In an interesting fund manager evaluation index , I introduce a reference index to evaluate whether a fund manager is left or right. Generally speaking, fund managers whose investments are on the left side are very scarce, accounting for about 10% of all fund managers (data source: answering three questions about fund managers ).

Compared with fund managers who trade in the trend, fund managers who trade in the opposite direction often have to bear more pressure in the investment process, and their positions tend to be more distinctive (non-group), so I think it is worth giving more. focus on.

Cathay Pacific Chengzhou is such a veteran of contrarian investment (he has served in public offerings for more than 14 years). With reference to the left and right evaluation reference indicators given in the previous article ( answering three questions about fund managers ), it can be attributed to public offering funds. Minority among managers.

1. Good long-term performance but poor stability

At present, Chengzhou manages a total of 10 fund products, with a total management scale of 16.865 billion . Its representatives are Cathay Pacific Golden Horse Steady Return (20080403-20131231) and Cathay Pacific Juxin Value Advantage (20140101-present).

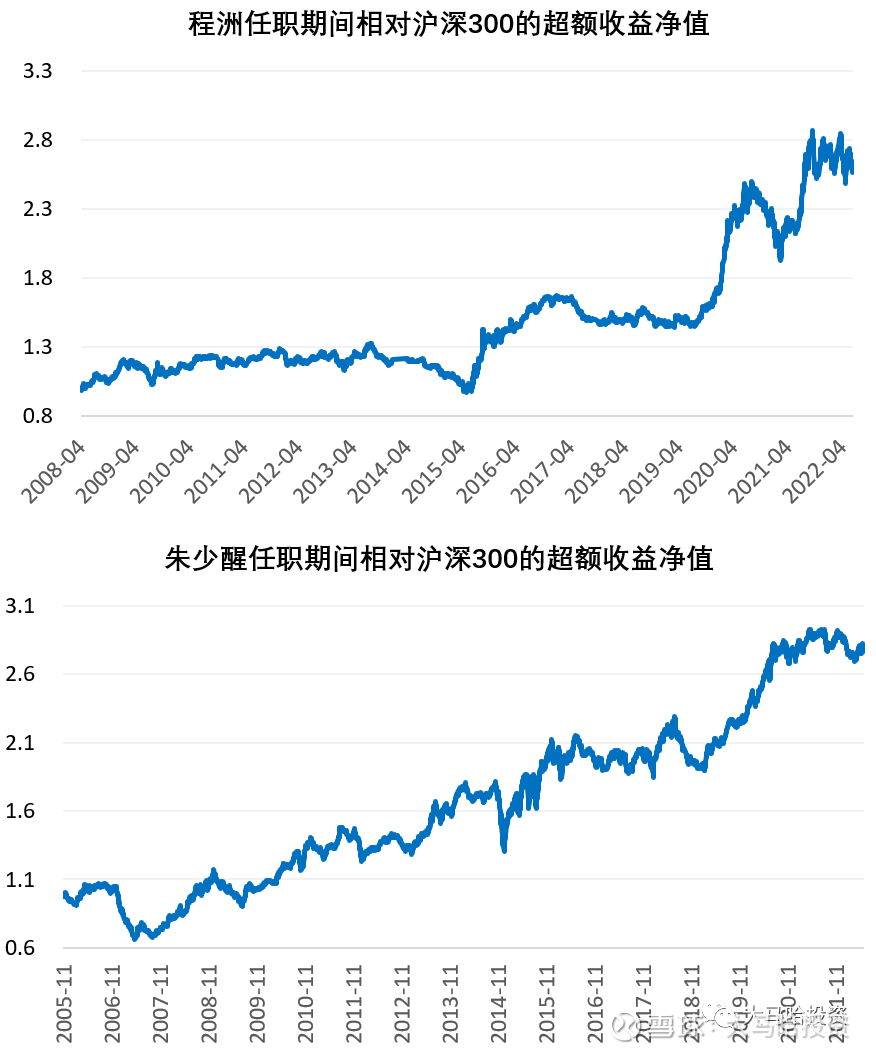

During his 14-year career in public offering, Cheng Zhou achieved an annualized investment return of 11.22% , while the total return of CSI 300 recorded an annualized return of 3.92% during the same period. 7.03% , slightly higher than Zhu Shaoxing, who is also an investment veteran (16.7 years in office, with an annualized excess of 6.33%).

However, there is a slight deficiency in the United States and China. During his tenure, Cheng Zhou’s performance was less stable than that of the CSI 300 Total Return Index, and its excess returns relative to the CSI 300 Total Return Index were mainly concentrated in the mid-2015-2017 period. In the middle of the year and from the middle of 2019 to the middle of 2021, the cumulative excess return relative to the CSI 300 Total Return Index is negative for the rest of the time.

To illustrate the problem, I listed the excess return curve of Zhu Shaoxing, who is also an investment veteran, relative to the CSI 300 during his tenure. It is not difficult to find that the stability of Zhu Shaoxing’s excess return curve is significantly better than that of Cheng Zhou. This means that if you hold Chengzhou’s fund for a long time, the investment experience may not be so good.

2. Flexible investment operations

Different from veteran investors such as Zhu Shaoxing and Dong Chengfei who focus on stock selection, Cheng Zhou has shown greater flexibility in the investment process.

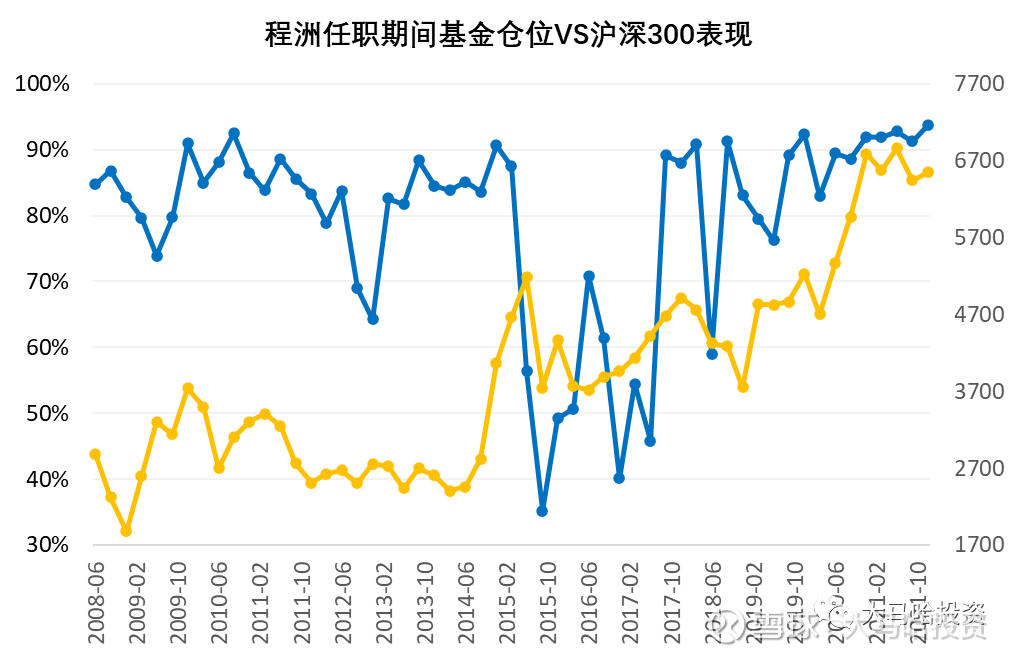

Cheng Zhou’s flexibility is first reflected in timing. During his tenure in office, he had many open and close timing operations (refer to the figure below for details). Looking at the effect of timing after the fact, the overall “gain” is less than “loss”. .

Among them, “deal” is mainly reflected in the first half of 2015. In Q2 of 2015, the value advantage of Cathay Pacific Juxin managed by Chengzhou has been greatly reduced, thus partially avoiding the market slump during the stock market crash.

As for the timing operation at other times, it is mainly reflected as “lose”, which is embodied in: From 2011 to 2013, Cheng Zhou’s position and market fluctuations showed a significant positive correlation; from 2016 to 2017, the CSI 300 went out During the slow bull market, Chengzhou’s position was low during the period, and it was not until the second half of 2017 that he increased his position significantly; in 2018, Chengzhou also made a timing operation, and then the value advantage of Cathay Pacific Juxin fell by 25.78% throughout the year.

Even for a professional player like Cheng Zhou with a background in strategy research, choosing the right time is not an easy task . Regarding this point, Cheng Zhou bluntly stated in the 2018 annual report:

Since 2015, we have made one or two major asset allocation adjustments every year. Except for 2015, which avoided the losses of the stock market crash, the rest of the year had no effect. After the sharp reduction of positions at the end of the second quarter of 2018, it also failed to In the third quarter, the Shanghai Stock Exchange 50 benefited from the rising market, which made us gradually ignore the importance of position adjustment, began to increase positions, and became obsessed with looking for structural opportunities. In the end, the net value was seriously damaged in the fourth quarter. The importance of asset allocation has resurfaced after a two-year slump. That’s what the stock market is like, when you start believing in something, the market moves in the opposite direction. 【Chengzhou】

In addition to the preference for timing, Chengzhou’s turnover rate is significantly higher than that of stock-picking fund managers. Since 2014, the average annual turnover rate of Cathay Pacific Juxin’s value advantage is 990% . With the increase in management scale, the overall turnover rate has decreased.

As for why Cheng Zhou is so flexible in investment, it should be related to his strategic research background in the early stage of his career. Strategy research pays more attention to market trends, and the investment model is more inclined to top-down. This background makes it more flexible in investment operations than pure bottom-up stock-picking fund managers. .

3. Reverse, dare to speak out

We mentioned earlier that Cheng Zhou is a contrarian fund manager, belonging to the minority in the market, and his positions also reflect the characteristics of non-mainstream. This means that his views on many sectors are bound to differ from the mainstream perception of the market.

And what is even more commendable is that Cheng Zhou dared to express his perceptions that are different from the market in the interview. It should be said that “daring to speak” is the biggest characteristic of Cheng Zhou.

For example, like Baijiu, Cheng Zhou expressed his concerns about its fundamentals very bluntly, and bluntly said that the liquor sector has no investment value in the next few years. Frankly speaking, there are many fund managers who have concerns about the valuation of the liquor sector, but very few fund managers directly question its fundamentals . Cheng Zhou said:

Taking baijiu as an example, I don’t think people can idolize a stock. The liquor industry is very clear from the data. The consumption growth in the past two years has been negative, and the industry’s income growth is between 3% and 5%, which means that the industry growth depends on price increases. The overall demand has shown a steady decline, which is also in line with the trend of an aging population. As you get older, you must drink less and less.

In such an industry where demand is steadily declining, we are not seeing supply contracting, but rather expanding. Many liquor brands that were once dying are now emerging. This is basically impossible in other consumer goods industries. The Chinese liquor industry is characterized by increased supply and stable demand, which is not in line with common sense. The only explanation is that the social stockpile is too big and sucks up a lot of it. However, the social inventory of the channel village must have an upper limit. I went to Qingpu Costco during the Spring Festival (note: early 2021), and a certain high-end liquor brand (note: Wuliangye) sold here was produced in 2018. This Costco is newly opened, it can only mean that the dealer’s inventory is sold to them.

Once the price of liquor does not rise, it will start to go to social inventory. I personally think that in the next 2 to 3 years, there is a high probability that there will be nothing to see in the liquor industry. And because the price of liquor will never drop, everyone will drink more. We have already seen leading liquor companies start lowering their earnings forecasts, and this may be just the beginning. 【Chengzhou】

Another example is Xinneng Car. He expressed his doubts about the Ningde era very strongly, and then indirectly expressed his optimism about BYD, believing that the market value of BYD will exceed the Ningde era. This view has been verified in stages. Cheng Zhou said:

There is also the battery leader of the new energy vehicle. I admit that the future profit can reach 100 billion, but the valuation at that time may be 15 times, corresponding to a market value of 1.5 trillion, which is not much different from today’s market value. By 2030, the penetration rate of electric vehicles in China may be more than 60%. At that time, it is called a car, not a new energy vehicle. It is not an emerging industry, and it cannot give a high valuation.

I don’t feel good just because everyone says it’s good. Including electric vehicles now everyone is optimistic about a certain battery faucet, but I don’t have one, and I bought a complete vehicle faucet (Note: BYD). I think the market value of this company will definitely surpass this battery leader in the next 3 to 5 years, either the former will fall or the latter will rise. 【Chengzhou】

There are many more straightforward expressions of the industry like Cheng Zhou. It is worth mentioning that, as everyone pays more and more attention to funds, regular reports have become the focus of various small essays for fund managers in the past two years. However, Chengzhou made full use of this channel to communicate with the holder before this. For example, in the 2014 semi-annual report, Cheng Zhou compared the economy to a master, the stock market to a dog, and further compared the CSI 300 to an adult dog and the ChiNext to a newborn puppy, and explained this by analogy. The market differentiation of the main board and the ChiNext in 2013-2014.

In the regular report, there are many more down-to-earth expressions like Cheng Zhou. A flesh-and-blood fund manager jumped on the paper, basically reflecting his summary of the investment gains and losses at various time stages. It can also be seen from the words between the lines that it has a lot of top-down thinking in the medium and short term in investment, which also explains the reason for its high investment turnover in another dimension.

In order to facilitate everyone to have a systematic understanding of Cheng Zhou’s interviews and opinions on regular reports, I have compiled these contents. Interested friends can get it in the private letter ” Cheng Zhou “.

4. Growth-oriented style, preference for APIs

In the interview, Cheng Zhou emphasized his low tolerance for valuation more than once. He said:

In general, try to choose targets with lower valuations. Under the spotlight, what everyone is buying must be overvalued, at least not undervalued or reasonable.

However, I think his low tolerance for valuation is significantly different from that of deep value fund managers. Instead of focusing on absolute valuation, he will pay more attention to the match between valuation and performance. In Chengzhou’s four stock selections In the standard, his requirement for valuation is PEG<1 (the price-earnings ratio is lower than the company’s expected annual growth rate). Cheng Zhou attaches great importance to the company’s growth, he said:

I am now more and more focused on industry growth. In the past, our economic growth was 9%, and all industries were growing, but at different rates. But today, no industry can bypass the cycle, but some cycles are less volatile, and some are more volatile. After the economic growth slows down to 6%, some industries will slow down, but some industries will experience negative growth. There will be valuation traps in many industries here, and you may not need to look at them for a long time in the future. 【Chengzhou】

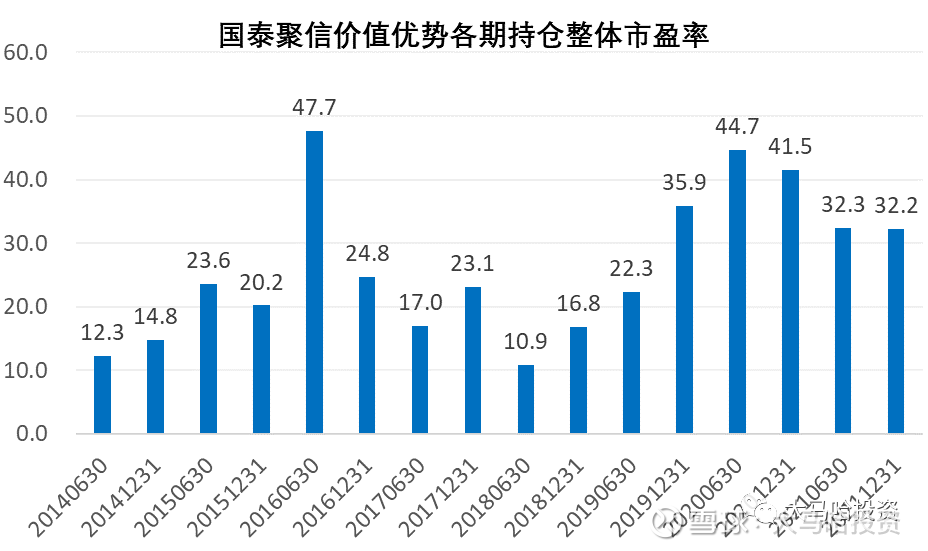

Although Cheng Zhou has repeatedly emphasized the importance of valuation, the valuation level of the overall positions in his portfolio is not low. I prefer to define Cheng Zhou as a growth fund manager . As for his concerns about the high share prices of liquor, new energy car batteries, CXO, ophthalmology, gene sequencing, and second-tier express delivery, this is mainly because Cheng Zhou believes that the growth of these sectors cannot match his current valuation.

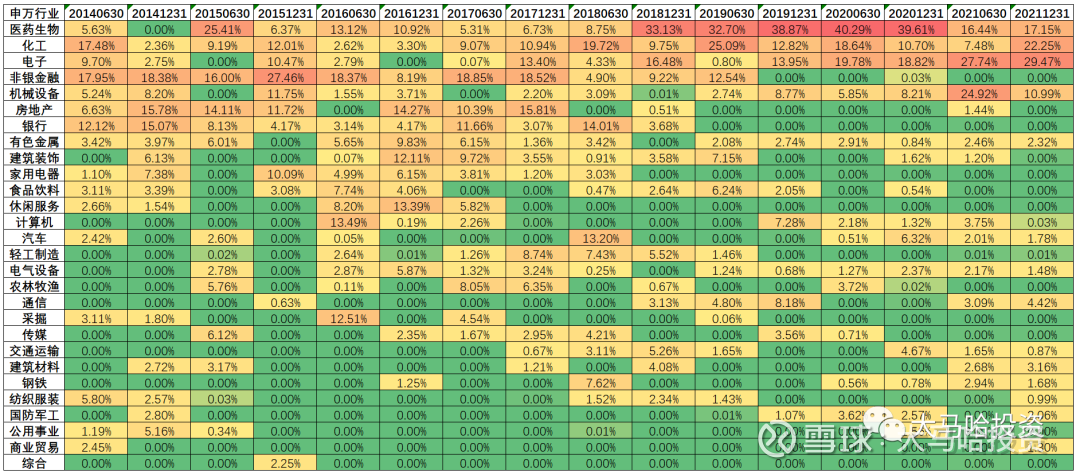

From the perspective of industry investment, Cheng Zhou mainly prefers the pharmaceutical and biological, chemical and electronic sectors. Since 2019, his holdings in these three sectors have basically remained at more than 60% or even higher, and the holding industries are relatively concentrated. It is worth mentioning that non-bank finance, real estate and banking, which Chengzhou deployed more in 2018 and before, basically disappeared in 2019 and later, mainly because Chengzhou has become more and more strict on the growth of the industry. These more general growth sectors were gradually removed from the portfolio. It is worth noting that Chengzhou has also allocated a lot of brokerage stocks in stages. The brokerage sector appears in Chengzhou’s portfolio as a strong cyclical variety, which also reflects its strong top-down investment process. thinking.

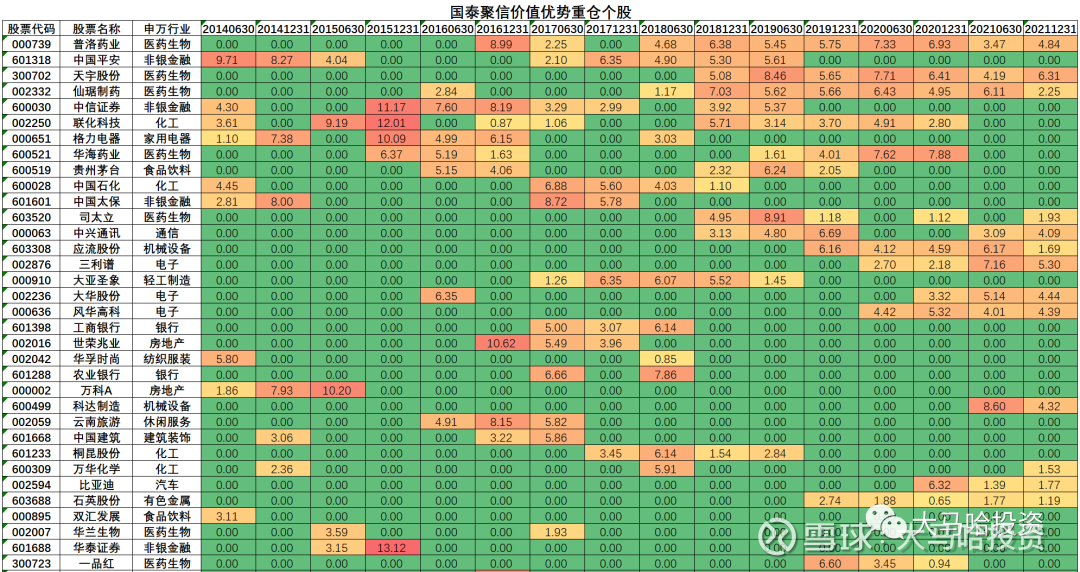

In terms of individual stock investment, Cheng Zhou does not hold too many individual stocks for a long time (for details, please refer to the table below).

Among them, Chengzhou’s most successful investment in individual stocks is mainly concentrated in APIs. For example, the top ten stocks with the value advantage of Cathay Pacific Juxin since its establishment, five of which are in the API sector ( Pluo Pharmaceuticals , Tianyu Co. , Ltd., Xianju Pharmaceutical , United Chemical Technology and Huahai Pharmaceutical ), the outstanding performance of these stocks since 2019 has contributed a large proportion of the net value increase to the fund. Regarding the investment value of the API sector, Cheng Zhou wrote a lot in the interview. He said:

APIs are a long-term logic, and due to changes in industry regulation, there is a process of systematic revaluation. In the past, with the upgrading of China’s industry, China’s API companies will also upgrade along this industry chain. Everyone gives high valuations to CDMO companies and low valuations of API companies. In fact, API companies have an advantage in CDMO. Moreover, the valuation of these API companies is more than half cheaper. 【Chengzhou】

In addition to APIs, there are not many impressive cases of Chengzhou’s investment in individual stocks in other sectors. I think that the concentration of successful investment cases will restrict the sustainability of performance to a certain extent.

V. Summary

On the whole, Cheng Zhou is a growth fund manager with a contrarian investment style, not conforming to the crowd, focusing on valuation and daring to express himself. He has both top-down and bottom-up thinking. a relatively good return on investment.

Of course, objectively speaking, there are also some unsatisfactory places, which are mainly reflected in: (1) long-term performance is good but not stable, and the investment experience is not good; (2) investment is flexible but not well converted into The investment performance of the fund manager, and the management scale of nearly 20 billion will also restrict its past investment model; (3) The investment highlights of individual stocks are mainly limited to APIs, and the circle of competence is relatively narrow. If there is a misjudgment in the face, the performance of the portfolio may be negatively affected to a greater extent.

If the allocation of fund managers also follows the “core + satellite” idea, individuals tend to allocate Chengzhou as a satellite, and the characteristics of not following the crowd and going against the market may bring unexpected effects to the portfolio at some point.

Related reading:

An interesting fund manager evaluation metric

Three questions about fund managers answered

The full text is over! All the statistical data in this article are from Choice. It is not easy to be original. If this article is helpful to everyone, please like , comment , favorite , and follow the four combos. Thank you for your support~

Disclaimer: The above content is for informational purposes only and does not constitute investment advice. Funds are risky and investment should be cautious.

There are 2 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/7245734636/223203186

This site is for inclusion only, and the copyright belongs to the original author.