The rebound in the stock market is just around the corner, and the questions I have encountered recently are:

I want to choose a medium-to-large quantitative private equity firm. Who has performed better this year?

This year is an interesting year for quantitative private equity, because everyone’s performance is no longer as good as it was in 2019-20, but the performance is very different.

For this, we performed a simple classification statistics:

1) Screen all quantitative private placements with a management scale of more than 5 billion;

2) Compare CTA, quantitative bulls, market neutral, CSI 500 Index Enhancement, and CSI 1000 Index Enhancement by category;

3) Prioritize the selection of standard products with a relatively long period of time and relatively complete net value, but there are still problems with the use of the net value of some products. If you find a problem during reading, you can refer to the table in the text, but actually different managers have different rules. Product design ideas, such as different net worth performance of cta leverage settings are not the same;

4) Comparing the four basic net worth data, and coloring the data higher than the average value, the more color blocks represent the better this year, the four data are all filled with color, representing the private equity in this strategy (products) ) has done a good job this year, and purely high returns are not a rational pursuit.

The data in this article may be wrong, the main source is Huofuniu database, for reference only, let’s start

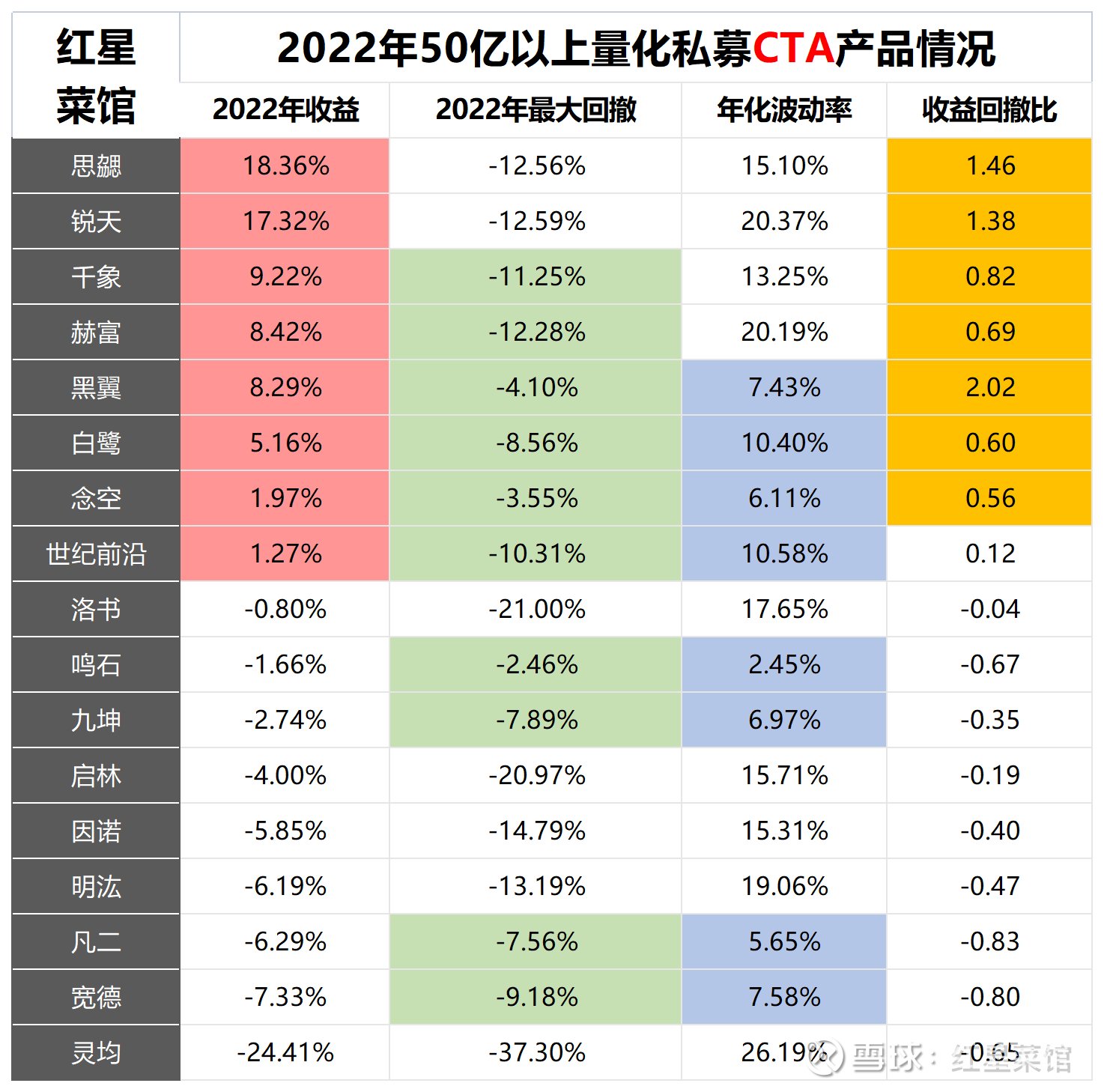

1. More than 5 billion quantitative private equity CTA products

CTA is a private equity management strategy that is very strict in terms of scale, so the “5 billion” standard here refers to the overall management scale of the company. than most.

details as following:

(The colored part is higher than the average value of the data in the same column)

There are only three companies that beat the tie value in all four items: Egret, Black Wing, and Niankong. Black Wing Zou Yitian is a very famous quantitative CTA veteran, and he has continued to maintain an excellent level this year. However, Black Wing’s CTA seems to have been in a state of shortage, and it is basically unavailable at present.

At the same time, the representative product of Egret is actually a multi-strategy product (Gulangyu series, which is relatively famous). The public net worth disclosure has not been able to find this leading product, and it is also in a state of shortage of quota. High-frequency short-to-medium-term trend, and Sixie CTA, which is the most profitable, is also a representative high-frequency intraday CTA, which basically represents a powerful direction of this year’s CTA market: hurry up, hurry up, and hurry up again!

The low-to-medium frequency trend means that after Luoshu’s success in the first half of the year, the four data items are all lower than the average. For the same reason of scale, Jiukun and Mingqiang, which cannot be particularly fast, have not performed well in the CTA product line.

However, it should be noted that Sixie and Ruitian, which are far ahead in terms of income in this group of private placements, are below average in terms of drawdown control and net worth volatility, which means that they have taken a certain amount of extra risk in their income this year. In addition, Sixie There are only two historical products left in the public data of Xie’s CTA products, and none of the newly issued ones have public net value. After inquiry, the main action this year is to transfer short-frequency products to the medium cycle. This kind of scale reduction, Black Wing Mingzhu, etc. seem to be doing this.

What is more surprising is Heifu and Qianxiang. Qianxiang is a very old trending CTA manager. Not to mention, most of Hefu’s products failed at the beginning of this year, including CTA:

(At the beginning of the year, the commodity market rose sharply, and the net value of HEFT’s CTA products turned downward)

However, in the second half of the year, its net worth performance is much better than that of its peers. The visible treatment is that the reverse short order was successfully opened in advance when the commodity market fell sharply.

In general, among quantitative managers with an overall size of more than 5 billion, the annual average income of the CTA product line exceeds the average income of all CTA private placements.

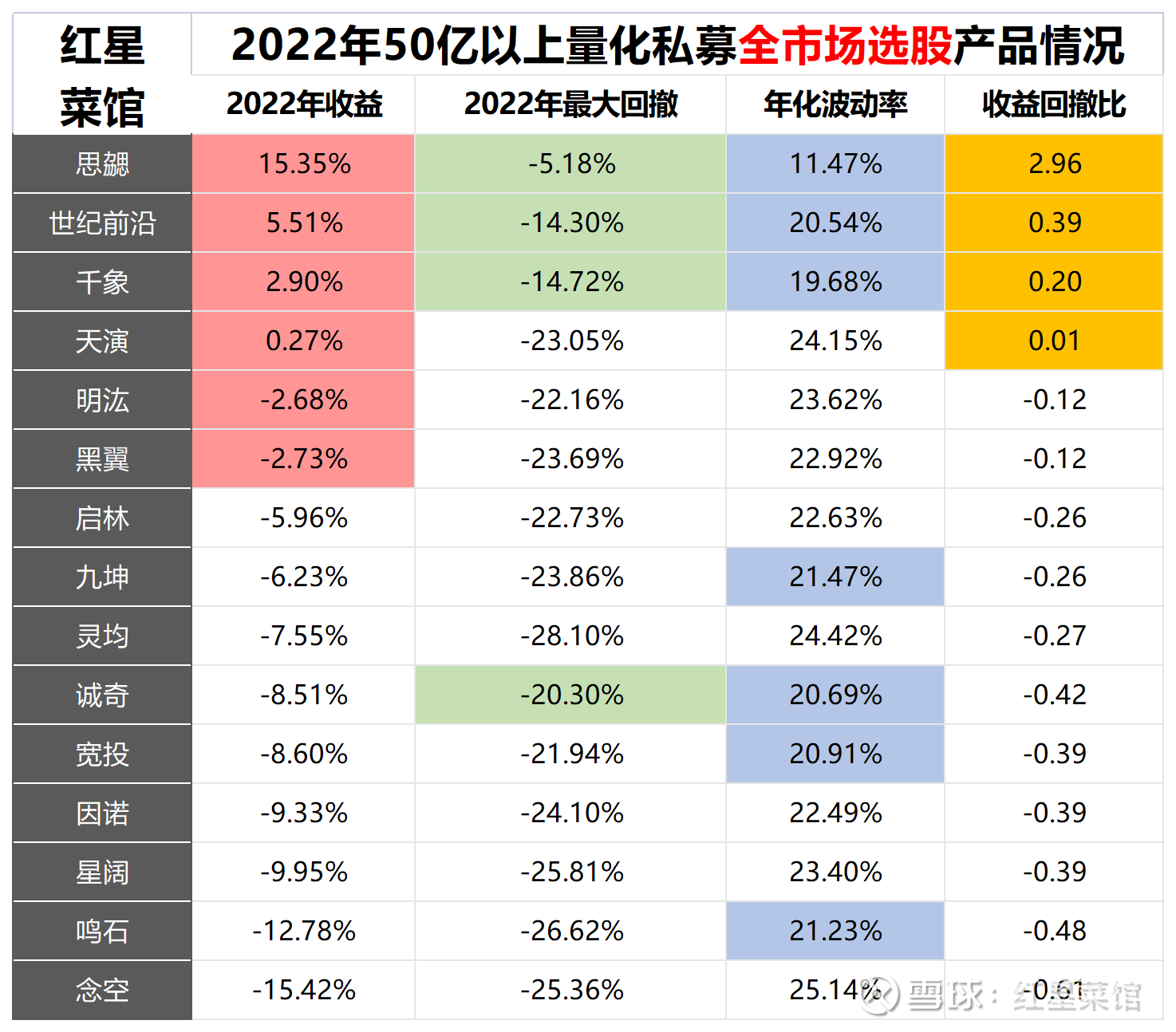

2. Quantitative private equity stock selection products of more than 5 billion in the whole market

Stock selection in the whole market is also known as “air index growth”. This year is the hardest hit area. The overall performance is far behind the index enhancement strategy with enhanced benchmarks. In the final analysis, the quantitative research process pays attention to “excess” and “comparison”. Originally, the situation is as follows:

There are only 7 private equity companies that beat the average, and managers who beat the average in all four categories: Sixie, Century Frontier, and Qianxiang, all of which started from CTA or high-frequency arbitrage. Take the small and medium-sized micro-quantity Jingqi we are concerned about as an example. This year’s performance level is also the average of all four data, but the current 2 billion scale still has 800 million CTA self-operated market.

Why does this feature appear? Because there is no accurate index benchmark for quantitative stock selection in the entire market, it is not enough to rely solely on the stock alpha model to determine whether it is doing well or not. Managers who started out as CTAs naturally have mature timing models to choose from and learn from, supplementing that beta may plummet. product weakness.

But we all know now that pure timing advantage is difficult to sustain, especially in the case of large-scale management, where should the market-wide stock selection products go? Try to choose the timing type? Or stick to stock selection? I don’t have a standard answer at present, as long as the composition of the strategy is special enough, it may emerge suddenly.

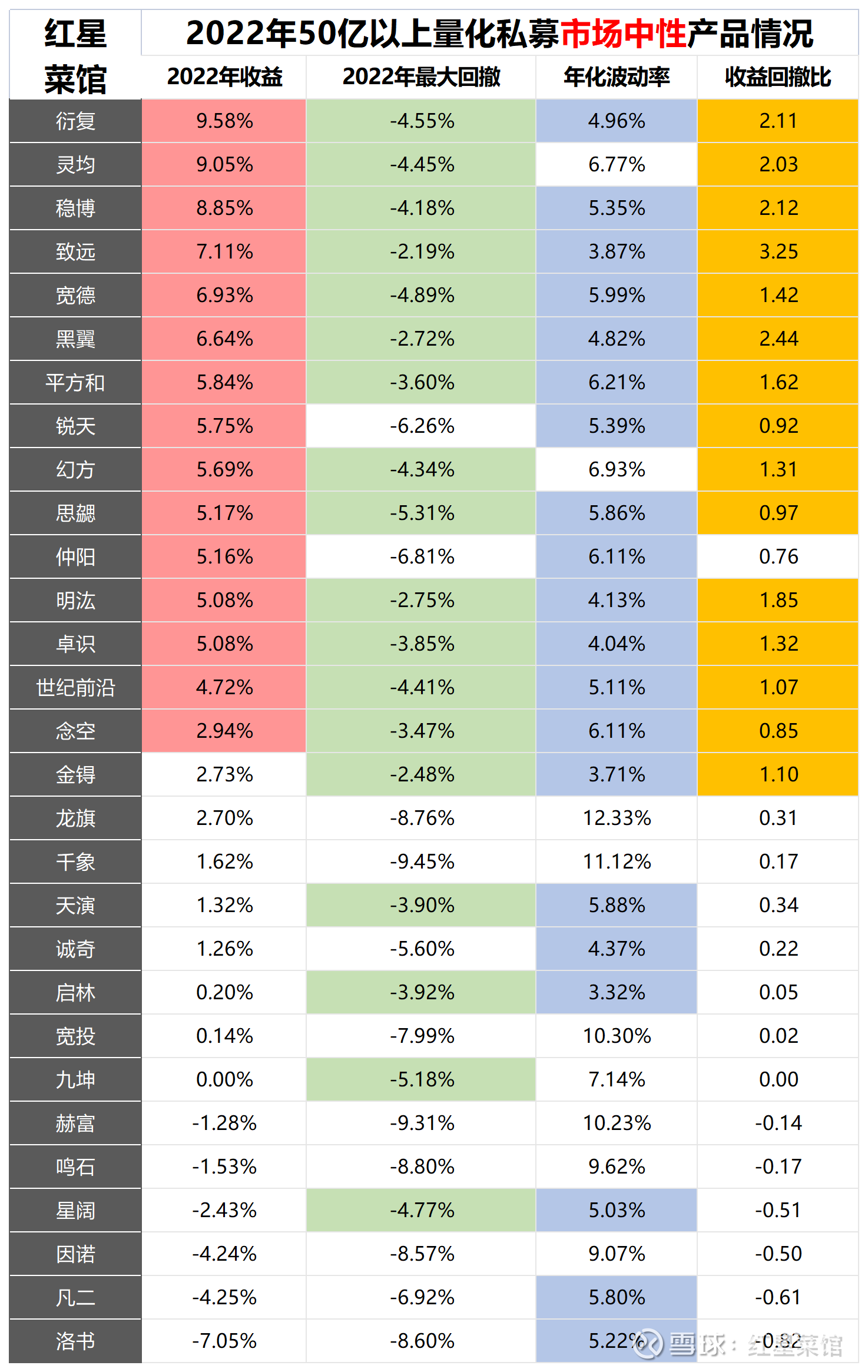

3. Quantitative neutral products in the private equity market of more than 5 billion

Market-neutral products are very difficult to make this year. The main reason for the difficulty is not only the excessive and general decline of the quantitative stock selection model, but also the extremely volatile stock index futures discount environment.

This year, the discount amplitude of stock index futures exceeds 30%. For market-neutral products, the hidden losses contained in this are really not small.

The overall situation is as follows:

No quantitative manager with more than 5 billion yuan can gain more than 10% of the market-neutral products this year. This is completely different from the impression of neutral products with 15%, 20% or even higher in previous years. In fact, this is the market-neutral product The standard normal for is:

A private equity product with a long-term return expectation of 8-10% for investors.

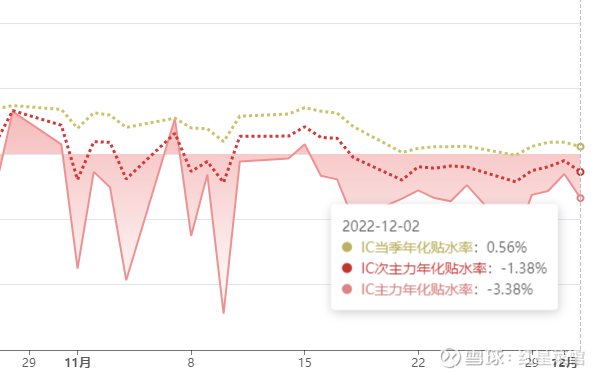

Because the market neutral income = excess income of the stock selection model – hedging cost, in the former good expectation of 15%, the hedging cost must fall between 5-7% to meet the long-term expectation. This year’s stock index futures have lower hedging costs The market environment accounts for very little, and only appears at the beginning of the year and in the near future.

At present, it can be said without a doubt that it is a gold allocation environment for market-neutral strategies, and the hedging cost is very low. Unfortunately, the stock market point is also very low:

(The hedging cost of market-neutral products is low in the near future, and the benefits will be released later)

In the private placement of market-neutral products, the four data are much better than the average. Some well-known market-neutral products have performed well. :

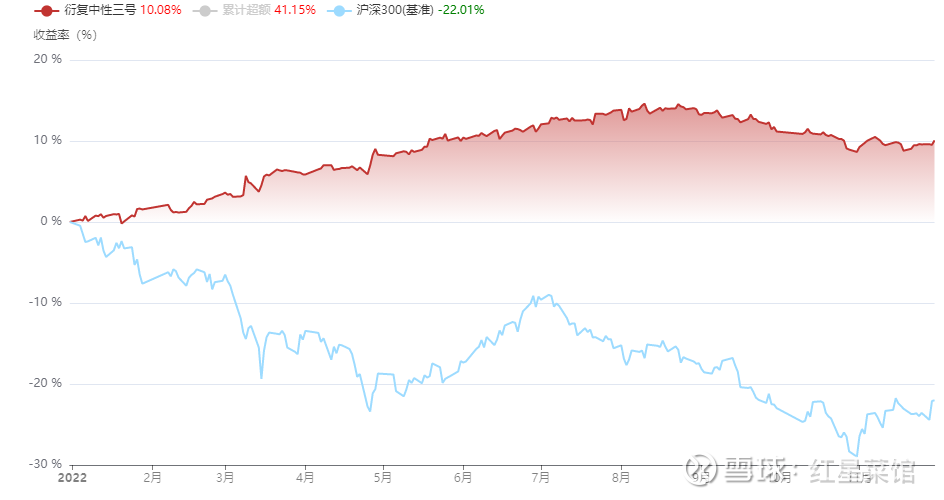

Market-neutral gains have been shrinking so far in August.

(Yanfu’s market-neutral products are in the biggest retracement of the year after the first half of the year)

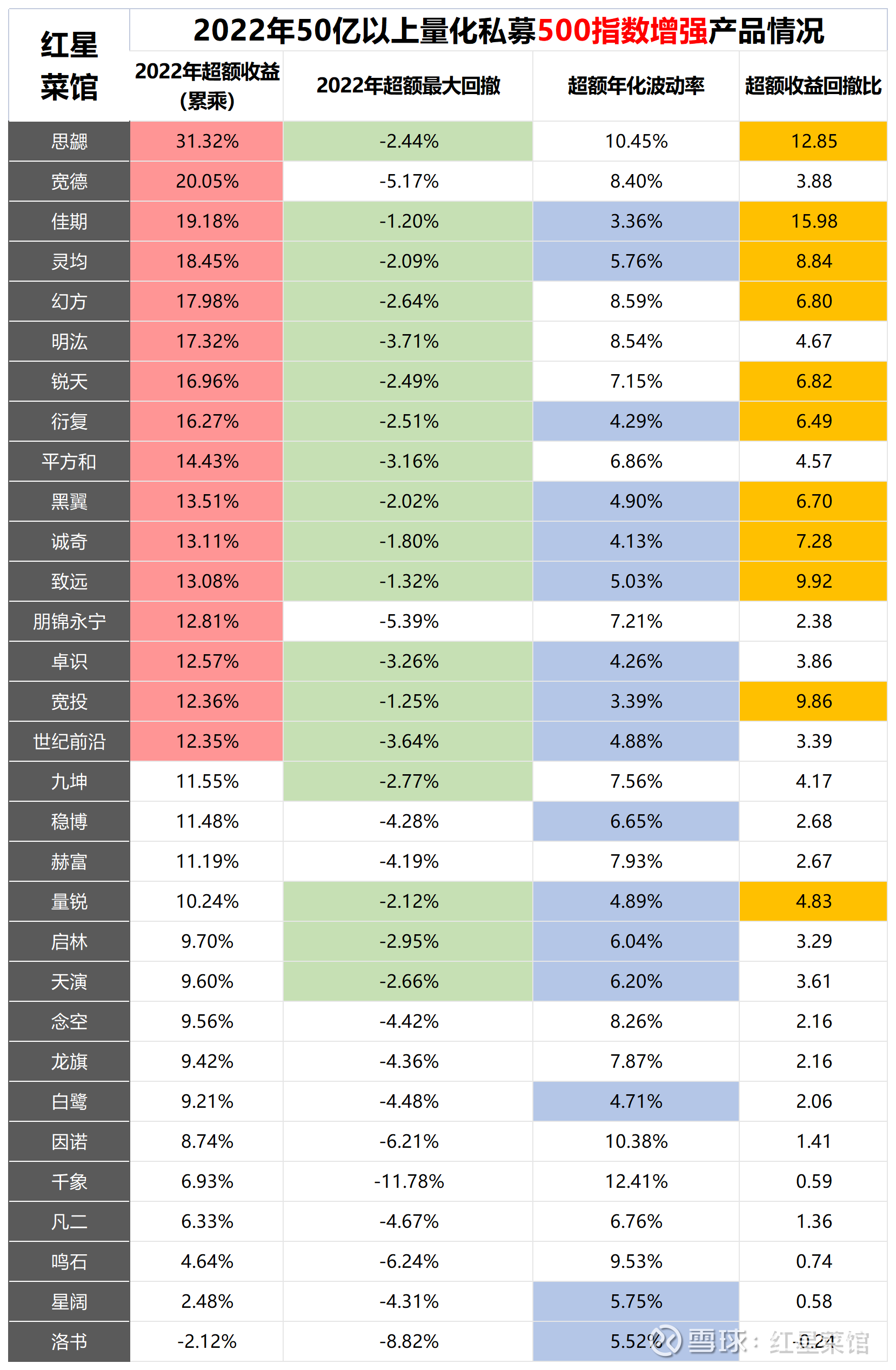

4. More than 5 billion Quantitative Private Equity 500 Index Enhanced Products

The backbone products of quantitative private equity are here, and the situation is as follows:

Sixie topped the list again. This should be the strongest quantitative private equity candidate this year. We had an exchange with him in the first half of the year. The record is as follows:

Ten Billion Interview | Wu Jiaqi, Founder of Think Investment

Si Xie’s index increase is different from most practices in that it embeds two modes of timing judgment and concentrating on defensive stocks when the trend is downward. How to understand this concept? That is, Sixie index enhancement products have undergone a layer of strategic transformation. Just like Jiukun constantly expressing the advantages of small market capitalization, Sixie has also been expressing his own understanding of unique risk factors. This is actually very similar to a subjective long-term stock fund manager difference in understanding.

What is more unexpected in the list is that the ultra-large-scale managers: Mingluo, Magic Fang, and Lingjun’s 500 index-increased products performed well, but they did not appear to be getting bigger and weaker. This may be the investment of quantitative private equity People need to constantly understand new changes, and scale is not the only criterion for quantifying the future judgment of private equity.

Among them, the excess retracements are relatively large: Kuande, Qianxiang, Luoshu, and Yinuo. Except for Kuande who exchanged the second excess return through a higher retracement, the remaining three are considered to have poor performance in excess control. This range The excess drawdown of is hard to understand at the factor-combination level….

However, this kind of out-of-control phenomenon can be explained from the liquidity factor link. Last year, the top three stars in excess were among them, but this year they are ranked at the bottom. According to the disclosure of the manager, this year lost about 7% of the liquidity factor. , that is to say, the market transactions are relatively light, and managers who rely on volume and price signals have more black swan crises.

This reflects the strength of the medium and low-frequency volume-price private equity fund. Although it did not beat the average, it still maintained an excess of 500 index growth of more than 10% in the very negative market impact, which is really stable.

Review of previous interviews:

In-depth interview with Jin Ge Liangrui——to help you better understand quantification

Other amazing 500-point increaser products include: Zhiyuan, Zhuoshi, and Century Frontier. These three companies do have their own characteristics.

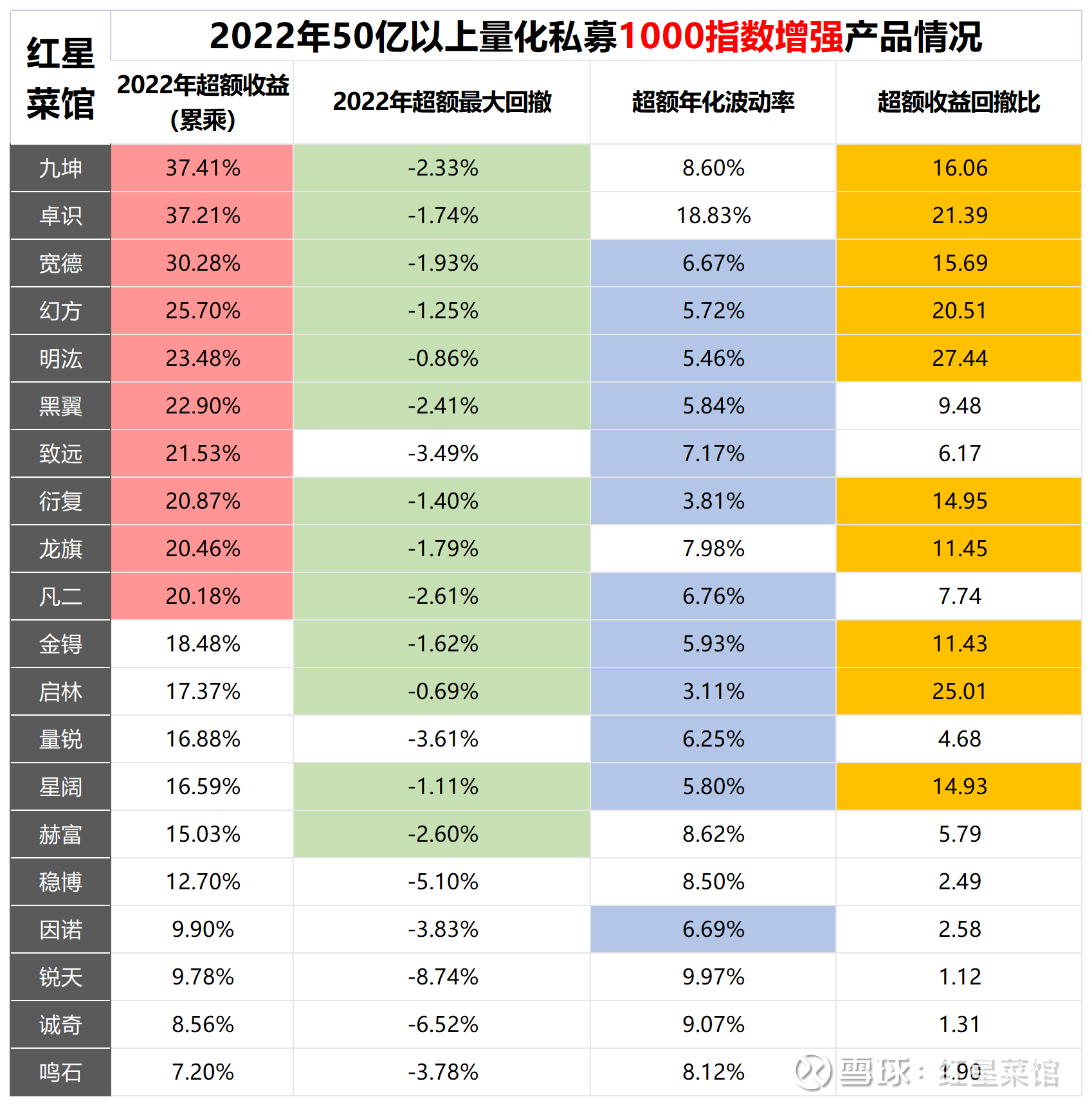

5. More than 5 billion Quantitative Private Equity 1000 Index Enhanced Products

This year’s 1000 Index enhanced quantitative private placement is the biggest breaking point, with high excess returns, rapid transactions, and a small decline in the index itself. The product data is very eye-catching:

Jiukun has won the 1000 Index Enhancement Crown of more than 5 billion managers. As a quantitative private equity that has long promoted and guided the advantages of small market capitalization, this year is indeed a big year for its strategy. The scissors gap between large and small caps has reached an outrageous height:

(Jiu Kun’s CSI 1000 Index strengthens the outrageous annual excess curve, trotting all the way, the king of small market capitalization?)

In the comparison of 500 index-increased products in the previous link, among ultra-large-scale quantitative managers, only Jiukun’s 500 excess data did not beat the average, but on the contrary, it has a very obvious advantage in 1,000 index-increased products. This phenomenon is also reflected in Xingkuo. Xingkuo’s 1,000 index growth performance is good. Although it is lower than the average value of 5 billion, it also maintains a normal excess level of 16%, which is very different from the weak annual excess performance of 500 index growth.

I recently made some inquiries and inquiries from managers. Generally speaking, it is the problem of understanding differences between different managers. Whether to open higher factor risk exposures for small market capitalization and other parameter ratios determine the excess of the 500 and 1000 index enhancements. The size of the difference.

In the list, factors such as the strengthening of the unissued 1000 index of Si Xie and the short release time of Century Frontier products have been eliminated. There are also a few managers who have broadly beat the average data in the five product lines. The representative ones are : Black Wing, this year has indeed done well in all strategic lines, with almost no weaknesses.

However, among the 1000 index-enhanced products, there are not many managers who beat the average with all four data. There are only four managers, Kuande, Magic Square, Mingluo, and Yanfu. First, this is because the underlying model of quantitative private equity will not be 500 or 1000, the underlying is the same, and what changes is the factor combination, strategy design and parameters.

Among them, the two quantitative private equity funds that are relatively inconsistent are Longcheer and Faner. The excellence of the two types of index increase products is very different, and it should be that more risk factor exposure designs have been done.

—————————

small summary

The scale of more than 5 billion is really not bad this year. Last year, it was a bit hurt to find a small scale this year.

@ @ Fund Fengyun Lu @ @ Today’s Topic

There are 3 discussions on this topic in Xueqiu, click to view.

Snowball is an investor social network where smart investors are all here.

Click to download Xueqiu mobile client http://xueqiu.com/xz ]]>

This article is transferred from: http://xueqiu.com/8915001532/236947068

This site is only for collection, and the copyright belongs to the original author.