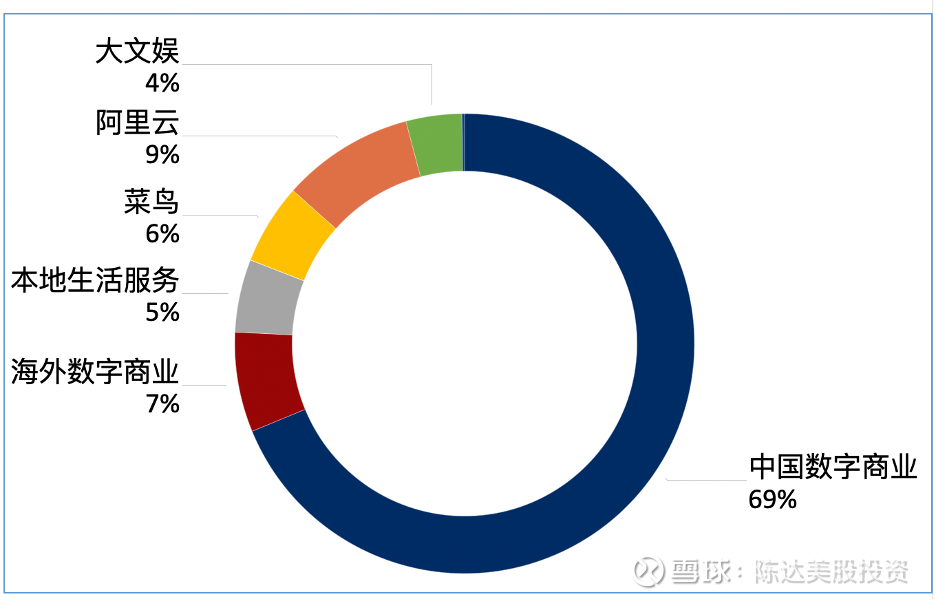

Ali’s total revenue in Q4 of fiscal year 2022 is 204.05 billion yuan, a year-on-year increase of 9%; the corresponding revenue figures for each business, as well as the donuts of business weight, are shown in the following chart.

(Data source: company financial report, drawing: Damou)

Of course, the income figure is a tricky thing. In different industries, it is not necessarily that the smaller the number, the better. In terms of income, e-commerce and retail have inherent advantages (if it is a platform market model, it is better, commission is a net income, if it is Self-operated revenue is retail sales. So it is not surprising that Walmart is the world’s largest company in terms of revenue ), so when we look at the composition of the business, revenue may be a confusing little fox, and we should also look at profit margins; but given that Alibaba Most businesses do not yet have operating profits, so use income doughnuts to outline the sense of an overall business.

In addition, this donut also helps us understand where Ali has developed as a company that intends to exist for 102 years. For example, we go back to 2017 five years ago. At that time, Alibaba Cloud’s revenue accounted for 4.2%, while the proportion of Amazon AWS was 9.82%, which is comparable to the current Alibaba Cloud. Of course AWS margins have been very high, which is another topic. Today AWS accounts for 16% of Amazon’s revenue. Cloud computing, as the second growth curve of high probability. We may also roughly deduce Ali’s revenue development. Even if there is a suspicion of carving a boat and seeking a sword, it is still a reference on the time axis. Because there are too few comparable companies.

(Data source: company financial report)

2. Consumption field: ACC supports the market, reduces costs and increases efficiency, and focuses on high-quality growth

When I was writing the forecast of the financial report, I said that Ali’s domestic ACC (annual active users) should be around 1 billion. The specific number depends on the financial report – the final figure is China’s digital business (Amoy) ACC 903 million, and the overall domestic AAC in the consumption field exceeds 1 billion. 1 billion, which is 1.31 billion overseas global ACC. Among the ACCs with an annual net increase of 113 million in domestic consumption, 70% come from underdeveloped areas that are simple and simple. The strategy of sinking the market has always worked.

The user growth dividend has gradually peaked, but the unit consumption capacity is still acceptable – in FY2022, more than 124 million ACCs spent more than 10,000 yuan on Taobao and Tmall. These users who contribute to the ultra-high ARPU value are Taoist iron fans, with a cross-year activity rate of 98%, that is, only a 2% churn rate . The 124 million was also labeled as a high-quality consumer group.

In addition to Tmall Taobao, 2C consumption in a broad sense also includes overseas, local, large entertainment, etc. You can also see from the business split at the top of me that most projects in Ali consumption are not profitable, except for Chinese figures, other businesses do not need Speaking of net profit, there is not even EBITDA or even operating profit.

But what I’m trying to say — very counterintuitive — is that this row of sub-zero numbers, I think, is the reason the market jumped on this earnings report (shares opened 14% higher).

Why is the capital market enthusiastic about this quarter’s earnings report? ——I don’t think that the early fall is one reason, and another important reason I think is that the market sees signs of profitability in many of Ali’s businesses (and this sign is not caused by the growth of the topline you are struggling to pull up, Instead, it is done to improve operational efficiency, so it is very controllable, such as reducing wasteful investment, cutting off inexplicable projects, etc.). This is far more realistic than breaking the growth ceiling.

For example, Ele.me, which has lost God knows how many years, is gradually approaching the breakeven breakeven line, the loss of Dawen Entertainment (digital media and entertainment) is narrowing, and Alibaba Cloud is also profitable for the first time in 13 years in fiscal year 2022. Even if the profit of consumption declines, it is due to the investment of Taocaicai and Taote, and the loss of the acquisition of Sun Art. These investments are easy to be recalled. Obviously, Alibaba has shifted its strategy from expansion to customer expansion and intensive cultivation of operational efficiency. As a budget-conscious investor, the market naturally smiled at these signs, and the stock price rose by 14%.

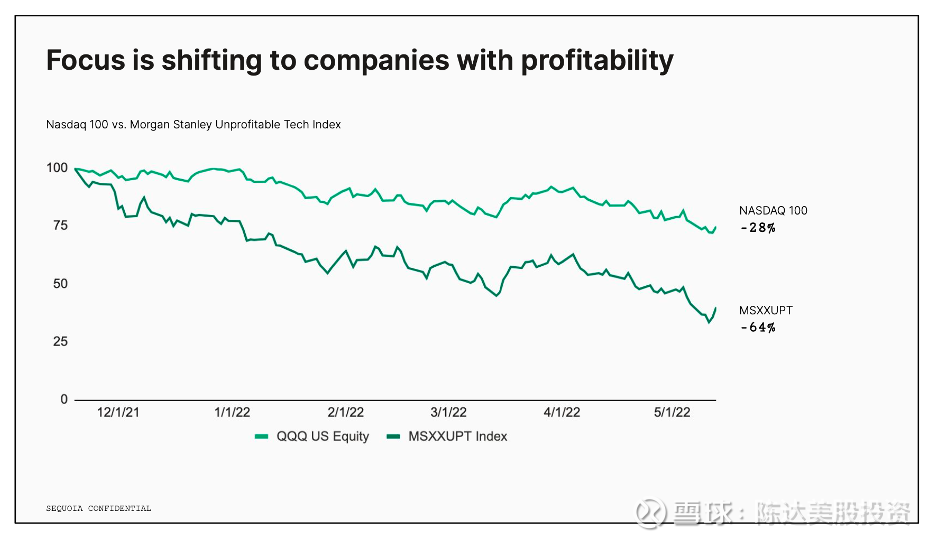

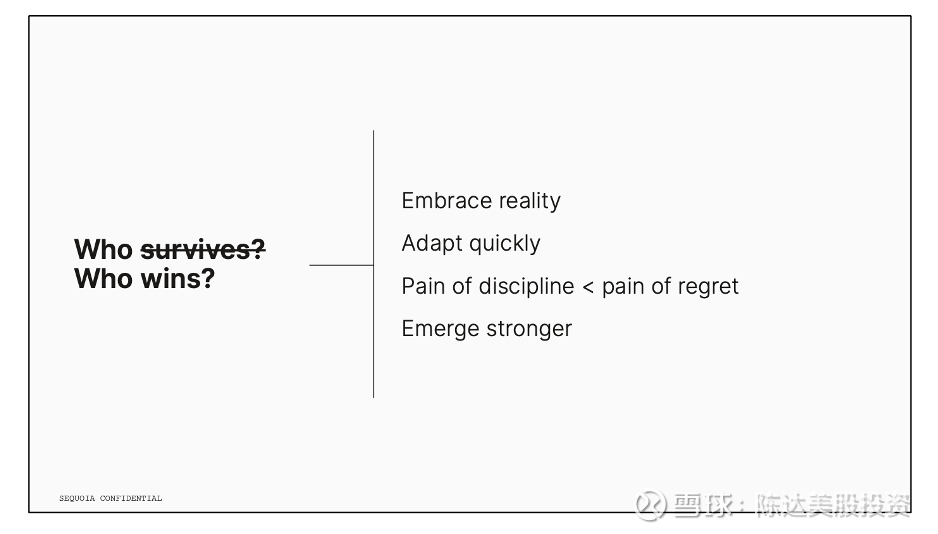

The times are tough these days. If you play the efficiency card, shareholders will naturally be happy for a moment. In the past, no one looked at the profits of Internet companies, because at that time, the economic boom was growing rapidly, the demographic dividend was sufficient, the cost of capital was extremely low, the expansion was not burdened, and the expansion of the business brought about, and even many startup investment fevers never considered the issue of making money. Because the IPO is the end of the line; and now, with high inflation and a weak economy, if you continue to wave, the market will spank you. For example, in this chart from Sequoia, the Nasdaq is down 28% since December, while the “Morgan Stanley Losing Tech Company Index” (dark green line) has fallen 64% over the same period, slashing from the thigh. Regardless of China and the United States, the investment environment is undergoing a huge change such as the cosmic microwave background, and for this change, the breaking point is four words – cost reduction and efficiency increase .

(Data source: Sequoia)

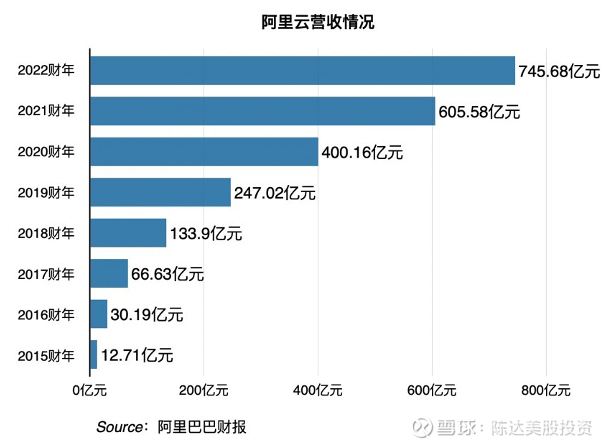

3. Alibaba Cloud’s first annual profit

Alibaba Cloud, Yunjuan Yunshu for 13 years, finally made money in fiscal year 2022, including Q4, it has achieved profitability for 6 consecutive quarters. In the global market, according to Gartner data, Alibaba Cloud will rank third in global cloud computing in 2021, with a market share of 9.55%, and has increased its market share for six consecutive years.

Of course, Alibaba Cloud’s business has a first-mover advantage, and it is also obvious in the domestic development echelon. Alibaba Cloud believes that its barriers lie in “self-developed core technologies and Alibaba’s continuous investment in technology research and development.”

What’s more troublesome in the past few quarters outside of technology is the growth rate. Alibaba Cloud’s loss of Byte, a major customer, led to a stall. Last quarter, the growth rate slowed to 20%, and this quarter slowed down further by 12%. Excluding the impact of Bytes, the year-on-year growth of cloud business revenue was 29% (for reference, the growth rates in the first four quarters were 36%, 30%, 33%, and 20% respectively). In addition to Bytes, the financial report revealed that customers in China’s Internet industry Due to the reduction in demand, the slowdown in economic activity and the impact of the epidemic, the delivery of some projects has been delayed.

I personally expect that Alibaba Cloud’s growth rate will pick up again in the second half of the year. Because Alibaba Cloud’s revenue has a trend of diversification, especially the revenue contribution of customers from non-Internet industries continues to rise, which has reached half of the business. Alibaba Cloud has more than 4 million paying customers, including 62% of A-share listed companies, and the customer base is very diverse.

In the long run, the cloud computing business is an economic account, whether there is an economy of scale, and whether it can make money. Alibaba Cloud, which lost 3.7% in adjusted EBITA in fiscal year 2021, made a small profit of 2% in adjusted EBITA in fiscal year 2022, and compared with AWS (operating income), which earned US$6.5 billion in a quarter, after the scale effect of cloud computing, it can be achieved after breakeven. Whether it will become Ali’s overall profit cow in the future. In addition, the cloud is also a sail to the sea. Previously, Alibaba Cloud opened two data centers in Frankfurt and Thailand. In fiscal 2022, the new data centers will be located in Indonesia, the Philippines, South Korea, Thailand, and Germany. In the future, China’s Internet and even all Chinese companies will further go overseas, and cloud computing is similar to the infrastructure of the Belt and Road Initiative.

(Data source: financial report)

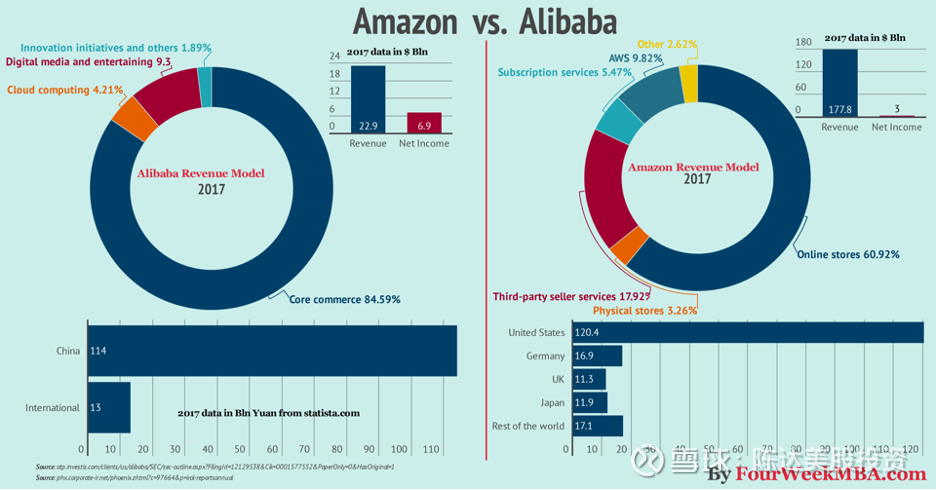

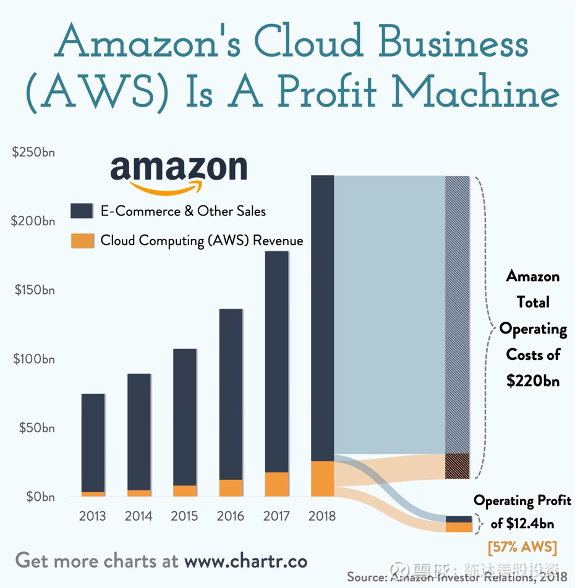

(Although Amazon’s AWS revenue in 2018 is much smaller than that of e-commerce, it relies on huge economies of scale to create 57% of Amazon’s operating profits. Can Alibaba Cloud replicate its profits?)

In addition, there is one thing that AWS does not have. Alibaba Cloud has a large-scale DingTalk. As of the end of March, the number of enterprise organizations served by DingTalk has exceeded 21 million.

4. Conclusion

While growth is slowing, I don’t think that’s necessarily a bad thing for investors. The obvious message I see is that the management emphasizes “adhering to high-quality growth”. If it is replaced by shareholders’ favorite, this is to start the rhythm of closing and closing, and at the same time, focus on core business through measures such as refined operation, cost reduction and efficiency increase. You once criticized you as a shareholder. Internet people who are too determined will use trial and error as the mother of innovation as a shield. They may even quote Taleb: Trial and error is freedom. – Now it’s your turn, you can quote Taleb’s antifragile.

So when I saw Zhang Yong’s financial report, he mentioned three “high quality”, and I felt very comfortable. This is a businessman talking about business in a realistic style. The first is to serve high-quality consumer groups. Alibaba serves the largest and highest-quality consumer groups in China. ; The second is to continuously build high-quality digital business infrastructure, the core that Ali has always emphasized. The third high-quality innovation and development of the broad potential of cloud computing, to put it bluntly, is to allow the second growth engine to generate scale effects and continue to improve profitability.

Let’s look forward to Q2 and Q3 in 2022 (2023 Q1 and Q2 in Ali’s fiscal year). Q2 is expected to compare the crotch, e-commerce, logistics, supply chain, and end-to-end crotch. The growth of topline’s revenue is almost certain to be affected, but a series of “high-quality” wordings make me have a good reverie about the bottomline’s profit side. I think that’s how the market reacted. Worrying about the uncertainty of the future, when I suddenly saw these words in the foggy forest, Ali CFO Xu Hong’s words made investors feel relieved-“Looking forward to fiscal year 2023, we will We will firmly focus on sustainable and high-quality revenue growth, focus on optimizing the operating cost structure, and improve the overall return amid uncertainty.”

As Sequoia recently talked about not only surviving, but also surviving, in an environment of great uncertainty—painful discipline is better than painful remorse. “Discipline”, “face reality”, “fully adjust and adapt”, “reduce costs and increase efficiency”, the development of Internet giants, both China and the United States, has entered a new stage.

(Source: Sequoia)

——————

Disclosure of interest: The author holds a long position in $Alibaba (BABA)$ $Alibaba-SW(09988)$ ;

This article does not constitute any investment advice

This topic has 230 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/9598793634/221277315

This site is for inclusion only, and the copyright belongs to the original author.