My core point of view is that the strategy in the first half of 2023 will continue to be the same as in 22, try to keep short positions and reverse repurchase, and wait for opportunities. In the second half of the year, Q3 began to observe whether the market showed signs of bottoming out at a large level. At the latest in Q4, I personally think that the market may really bottom out for the first time. Of course, after bottoming out, it does not mean that the bull market is coming, but it will take a long time to bottom out. time.

Many of the following are some opinions of this year. They are just summed up. They can be regarded as personal notes, and they can also be regarded as a kind of sharing.

1. The underlying logic of A shares

First of all, if you want to survive in A-shares, you must understand the underlying logic of A-shares. If you don’t know how to adapt to US stocks, I’m sorry, I’m not acclimatized.

A-shares are essentially a financing market (look at new shares, convertible bonds, fixed increase and reduction of real estate holdings), and retail investors are at the bottom of the food chain, and in the long run they are paying for the market.

If you want to have a high-certainty opportunity to buy at a low price and make a lot of money, you have to wait until the financing starts to be very difficult, and even if you don’t start the market, you will have problems (think about the starting point of this round of structural bulls at the end of 18, when there were trillions of pledged disks? Situation) is the best time to draw your sword out of its sheath.

Because at this time, your interests are consistent with the overall interests of the A-share market. At other times, the interest of the market is financing, and your interest is to make money, which is inherently contradictory. Otherwise, who will pay for it? Intervening in the market at an inappropriate time, telling yourself a big narrative, and then calling for a big bull market after watching the bull market is just making trouble with the account and constantly internalizing yourself.

As reflected in the current market, economic pressure is high, and performance in all sectors will be under pressure (especially the real estate chain will feel colder next year), and the company is still short of money.

Then, as a financing market, A-shares will draw a lot of liquidity as long as they can still raise funds to support the economy (look at the number of new shares and convertible bonds this year). Moreover, listed companies have financial difficulties, and they will also find ways to refinance, and reduce holdings to cash out funds (see the recent fixed increase and reduction of holdings, which are the same as snowflakes).

Moreover, real estate also needs money to solve debt problems, and the bond financing market also needs money (didn’t you find it seesaw with the fluctuations in the bond market this year?), and money is everywhere, so how can the stock market go up?

So you have to wait, not until these companies don’t want to raise money to collect money, but when new shares and new debts break, and whoever decides to increase the allotment will plummet, and even the repurchase market will not buy it. When you solve these problems, you get a free ride.

2. The triple bottom of the market

The underlying logic mentioned above is deduced to the market, which is the triple bottom of the market, bottom of valuation -> bottom of policy -> bottom of market.

Let’s talk about the bottom of the valuation first. When the market value returns, it will be the first to appear. Both PE and PB have fallen to a reasonable or even underestimated range. Hundred-yuan stocks are rare, and the leading consumer stocks are only 20 PE. Many stocks have good performance, but their net assets are discounted by 50%, and convertible bonds are broken when they come up. More than 100 is a luxury, and the market value is obviously underestimated.

And is there a valuation bottom now? Just look at the two phenomenon-level weight varieties of structural bulls, Maotai and Ningwang, which represent the ceiling of consumer blue chips and the ceiling of technology growth stocks respectively.

And Moutai is now only a week away from a positive stock price, but the current valuation is actually twice as high as the normal valuation range of consumer stocks, even according to the PEG valuation of growth stocks, it is twice as high.

The valuation of the battle group of consumer stocks is as follows, is it cheap? From any angle, it is obviously expensive.

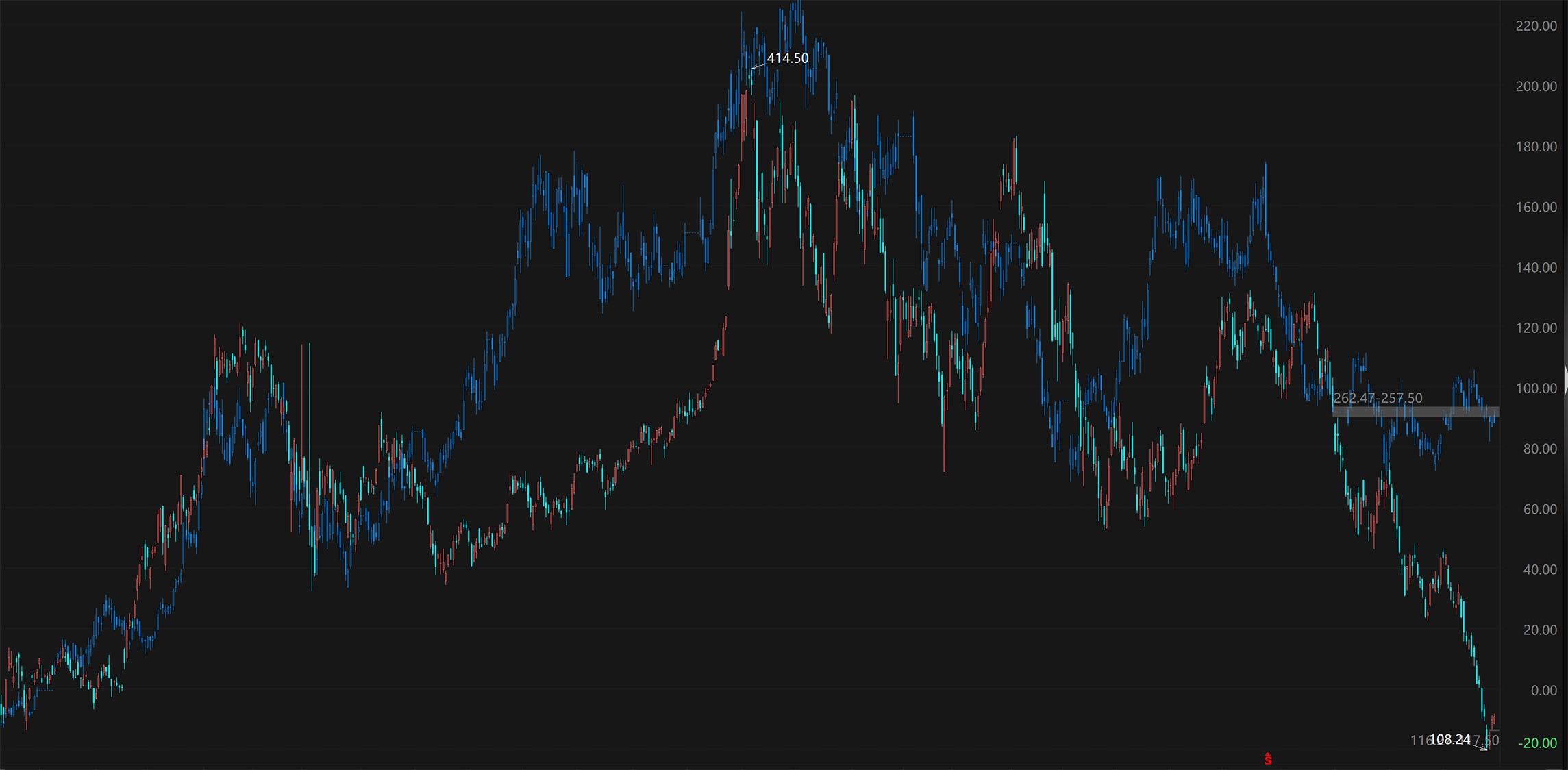

As for King Ning, Tesla, which is on the outside market, is strongly related in all aspects (the K line in the picture below). Recently, the track funds are dead, so there is no strong correlation.

After reading Moutai and King Ning, you will find an obvious problem in the market. These two varieties have actually been holding on. What will happen if Moutai falls on the main board next year? If King Ning falls, what will happen to the GEM? There are no eggs under the overturned nest of the market.

Moreover, in order for the A-share market to achieve a bear-bull cycle transition, it is generally the leading sector in the previous wave of the market that has fallen, and then the market finds a new medium-to-long-term high boom that can lead the sector to rise.

This is easy to understand. The new main funds need to start anew. They will not take over the old leading plate from the previous wave, and will even take advantage of the decline of the old leading plate to hit the index to build positions at low prices.

For example, look at the market in these years. From 2006 to 2007, it was a blue chip cycle. Chinalco, PetroChina, which was listed for 48 yuan, and Yunnan Copper, which was 100 yuan, were all products of that wave. After that, they never reached their previous heights.

In 2013-15, it switched to the small and medium-sized products and the varieties with the Chinese prefix. The two phenomenal varieties are LeTV and CRRC. The result is that the LeTV code is gone. CRRC’s 15-year maximum was 39 yuan, and now there are only 5 yuan left.

In the past three years, the leading breeds with super large market value of structural cattle are Moutai and Ningwang. Let’s look at the position and valuation that are still high. It means that the main capital of the next wave of market needs to find another type, and even use these two types to suppress the points of the main board and the gem, so as to open up space for opening positions at low positions.

After talking about the low valuation, let’s talk about the policy bottom. Generally, when the policy bottoms out, systemic risks such as pledge orders and financing orders will appear when the market falls again. The management will continue to call out to protect the market, and financing will also start to be greatly reduced. You will see it when it appears.

As for the accelerated new shares and new debts, real estate has come to refinance, is there a policy bottom? The market rise is piled up with money. Moreover, if the stock market soars, it will cause a strong liquidity siphon. How do you let the real estate and bond markets, which are also waiting for capital inflows, deal with themselves?

As for the A-shares that many people struggle with, the 3,000 points are really meaningless. The total market value of the market is shown in the figure below. The current market value is 78 trillion, and it was also at this point in June 2018, with a total market value of more than 50 trillion.

A-shares don’t seem to grow taller, but they actually gained a lot of weight, and the extra “fat” needs to be maintained by incremental fluidity. If the fluidity cannot be achieved, then I’m sorry and can only “lose weight”.

Of course, the anchor point of 3000 points also pitted a group of bottom-hunters. They thought that 3000 points were low. In fact, the current 3200 points are equivalent to the market level of around 3600-3800 points in 2015, and even the high point at the beginning of this year has reached 15. The water level is around 4500 points a year!

Why do you say that, just look at the average stock price. The average stock price at the bottom of the two bear markets in 2014 and 18 was around 10 yuan, and now it is still 22 yuan. Compare it horizontally with the past.

It should also be said that the general policy bottom is a low level, not a low point, and the market will still decline inertially, and the range may be quite large.

The last thing I want to talk about is the bottom of the market. The bottom of the market is the “true” bottom. The market has gone through a stage of ignoring the bottom of the valuation and the bottom of the policy and still falling emotionally. The market has finally become numb.

At this stage, you will see that the index has stopped falling, individual stocks have negative performance but opened lower and higher, and the bull-bear cycle of the brokerage market is expected to show signs of explosive volume, stop falling and strengthen, and the market will usher in a reversal.

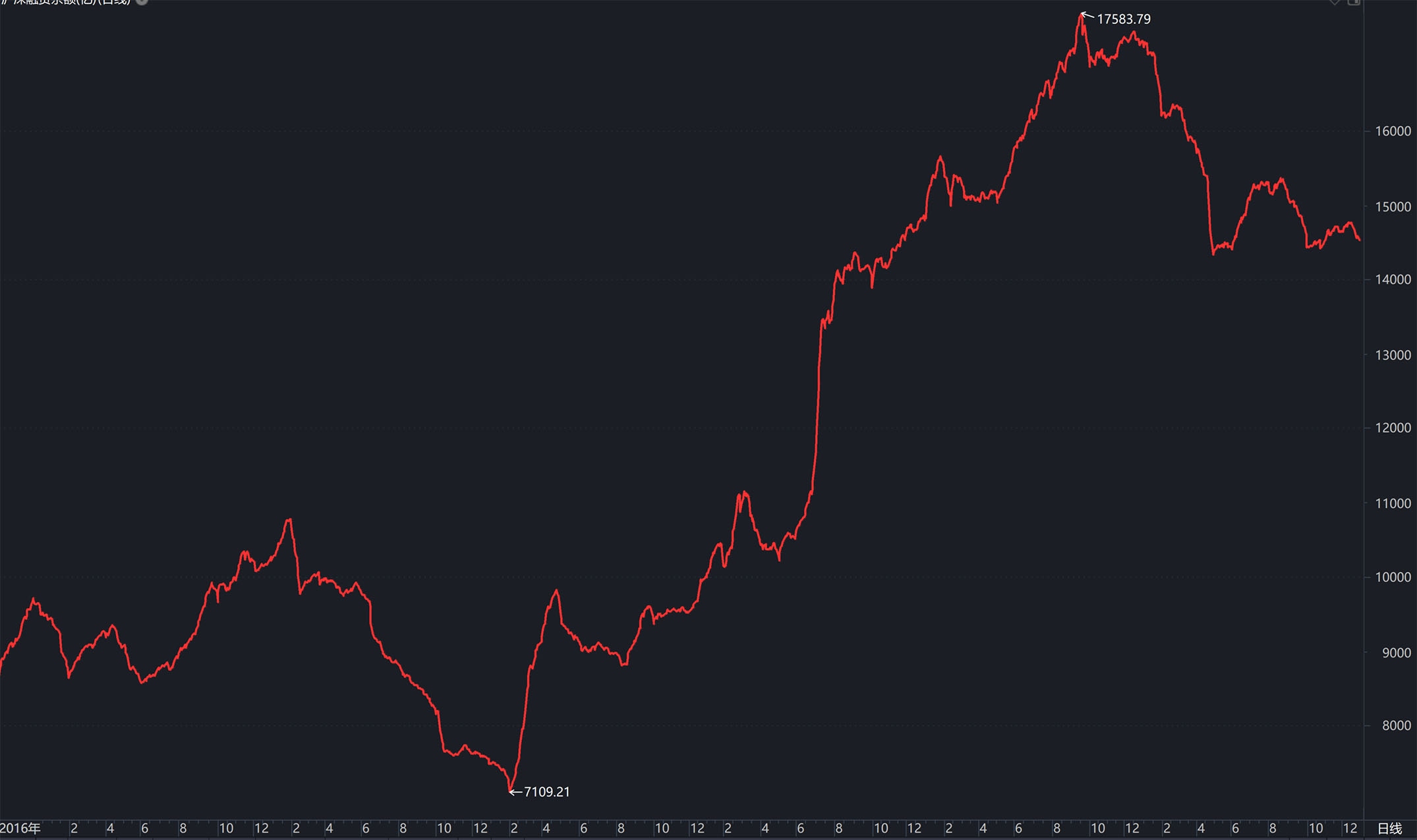

As for the bottom of the market, there are a lot of people shouting “big bull market” after a few days of rising. The financing balance in the figure below is still 1.45 trillion, and it was only 700 billion at the bottom of 18 years. Obviously, the leveraged funds with the highest risk appetite are still very optimistic.

3. External disk

The external market is a big variable, and I don’t know what the basis is for those who say that the A-share market trend is independent. In fact, due to the large amount of northbound funds, the correlation between A-shares and the external market is very high.

For example, in the picture below, CSI 500 vs S&P (blue K line)

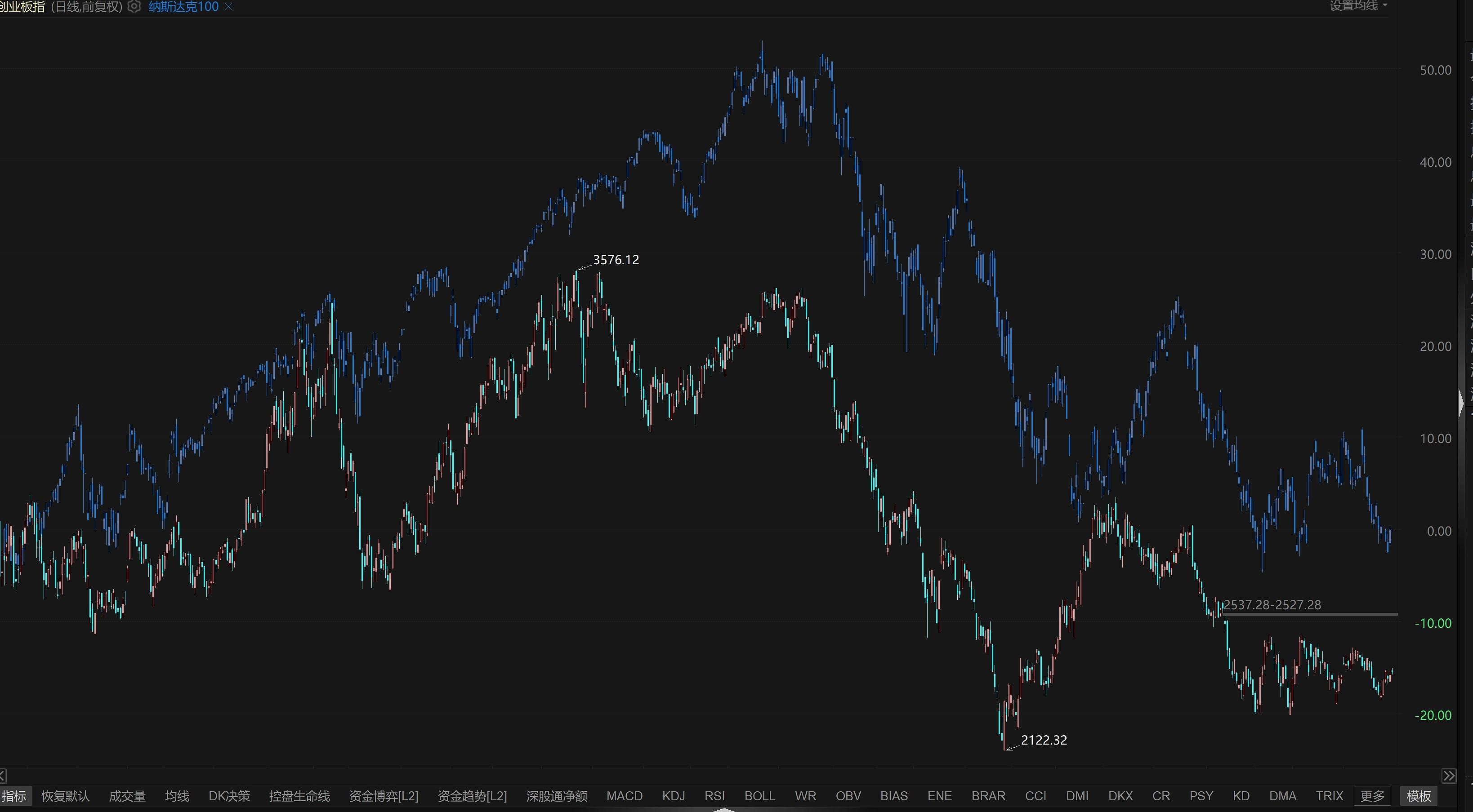

For another example, the GEM is benchmarked against Nasdaq (blue K line)

In fact, the outer disk is not optimistic about the market cycle now.

It is the dollar tide cycle that dominates the trend of the external market, and it generally goes through three stages.

Gradually raising interest rates to a high level this year, the corresponding stage is that high yields will kill valuations, and assets that rely on high liquidity and cheap capital costs will be disabled first, so the intensity of this year’s decline is the pure liquidity speculation of big pies Assets >> Nasdaq Growth Stocks >> Dow Value Stocks.

The second stage is when the market comes back to life. I feel that the interest rate has seen the ceiling and is about to “reverse”. It is time to buy the bottom, and the big bull market is back. But in fact, raising interest rates is just an appetizer. What really kills is that interest rates continue to run at high levels.

Afterwards, what awaits them is the third stage of trading recession, which is actually the Davis double kill of liquidity premium and fundamentals. The performance of the market is a “black swan”. The main decline will kill the company’s fundamentals. Even if the Fed turns around, the liquidity will not be able to hedge against the decline, and we need to wait for the market to stop by itself.

In other words, it is likely to enter the third stage next year. Even when the Fed cuts interest rates, the market will accelerate to catch up to the bottom for a long time in experience.

The reason for talking about the external market is that, do you think that if the external market falls sharply next year due to the recession, will it be transmitted to A shares through the 50 track? Of course, unless the intensity of the external market is too high, there will often be a certain lag in the time dimension.

Of course, it is not all pessimistic about the external market. In the second half of next year, especially after Q3, the Federal Reserve may turn around, and at the same time, the active destocking cycle of the semiconductor technology industry will bottom out. That means that the external market is likely to bottom out at that time position, both liquidity and fundamentals.

Finally, let me say a few words of truth, whether it is an institution or an individual, in fact, the opinions are “worthless” to the market, including this article of mine, which is just a deduction of experience.

As the weakest in the market, retail investors want to survive and make profits not because they can predict the market logically and self-consistently. The biggest competitive advantage is that they can bear it, while institutions naturally cannot bear it.

What does this mean? No matter how high and uncertain the environment is, even if there are few losses, institutions must relatively beat the market. For example, if 300 falls by 20%, they will beat the market if they lose 15%. Look at this year, is it so?

And this is obviously meaningless to you, because you come to the market to make money, not to find a way to hold a high position and hold a relatively small loss. The only way to survive in the long run is to hold back, keep your principal, and wait for the market to tell you that it is the bottom.

There are 8 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/9222280625/238973325

This site is only for collection, and the copyright belongs to the original author.