To study the development history and success factors of a company, it must be combined with the background of the times, because companies standing on the top of the tide are often the product of the combination of their own advantages and the characteristics of the times. If the market is not what it used to be, then even learning the company’s successful strategy will never replicate its success.

This year, I spent a little time examining the path to success for BlackRock, the world’s largest asset manager. First of all, I would like to state that this research has not been approved by BlackRock. The motive is purely to satisfy curiosity.

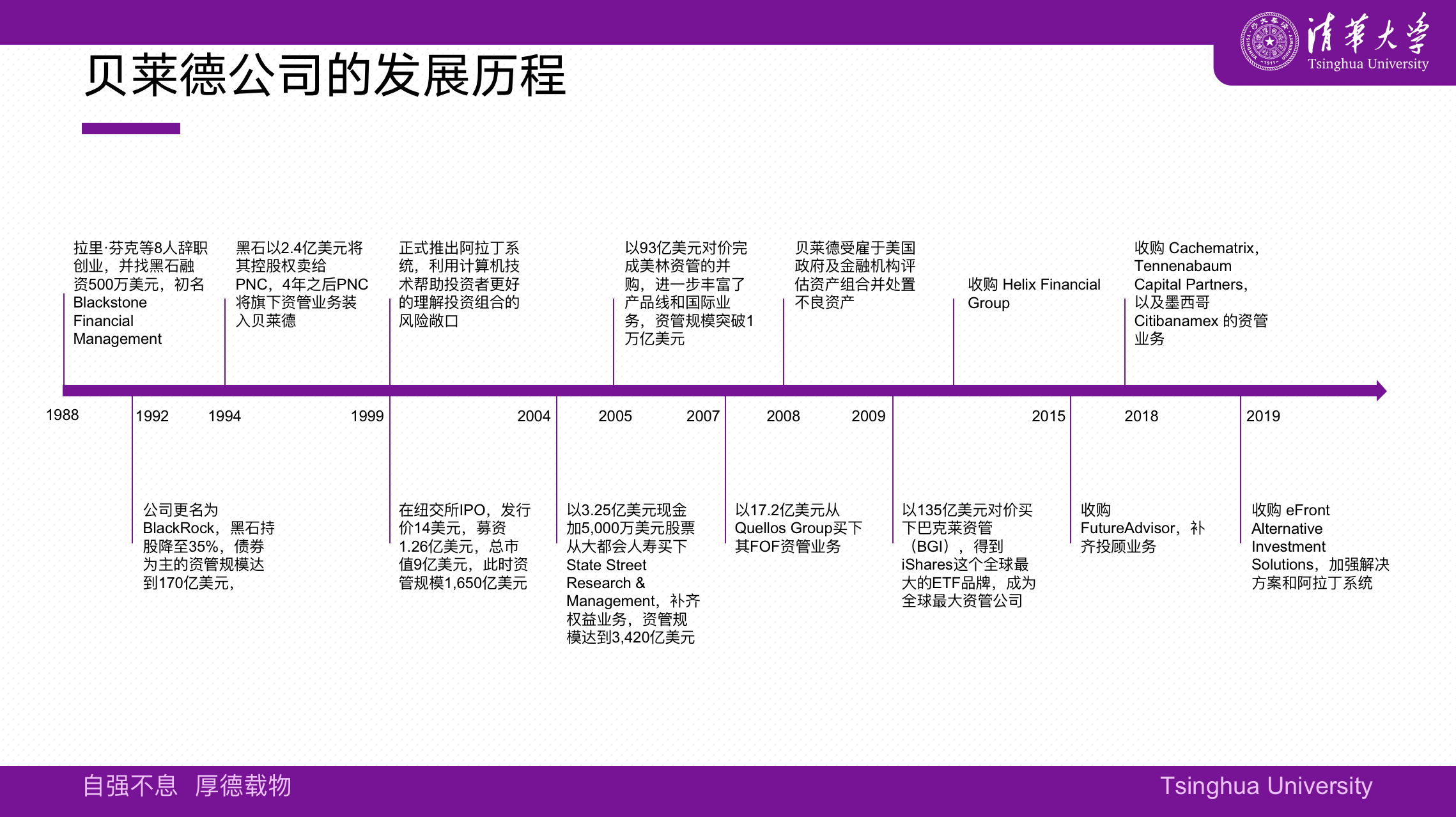

Founded in 1988, BlackRock started at least half a century behind its main rival. How BlackRock became the world’s largest fund company by asset management in only 30 years is a common narrative in the market that its dominance comes from mergers and acquisitions. In fact, this is an oversimplified narrative. It must have done something right, I thought, and that was the original origin of the thought.

BlackRock is primarily run by Laurence Fink, often nicknamed Larry Fink. To this day, he remains at the helm of the industry giant as chairman and CEO. Fink was born in California in 1952 to a Jewish family. His father owned a shoe store and his mother was an English literature professor. He holds an undergraduate degree in Political Science and an MBA in Real Estate from the University of California, Berkeley (UCB).

It is said that the company that Fink, who graduated with a master’s degree, most wanted to go to was Goldman Sachs, but his interview was ruined by him. With his knowledge of real estate and business, Fink played an important role in the process of US Mortgage Loan Securitization (MBS), rising through the ranks, becoming the head of the bond department of First Boston in less than ten years, And sit on the company’s executive committee.

There is an old saying in China, “Fortune depends on misfortune, and misfortune falls under misfortune.” The young and promising Funk was proud of his spring, but he was overconfident in 1986 when he misjudged the trend of interest rates, and the superimposed hedging tool failed. This is the first Boston brought in as much as $100 million in damages, and he was fired for it. However, this is not all bad. First of all, this gave Funk the opportunity to start his own business, and secondly, he put risk control in a very important position at the beginning of his business.

Fink had frequent conversations with Ralph Schlosstein of Shearson Lehman Hutton while he was still working in First Boston, and since both were accustomed to getting up early People, often call each other around 6:30 in the morning to chat about the recent financial markets before the market opens.

It is said that one night in March 1987, they happened to book the same flight from Washington to New York and had dinner together upon arrival. It was during dinner that they began to outline plans for a company that would reshape financial securities, aggregate them into a portfolio, and better analyze all the risks they contained.

Fink then invited a small group of his most admired “fellow people” to his house to discuss the idea for the new company, among them Robert S. Kapito of First Boston, Fink’s mortgage-trading desk at the time. The right-hand man, Barbara Novick is a very senior portfolio product executive, Ben Golub is a math whiz who has designed risk management tools for many banks, Keith Keith Anderson is First Boston’s top bond analyst.

Schlossstein brought Susan Wagner from Shelson, Lehman & Hatton, and later Hugh Frater, both experienced mortgage lenders. Bond specialists determined to form a new bond investment firm based on modern technology and more robust risk management.

This is the origin of BlackRock, four of whom are still in service with BlackRock today, including Fink’s closest assistant, Robert S. Kapito, who has long served as the company’s president.

Throughout the history of BlackRock’s later development, it is inseparable from Larry Fink’s real talent, foresight, and strategizing, but it is also inseparable from the several paradigm shifts that pushed it to the top of the wave (paradigm shift). , which is an external factor that we must pay attention to when analyzing BlackRock’s competitive strategy. That said, BlackRock’s success strategy won’t help other emerging asset managers succeed if they’re out of a similar environment.

Fink approached Pete Peterson of The Blackstone Group when he was raising capital. Peterson and another Blackstone co-founder, Stephen Schwarzman, admired Fink’s work in mortgage securitization. Talent, invested $5 million in it in exchange for 50% of the equity, and put the company they founded under the banner of Blackstone, which was originally called “Blackstone Financial Management”. The money invested in the project also provides services for institutional clients with similar needs. Soon they raised their first fund called Blackstone Term Trust, raising $1 billion.

The start of the business was smooth sailing, and within a few months, Fink and his team were already profitable. Just a year later, they had $2.7 billion in assets under management, which was rocket-speed at the time. In order to retain core entrepreneurial partners, Fink granted the team equity as an incentive, which also led to the dilution of Blackstone’s shares in it to 40%.

Here we must first mention the first wave of the era that propelled BlackRock, that is, its creation coincided with the booming U.S. bond market, and Fink and his team are the people who understand bonds best .

There were also several reasons behind the rise of the bond market at that time. First, during Paul Volcker’s tenure as Federal Reserve Chairman, he kept raising interest rates in order to curb inflation, which kept US interest rates at a very high level, up to 15%. The risk-free interest rate level is difficult to obtain stably in the equity market, so a large amount of funds are turned to the bond market.

The second was the rise of leveraged buyouts at the time. In the 1980s, there were more than 2,000 LBO cases in the United States, with a transaction value of $250 billion. The second reason for the booming bond market is that a large number of companies issue “junk bonds” (also known as high-yield bonds) with super high interest rates to raise funds for mergers and acquisitions.

Third, fixed-income products including mortgage loan securitization (MBS), asset securitization (ABS), credit default swaps (CDS) and other fixed-income products continued to innovate, and a large amount of funds poured into the fixed-income market.

The company’s external environment is developing in the direction of the company’s expertise, which was the most important factor in BlackRock’s early success. Fink, himself a top expert on mortgage securitization, made more than $1 billion for First Boston over a period of several years as a trader and later bond chief. The colleagues he selected to start a business together are also leaders in the bond field. Coupled with the lessons he learned from the huge losses caused by improper risk management, they stand out in the fixed income field.

In 1992, the company officially changed its name to BlackRock (BlackRock), which literally translates to “Black Rock”, meaning that it is in the same vein as Blackstone. At this time, BlackRock’s asset management scale has reached 17 billion US dollars, and Blackstone’s shareholding has been reduced to 35%.

The second wave of the era that propels BlackRock forward is the surging mergers and acquisitions activities. The industry ecology is constantly concentrated in the frequent mergers and acquisitions integration, and BlackRock has also seized the opportunity to grow and develop . The first major merger transaction occurred in 1994, when Fink and Schwarzman had a disagreement over employee compensation and equity incentives. Fink wanted to transfer more equity to employees, but Schwarzman did not want to be diluted, and the conflict continued to intensify.

That year, Blackstone sold this mortgage securitization and bond-based business unit together with an external asset management scale of 23 billion US dollars to Pittsburgh’s PNC Financial Group at a price of 240 million US dollars. Fink then left Blackstone and served as the BlackRock Chairman and CEO of Financial Management Corporation.

PNC was formed by the merger of the Pittsburgh Trust and Savings Company, established in 1852, and the Provident National Corporation, established in 1865. It is currently the fifth largest bank in the United States and ranks among the world’s 500 largest banks. powerful. Through PNC’s nationwide distribution network, BlackRock’s asset management scale has expanded rapidly, reaching $53 billion at the end of the year.

Four years after BlackRock was sold to PNC, in 1998, PNC put all of its stock equity, cash management, and mutual fund businesses into BlackRock, making it a medium-sized asset management company. It is a key step in its leap-forward development through mergers and acquisitions.

As mentioned earlier, BlackRock has put risk management at its core from the very beginning, and this is the most important lesson Fink has learned in the first half of his life. The first decade of BlackRock’s business was also a decade of rapid development of computers and the Internet, so they began to study how to manage risks through increasing computing speed and constantly learning software algorithms very early on.

After several years of research and development and internal testing, the Aladdin system was finally officially launched in 1999. This is the most important factor for BlackRock on its way to the throne of the global asset management industry, and it is also the third wave of the times that coincides with the times. Because as structured financial products become more and more complex, the market needs modern risk management tools that can penetrate complex financial products.

The Aladdin system was developed under the leadership of BlackRock’s first employee and later co-president, Charles S. Hallac, named after Asset (asset), Liability (liability), Debt (debt), Derivative Investment Network (derivative investment network) Network), the first version of which was coded on a $20,000 Sun workstation between an office refrigerator and a coffee maker.

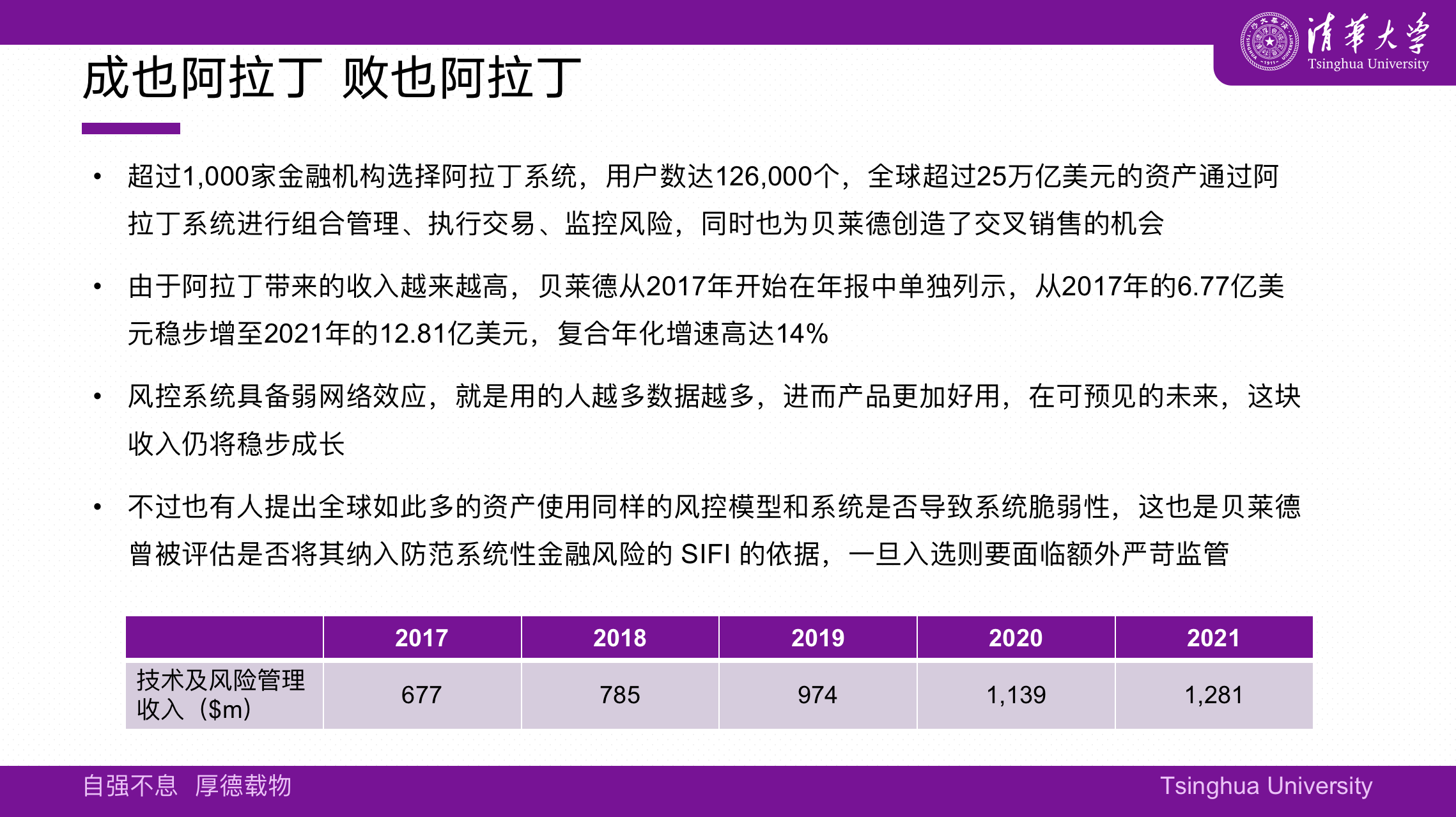

As a terminal operating system, the Aladdin system can make timely adjustments under different risk scenarios, helping investors better understand the risk exposure of the portfolio. The Aladdin system was very popular as soon as it was launched, and its functions continued to expand in the later period, becoming the most commonly used asset allocation tool for global capitalists. Currently, tens of trillions of dollars of funds are allocated, traded, monitored and reported through the Aladdin system.

The Aladdin system not only adds a stable cash flow for technology services to BlackRock’s asset management income, but also establishes the image of an expert in risk analysis, resolution, and control, attracting the attention of many financial institutions. later

At the same time, in 1999, another major event was the IPO of BlackRock. There are two main advantages of going public. One is that it can raise funds and open a channel for continuous fundraising if necessary; the other is to expand the company’s reputation and credibility. However, in Fink’s eyes at the time, BlackRock’s listing was a failure, because the underwriter Merrill Lynch valued BlackRock at a mere $900 million. He once considered giving up listing, but under pressure from multiple parties and comprehensive consideration, he went up.

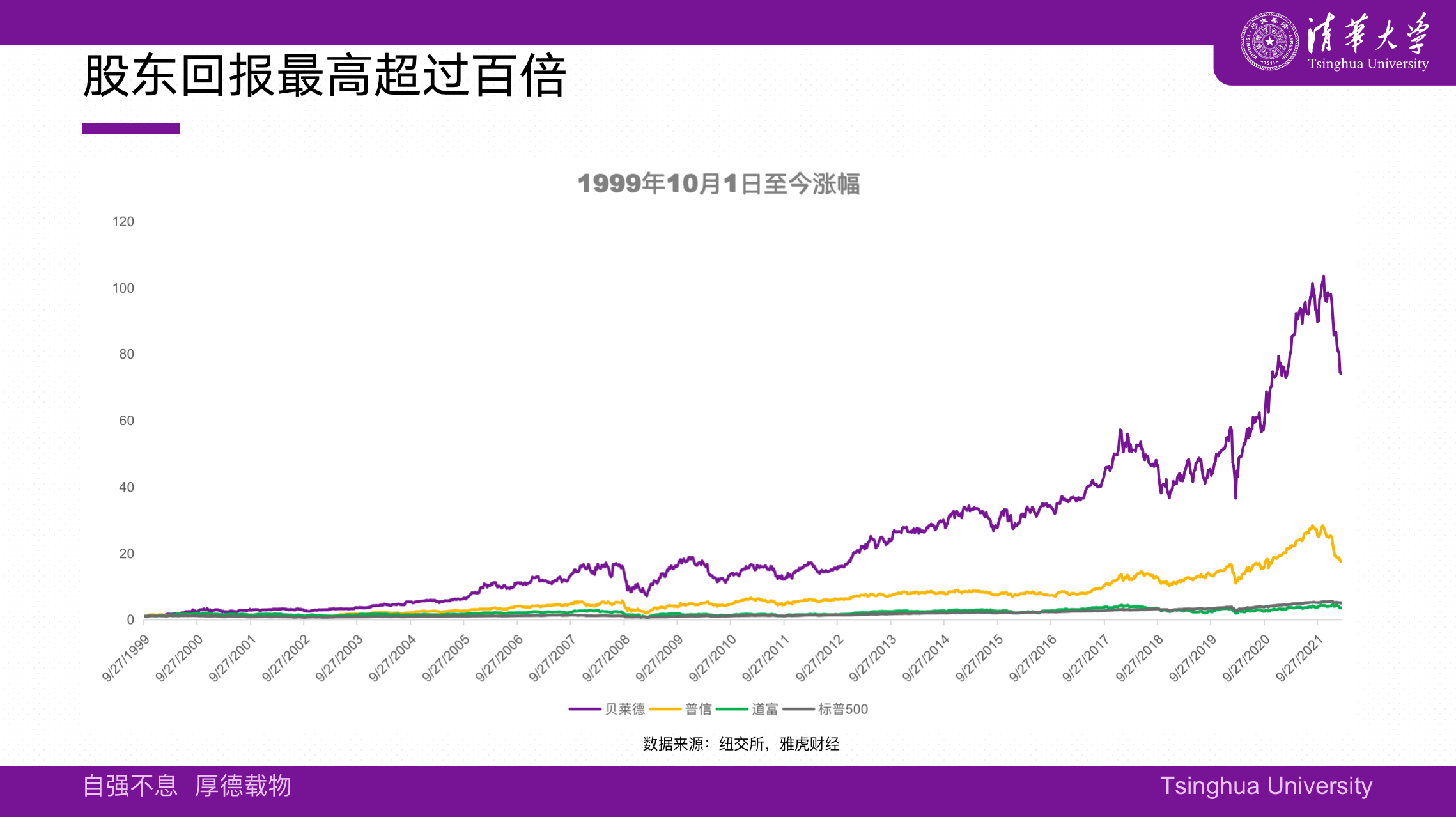

It was listed for trading on October 1, 1999, at an issue price of $14 per share, raising $126 million. In 2021, BlackRock’s stock price will rise to a maximum of $962, with a market value of more than $150 billion, a standard “hundred-fold”. Accompanying it is the growth of asset management scale. At the end of 1999, AUM was 165 billion US dollars, and by the end of 2021, AUM has exceeded 10 trillion US dollars.

From the perspective of hindsight, BlackRock is most fortunate to complete the listing and financing before the burst of the Internet bubble. The cash obtained from the financing and the ability to continue financing allow it to have the capital to make low-cost acquisitions in the crisis caused by the Internet bubble.

The first M&A transaction occurred in 2004, when it bought a mutual fund company called State Street Research & Management (SSRM) from MetLife for $325 million in cash and $50 million in stock , and changed its asset management products from the original bond-based to a two-wheel drive of stocks and bonds.

It is worth noting that the acquired party is not State Street Corporation, which invented ETFs and ranks fifth in asset management. After the merger, BlackRock had $342 billion in assets under management at the end of the year. Now its business is not only balanced, including stocks, bonds, cash management, and BlackRock solutions based on the Aladdin system, but it has grown to an upper-middle position in the United States, just 16 years after its founding. year.

The pace of mergers and acquisitions did not stop there. At that time, investment banks were divesting their asset management business. In 2005, Fink learned that Merrill Lynch CEO Stan O’Neill had the idea of selling his asset management business, so he invited him to have breakfast. In just 15 minutes, they had reached the terms of the deal and signed the menu receipt to witness this provisional agreement.

Before the financial crisis, Merrill Lynch was one of the five investment banks, and its asset management business (Merrill Lynch Investment Managers, MLIM) was huge, and the success or failure of this transaction will be the key to the success or failure of this transaction. Fortunately, Capito did an excellent job of completing the integration, which also laid a solid foundation for the next merger. The acquisition cost US$9.3 billion, but it gained Merrill Lynch Asset Management’s rich product line and international business. The total asset management scale exceeded US$1 trillion. At the same time, Merrill Lynch became the major shareholder holding 49.5% of BlackRock’s shares.

In 2007, BlackRock acquired the asset management business of Quellos Group, a Seattle-based investment bank, for $1.72 billion. Capital Management is known for its Fund of Funds (FOF) business, and it is a Funds-of-Hedge-Funds business with a combined size of $20 billion.

In 2008, the world fell into a financial crisis caused by subprime mortgages. Although BlackRock was also an investor in MBS, it did not get burned due to accurate risk control. Crisis is a crisis, and there is opportunity in crisis. This financial crisis is a great development opportunity for BlackRock. Because Larry Fink is famous as early as 1994 for helping General Electric (GE) value the complex financial assets of its acquisition of veteran investment bank Kidder Peabody, and he and his team’s ability to see through the bulls in the past In the past ten years, it has continued to improve, and now it has a greater scope of use.

At the time, everything from investment banks on Wall Street to central banks and even the U.S. government itself was scrambling to find experts to analyze the toxic securities that nearly crashed the entire system. The first case they received about the subprime mortgage crisis was the Florida government, when they held a lot of MBS bonds issued by Lehman Brothers, and BlackRock’s “financial special forces” quickly helped customers complete asset analysis and dispose of non-performing assets.

Since then, more and more businesses have actively called BlackRock. JPMorgan Chase hired BlackRock to evaluate Bear Stearns’ balance sheet to determine the acquisition offer; AIG hired BlackRock to save itself, although the US government later After taking over, BlackRock directly liquidated assets of nearly 10 billion US dollars without comparing prices through bidding; Bank of Tokyo-Mitsubishi UFJ hired BlackRock to conduct risk analysis on the equity of Morgan Stanley to be acquired…

It is precisely because of his excellent risk control ability and deep knowledge reserve that the then US Secretary of the Treasury Paulson has repeatedly contacted Fink for help urgently. During this period, Fink offered the Aladdin system to the Treasury Department and the Federal Reserve to assist in measuring mortgages. Asset risk in the loan-backed securities market, and sovereign funds including Japan, Norway, and Singapore also sought Fink’s help and used the Aladdin system. Later, even big companies including Apple, Google, Microsoft, etc. used the Aladdin system to manage their large-scale funds and investment portfolios.

All in all, 2008 was a bad year for the world, but a good year for BlackRock. Next in 2009, BlackRock will usher in the most pivotal M&A transaction in its history. But before that, BlackRock acquired R3 Capital Management and secured its $1.5 billion fund, warming up for a bigger takeover.

During the financial crisis, Barclays bought a part of Lehman Brothers’ business. As a result, the deal almost brought down the old financial group, so they tried to raise funds to avoid the fate of being bailed out by the British government. One of the measures was to consider selling its capital. Managed business – Barclays Global Investor (BGI).

Barclays is said to have accepted a takeover offer from private equity firm CVC to sell BGI iShares, a rising ETF business, for $4.2 billion. But within the 45-day period to finalize the terms of the deal, BlackRock seized the opportunity to intercept and…

The Financial Times later reported that BlackRock president Capito approached Barclays president Bob Diamond to say that instead of selling iShares to CVC, he would sell the entire BGI to BlackRock in exchange for a large sum of money Funding and stock in the combined company. That would allow Barclays to get the money it needs without a bailout and still have an interest in the money management arm through its substantial ownership in BlackRock, which would transform into an investment giant.

Barclays quickly reached an agreement with BlackRock, and finally completed the transaction at a consideration of $13.5 billion. After the transaction was completed, Barclays held a 20% stake in BlackRock. This was the largest merger and acquisition in the asset management industry at the time, and BlackRock became the largest fund company in the world in terms of asset management, with operations in 24 countries and regions around the world.

The most valuable part of this deal is that the original good at active management and the newly replenished passive investment fully expand the company’s product and service array. Index investment itself is not difficult, but profit requires scale, and Barclays’ iShares is the world’s largest ETF brand, and the scale of index investment is also one of the largest in the world. It can be said that BlackRock’s global dominance was completed in 2009. And it must be pointed out that the decade of passive investing and ETFs has begun, and this is the fourth major wave of the era on the road to BlackRock’s success .

For the integration after mergers and acquisitions, BlackRock has always adhered to a belief that it requires the entire company, including the merged enterprise, to use a set of information systems. It is a very huge project to switch the IT system of BGI with a long history and a large scale in an orderly manner. In addition, BGI is headquartered in San Francisco and BlackRock is headquartered in New York, separated by thousands of kilometers and three time zones, which is even more difficult. Disaster. At that time, the progress was less than expected, and it took three years before and after the integration.

Fortunately, BlackRock has been leading in terms of scale since then, and has completed some acquisitions from time to time to make up for what may become a shortcoming in the future, including the acquisition of Helix Financial Group in 2010, the acquisition of FutureAdvisor in 2015, the acquisition of Cachematrix in 2017, and the acquisition in 2018. Tennenabaum Capital Partners, which also acquired the asset management business of Citibanamex in Mexico in the same year, as well as the acquisition of eFront Alternative Investment Solutions in 2019, etc., mainly strengthens BlackRock solutions and alternative investment businesses.

In addition, BlackRock is also increasingly focusing on sustainable investing. With Larry Fink’s annual letter to shareholders, BlackRock is seen as a leader in ESG investing and is well positioned for the next wave.

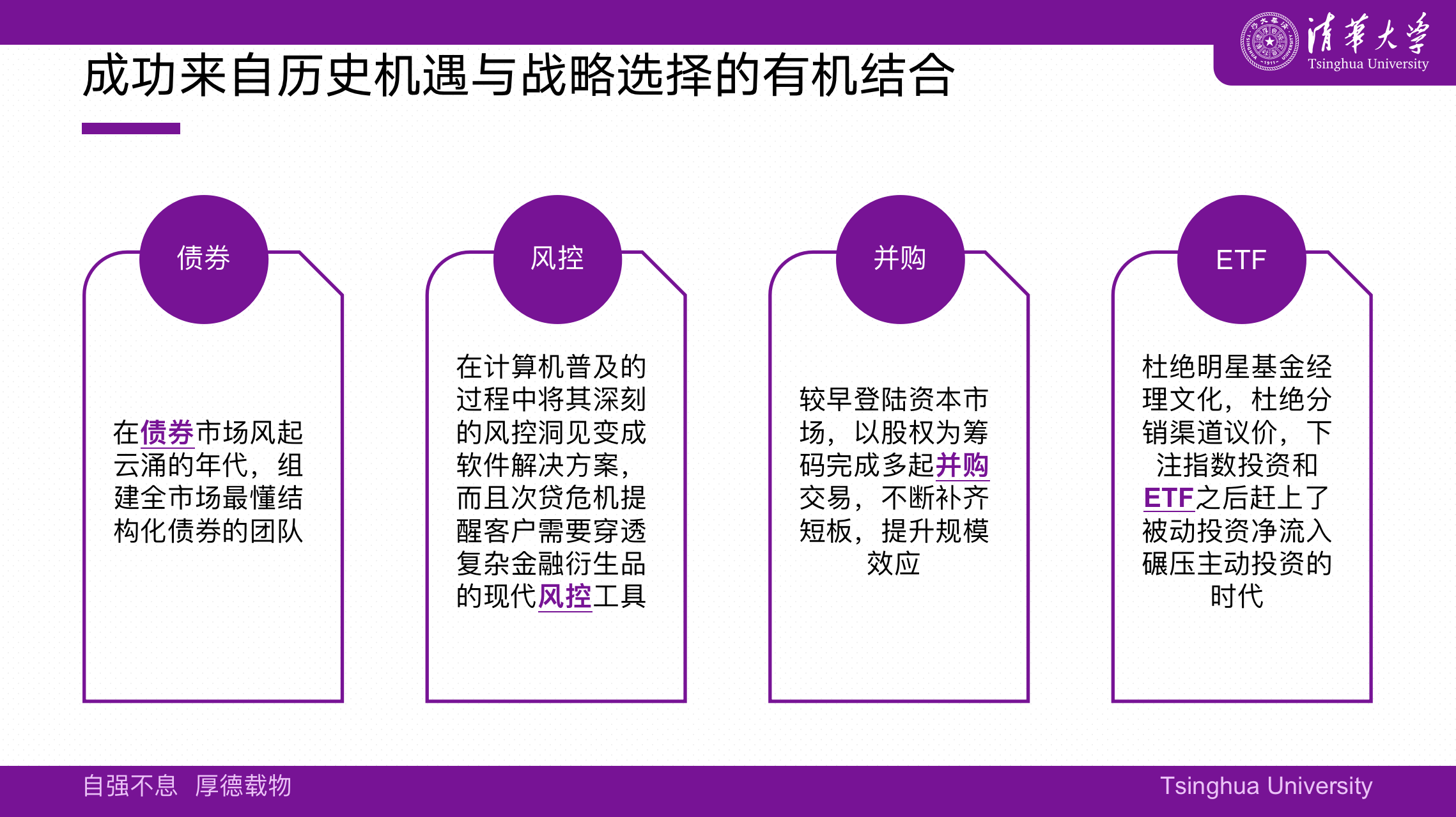

In the process of reviewing BlackRock’s success, I made a brief diagram of its development process, and highly summarized its success factors as four points: bonds, risk control, mergers and acquisitions, and ETFs. The reason why BlackRock has today’s dominance is that it has gone in the right direction in the development trends and waves of several major industries and has repeatedly stood at the top of the waves. The selection of several times is superimposed on the corporate culture of efficient execution and customer first. Why BlackRock is a $10 trillion asset manager.

Four key strategic choices include:

1) Actively managed bond business and product innovation in the 1980s, when the U.S. bond market was the hottest;

2) The combination of super risk awareness and evolving computing technology gave birth to the Aladdin system. It happened that the 2008 financial crisis not only made global mainstream institutional investors realize the importance of understanding and managing risks, but also gave Larry Finn An excellent stage to show off your strengths;

3) Listing as soon as possible and continuously enriching the categories of products and services through mergers and acquisitions, making up for equity investment and alternative investment;

4) The acquisition of Barclays BGI allowed BlackRock to occupy a favorable position at the beginning of the two waves of index investment and ETF, and then ushered in a crushing net inflow ratio of index investment to active investment.

Looking at the future based on the present, we can be certain that the first and second items in the above-mentioned four strategic lists will definitely not play a major role in the future development process, because the environmental situation has changed. Rules 3 and 4 should continue to work for the next decade and beyond, which is why the Aladdin System and ETFs remain at the heart of its strategy to drive future growth.

It’s important to point out, however, that just as BlackRock helped the Treasury and the Fed sort out the mess of the financial crisis in 2008, it sparked complaints about BlackRock’s proximity to power and the growing scope of the Aladdin system. The expansion has also rattled some regulators, who have grown increasingly concerned about whether so many different investors using the same risk analysis platform could lead to dangerous unification of views.

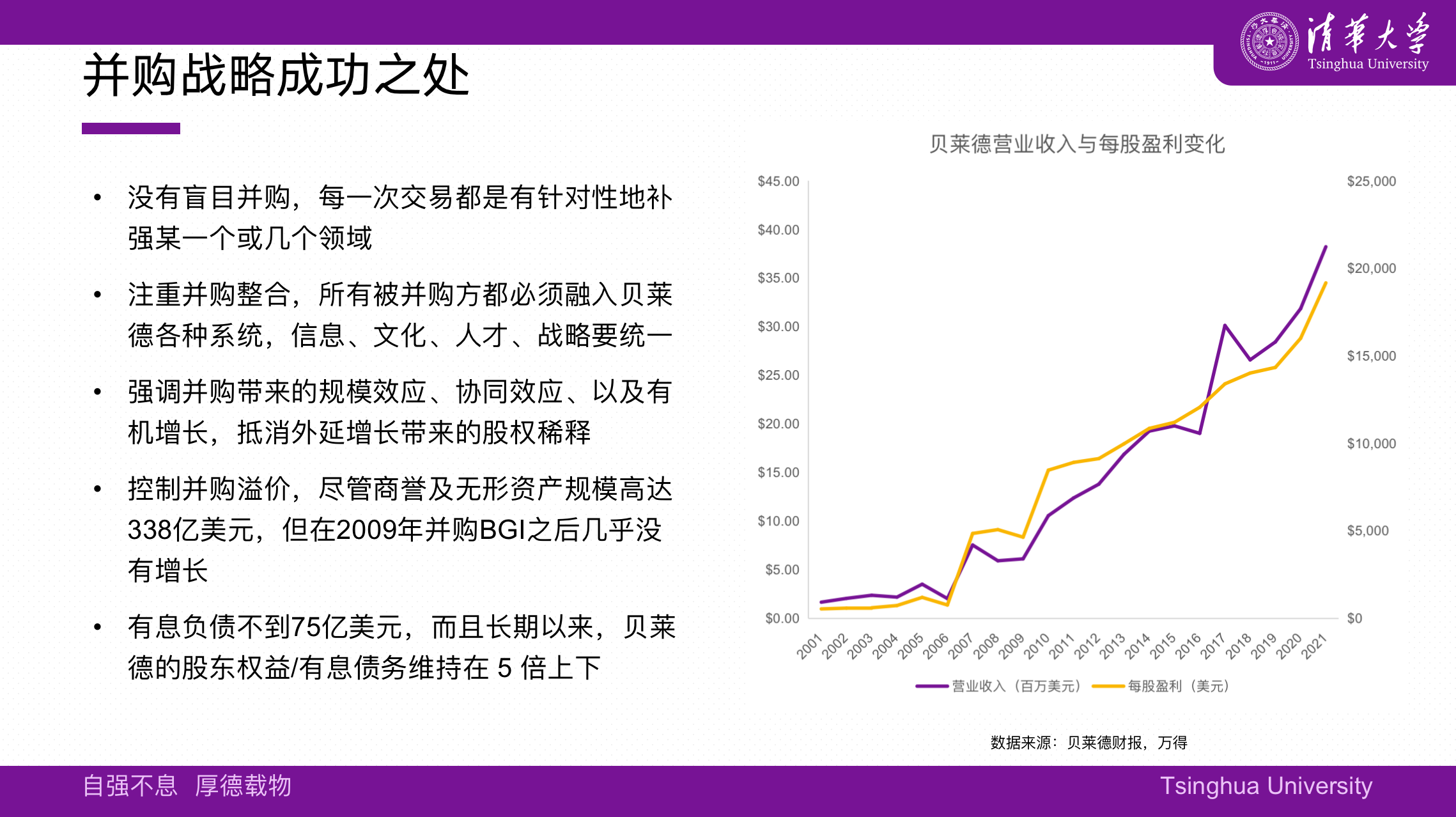

For each specific strategy, I have done in-depth analysis based on financial data and industry comparison. I will not expand it here. I just want to briefly talk about mergers and acquisitions, because large mergers and acquisitions are often obtained at the cost of equity expansion, so while the consolidated income increases, Equity per share is also diluted. To evaluate the success of a corporate merger, it depends on whether the diluted earnings per share can keep pace with the growth of receivables.

As we can see from the chart below, BlackRock’s revenue jumped twice between 2006-2007 and 2009-2010, the year of the merger of Merrill Lynch Asset Management and BGI. It is worth noting, however, that earnings per share (EPS) increased from $1.65 in 2001 to $38.22 in 2021, an increase almost in line with revenue growth, and shareholders’ equity was not eroded by mergers and acquisitions, which is also from another Dimension is a testament to the success of BlackRock’s M&A strategy.

Another consideration is BlackRock’s ability to digest and absorb mergers and acquisitions, and whether it can eliminate staff redundancy and improve business synergy through efficient management. We see that BlackRock’s operating profit margin was only 22% in 2006. Since then, it has been steadily improving and reached a peak of 42% in 2017. In the most recent fiscal year, it was 38%, which is still lower than its peers Puxin and Invesco , but it is gradually improving.

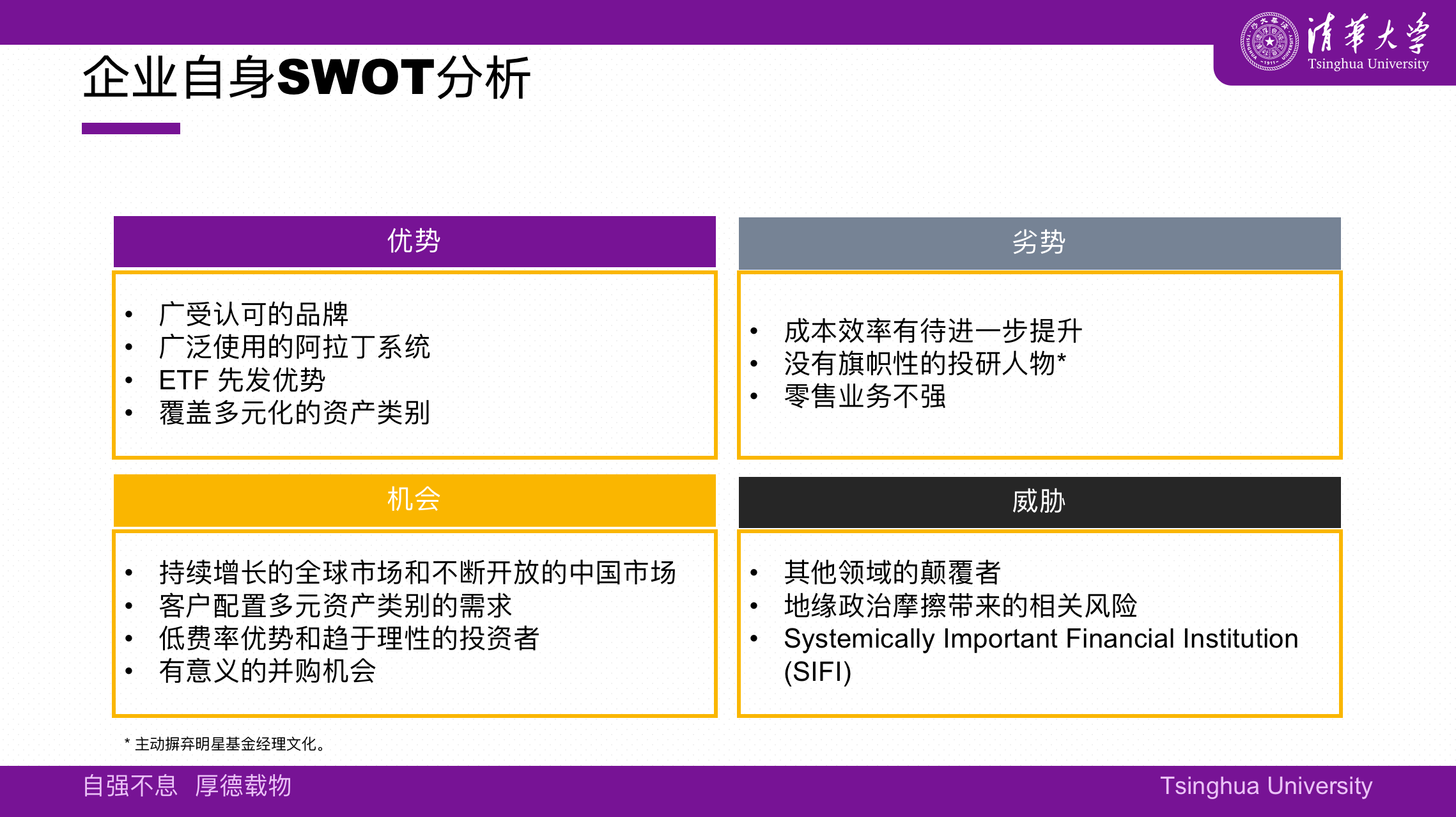

Looking to the future, I summarize the results of BlackRock’s SWOT analysis into the table below, and then formulate or analyze the company’s strategy based on the strengths and weaknesses of affiliated companies, as well as opportunities and threats in the market.

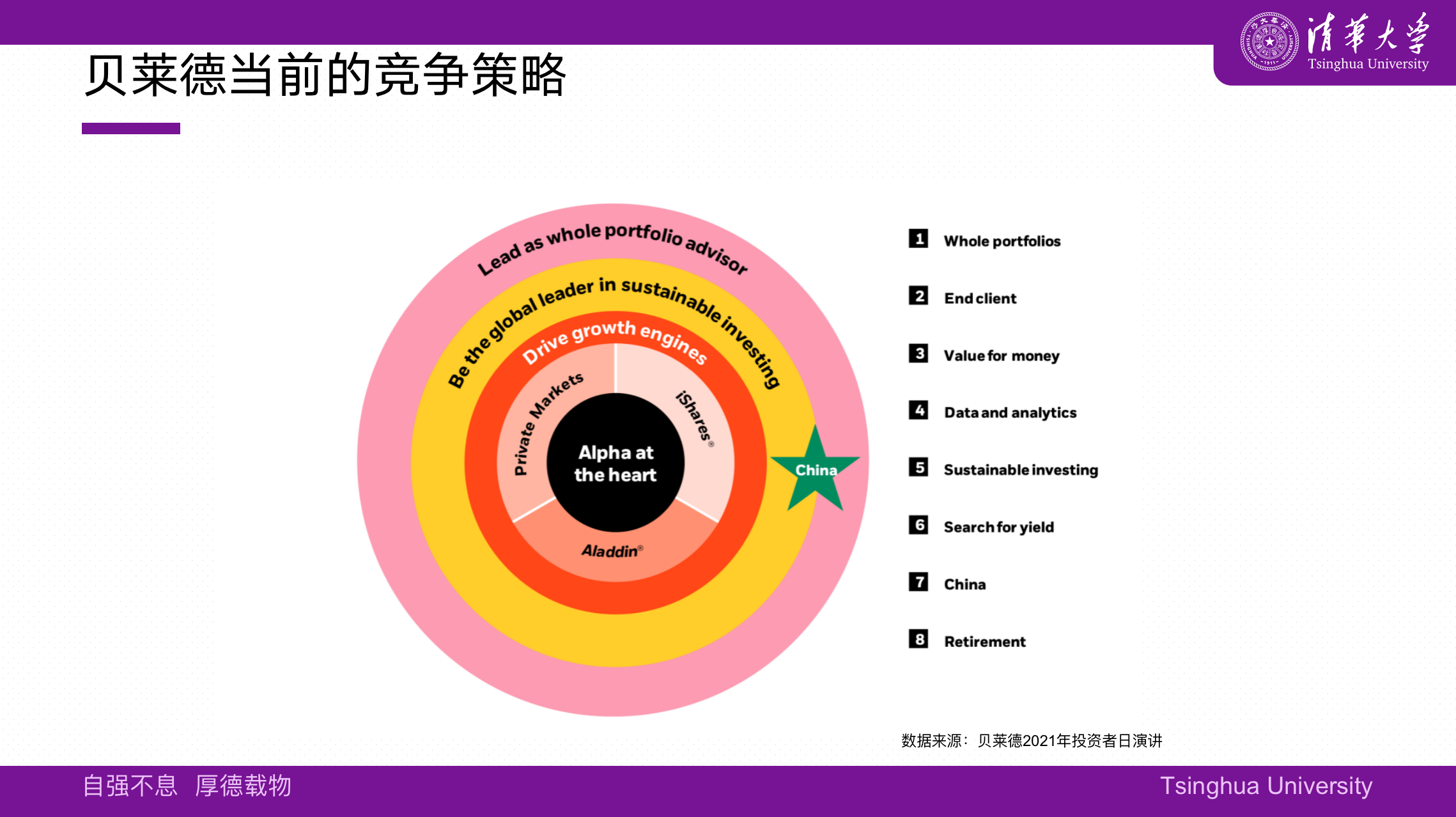

Coincidentally, I saw at the company’s 2021 Investor Day event that BlackRock summed up their long-term competitive strategy very clearly, just to be compared with the analysis above.

BlackRock summarizes its long-term competitive strategy into a picture and several keywords. The core goal of which is to bring alpha excess returns to investors. The three engines driving growth include Aladdin System, iShares, non-public Markets (Private Markets, which some companies list as “alternative investments”), two platforms that run across all businesses focus on becoming a global leader in sustainable investing and portfolio advisory, with two key market sectors including China market and pension market.

In addition to not mentioning actively looking for M&A opportunities, the market opportunities we saw in the SWOT analysis basically have targeted layouts, and the means are to continuously strengthen advantageous projects and strive to continue to lead. In the foreseeable future, if there is no regulation to force it to be split, BlackRock will be strong and strong…

(The above is not the whole content, only a small excerpt)

This topic has 26 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/5596182416/227600965

This site is for inclusion only, and the copyright belongs to the original author.