Original link: https://www.ifanr.com/app/1495003

In 2014, Apple launched Apple Pay, an online payment service, and 8 years later, more than 90% of retailers in the United States accept Apple Pay as a payment method.

Even with such rapid growth, Apple has not touched one of the most lucrative financial services — lending — for a long time, according to the Wall Street Journal , because Chief Executive Officer Tim Cook was concerned about the company’s reputation.

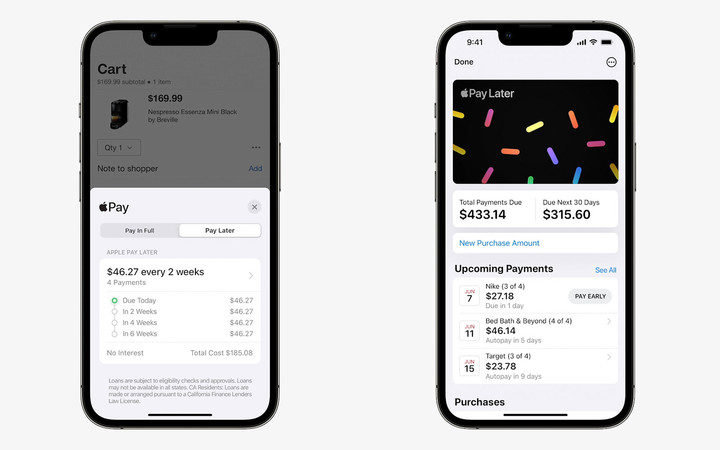

Until this year’s WWDC developer conference, the truth went in the opposite direction. Apple has launched Apple Pay Later, a buy-now-pay-later service, where people can choose to pay in interest-free instalments when they place an order, and pay in four instalments within six weeks after delivery.

Buy now, pay later is essentially a small loan service. In order to ensure repayment, Apple must review the credit and financial situation of consumers, such as transaction data related to Apple ID.

According to CNBC, Apple does not choose a mature financial institution like a bank for the Apple Pay Later service, but operates through a subsidiary.

▲ Apple Pay Later

In the past, Apple Pay was just a payment channel between consumers and banks. Now, with Apple Pay Later, Apple has transformed itself into a lender. This technology company is becoming more and more like a bank.

Buy first, pay later, let “young people” spend money like water

Buy Now Pay Later (BNPL) is a new type of payment method that has emerged overseas in recent years, that is, people can place an order first, receive the goods and then pay in installments. Generally, it is divided into 4 installments. No interest or handling fee is charged. Relatively low, mostly within $10.

The loose payment cycle, lower overdue fees, and the design for small-amount payments are much more relaxed than the payment terms of credit cards, which will naturally be welcomed by consumers.

In addition, Klarna, Afterpay, and Affirm, as well-known companies in the field of buy now, pay later, will settle the payment for merchants after consumers place an order, reducing the pressure on merchants’ funds.

With the dual support of consumers and merchants, buy now and pay later is like a tiger entering the flock, and it has quickly become a new star in the field of online payment. Adidas, IKEA, Zara, almost all the overseas brands you know are connected Buy now, pay later

According to the media SFgate , people spend an average of $365 on the buy-now-pay-later service Affirm, while the average single purchase price in the United States in 2020 is $100. The data is basically similar to that disclosed by companies such as Klarna and Afterpay.

Even if the single amount is small, the frequency is high, and the total transaction amount is also high. SFgate also mentioned that Generation Z (people born between 1995 and 2012) prefer to buy now and pay later.

The popularity of digital payment has greatly reduced the “ceremonial sense” of spending money. In the past, if you spent 10,000 yuan, you had to take out a thick stack of money from your bag, while digital payment only requires entering a few numbers.

The payment is faster, the perception of money is weaker, and the order is paid more.

Therefore, even though Klarna, Afterpay, Affirm and other buy-now-pay-later companies take a high percentage of merchants, there is still a continuous stream of merchants accessing the service.

Apple entered the buy-now-pay-later field and launched Apple Pay Later, both offensive and defensive.

▲ PayPal also launched PayPay In 4

Although Apple Pay is recognized as a payment method by nearly 90% of U.S. retail merchants and has access to corresponding services, merchant support does not mean that people will use it. Apple still has to face competition from digital payment companies such as PayPal and Klarna.

In March of this year, Apple acquired Credit Kudos, a financial company that can evaluate credit based on public bank data. This is also regarded by the industry as a preparation for entering the field of buy now and pay later to strengthen credit review, which is different from e-commerce platforms such as Shein. , Apple firmly controls the entire loan process in its own hands.

The iPhone and Apple ID accounts are connected to the application ecosystem and allow Apple to master a large amount of consumption data. It is almost natural to add it to the review process as a credit certificate.

According to the introduction on the official website, Apple will launch the Apple Pay Later service in the United States and other countries and regions this fall. People can pay in 4 installments after placing an order. There is no interest and other handling fees. Before using it, you must complete the review, but you need to pay attention. Yes, the service temporarily only supports in-app consumption and Apple Pay-based network consumption.

According to the Wall Street Journal, the initial limit of Apple Pay Later is $1,000, which is the same as the initial limit of most buy-now-pay-later. The small amount and short account period are also the reasons why Apple is uncharacteristically willing to enter the lending field.

The iPhone has a 51 percent share of the U.S. smartphone market, and Apple Pay Later is targeting them.

The high ownership of the iPhone and the ecosystem of supporting applications and hardware products have attracted a large number of users. Strong stickiness and ecological barriers allow Apple to more easily introduce these users into self-operated services such as Apple Pay Later.

Even with the successive sales of the iPhone 12 and iPhone 13, the revenue of services in Apple’s financial report continues to increase. Apple’s second quarter financial report for 2022 shows that service revenue reached $19.821 billion, compared with $16.901 billion in the same period last year. Apparently, Apple Pay Later is intended to add another fire to the service business.

![]()

▲ Apple previously launched Tap to Pay, two iPhones can be traded with a tap, further reducing payment costs

Regardless of tools or social apps, you can see “lending” services at almost every entrance of the Internet. As one of the pioneers of the mobile Internet, Apple is not exempt, even if Apple Pay Later is only a small loan.

Borrow money, you have to pay it back

For the promotion of Apple Pay, the buy now and pay later service is like a fuel-filled booster rocket. If you use it well, it will soar into the sky. If you don’t use it well, you can only suffer the consequences.

Companies like Klarna, Afterpay, Affirm, etc. are the best examples. Buy now pay later services have dominated the market for them, but when the trend faded, the problems became apparent

Klarna’s official website has a particularly expressive promotional photo, a coffee pot with four mouths, pouring coffee into four cups, like the definition of buy now, pay later.

▲ Picture from: Klarna

It’s just that not everyone’s wallet is big enough to fill four cups of coffee at the same time.

Debthammer, an institution specializing in loan research, conducted a random survey in the United States and found that nearly 32% of people could not repay the micro-loans of the buy-before-pay service, and some people even had to deduct cost deductions from water, electricity and rent costs, which affected their daily lives. .

Buy now, pay later, with flexible billing periods and extremely low overdue fees, greatly reduces the pressure to spend money, and people overspend before they know it.

How fun it is to spend money at the beginning of the month, how painful it is to pay it back at the end of the month.

Soon, the overdue tide triggered a series of chain reactions. The first one that could not sit still was the credit company. Credit companies such as Experian and Equifax expressed their hope that the consumption records of buy now and pay later would be included in personal credit reports.

Although Apple said that Apple Pay Later will not be included in the personal credit report, it is difficult to guarantee that it will not change in the future. After all, there is legislation outside the company. The British government said last year that it will establish stricter regulatory policies for companies that buy first and pay later.

Buy first, pay later is too popular. Internet technology has a natural advantage in high-speed communication. In recent years, similar services have gone global, and people have not had time to fully understand buy first, pay later, and they have already begun to overspend and overdue. .

▲ Are your express boxes also “piled up like a mountain”?

Although buy-before-pay is mostly micro-credit, it does not mean that the risk is lower than that of large-scale credit. If it is fully included in the credit report, it is very likely to affect people’s future mortgages, car loans, etc.

What consumers want is not only the convenience of ordering, but also the right way to spend money. In addition to encouraging consumption, service providers should provide more detailed and conspicuous risk warnings. Tell people that they’re not just spending in installments, they’re borrowing, and it’s important to repay on time, no matter how small the amount.

Apple has hesitated for several years outside the door of lending, and I believe it will not be ignorant of this truth. While convenient consumer payment services are good, the balance of income and expenditure is equally important.

This article is reprinted from: https://www.ifanr.com/app/1495003

This site is for inclusion only, and the copyright belongs to the original author.