Welcome to the WeChat subscription number of “Sina Technology”: techsina

Source: Yuanchuan Research Institute

It is difficult for a company to make mistakes in the trough, but it is easy to make mistakes in the peak.

In 2016, Intel was in full swing, with various product lines covering 14nm, including high-end processors and server products; at the end of that year, Intel launched Kaby Lake architecture processors that replaced Skylake.

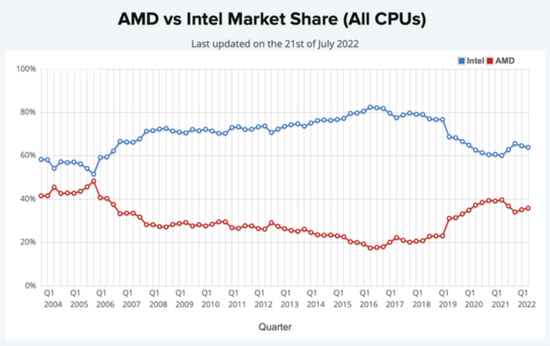

During the same period, it was still a year before AMD’s classic Zen architecture came out, and the APU market, which had high expectations, had a mediocre response. In the CPU market, the share gap between the two sides has reached the highest level in nearly a decade.

But after 2016, Intel’s old and new businesses were in trouble:

The development of Atom series processors for mobile terminals stopped, and the baseband chip business was sold to Apple. The process iteration of the TMG department has been stuck at 14nm for a long time, and the major business production capacity that should have transitioned to 10nm was forced to collectively squeeze in 14nm. TSMC and Samsung have completely overtaken Intel in this window.

On AMD’s side, after three generations of iterations of the Zen architecture and the blessing of TSMC’s new process, AMD’s CPU market share has steadily increased since 2017, and reached a historical peak of 27.7% in the first quarter of 2022.

In the previous second quarterly report, AMD’s revenue exceeded US$6 billion, a year-on-year increase of 70%, and its profit soared 119%. In contrast, Intel pulled a big crotch and successfully broke the 30-year streak of profitability. Analysts at Bernstein said they were shocked. “This is the worst report we’ve seen in our careers.”

The gap that widens and then narrows

The gap that widens and then narrowsIn the end, AMD’s market cap historically surpassed Intel’s.

In the past decade or so, Intel has missed almost all of the largest incremental markets in the electronics industry: In 2005, Intel refused to develop mobile SoCs for Apple, missing the highest value-added link in the smartphone industry chain. Nor did they foresee the use of GPUs in AI.

The most serious problem facing Intel is that its main business is also shrinking in the context of the continued decline of the consumer electronics market.

So, how did all this happen?

01

Stop bleeding: cut love for innovative business

In 2020, Robert Swan, who took over as Intel’s CEO for the fourth year, made a decision that went against his ancestors: he sold the NAND flash memory business to SK Hynix for $9 billion and took off Intel’s first underwear.

NAND flash memory was once a business for Intel, originally invented by Toshiba, and had a golden age of nearly 20 years. But both the Americans and the Japanese lost out to the Koreans, and the biggest players in the industry are Samsung and SK Hynix. Before the sale, although Intel’s market share in the NAND field was 11.5%, it was losing money for a long time, and it only made a profit of 120 million US dollars in 2019.

NAND flash isn’t Intel’s only drag on the gas. After missing the mobile terminal market, I regret that the original Intel has been addicted to expanding its territory and looking for a new second growth curve, but it has taken many detours.

In the mobile market, Intel’s x86 architecture lost to ARM, and then Intel tried to fight back with atom processors, but it bet on the short-lived netbook market, and then it was installed in mobile phones, and its performance was still flat.

At the same time, in the face of NVIDIA’s penetration in the AI field, Intel had hoped to overtake NVIDIA in the field of artificial intelligence by acquiring Nervana. But after three years of development, Intel realized the cost and versatility of the product, and had to turn around and buy another company to start over.

After Robert Swan took office, in the face of excessive debts from innovative businesses, Intel began to “reluctantly part with love”, and a series of non-core businesses were stripped off one after another:

In 2019, Intel packaged and sold its 4G/5G baseband business to Apple along with 2,200 employees; two years later, Intel announced the closure of its depth camera business-although they were already the leader of the track; in July this year, 9,000 The Intel drone, which has performed light shows at the Olympics and the Super Bowl, was successfully photographed by the Musk brothers.

What shocked the outside world the most was undoubtedly the shutdown of the Optane business.

Optane is a two-in-one product of memory and hard drive developed by Intel, which was regarded as a weapon in the past to counterattack the storage market. It is also the sixth non-core business that Intel has divested in recent years, which directly brought a loss of $559 million in the second quarter.

There are two reasons for Optane’s failure: The intuitive reason is that after the dissolution of the joint venture between Intel and Micron, Micron became the only company on the market with a 3D XPoint production plant, but Micron gave up this business.

On the other hand, there is a lack of competitiveness. Over the past few years, the storage industry has clearly favored CXL memory: it is not only a perfect replacement for Optane’s functionality, but also at a lower cost, while also enabling a more flexible external memory pool. The huge losses brought about by this have already made Intel somewhat unbearable.

But the core factor is the shrinking of the main business: as the leadership in the CPU market becomes increasingly unstable, there will be less and less room for “strategic losses” for new businesses.

This is actually the case in many Internet companies – revenue in the core sector has declined, and layoffs in the peripheral sector have shrunk.

The last to be spun off was finance-turned-CEO Robert Swan, who replaced Brian Krzanich in 2016 because of his “affectionate relationship with his employees.” But in January 2021, the board brought in Pat Gelsinger, an engineer who had worked at Intel for 30 years, hoping that the latter would turn the tide.

This was regarded by the capital market as a signal that Intel was regrouping. On the day Kissinger took office, Intel’s stock price rose by 7%.

02

The crux: a failed pendulum

On the eve of Robert Swan’s resignation, he planned to lead Intel’s transformation to Fabless — that is, he only designed chips and handed them over to TSMC for foundry. Before this, Intel has been the IDM model of design + manufacture.

However, after Kissinger took office, he set things right and put forward an ambitious IDM2.0 plan: not only to make his own chips, but also to manufacture chips for other companies.

In Kissinger’s plan, Intel must quickly close the gap with TSMC and Samsung within a few years, because the backwardness of the process is the core factor for Intel’s gradual decline in the past few years.

The so-called IDM refers to the three core links of semiconductor production: design, manufacturing, and packaging and testing, and the entire industry chain is managed by itself. The advantage of this model is that it has strong production capacity and can implement its own strategy in an all-round way. The disadvantage is that the company has a long production front and high investment costs.

Based on this model, Intel has developed a production model called tick-tock: that is, two years are used as a unit. The “tick year” focuses on chip manufacturing, updating the chip manufacturing process and improving the process, and the “tock year” focuses on chip design and innovating the architecture.

Intel once relied on this strategy to beat the world’s invincible players and gain a market position close to a monopoly. But since 2014, the “tick-tock” pendulum has gone wrong:

Intel mass-produced the 14nm process this year, nearly two and a half years away from 22nm; it took four years for the 10nm process to be mass-produced. So far, the 10nm process has been used for nearly 3 years, but the fastest time for the 7nm process to come out is in the second half of this year.

During this period, Intel once took out the third generation of 14nm+++, but the processes of TSMC and Samsung were iterating steadily. Strictly speaking, part of the reason for Intel’s lag is the excessively stubborn pursuit of chip density, which has made it difficult to break through in the process.

For example, according to TSMC’s standards, Intel’s 10nm can be called 7nm. Even TSMC admits that nanometers no longer represent the real physical scale, but are more like a marketing term.

That being said, it is an indisputable fact that AMD relies on TSMC’s puffy 7nm Jedi counterattack.

At the beginning of 2016, Intel alone ate about 80% of the market, but in the following years, Intel’s market share gradually fell to around 60%, while AMD relied on Zen architecture to steadily narrow the gap.

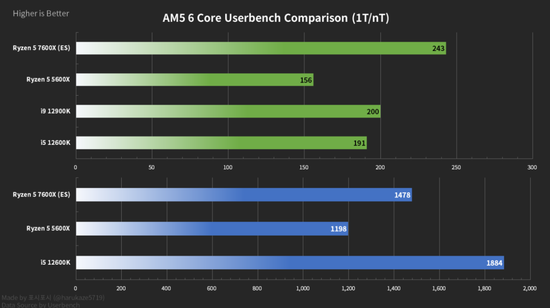

At the end of July, AMD’s next-generation chip, the Ryzen 5 7600X, was suspected of sneaking away. In the leaked evaluation results, the 7600X, which is positioned in the mid-range running market, has a single-core running score that exceeds Intel’s flagship chip i9-12900K.

The IDM model can play an advantage, a crucial factor is the share of downstream products. Since the investment at both ends of chip design and manufacturing is getting higher and higher, the huge upstream R&D cost can only be covered by relying on the huge product shipments.

Among the big companies in the consumer electronics industry, almost only Samsung and Intel use this model, because their product market sales are high enough and shipments are large enough.

In 2008, AMD sold its own fab, GlobalFoundries, which is currently the fourth largest chip foundry in the world, in order to get rid of losses and focus on fighting Intel and Nvidia in chip design.

In terms of process and cost, IDM’s “I want it all” is bound to be much higher than TSMC/AMD’s “specializing in manufacturing/specializing in design”.

Especially when the sales of downstream products decline, the financial pressure on both ends will be even greater. For example, in 2021, TSMC’s capital expenditure will reach $30 billion, while Intel, which has higher revenue, is only $17.9 billion.

In this case, a vicious cycle of “process lag – sales decline – R&D spending reduction – process further lag” is prone to occur, which is why Robert Swan is pushing for the abolition of the IDM model in 2020.

But a year later, Kissinger came to power to revisit chip manufacturing, targeting both AMD and TSMC.

03

Underpants: The last resort

Not long after the announcement of IDM2.0, Intel and MediaTek reached a cooperation to manufacture a series of chip products with low complexity. However, the cooperation between Intel and MediaTek has a heavy condition – open X86 architecture.

The X86 architecture was born in 1978. It is a computer language instruction set developed by Intel, and it is also the key to Intel’s ability to make money lying down in the past. For more than forty years since then, most PCs have used the X86 architecture, so much so that it has almost become an industry standard. In 2009, the European Union sued Intel, accusing Intel of abusing the market dominance of the X86 architecture.

Letting Intel open the authorization of the X86 architecture is comparable to Coca-Cola’s public formula table, which is tantamount to letting Intel take off its last underpants.

1978 8086 processor with x86

1978 8086 processor with x86Intel’s willingness to “give up monopoly”, on the one hand, stems from the increasingly acute internal contradictions in the camp. Intel and AMD are the only companies that have licenses for the X86 architecture, and the aggressive AMD has made Intel even more difficult. In the fourth quarter of 2021, AMD’s market share in x86 processors exceeded a quarter for the first time.

But in the long run, challenges from the outside are just as threatening.

In 2019, Apple, a former major customer, decided to abandon Intel: First, the chips under the Intel X86 architecture have long-term energy consumption problems, which makes Apple, who is extremely pursuing energy consumption ratio, unbearable; second, Intel’s manufacturing process cannot keep up with the fast-paced R&D progress of Mac .

In fact, Intel not only lost a customer, but also a future competitor – Apple decided to develop its own chip M1 based on the ARM architecture.

It took only about a year for Apple to take a piece of the cake from the market that Intel has dominated for more than 40 years, and it has maintained a certain growth: According to the statistics of Mercury Research, in the third quarter of 2021, the ARM architecture in the field of PC chips will continue to grow. The market share has reached a full 8%, and it has risen to 9.5% in the fourth quarter.

The ARM architecture counterattacks from the mobile side to the PC side, eroding the share of x86, which is the last thing Intel wants to see. At the same time, the RISC-V architecture is also growing in influence. In the face of internal and external troubles, Intel decided to give it a go – instead of keeping the X86 architecture in its arms, it is better to open some authorizations to new partners and re-drive the market’s attention to x86.

At the same time, Intel can also turn the once “monopoly tool” X86 architecture into an attractive bargaining chip, optimize the production capacity structure and inject new vitality into the foundry business.

Prior to this, Intel’s foundry was “self-sufficient”. Once the chip process was updated, all product lines would be replaced with the latest process, which also brought a problem: many obsolete old processes were difficult to bring benefits. You must know that TSMC also has nearly half of its revenue from mature processes above 16nm.

If it can leverage some customers through the opening of x86, Intel can also revitalize some backward production lines and manufacture relatively low-end chips. This may be a very practical strategy for Intel today.

But just as the power of a nuclear weapon is manifested when it is not launched, Intel’s openness looks like a helpless stop-gap measure after they have missed so many times.

04

Intel founder Andy Grove, in his book “Only the Paranoid Survive”, unfortunately pointed out the current situation of the company:

The brilliant superstars of the previous era were often the last to adapt, the last to succumb to the principle of strategic turning points, and he failed more badly than most.

In the 1980s, Japanese companies forged an indestructible advantage in DRAM, forcing Intel to turn to microprocessor development, giving birth to the electronics juggernaut. Today’s Intel is somewhat similar to Toshiba and NEC at that time.

When the media asked about the second-quarter earnings report, CEO Kissinger left only four words, “It’s up to you.”

Thirty years ago, Intel opened up the second battlefield in the cracks of Japanese companies. There is a big background, that is, the transformation of mainframes to consumer products, and the rapid prosperity of the consumer electronics market. But today, the entire consumer electronics market is shrinking.

According to data released by Gartner, the global PC shipments in the second quarter handed over the worst answer in the past nine years: the actual number was about 72 million units, a year-on-year decrease of 12.6%. Looking at the whole of 2022, shipments are expected to decline by 6.2% year-on-year.

To return to the top under such circumstances, I am afraid that it is several times more difficult than AMD’s Jedi counterattack.

(Disclaimer: This article only represents the author’s point of view and does not represent the position of Sina.com.)

This article is reproduced from: http://finance.sina.com.cn/tech/csj/2022-08-19/doc-imizmscv6885120.shtml

This site is for inclusion only, and the copyright belongs to the original author.