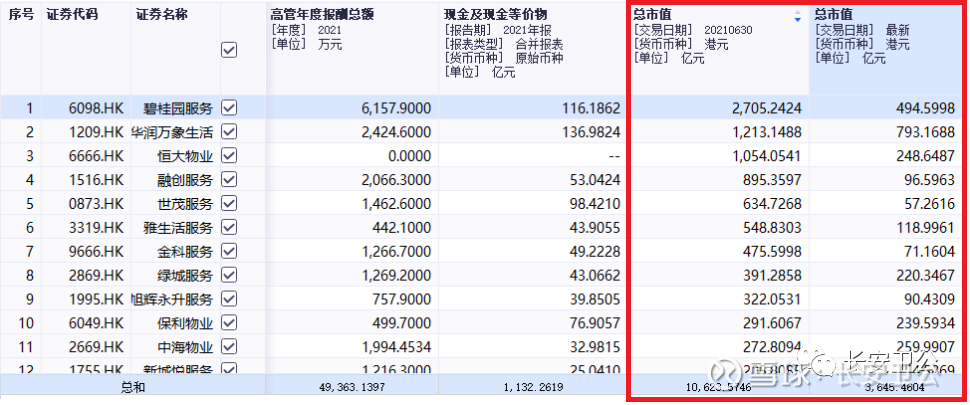

In the mid-year report last year, there were 49 property companies listed on the Hong Kong stock market, with a combined market value of over 1 trillion Hong Kong dollars.

Today, the number of Hong Kong property listed companies has reached 61, but the market value of the entire sector is only 364.5 billion .

The two private placements of the heavy-holding properties on Snowball fell for a whole year. For one, the gain went from +100% to -16%.

It is most apt to describe it as appalling.

They were probably confused.

To be fair, I’m actually a little confused.

However, from the perspective of the global capital market, as long as it is a sustainable index, a drop of 65% is almost the limit of decline.

Is it an opportunity or a trap for a large number of property companies that have fallen by more than 70% in one year?

1. Talking about the trillion-dollar property and the sea of stars last year

Let’s start with something interesting…

From 2019 to 2020, the property industry outperformed various AH indices by a large margin, and in the first half of 2021, the growth rate exceeded 46.6%, accelerating the rise .

In fact, at that time, I thought that the property had net cash, low leverage, long operating cycle, and an observable five-year growth rate of 30%+ for the sector. The valuation of 20X~30X was generally reasonable .

In addition, last year, it was generally believed that the property had the following advantages:

(1) Policy support: Real estate is subject to greater restrictions, and property is supported more;

(2) Stock + incremental model : no major capital expenditure, financial control of net cash, double growth curve, and strong growth certainty;

(3) Exogenous growth is still accelerating: Although the real estate is facing a debt repayment peak, its completion is in a high boom stage;

(4) Value-added services have high gross profit and good growth rate: word-of-mouth is good for traffic realization;

(5) Increase in penetration rate: The penetration rate of property services has increased under the support of the 14th Five-Year Plan;

(6) The development of multi-format property management has just started: the leading companies in the industry integration capability and performance growth model have already run through, and the potential and certainty determine the valuation ceiling to be further raised.

However, there is nothing new in the capital market, and things have changed since the famous counterpoint.

After a famous brokerage began to vigorously sing about multi-property and promote the property PS valuation method.

Soon, the real estate company ushered in the peak of debt repayment, Bao Lei one after another, and the real estate and property sectors ushered in a year-long main downtrend.

2. Private enterprise real estate is gradually thundering, and negative feedback begins

In 2021, real estate companies will usher in a debt repayment peak; in 2022, real estate companies will usher in the highest debt repayment peak in history, with a total of over $63.1 billion in real estate debt due during the year.

After the three red lines were drawn, the domestic real estate industry, which relied on Gao Zhou’s forwarders, became increasingly overwhelmed.

Up to now, there are Evergrande, Sunac, Powerlong, Shimao, Zhengrong, Tianyu, Zhongliang, Xinyuan, Zhongnan Construction, Rongxin, Sunshine City, Yuzhou, Xinli, Aoyuan, Kaisa, Contemporary Real Estate, Fantasia More than ten real estate companies have defaulted on their debts.

This directly brings 4 risks to the property company:

First, after a real estate company defaults on its debts, it will affect subsequent financing and delivery of new houses, which will have an impact on the delivery of the contracted area of its affiliated property company, which in turn will affect the sustainability of the property company’s subsequent performance. For example, the dozen or so defaulting companies listed above will inevitably It will affect the delivery process of the property company;

Second, the decrease in the delivery of new houses by real estate companies will affect the revenue and profit of value-added services (case and sales assistance services) for non-owners in property companies, and may even transmit profits to the parent company through the case and field sales assistance business;

The third is that it is possible to empty the property company’s account of cash through related transactions. Now China Evergrande has been hammered. There are still some companies with general governance, and there are also relatively high risks to carry out robbery operations, such as X Park, X Mao, XX industry;

The most ruthless one is to sell the property assets of the subsidiary at a low price to get cash back, and at the same time to buy the junk assets of the parent company at a high price. This is more typical of X Park , but it only made an announcement and did not make the trip.

Cang Lin knows the etiquette in reality, and knows honor and disgrace when she has enough food and clothing.

Private real estate companies are now seriously bleeding, losing most of the financing channels, and some companies have made some outrageous behaviors, which has caused the entire industry to be shaken.

In addition to the above substantive effects, many shortcomings of property companies have been viewed with a magnifying glass, such as:

(1) Labor costs account for a large proportion of the operating costs of property service companies . If the wage level rises too fast, the gross profit margin level of the industry will be squeezed.

(2) Third-party outsourcing competition risk. At present, the development of the property management industry has entered an expansion period, and the main expansion areas are concentrated in the Greater Bay Area, the Yangtze River Delta, and the Chengdu-Chongqing Economic Circle. The services of most property companies are homogeneous, and the competition for third-party projects to expand is intensified.

(3) Risk of value-added service expansion. For the value-added services of owners, various business models are being explored, the profitability and competition pattern are not yet completely clear, and there will be certain expansion risks and trial-and-error risks in the future.

(4) Outsourcing risk. The proportion of outsourcing costs in operating costs is increasing year by year. If the quality of outsourcing business cannot be effectively controlled, it will pose risks to the brand image of property service companies and the satisfaction of owners.

The above are the core factors that have caused the property to enter the death spiral in the past year, and are also the core concerns of the market.

3. Not so good, not so bad

From being extremely sought after by the market to being extremely disgusted, the property took only one year to do it.

Be optimistic when it goes up and pessimistic when it goes down.

However, at this point in time, I think for the property sector, the opportunities far outweigh the risks.

In the very early days, I selected several targets that I wanted to hold for a long time, namely hydropower, energy, banks, REITs, property, and highways.

After reviewing the history of Japan’s economic development, banks were excluded.

From this point of view, if the property can get out of the predicament, it is indeed the most cost-effective configuration.

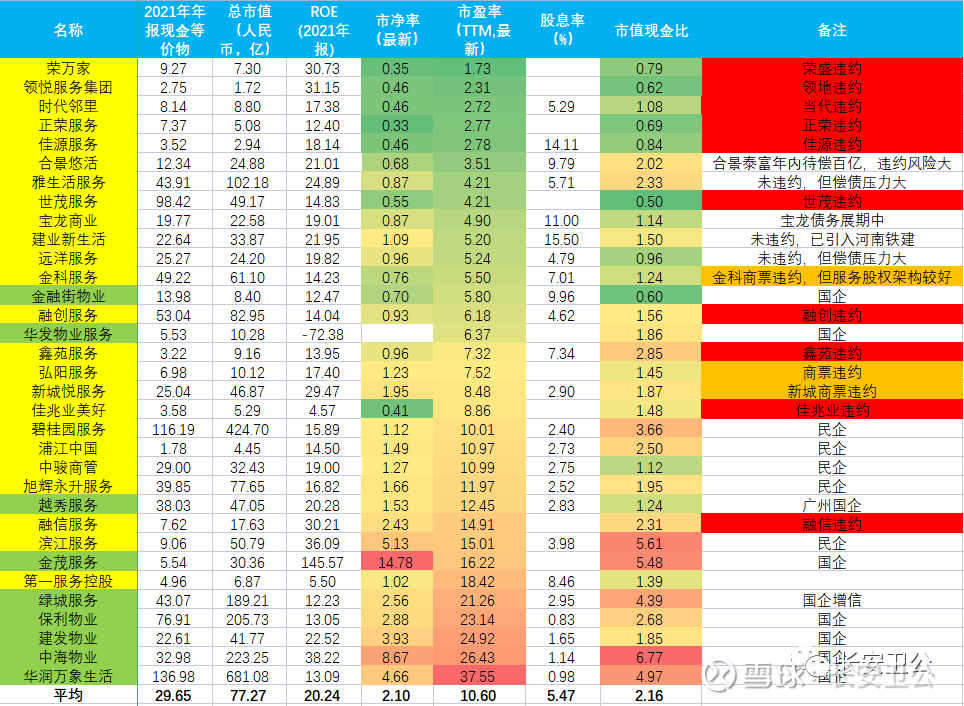

I focused on 33 property companies, of which 15 fell below net assets and 7 fell below net cash, all of which were private real estate companies.

Among these 33 companies, the average price-earnings ratio of private property companies was 7.32; the average price-earnings ratio of non-private property companies was 19.34 times.

However, from the perspective of growth rate, the growth rate of private property companies is generally faster than that of non-private property companies.

This kind of valuation logic is blunt: now the market generally expects that all private real estate companies will go bankrupt and will not be reorganized, and will slowly die; and all private real estate companies will empty the cash on their subsidiaries’ accounts.

I think that’s unlikely.

What if half of the private property companies did not die?

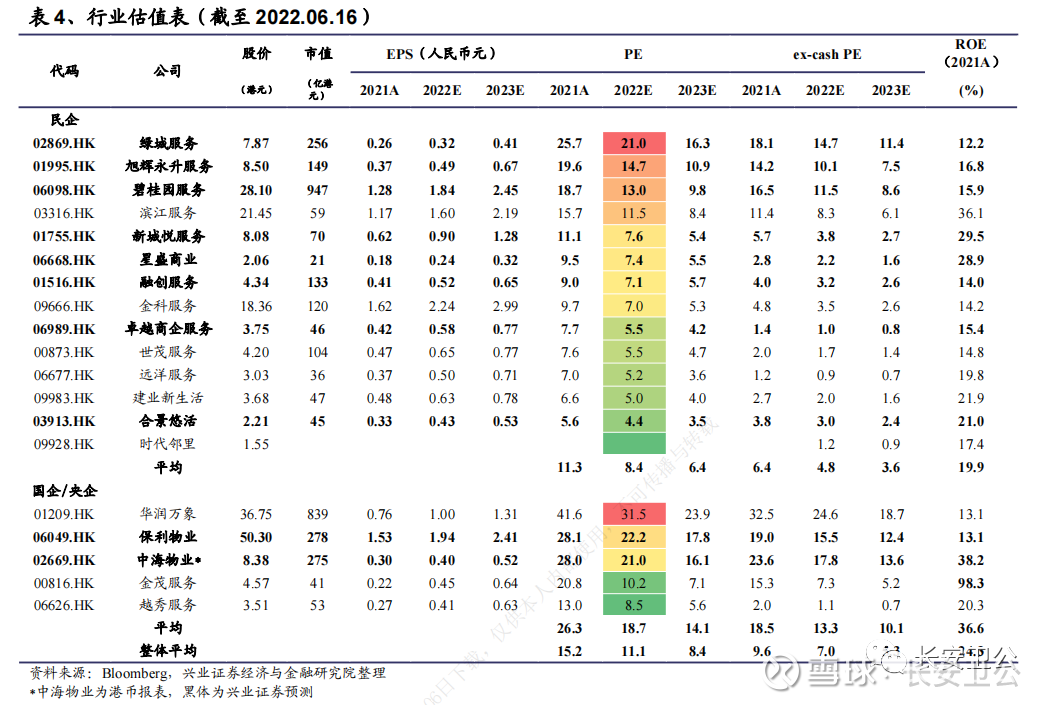

According to a calculation by Industrial Securities, according to the development plans of some private property companies, by the annual report of next year, there will be 9 private property companies with a price-earnings ratio below 6 times.

According to the general dividend rate of more than 50% of property companies, the dividend rate of these 9 companies is expected to exceed 8%.

All in all, the logic of the current property valuation is: private real estate companies make a hard landing – private real estate companies embezzle all the cash of subsidiaries – private real estate companies sell most of the subsidiaries’ assets and buy their own junk assets at high prices .

Unless the chain is complete, the valuation logic is valid. I think it is unlikely that the chain will be complete.

If it gets past this period, then property stocks could be in for a very long period of sunny days.

Therefore, the current property, the opportunities outweigh the risks, it is worthy of focus.

$Sunac Service(01516)$ $Jinke Service(09666)$ $Jianye New Life(09983)$

There are 101 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/3203620784/227511372

This site is for inclusion only, and the copyright belongs to the original author.