“Without collagen, half of the actresses would not be able to live.” Big S once wrote this in “Beauty King”. After hyaluronic acid, what will be the next “super raw material” in the medical aesthetics circuit?

Collagen will probably be the answer given by most investors.

Collagen (collagen) was discovered by humans in 1865, and the first collagen filler (Shuangmei) entered the Chinese market in 2009. Collagen, which has experienced a long history, is not a new concept from being recognized to being applied.

Since entering 2022, judging from a series of moves in the market, the commercialization of collagen seems to be accelerating. Juzi Bio (02367.HK), Fuerjia, Chuanger Bio, and Jinbo Biology successively sprinted for listing, vying for the “first share of collagen”. In the end, Juzi Bio was the first to ring the bell for listing, and its market value once exceeded HK$30 billion.

On the other hand, a group of medical beauty and skin care giants are not to be outdone. Marubi (603983.SH)) has cooperated with Jinan University to launch several collagen series products. Bloomage Biotech (688363.SH) acquired Yierkang Biotech, which has been in the collagen market for several years, for 233 million yuan. The beauty giant Shiseido’s first investment in China is to focus on collagen raw material company Chuangjian Medical.

Pharmaceutical companies are also “ambitious”. Jiangsu Wuzhong (600200.SH) has started the research and development of recombinant collagen-related products. In October last year, this pharmaceutical company introduced the biosynthesis technology of recombinant type III human collagen with triple helix and trimer structure from the United States.

Among the above-mentioned companies entering the collagen industry, the one that cannot be bypassed is Juzi Bio. Its founder Fan Daidi is not only known as the “Mother of Human Collagen”, but also leads the domestic substitution process of China’s collagen industry. market share.

Because the gross profit rate is comparable to that of Aimike, Juzi Bio is also regarded as the next “Medical Maomao”. However, if you carefully disassemble its operating performance and the competitive landscape of the collagen industry, the logic of the market’s optimism about Juzi Bio is that a good track is greater than a good company.

The article mainly answers the following three questions:

1. Why do giant creatures rise?

2. Why is it difficult for Juzi Bio to become the next “medical beauty”?

3. How do you view the current valuation of giant biotech?

In the medical beauty and functional skin care products industry, most entrepreneurial stories can be divided into two categories, one is scientists entrepreneurship. For example, the founder of Shandong Freda Chemical, the predecessor of Bloomage Biotechnology, is Guo Xueping, the “father of hyaluronic acid”;

The birth of Giant Bio is a typical entrepreneurial story of scientists.

Back to the beginning of the 21st century, Fan Daidi and his wife, holding 5,000 yuan of scientific research start-up funds, successfully prepared recombinant collagen in the laboratory through genetic engineering technology, which opened the prelude to the wealth creation of “collagen”.

The difference between the two types of stories is that one can use the first-mover advantage of technology to grasp the bargaining power in key links of the industrial chain and become a “water seller” who can make money lying down, while the other is to realize the commercialization of products with strong channel advantages landing.

And why can giant creatures rise? In summary, it is actually due to “luck + strength”.

An external environment that cannot be ignored is “luck”, and the collagen industry is currently ushering in a “golden age”. On the one hand, similar to hyaluronic acid, collagen is widely used in the two fields of beauty and health, and due to its dual attributes of “medical care + consumption”, it is expected to realize the possibility of “high unit price + high-frequency consumption”.

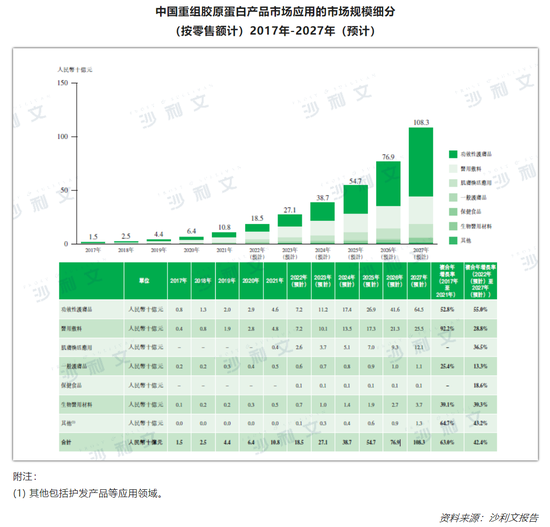

The broad application scenarios and visible “money scene” also make collagen be regarded as the next “hyaluronic acid”. According to Frost & Sullivan data, the market size of China’s collagen products has risen from 9.7 billion yuan in 2017 to 28.8 billion yuan in 2021, with an average annual compound speed of 35%. It is expected that the market size will approach 100 billion yuan by 2023.

From the perspective of subdivided tracks, the collagen track can be divided into recombinant collagen and animal-derived collagen, and the scale of recombinant collagen in Juzi Bio is expected to exceed that of animal-derived collagen, which is the “golden track” The new gold rush in China.

Referring to the data given by Frost & Sullivan, in 2021, in the Chinese collagen product market, the scale of recombinant collagen products will account for nearly 40%, and the proportion may continue to increase. It is estimated that by 2027, the scale of recombinant collagen products in China is expected to reach 108.3 billion yuan.

In contrast, it is estimated that by 2027, the scale of animal-derived collagen products in China is only expected to reach 65.5 billion yuan.

The reason why recombinant collagen is more optimistic points to the application layer, and the application space in the two major consumer tracks of functional skin care products and medical dressings is more imaginative.

In addition to the high prosperity of the track, the reason why giant creatures have become “favorite” in the eyes of capital, of course, also has its own strength.

Judging from the fundamental results alone, Juzi Biology has delivered a rather impressive report card, and its gross profit level is even close to that of Aimike, which is regarded as a “beautiful medical doctor”. As of the first half of 2022, Juzi Bio’s gross profit margin has remained above 80%. Although this level of gross profit is lower than Amic, it is higher than Bloomage Biotech and Bethany.

Specifically, how did giant creatures do it? Caijing Wuji believes that it can be analyzed from three aspects: technology, product and channel:

1. The first-mover advantage of technology holds the bargaining power in the industrial chain

The high gross profit of Juzi Bio actually comes from its mastery of the bargaining power in the collagen industry chain, especially in the upstream preparation technology. Similar to Bloomage Biotechnology’s mastery of the preparation mode of hyaluronic acid, Juzi Biotech mastered the extraction and preparation of genetically recombinant collagen in 2000, and a few years later relied on the recombinant collagen technology to obtain the industry’s first invention patent authorization in China .

At that time, Chuanger Bio was established less than three years ago, and it was seven years before Fu Erjia moved to the skin care track. Therefore, the breakthrough in preparation technology not only allows Juzi Biotech to enjoy technological dividends, but also establishes a first-mover advantage for later commercialization of products.

2. Create high-repurchase hit products

Dismantling the business structure of Juzi Bio, its main revenue contribution comes from the support of professional skin care products, of which the two majors are “Kefumei” (accounting for 59%) and “Kelijin” (accounting for 33%) The skin care brand is the core, and the revenue of the two brands accounts for 92%, which is a veritable “cash cow”.

According to the prospectus of Juzi Biology, in 2021, the overall repurchase rate of Kefumei and Kelijin on Tmall will be more than 30%. The cosmetics industry has an average repurchase rate of 20%.

The reason why Kefumei and Kelijin can have such a high product viscosity, in Caijing Wuji’s view, is that the “mechanical brand” products of medical dressings are scarce, because the production standards are stricter than ordinary skin care products. , the halo of “medical beauty” on the head, so it is more attractive than ordinary “makeup brand” products.

On the other hand, based on the logic of large single products, Giant Biotech has iterated its categories and ingredients around Kefumei and Kelijin. While enriching the product matrix, it has strengthened product competitiveness and further increased the repurchase rate.

According to the statistics of Juzi Bio and China Merchants Securities, the number of SKUs of the two major brands of Kefumei and Kelijin has reached more than 90. In addition to the main product forms of dressing and film products, they have also launched a variety of products such as water, essence, lotion, and spray. Form products.

According to the incomplete statistics of Caijing Wuji, and according to the data of the Tmall platform, the number of SKUs of Chuangfukang and Chuangermei, the two major brands of Chuanger Bio, is close to 60, which is far lower than that of Giant Bio.

A rich product matrix and diverse SKUs are actually a typical approach to consumer goods. From technology to products, with the help of high-repurchase fist products, Juzi Biotech has successfully taken the lead.

3. Low-cost channel model

In addition to technology and products, compared with Bloomage Bio and other channel systems that focus on online direct sales, Juzi Bio’s channel model is characterized by “medical institutions + mass consumption”. From the perspective of dismantling, there are actually two types: online is a direct sales model based on e-commerce platforms, while offline is “direct sales + distribution” for public hospitals, private hospitals, chain pharmacies, offline CS and chain stores.

Juzi Bio relies heavily on distribution channels. As of 2021, the sales channel revenue of Juzi Bio dealers will still account for more than 50%, and among them, Xi’an Chuangke Village E-Commerce Co., Ltd., the largest distributor, will account for nearly 30% of the revenue .

Reliance on distribution channels is the positive side of a coin. On the positive side, different from the high marketing cost of the direct sales model, because the dealers are relatively stable, the cost is lower; but on the other hand, the impression of “micro-business” brought about by the sales model of Xi’an Maker Village makes the brand image of Juzi Bio Always controversial.

Previously, according to Fenghuang.com, the Maker Cloud Business Platform released by Xi’an Maker Village adopts a hierarchical agency model. If an individual wants to become an agent at the lowest level, he needs to pay 12,000 yuan and enjoy a 3.5% discount on the purchase price and promotion sharing. , and at the same time have the power to invite others to join.

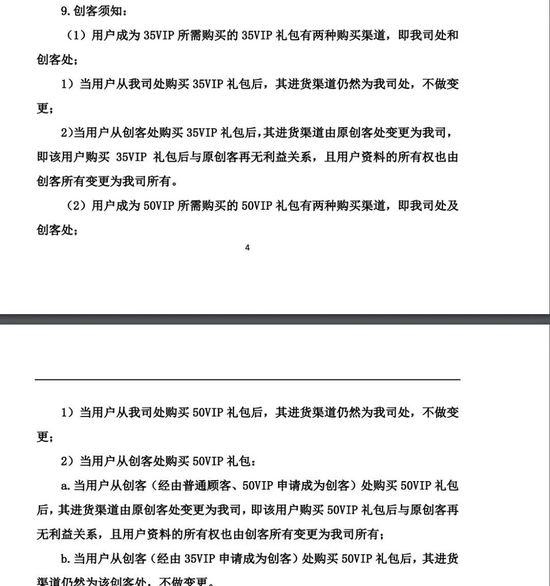

Caijing Wuji logged into Maker Cloud Business (the website of Xi’an Maker Village) and found that the “Maker Notes” proposed in its Maker Agreement also mentioned two purchase channels: 35VIP and 50VIP.

Screenshot of the Maker Agreement on the official website of Maker Cloud Business

It is worth mentioning that, as the largest distributor, Xi’an Maker Village itself was established by Fan Daidi’s husband Yan Jianya, and then transferred all the shares to Ma Xiaoxuan in 2017, and Ma Xiaoxuan was the general manager of Juzi Biotech.

Although there are controversies about the distributor channel, it is undeniable that the rise of Juzibio is not accidental by virtue of “luck + strength”.

But outside of the halo of the track, the profitability of giant creatures has actually been declining. From 2019 to the first half of 2022, Juzi Bio’s net profit fell from 60% to 43%.

On the surface, the decline in profitability stems from the usual practice of “marketing for sales” by medical and beauty concept stocks, but in essence, it actually stems from the deep-seated worries of giant biotech.

1. The dependence on a single brand is large, and the second curve has not yielded results

The “big single product strategy” is very common in medical beauty and skin care companies, such as the “Hey Body” of Aimike, the “Moisturizing Beauty” of Bloomage Bio, etc. The key to measuring the success of this strategy is that large Whether the single product can maintain a sustained revenue growth rate, thereby driving revenue growth.

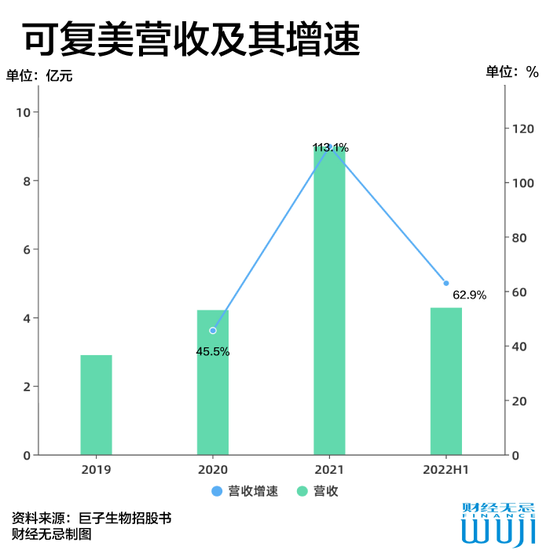

As a large single product that accounts for nearly 60% of revenue, Juzi Bio is very dependent on Kefumei, but from the financial report data, Kefumei’s revenue growth rate is declining, from the triple-digit growth rate in 2021 dropped to 62.9% in the first half of this year.

While the growth momentum of large single products is sluggish, other businesses of Juzi Bio have not yet possessed the ability to become the “second curve”. Taking the functional food brand ginseng as an example, in 2021, the revenue of this business will only account for 3.2%.

2. The price system is chaotic and channel control is insufficient

Compared with the direct sales model, Juzi Bio’s dealer model tests the source manufacturers’ control over channels. Although the marketing cost of the offline distribution model is local and stable, Juzi Bio, which started off relying on offline distributors, is currently facing a new channel crisis.

The first is the confusion of the price system. According to a first-level agent of Kefumei who sent the latest agent price of Kefumei to Caijing Wuji, the market price, bulk batch and box-up supply prices are all different. The agent said: “The official of Fuerjia can check Our power of attorney, because Kefumei signed a contract with the company, it has not been made public.”

A screenshot of the price list provided by an agent

Caijing Wuji learned that in recent years, in order to improve channel control, especially in terms of online price control, Juzi Bio has fined some distributors: “The starting point is 50,000, and the agency qualification will be permanently cancelled.” On the other hand, In recent years, Juzi Bio has also gradually increased the proportion of online direct sales, which will inevitably affect the relationship between distributors and manufacturers.

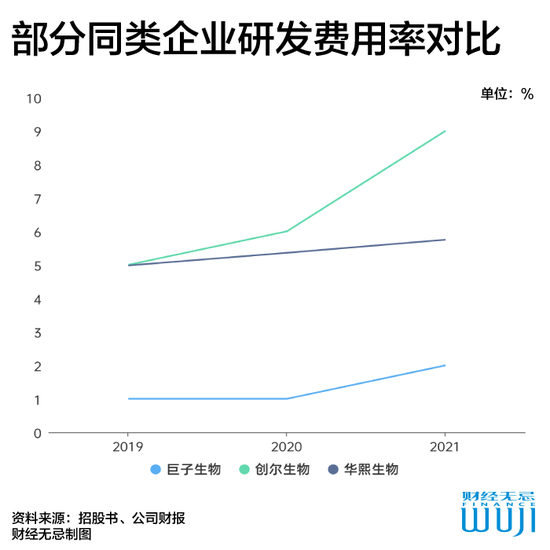

3. Technology does not have “monopoly”, and R&D does not invest

To review the development history of the “leading hyaluronic acid” Bloomage Biotech, breakthroughs in upstream preparation technologies are the key. Realizing the mass production of raw materials through technology, Bloomage Biotech has been able to continuously expand the downstream application fields, realizing the full coverage of medical aesthetics, medical materials, functional skin care and food.

In the field of collagen, the commercialization of technology is not as good as that of hyaluronic acid.

As of 2021, Juzi Bio’s recombinant collagen production capacity will be 10.88 tons per year, and the total designed production capacity will exceed 200 tons after IPO fundraising and expansion.

In other words, although collagen companies have made breakthroughs in preparation technology, whether they can achieve scale benefits through mass production like hyaluronic acid, thereby greatly reducing costs, is still a question mark.

In the production and preparation of collagen, the technical route is mainly divided into enzymatic hydrolysis and genetic engineering technology. Representative companies of the former include Taiwan Shuangmei, Chuanger Bio, etc., and the latter include Juzi Bio, Jinbo Bio, and Marubi Co., Ltd. Wait.

Although the enzymatic hydrolysis method is fast and the resulting product has stable physical and chemical properties, the cost of raw materials is high. Although the cost of raw materials required by recombinant collagen technology is low, due to the limited technical level of biosynthesis, the stability of the product after mass production is weak.

In addition to how to achieve larger-scale and low-volume production, the development of related cross-linking technologies also has room for optimization. Combined with the research and development technology reserves of domestic collagen leaders, the cross-linking process is also the focus of competition.

In addition to breakthroughs in key technologies, the technological concentration of the giant bio known as “Huawei in the beauty industry” is not high. From 2019 to 2021, Juzi Bio’s R&D expenditures only accounted for 1.2%, 1.1%, and 1.6% of the total revenue for the same period. American customer is 7%. Chuanger Bio, also in the collagen industry, will spend 22.22 million yuan on research and development in 2021, and the research and development expense rate will rise to 9.25%.

There is no doubt that collagen is a high-speed growth track, but at present, the logic of the market’s optimism about Juzi Bio is: a good track is greater than a good company.

According to the forecast of Tianfeng Securities, the A-share listed companies Bettany, Proya and Hong Kong-listed company L’OCCITANE, which are on the medical and cosmetics track with Juzi Bio, will have an industry average PE of 42/30/23 times from 2022 to 2024 , Consider giving Juzi Bio a 26 times PE in 2023. At present, the current giant biological rolling price-earnings ratio is 40 times.

Based on the above analysis and the forecast of the brokerage, the current Giant Biotech still has the possibility of being overestimated. While further consolidating its core barriers, it must answer the “three questions” about its own growth:

1. In order to enhance the influence of the C-end, the increase in the proportion of the online direct sales model will inevitably increase the pressure on the cost side. In the short term, its profitability will fluctuate. Will it fall into the trap of “increasing revenue without increasing profits”?

2. In the short term, functional food has not entered the second curve, and its gross profit is low. Juzi Bio’s current revenue growth still depends on collagen. With the intensification of competition in the industry, how can Juzi Bio improve its core competitiveness?

3. At present, consumer education in the medical beauty industry and functional skin care products is still immature, and the core that affects consumer decision-making is still product prices. How can Giant Biotech improve its brand influence?

On the one hand, in terms of functional skin care products, Fu Erjia is still the market educator of “medical beauty mask”, and has shown a leading edge in marketing strategy and product thinking.

On the other hand, in the field of collagen injections, Juzi Bio-related products have also entered the product development or clinical stage, but they do not have the first-mover advantage. At present, there are 4 main competitors of Class III collagen injection products that have been listed in China, namely Taiwan Shuangmei, Changchun Botai, Netherlands Hanfu and Jinbo Bio.

At the same time, Juzi Bio is also facing the problem of market education.

Xiao Yue, an in-depth user of medical aesthetics, told Caijing Wuji that people around him often get hyaluronic acid injections every few months, but not many choose collagen injections. “The price is still relatively expensive. I have friends who have done it, and basically all of them start at 10,000 yuan.”

A practitioner from a beauty agency in Changsha also told Caijing Wuji that with the same budget, many consumers would choose macromolecular hyaluronic acid, and in terms of collagen brand, there are more consumers who inquire about Shuangmei. The above-mentioned practitioners said that in order to speed up the market education of collagen injections, the organization is also offering large discounts through live broadcast and other channels to attract more users to the store for consumption.

Undoubtedly, although the giant creature that rides the wind of collagen has good luck, its subsequent strength is not enough to support its growth. At the moment when many players enter the collagen industry, it is bound to accelerate the business of this industry With the process of globalization and the pattern of competition, for giant creatures, hard times are yet to come.

References:

1. China Merchants Securities: “Comparison of Medical Dressing Industry: Fuerjia, Juzi Bio and Chuanger Bio”

2. Tianfeng Securities: “Leading the development of recombinant collagen based on research and development, and leading the professional skin care industry through accumulation and growth”

3. CITIC Securities: “Collagen, Playing the New Horn of Beauty and Health”

4. Zhongtai Securities: “Medical Beauty Segmentation: Path Selection for Restructuring Collagen Leaders”

5. Caijiandao: “The Eve of the Market Explosion: What Happened Behind the Explosion of the Collagen Market?” ”

(Disclaimer: This article only represents the author’s point of view, not the position of Sina.com.)

This article is reproduced from: https://finance.sina.com.cn/tech/csj/2023-01-12/doc-imxzxanh8949790.shtml

This site is only for collection, and the copyright belongs to the original author.