$CNOOC(00883)$ $CNOOC(SH600938)$ $CNOOC(SH601857)$

Recently, I have seen some new faces in the CNOOC Forum. They still know very little about CNOOC, while many stockholders with deep research are calm and seldom speak.

I asked and answered myself, from the perspective of a new shareholder, asked 15 questions around “Why many people dare not buy CNOOC”, and then answered it myself, hoping to attract more people to pay attention to and discuss CNOOC.

1. PetroChina, which was bought for 48 yuan at the time, has not been solved yet, and I dare not touch oil stocks.

2. I bought a crude oil fund in 2020, and there was a negative oil price event, which plummeted. I was afraid.

3. Now that new energy is advocated, the penetration rate of new energy vehicles is rising rapidly. Will the oil be sold in the future?

4. The capital expenditure of CNOOC in 2021 is 88.73 billion yuan, which is higher than the net profit of 70.31 billion yuan. It is too scary. Will it be like real estate?

5. Is low PE reliable? COSCO SHIPPING Holdings has not fallen from 3PE last year to 2PE now.

6. Dividends must be ex-righted, the money is only from the left pocket to the right, and the dividend tax must be paid. The higher the dividend, the more deductions, which is boring.

7. I am very afraid of cyclical stocks. I lost a lot in cyclical stocks before, and I am afraid.

8. Cyclical stocks should be bought when PE is high or even at a loss. Now CNOOC’s PE is very low, and it should be sold at the top of the cycle.

9. CNOOC only has about 10 years of proven reserves, and the oil is exhausted. What will happen in the future?

10. The US dollar raises interest rates, which is bad for commodities, dare to buy oil?

11. The price of crude oil is too difficult to predict. I don’t know the rise or fall of tomorrow. How dare I buy oil stocks.

12. CNOOC has gone up a lot this year and doesn’t want to carry a sedan chair for others. I heard that the big gold chain recently supported oil stocks.

13. CNOOC makes so much money, will there be any company to grab its business in the future?

14. CNOOC Port A shares are twice as expensive as Hong Kong shares, and the new shares are terrible.

15. Since CNOOC is so good, why is no one willing to buy it? If there was gold on the ground, it would have been picked up long ago.

1. PetroChina, which was bought for 48 yuan at the time, has not been solved yet, and I dare not touch oil stocks.

Answer: At the end of 2007, PetroChina was listed on A-shares with an issue price of 16.7 yuan and a net profit of 136.2 billion yuan in 2006. Calculated based on the total share capital of 183 billion shares after the issuance, it was issued with a market value of 3,056.1 billion yuan and a 22PE static price-earnings ratio. The highest on the first day of listing rose to 48.62 yuan, 8897.4 billion market value, 65.3PE! And my country’s GDP in 2007 was 27 trillion yuan, and the market value of PetroChina was as high as nearly 1/3 of the country’s annual GDP. Can it support it?

15 years later, CNOOC issued at a low price of 10.8 yuan, calculated based on 47.6 billion shares after issuance, net profit of 70.3 billion yuan in 2021, 514.1 billion market value, 7.31PE, note that this is not the top of the cycle, but the average realized oil price of 67.89 US dollars corresponding performance.

The issue price of CNOOC’s A shares has made Hong Kong stockholders angry enough. However, there were many people in forums such as Dongcai at that time discussing whether they would break!

Is it because the investors back then were brave, but are the investors now timid? not necessarily! Maybe only the brave ones are different. Five years later, look at the Ningde era and BYD.

How much worry can you have, just like 48 full warehouses of PetroChina! PetroChina’s high-price issuance and the nearly tripled speculation on the first day seriously affected investors’ sentiment towards oil stocks.

2. I bought a crude oil fund in 2020, and there was a negative oil price event, which plummeted. I was afraid.

A: The crude oil fund tracks crude oil futures, and there is a loss of positions; the crude oil fund is FOF, and the fund of the fund receives double management fees. That is to say, when the oil price in one year is the same as it is now, the net worth of the crude oil fund will be lower than it is now. Under the extreme negative oil price event in early 2020, the fund lost 30% in the short term, and the oil price rebounded, but the net value of the fund was permanently lost.

Time is the enemy of crude oil funds, but it is the friend of oil companies. Because oil companies produce oil, they continue to make profits when oil prices are higher than costs. The average annual oil prices in 2016 and 2020 are similar, but CNOOC only broke the capital in 2016, and its net profit in 2020 is 25 billion yuan.

3. Now that new energy is advocated, the penetration rate of new energy vehicles is rising rapidly. Will the oil be sold in the future?

A: Some people say that electric vehicles will replace gasoline vehicles, just as cars replaced horse-drawn carriages, and penetration will accelerate. That’s a lot of thinking. Now the comprehensive competitiveness of trams is obviously not as good as that of gasoline cars, and it is supported by policies. The overall cost of using trams is higher, mileage anxiety due to inconvenient charging, and unpredictable battery spontaneous combustion. Even if there are some advantages, it may become a disadvantage when it is not used properly, such as fast starting and assisted driving.

Optimists believe that with the increase in scale and the development of technology, key problems can be solved. In fact, with the increase in penetration rate, due to the scarcity of lithium ore, the cost of battery raw materials has risen sharply. , by the beginning of this year, it will rise to 500,000 yuan / ton, you are right, it will rise 10 times a year! As the penetration rate of trams increases, there will be more queues for charging, which will increase range anxiety.

Xiaoming scored 10 points last year and 20 points this year; Xiaohong scored 70 points last year and 90 points this year; Xiaoming’s score has increased by 100%, and the proportion is much higher than Xiaohong’s. Is his learning ability stronger and more promising? ?

The penetration rate of new energy vehicles (lithium electric vehicles) in my country is rising rapidly, but the number of gasoline vehicles is increasing faster. In 2021, China’s car ownership will be 302 million, a year-on-year increase of 7.5%, or an increase of 21 million! In 2021, the production and sales of new energy vehicles will be 3.545 million and 3.521 million respectively, up 159.5% and 157.5% year-on-year, respectively, and the amount of scrap is not subtracted here. Let’s make a rough calculation. The increase in the number of gasoline vehicles is more than 5 times that of new energy vehicles. Do you want to burn oil? In 2021, the domestic consumption of refined oil products will be 341.48 million tons, a year-on-year increase of 3.2%, of which gasoline, diesel, and jet fuel will increase by 5.7%, 0.5%, and 5.7% year-on-year, respectively.

Globally, the total sales of electric vehicles (EV) and hybrid vehicles (PHV) in 2021 will reach nearly 6.6 million units, setting a new record again; my country accounts for more than half of this increase.

Taking a step back, even a slight drop in automobile oil consumption does not mean a drop in crude oil consumption. Crude oil is not only used to produce gasoline, but also diesel and aviation kerosene, as well as plastics and various chemical raw materials. Crude oil is not only energy, but also an important resource.

4. The capital expenditure of CNOOC in 2021 is 88.73 billion yuan, which is higher than the net profit of 70.31 billion yuan. It is too scary. Will it be like real estate?

A: The capital expenditure is not deducted from the net profit. The capital expenditure will be included in the cost, and there is a dislocation in time. Some previous capital expenditures are included in the current cost; current capital expenditures will be included in future costs. Last year, CNOOC’s cash flow was 147.89 billion, which was much higher than its net profit.

It is different from real estate companies; after housing companies sell houses, in order to maintain continuous production, they have to buy land at higher prices; but CNOOC’s exploration and development costs have not increased, and the increase in expenditures is due to the increase in volume, not the amount. The price increase is a manifestation of growth.

5. Is low PE reliable? COSCO SHIPPING Holdings has not fallen from 3PE last year to 2PE now.

Answer: COSCO SHIPPING Holdings, container transportation, has a high cycle. After the sharp rise last year, the PE dropped to 3. The prosperity is likely to decline slowly in the next few years instead of a cliff, and in the next two or three years, it will earn more money than the market value. Can you buy it? Not necessarily, it depends on the dividend . The dividend distribution of Haikong in April was seriously lower than expected, and the dividend payout ratio was also very low. From last year’s highest point of 25 yuan to 13 yuan, it was almost cut in half, and the big V suffered a loss from worry and effort.

6. Dividends must be ex-righted, the money is only from the left pocket to the right, and the dividend tax must be paid. The higher the dividend, the more deductions, which is boring.

A: Can the dividends and ex-rights be divided until the stock price is negative? impossible. That is to say, for long-term stable and high dividend stocks, it is inevitable to fill in the right. Even if the right cannot be filled completely, most of the rights can be filled.

Maybe you don’t like to eat eggs and just want to make the difference between buying and selling hens. In this case, laying eggs is also very important. Egg laying proves the health and value of hens, so they can sell for a good price, because many people like hens rather than iron roosters.

7. I am very afraid of cyclical stocks. I lost a lot in cyclical stocks before, and I am afraid.

A: If you want to choose a son-in-law, there is a young talent whose annual income is very unstable. When the industry is booming, he earns more than 7 million yuan per year, and when the industry is at a low point, he only earns more than 60,000 yuan. In the past 12 years, he has earned an average annual income of 4.66 million yuan. Work very hard, have enough savings, have a good family background, have a good character, and make money and give it to you. Would you like to think about it? Do you think he made too little money that year?

In the past 12 years, after two oil price troughs, CNOOC has achieved no annual loss (even if it is smooth), with an average annual profit of 46.6 billion RMB and a dividend payout ratio of about 50%. With growth potential, good financial status, state-owned enterprise background, high dividend.

When the oil price plummeted in 2020, CNOOC still had a net profit of 25 billion attributable to the parent. Since it cannot lose money at the bottom of the cycle, it is the icing on the cake when the cycle is booming.

8. Cyclical stocks should be bought when PE is high or even at a loss. Now CNOOC’s PE is very low, and it should be sold at the top of the cycle.

Answer: ① This kind of view is similar to that when it goes up, it is considered to be the top, and when it falls, it is considered to be the bottom. Now CNOOC’s PE is very low. If the stock price remains unchanged, how do you know if its PE will be lower in the future due to the rise in performance?

At $110 oil, are you worried that it will fall, but you are not worried that it will rise? See the peaking signal? Excluding the pulse price of $139 on March 7 due to an emergency, the general trend of crude oil prices is upward, so you can guess the top? Guess the top at every turn, and it is easy to miss the big bull stocks.

In fact, there is no need for oil prices to rise. As long as the current price is around $110 for two or three years, CNOOC can make a lot of money. Even if the oil price falls to $70, the dynamic 5PE is still obviously undervalued. As for the surge in crude oil, it was a pleasant surprise.

International oil price is the most critical parameter of CNOOC’s performance. For details, see Question 11.

② “Cyclical stocks should be sold when PE is low”, which applies to the following example: a stock with a loss or 300PE, due to the growth of the cyclical prosperity, after the stock price rose sharply, the PE dropped to 10, but the prosperity was unsustainable, this is the selling point rather than buy some.

If the PE is so low that dividends can be paid back soon, that’s another story . CNOOC Hong Kong stocks, it is now the end of June, considering the mid-year dividend of about 0.8 yuan, (9.86-0.8) × 0.85 × 477 ÷ (750 × 2) = 2.45, about 2.5 times the dynamic PE; According to the current oil price, the company will earn supermarkets in 3 years Value, about 6 years to pay dividends. It is conservatively estimated that oil prices fall to $70, which is the dynamic 5PE. In addition, the company has a certain growth potential, and it can also make a lot of money at the bottom of the cycle, so why worry?

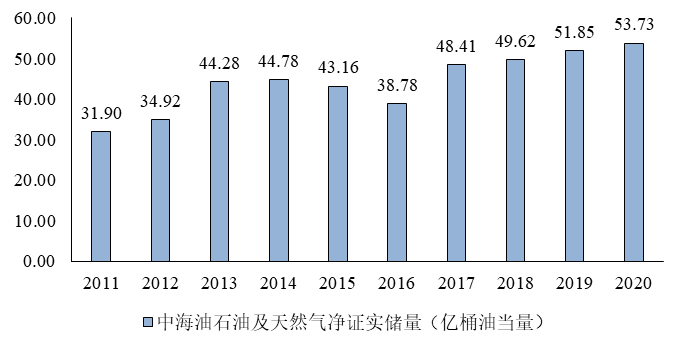

9. CNOOC only has about 10 years of proven reserves, and the oil is exhausted. What will happen in the future?

A: As shown in the figure, the proven reserves of CNOOC in recent years have an obvious upward trend. There are still many oil and gas resources to be explored in the South China Sea.

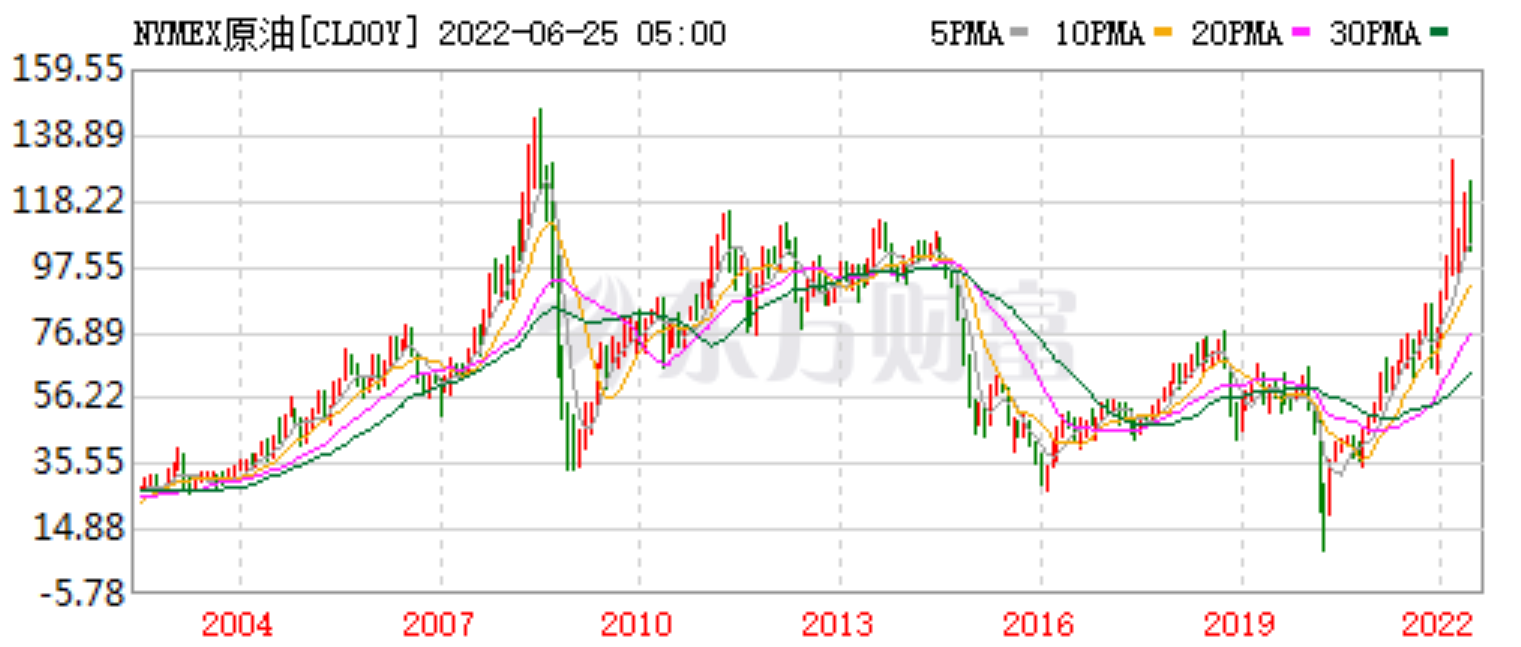

10. The US dollar raises interest rates, which is bad for commodities, dare to buy oil?

A: Interest rate hikes are bad for commodities, which means that interest rate hikes inhibit investment and demand, thereby causing commodity prices to fall. However, from the historical data, the 2004-2006, 2016-2019 interest rate hike cycle, oil prices rose. Check out the two pictures below.

11. The price of crude oil is too difficult to predict. I don’t know the rise or fall of tomorrow. How dare I buy oil stocks.

A: The medium and long term are usually easier to predict than the short term . There are many such examples in reality. For example, I don’t know whether stockholders will eat meat or noodles tomorrow, but I believe stockholders can make money in the medium and long term. For example, I don’t know if the temperature will rise or fall tomorrow, but I know that in 6 months, the local temperature will be cooler than it is now.

Short-term oil prices, affected by emergencies, are extremely difficult to predict; however, medium-term time scales of two to three years are easier to predict.

Price depends on supply and demand. The lower supply in the next two or three years is a foregone conclusion, because the capital investment in global oil and gas exploration and development was relatively low in the past few years, and now it will take a few years to produce output (different mines take different time, shale The oil output is fast, it may only take a few months, but the decay is also fast; and the cycle of offshore oil fields is very long. @Run brother has a lot of research on cyclical stocks, especially mineral resources stocks.) And what about demand? Everyone just guesses that it will decline, it doesn’t necessarily happen, and even if it does, the weakening of demand is not necessarily more serious than the weakening of supply. And fear of recession will also affect investment in oil and gas exploration and development.

In the long run, technological progress will not be worth the exhaustion of resources, money printing inflation will push up commodity prices, and the price center of crude oil will increase. In addition, carbon neutrality and carbon peaking will also push up the price of fossil energy.

Many people are worried about the two big pits in oil prices in 2016 and 2020. In 2016, mainly because of technological breakthroughs, hydraulic fracturing technology has greatly reduced the cost of shale oil production and the supply is sufficient. However, hydraulic fracturing technology has great damage to the environment and has been banned by many countries. In 2020, it was mainly the epidemic that affected demand. Neither event was easy to happen.

What if it happened? In 2020, in the negative oil price event, the average annual price of oil distribution is about 40 US dollars, and the net profit of CNOOC is 25 billion RMB. CNOOC’s oil production cost is slightly less than 30 US dollars, which is very low in the world, and it is not afraid of falling oil prices.

12. CNOOC has gone up a lot this year and doesn’t want to carry a sedan chair for others. I heard that the big gold chain recently supported oil stocks.

A: CNOOC Hong Kong stocks have risen 44% so far this year, which seems high, but is seriously lower than that of foreign oil stocks.

@Master Lianghongliang is not a consistent price investment, but a slippery head (note, this is a compliment), sometimes speculating, sometimes investing, and requires high ability. He recently supported CNOOC, and many stockholders don’t know whether he is a price bet or a slicker at this time. For fear that he will sell while blowing the vote, they will not dare to buy or run first as a respect.

If you want to copy your homework, look at Buffett . He bought a heavy position in Chevron, an oil stock; he also bought Occidental Oil, and continued to increase his position in the past few days. CNOOC’s asset quality and valuation are significantly better than Occidental Oil; Buffett can’t buy CNOOC due to control, but we can refer to his views on oil prices.

13. CNOOC makes so much money, will there be any company to grab its business in the future?

Answer: An excerpt from Encyclopedia: “On January 30, 1982, the State Council promulgated the “Regulations of the People’s Republic of China on Foreign Cooperation in the Exploitation of Offshore Petroleum Resources”, decided to establish China National Offshore Oil Corporation, and authorized the China National Offshore Oil Corporation in the form of legislation to operate in China. It has the exclusive right to carry out oil exploration, development, production and sales in the foreign cooperation sea area, and is fully responsible for the foreign cooperation in the exploitation of offshore oil resources.” (Here I am talking about a group company, not a listed company).

Since it has a franchise and is a state-owned enterprise, no one can take away the business of CNOOC; there will be no competition like Pinduoduo taking Alibaba’s business or Meituan taking Didi’s business.

14. CNOOC Port A shares are twice as expensive as Hong Kong shares, and the new shares are terrible.

A: I personally think that the current price of CNOOC’s A shares is normally undervalued, while the Hong Kong stock market is seriously undervalued. The share capital of CNOOC A-shares is only 3 billion shares, and the outstanding shares account for about half. It is a small-cap new stock and is easy to be fried; The transaction of CNOOC A shares is a natural occurrence, and the price is relatively close to the value, while the transaction of CNOOC Hong Kong shares has been artificially and rudely interfered, and the value and price are far worse. Imagine that the players are playing a football game in HK, but the football referee far away in North America blows the whistle and sends the player off. Do you think the result of the game is reasonable?

15. Since CNOOC is so good, why is no one willing to buy it? If there was gold on the ground, it would have been picked up long ago.

Answer: This analogy is not appropriate.

If there was only a piece of golden gold on the ground, of course it would have been picked up long ago; even a golden copper block would be picked up, and bent over to pick it up at almost zero cost.

However, thousands of stocks in the stock market are equivalent to thousands of black things on the ground, which may be dusty gold, copper, or clay. If you want to pick up gold, you must first notice it, and then bend over to measure and identify it. It costs time and cannot be picked up in vain. It costs a certain price to buy.

In the investor interaction, we saw, “Hello, as of March 31, the company has not yet been listed on the A-share market, and there are a total of 1,565 ordinary shareholders of Hong Kong stocks.” The number of shareholders of CNOOC Hong Kong stocks is surprisingly small! It is estimated that the Shenzhen-Hong Kong Stock Connect and the Shanghai-Hong Kong Stock Connect are only one shareholder each.

@dog not call the rich man only buys seriously undervalued stocks, and he also likes it. @yulinzizhou focuses on the research of individual stocks, and the microscopic research on Shaanxi Coal Industry has reached an astonishing level. I look forward to his in-depth research on CNOOC! @星dustabc , the two little Vs of Carr and sister , follow this ticket very seriously.

This is the third time in 6 years that I have written a long article to blow the bill. The first two times were Gree Electric Appliances in 2017 and China Shenhua in early 2021. Both of them have performed well since then; I hope this time too. For the first two tickets, I didn’t get enough gains because of my tossing. Now write a long article to organize ideas and absorb different opinions. If no obvious problems are found, you can increase your confidence in holding shares and strive for enough gains.

This article is not intended as investment advice . This article wants to be as objective as possible, but due to heavy positions, it is inevitable that there is a tendency, please correct me!

Interests: I hold a heavy position in CNOOC, and there may be a transaction within 3 days.

@Today’s topic

This topic has 25 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/6700029114/223623956

This site is for inclusion only, and the copyright belongs to the original author.