In the era of #digital economy, which investment directions will benefit? #

I remember that when the words “digital economy” and “counting in the east” exploded on the Internet, it was still in February of this year.

After I carefully read the “14th Five-Year Plan for Digital Economy Development” issued by the State Council on January 12, 2022, I began to vaguely feel that the “digital economy” may really be the next new energy source.

Let’s go through the key points of the digital economy development plan first.

First, attach the link of the State Council. You can read the “14th Five-Year Plan for Digital Economy Development” when you have time.

In the opening paragraph, the figure highlights the strategic position of the digital economy:

In addition to the “Digital Economy Development Plan”, the outline highlights the strategic position. In fact, in the entire “14th Five-Year Plan”, we can also see the emphasis on the “digital economy”-in the “14th Five-Year Plan” economic development indicators , there are Twelve projects have clearly written specific goals for 2025, among which is the “digital economy” : the proportion of the added value of the core industries of the digital economy to GDP will increase from 7.8% in 2020 to 10% in 2025.

Well, after the strategic position is emphasized, the following is the “reading comprehension” level to see the key points.

I don’t know how you feel after reading “Planning”. Anyway, the key point I felt after reading it was: there are still many problems and challenges, hurry up and make up for the shortcomings!

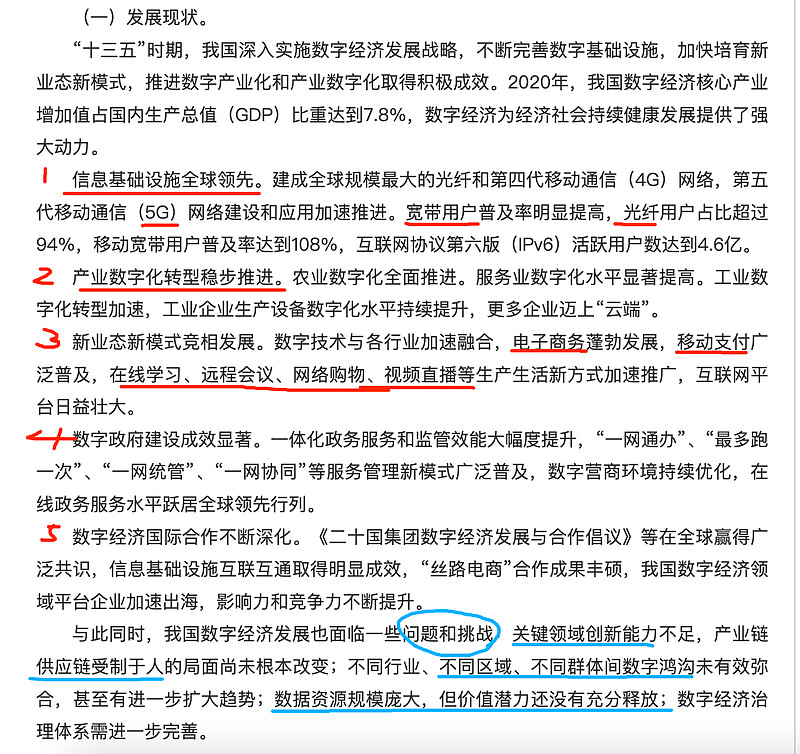

When stating the current situation of development, he first praised several areas of good development: information infrastructure (5G), industrial digitalization (smart agriculture and industry), empowerment of all walks of life (e-commerce/mobile payment/remote conference/video live broadcast) .

The achievement is good, but the real point is often the “but” that follows:

Issues and Challenges:

1 Insufficient innovation capability in key areas

2 The supply chain of the industrial chain is controlled by others

3 There are gaps in the development of different regional industry groups

4 The value potential of huge data resources has not been fully released

5 The governance system needs to be further improved

In response to the current three main challenges, the policy proposed coping strategies

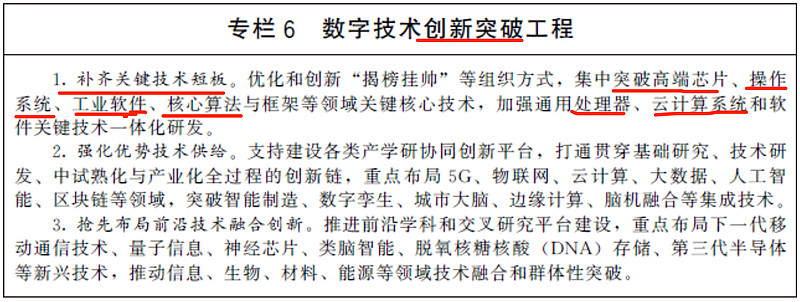

1. Insufficient innovation ability in key areas➡️Make up for shortcomings ( high-end chips, operating systems, industrial software, basic software , etc.)

2. The supply chain of the industrial chain is controlled by others➡️ Develop core electronic components (I understand the focus is on semiconductors )

3. There are gaps in the development of different regional industry groups ➡️East and West count (cloud computing, big data, information security , etc. )

In addition to the 14th Five-Year Plan, more favorable policies have been introduced intensively

For example, many stocks in the ” software and network security sector ” strengthened last Friday!

Recently, there have been frequent news about the “cybersecurity” sub-section.

(1) On September 14, the Cyberspace Administration of China issued the “Notice on Publicly Soliciting Opinions on the “Decision on Amending the Cybersecurity Law of the People’s Republic of China (Draft for Comment)”, intending to focus on increasing penalties for some illegal acts And expand the scope of application of penalties – this is the first revision since the “Cyber Security Law” was officially implemented in 2017.

(2) The Ministry of Industry and Information Technology recently stated that in the next step, relevant departments will promote the issuance of policy documents to promote the development of the data security industry, and cultivate internationally competitive data security leaders and specialized and new “little giant” enterprises.

(3) On September 15, local time, the European Union announced the draft Cyber Resilience Act, which states that smart devices connected to the Internet will have to assess their cybersecurity risks and fix them.

(4) Regarding new energy vehicles and intelligent connected vehicles, Xin Guobin, vice minister of the Ministry of Industry and Information Technology, also stated on September 15 that regulations and management requirements should be further refined, the standard system should be continuously improved, and network security and data security supervision should be strengthened.

So, what exactly is the big sector of the “digital economy”?

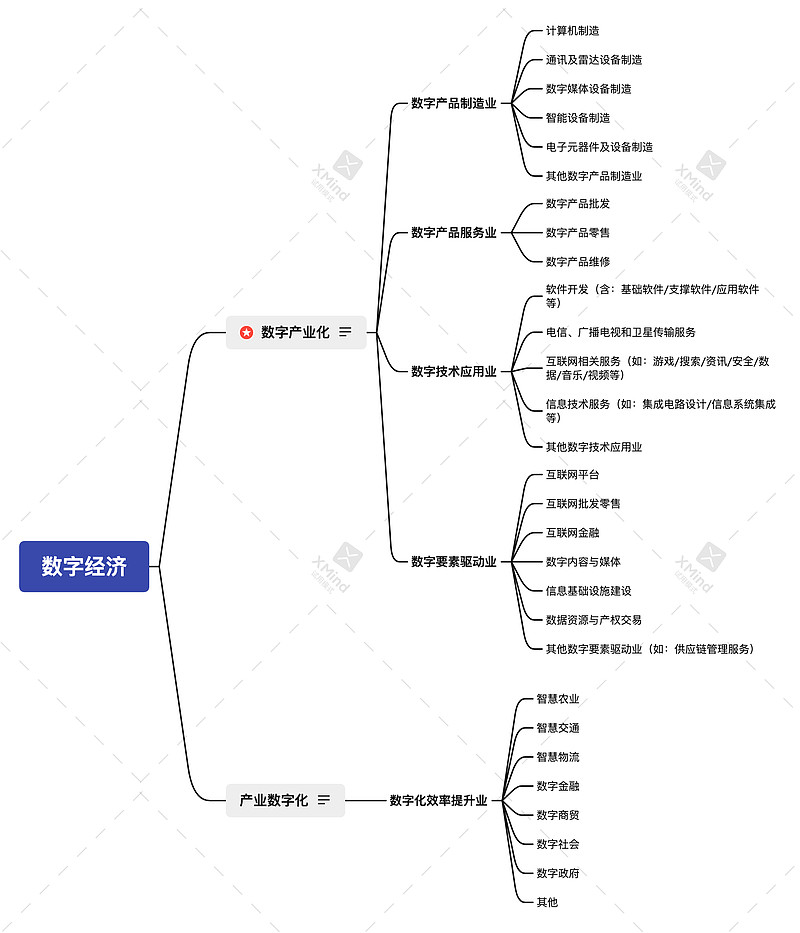

I feel that “digital economy” is a fairly broad concept in the investment sector. It mainly covers two major directions: digital industrialization & industrial digitization.

—Digital industrialization : It is the basic part of the digital economy, mainly referring to the information industry, including electronics, communications, the Internet, software, etc., which is what we often call the TMT industry, which constitutes the foundation of the digital economy.

—Industry digitization : The application of digital technology in traditional industries will increase output and improve efficiency of traditional industries. All walks of life can achieve transformation and upgrading through this, and investors can also obtain better returns.

So just how broad is the digital economy?

Let’s take a look at the “Statistical Classification of Digital Economy and Its Core Industries (2021)” released by the National Bureau of Statistics

I briefly sorted out the industry categories: (Judging from the official document “marking stars”, the focus of this development should be “digital industrialization”.)

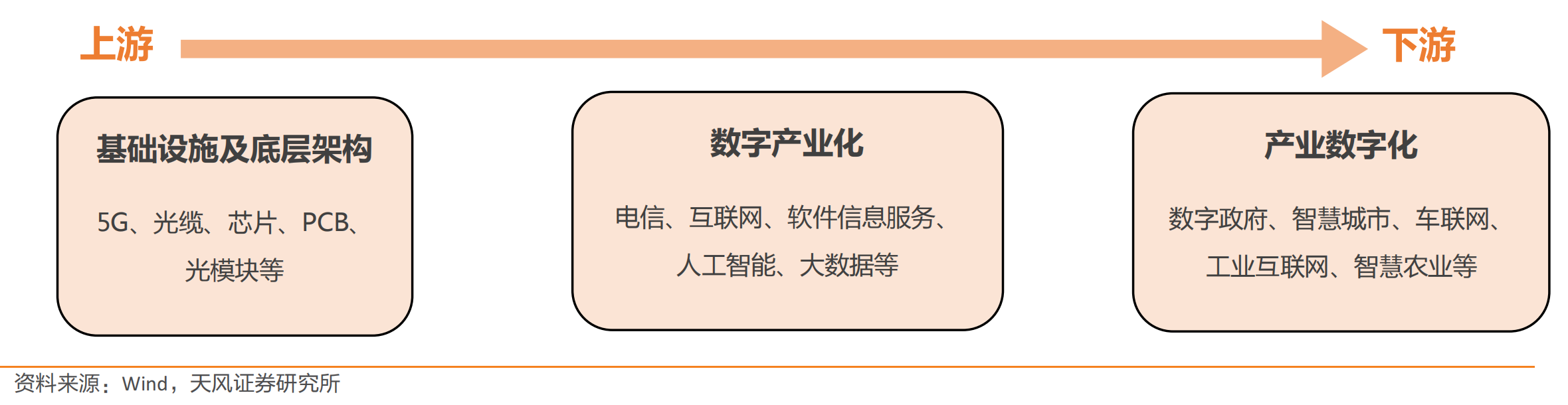

From the perspective of the industrial chain, there are also three layers: upstream ➡️ midstream ➡️ downstream

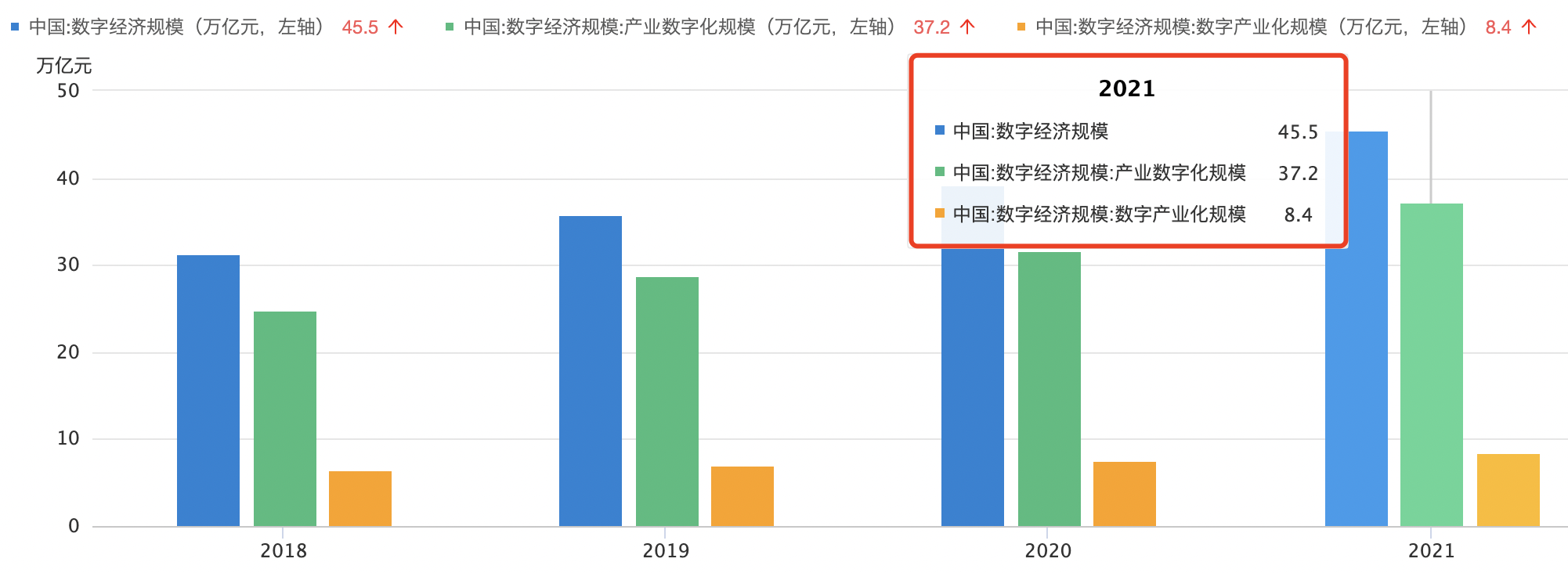

How has the digital economy developed in recent years?

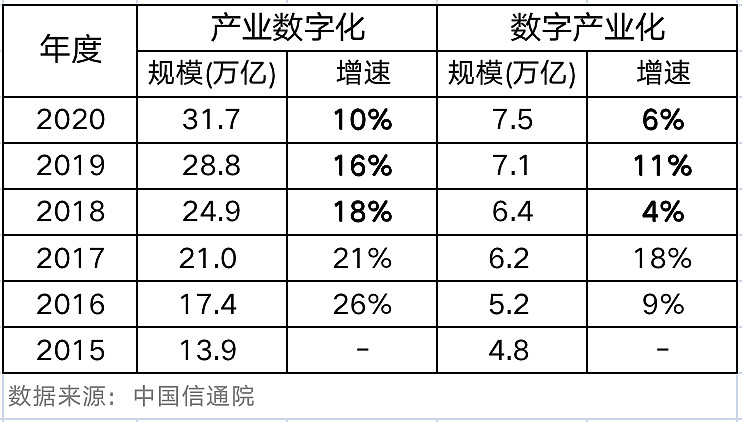

According to the data released by the “China Academy of Information and Communications Technology”, 80% of the total is “industrial digitalization” , while the “digital industrialization” part that wants to focus on development this time only accounts for 20% (ie 7.5 trillion).

Moreover, judging from the growth rate in the past three years, China’s “digital industrialization” is indeed quite short-circuited: the average annual scale growth rate is only 6.8% – this growth rate is in line with the growth rate of “high-prosperity growth” industries in our perception. The speed difference is far. However, any industry has a process from the “introduction period” to the “explosive period”. For example , in the electric vehicle industry from 2013 to November 2019, the electric vehicle industry was in the introduction period in these 6 years (limited to a certain technology, and the market did not recognize the product due to lack of good experience). Changes were repeatedly hyped 3 times at this stage, and later all were falsified because the penetration rate was less than 10%. However, once the penetration rate reaches about 10%, the industry will enter the outbreak period after a long introduction period.

“Digital industrialization” is divided into four layers from the perspective of the industrial chain:

The first layer: the lowest basic hardware facilities, such as electronic components (such as semiconductors)

The second layer: infrastructure, that is, building a layer of infrastructure on basic hardware, such as cloud computing, Internet of Things, operating systems, etc.;

The third layer: application layer – Internet platform (such as: online car-hailing platform, etc.)

The fourth layer: integration with various industries. For example, companies that provide digital management, digital monitoring or digital operations for different industries (I understand Internet finance, digital supply chain management, etc.)

However, since we have only begun to emphasize “making up for shortcomings”, and this shortcoming may not be quickly made up with a little money and time, therefore, I am more in favor of a fund manager with a “digital economy” theme. The point of view: “For the technology industry, now may be the time for the gradual layout on the left side, and the stage of accelerated layout has not yet reached .”

Digital Economy ETFs: Mid-to-Large Growth Style

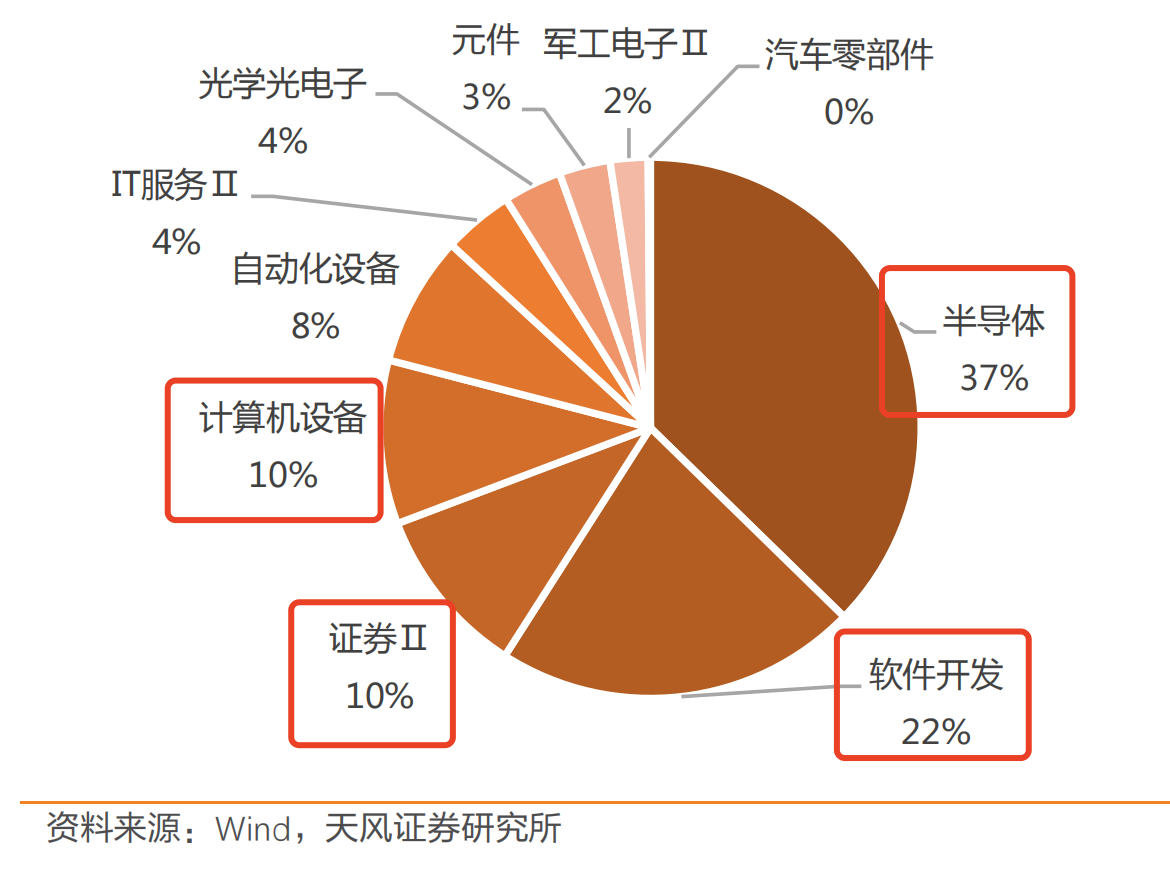

From the perspective of industry distribution, as of August 31, 2022, the top five weighted (Shenwan secondary) industries on the GEM are: semiconductor (37%) , software development (22%) , securities (10%) , Computer equipment (10%) , automation equipment (8%) .

From the perspective of industry proportion, semiconductors can be said to be absolutely heavy!

Friends who know me better should know that I have always been very optimistic about the semiconductor industry, and I have always been heavy on semiconductors.

Needless to say, the strategic significance of semiconductors to our country, about “solving the problem of stuck neck”, “domestic substitution”, etc., everyone must be tired of hearing it. I will tell you the actual situation.

First of all, we must admit that semiconductors are indeed in a “decline cycle”. The main reason is that the market demand for mobile phones, PCs, and tablets has declined, and the reduction of orders and prices is concentrated in consumer electronics, while the demand for automobiles is not enough to make up for the decline in consumer electronics.

So, where are you currently in the “down cycle”?

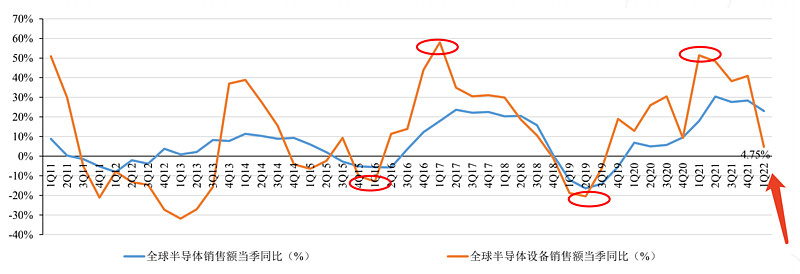

From the historical data of “Global Semiconductor Equipment Sales & Global Semiconductor Sales”:

The “year-on-year growth rate of semiconductor equipment sales” in Q1 of 2022 has dropped rapidly, but there has not been a negative number yet, that is to say: the current is indeed not in the end. Based on historical data, semiconductor equipment sales typically bottom/peak 1-2 quarters ahead of sales.

In other words, it is expected that the bottom of the current semiconductor cycle will be in the first half of 2023.

According to the rule of “the stock market usually leads half a year and starts to run”, the stock price is likely to start to rebound at the end of 2022, and with Davis double-clicking, this wave of rebound should be very rapid

In addition to semiconductors, there are 3 segments worth paying attention to

1. Operating system: In a computer system, the operating system is the core underlying basic software, responsible for controlling, managing, and scheduling the hardware and software resources of the entire computing system. At present, the process of localization of operating systems is accelerating. According to the prediction of Yiou think tank, the market size of domestic operating systems will increase from 3.33 billion yuan in 2021 to 5.62 billion yuan in 2023, with a CAGR of 30% . The popularization of domestic operating system ecology can be expected in the future. $China Software(SH600536)$ $Qianxin-U(SH688561)$

2. Database : The database is the basic core software of the computer industry, and the operation and data processing of all application software must interact with it. With the exponential growth of data volume in the Internet era, a large number of data analysis needs have been generated, and new opportunities in the database market have emerged. In 2020, the localization rate of the domestic database market is about 47.4%, and there is still some room for improvement in the future.

3. Industrial software : Industrial software is the precipitation and crystallization of industrial wisdom, the “soul” of the modern industrial system, and an important tool for an industrial powerhouse. In recent years, the scale of my country’s industrial software market has maintained rapid growth. According to the data of the China Industrial Technology Software Industry Alliance, the scale of China’s industrial software has increased from 72.86 billion yuan in 2012 to 197.4 billion yuan in 2020, with a compound annual growth rate of about 13.27. %. According to the forecast of the Prospective Industry Research Institute, the scale of China’s industrial software market is expected to maintain double-digit growth from 2021 to 2026, and the market scale is expected to reach 430.1 billion yuan by 2026. Although European and American companies have a strong first-mover advantage in the field of industrial software and occupy a dominant position in the domestic and foreign markets, with the overall accelerated development of my country’s Xinchuang industry, the localization of industrial software has a strong driving force and market space .

summary

The “digital economy” sector as a whole is still a relatively new concept. Therefore, there are actually quite few “themed funds” specifically called digital economy! Moreover, the few ones that are already in operation have been established for a very short period of time. Therefore, if you are optimistic about the digital economy sector, you can try $Digital Economy ETF(SZ159658)$ first.

@Today’s topic @snowball fund @snowball creator center #How should Christians respond when the market falls#

This topic has 6 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8687456694/230993656

This site is for inclusion only, and the copyright belongs to the original author.