1: The revenue in the first half of the year was 15.3 billion, a year-on-year increase of 14.2 billion, an increase of 7.7%; specifically, the revenue in the second quarter was 9 billion, compared with 8.85 billion in the second quarter of 2021, a slight increase. Needless to say, the various difficulties in the second quarter, Oriental Yuhong’s ability to achieve such revenue is worthy of its status in the arena, or it is a manifestation of the capabilities that a leading company in the industry should have.

2: Net profit: 970 million in the first half of the year, compared to 1.54 billion in the same period last year; specifically, 650 million in the second quarter compared to 1.24 billion in the same period in 2021, almost halved, which is quite tragic. If it is acceptable in terms of revenue, it is terrible in terms of real net profit. As for the 40 billion revenue and 5 billion net profit that the company plans to accomplish this year, I think it is very, very difficult, almost impossible.

Specifically, analyze the reasons for the decline in net profit;

(1) The gross profit margin was 25.9% in the second quarter, compared with 30.8% in the same period last year, a decrease of 5 percentage points. Let’s simply calculate the revenue of 9 billion corresponding to 5 percentage points, and this alone reduces the profit by 450 million.

(2) Looking at expenses, the expense ratio in the second quarter was 14.4%, compared with 12.3% in the same period last year, which is another 2-point difference, bringing a profit of 180 million. (According to the company’s performance briefing meeting: the expenses are arranged according to the annual plan, that is, I did not expect such a moth this year, resulting in a sharp rise in the cost side and a decline in net profit, but the expenses are indeed planned according to the optimistic situation, As a result, the expenses will be spent more, and the net profit will naturally decline. Relatively speaking, we look at the management of the company Jushi. The company decisively adjusted the cost budget at the beginning of the year in response to various moths in the second quarter, reduced expenditure, and abruptly In the second quarter, the expense ratio decreased by 2 points, so a comparison can reveal the gap in the company’s management. Although Yuhong is also very good, it is obviously insufficient to deal with various emergencies in the second quarter.)

(3) In the second quarter of this year, an extra 50 million bad debts were accrued

Add these abnormal expenses in this way and restore it: 6.5+4.5+1.8+0.5=1.33 billion

Does this look more normal?

Of course this may be a way of self-comfort ha ha ha ha ha!

The decline in gross profit margin is well understood. In the second quarter, various unfavorable factors led to soaring crude oil prices and soaring asphalt prices, which led to the increase in the price of the company’s raw materials. This situation is beyond the control of the company. What we can do is to have low prices at the beginning of the year A large number of stockpiles (the cash flow statement in the first quarter of which the purchase price of goods reached 6.55 billion is a major reason) However, the price of asphalt continues to be high, and the company’s inventory will always be used up, no matter how expensive it is. To survive in this industry, you can only endure this kind of disaster. Of course, the company has also raised the price of the product several times as a last resort, but after all, it takes a process from price increase to response to terminal, and in this process, it also needs to face the pressure of competitors step by step. The macroeconomic downturn makes life difficult for everyone, and competitors in the industry will naturally become preoccupied with competing for the gains and losses of one city and one pool, even at low prices, credit, and payment periods to snatch customers and seize the market.

In short, the rising prices of raw materials, the economic downturn, and the intensified competition in the real estate market have resulted in a decline in gross profit margins.

3: Receivables

The characteristics of the waterproof industry determine that the problem of receivables will exist for a long time.

When the quarterly report for the third quarter of last year came out, the market saw that Yuhong’s receivables were as high as 11 billion, so the sound of thunder was heard. As a result, by the end of the year, the annual report was released, and the revenue ratio in the fourth quarter was as high as 151%.

In this year’s 2022 semi-annual report, the receivables reached 12.95 billion, far exceeding the same period last year. If you look at it in detail, you will find that there are 8.76 billion receivables at the beginning of the year, and 790 million new receivables in the first quarter of 2022. The second quarter added 3.4 billion.

Further analysis, the revenue in the second quarter was 9 billion, and the cash received from sales was 6.1 billion, with a difference of 3.9 billion. It will be clearer if you look at it this way.

Under normal circumstances, pay attention to Yuhong’s receivables, mainly based on the cash-to-payment ratio. The company is now very strict in the assessment of receivables.

Of course, the situation this year is rather special. The real estate market has exploded, and the huge amount of receivables against Yuhong will undoubtedly make investors uneasy. To be honest, I believe management is more worried about such issues than we are. This is also a major difficulty in investing. If you are worried that it will not work properly, it is better to stay away.

In the past two years, Yuhong has also increased the development of the integrated company’s non-real estate field, and the development of the C-end market has also achieved very good results.

4: Yuhong’s future:

Of course, we should also see the optimistic factor from the negative factors. Rising raw material prices, real estate market regulation factors and the impact of the epidemic have all led to the deterioration or even closure of many small businesses in the industry, accelerating the concentration of the industry.

Yuhong’s goal is to have a market share of 30% in 2025 and a market share of 50% in 2030. The current market share is only 15-20%, and the annual revenue is 30-40 billion.

According to the information of the performance briefing:

The key layout of Yuhong in 2022:

(1) B-end non-real estate market (infrastructure, municipal, etc.)

The B-end is de-realized and vigorously develops non-real estate business.

The B side mainly conducts business through various regional integrated companies, mainly including: infrastructure, municipal, policy housing, public construction projects (hospitals, schools, etc.), energy projects, underground pipe networks, etc., renovation, industrial and mining enterprise storage, etc.

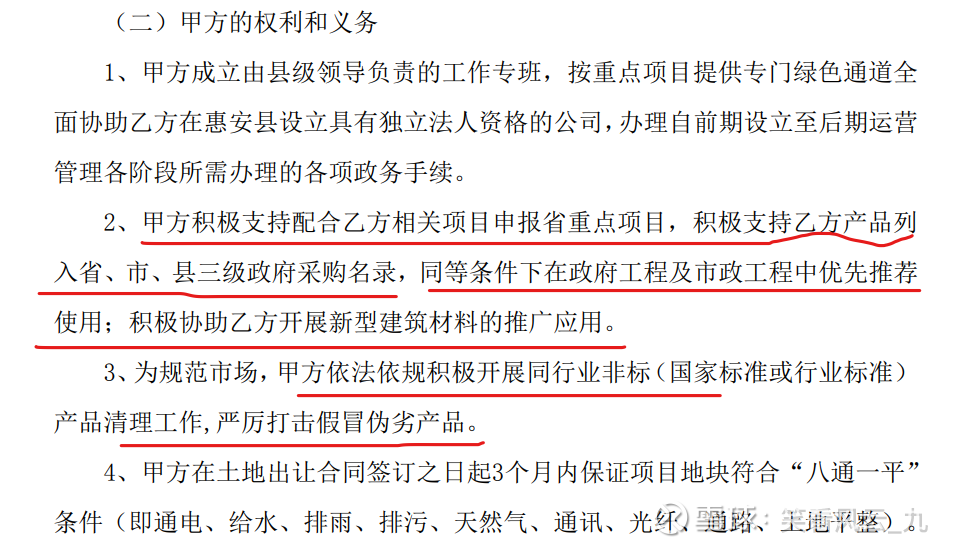

If you look carefully at the agreements signed by the integrated companies of Oriental Yuhong and local governments, there is one item that lists Oriental Yuhong products in the local government procurement directory, giving priority to purchase and use.

The country’s vigorous development of infrastructure projects in the second half of 2022 will undoubtedly have a very positive impact on Oriental Yuhong. It is believed that Yuhong’s projects in the infrastructure field will be soft in the next two years.

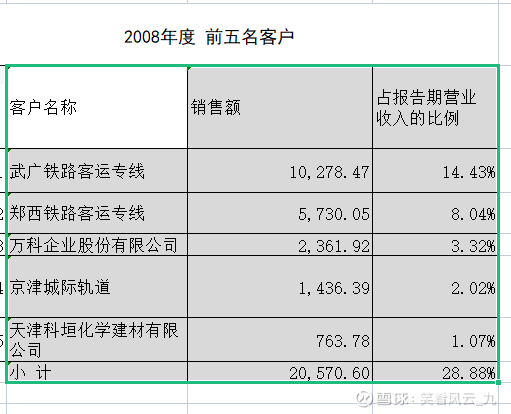

I feel that I have returned to Oriental Yuhong, a major project specialist around 2008. ![]()

![]()

![]()

(2) C-end: Overall, the C-end will reach 7 billion to 8 billion in 2022, accounting for about 20% of the company’s overall revenue. In 2021, the C-end revenue is 4 billion; in 2023, the C-end is expected to exceed 10 billion, accounting for 20% to 25% of revenue.

China National Construction Group (wall and floor auxiliary materials), the revenue of the civil construction in 2022 will exceed 5.5 billion.

In the field of home improvement (Honggehui), the revenue in 2022 will reach 1 billion to 1.2 billion

Repair: The revenue in 2022 will reach 1 billion to 1.2 billion.

At the same time, according to the internal use of the company’s performance briefing meeting:

The demand in the waterproof industry mainly comes from non-housing business. At present, the waterproof market is about 200 billion yuan, and the real estate market accounts for 50 billion to 60 billion yuan. The reliability of the company’s growth comes from the increase in market share:

Assuming that the scale of the waterproof industry remains unchanged at 200 billion to calculate:

In 2022, the market share will be 20%, then deduct the real estate market company revenue of about 30 billion to 40 billion

In 2025, the market share will be 30%. In the same situation, the company’s revenue will be about 50-60 billion

In 2030, the market share is 50%, and the same situation, the company’s revenue is 80 billion to 100 billion.

However, in fact, the growth rate of the waterproof industry scale is not lower than the annual GDP growth rate.

Valuation: (Very arbitrary ![]()

![]()

![]()

![]() )

)

According to the company’s net profit margin of 13~15% in the past, it is conservatively estimated that the future sales net profit will be 10~12%. Based on this, it is estimated that the net profit in 2022 will be about 3 billion to 5 billion. That is 40 ± 10% billion, and the company’s net profit in 2025 will be about 5 billion to 7.2 billion, or 60 ± 10% billion. Take the risk-free rate of 3~4%.

The current reasonable valuation: 40±10%*25~30=1000±10% billion.

Buying point: 60±10% *25~30 *0.7 / 2 = 580 ±10% billion

Selling point: 40 50=200 billion, or 60±10%*25* 150% = 225 billion

4: Executives reduce their holdings

It’s really disgusting that executives reduce their holdings. But as for whether to know the content of the quarterly report in advance, I don’t think so.

Do you think, as a group of people at the top of the company, can they not know the operation of the company? Like the situation in the first half of this year, not to mention executives, as the company’s internal employees, they all know that the company’s operating pressure will be very high, and the quarterly results will not look good.

Perhaps it was because the market saw executives run away, causing speculation about explosive performance, so they rushed to run, which brought the stock price down endlessly.

In short, the collective insistence of executives at this node is very hateful.

This topic has 6 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/6509603082/229486604

This site is for inclusion only, and the copyright belongs to the original author.