The research bank is divided into four levels. The lowest level only looks at the growth of PB, PE and statement, which can only see the modified results. The second layer must learn to look at asset quality, non-performing assets, provisions, and real profits and growth under the same standard after restoration. But what you see at this time are only relatively real effects. If you want to dig deeper into the bank, you will understand the causes of these effects.

The third layer should study the bank’s liability structure and its asset allocation, which are the factors that determine the bank’s non-performing and profit.

At the highest level, you need to understand a bank’s corporate culture, risk strategy, and business strategy. See through regional development and macroeconomic trends. See if the company’s strategy matches the general trend of the external environment. Anticipate the future development of the enterprise.

The main business of the bank is actually very simple to raise funds from the society and then lend them to those who need funds. The bank’s ROA = loan interest rate – deposit cost – credit cost – operating cost. In addition to the cost of deposits, the biggest variable cost is the cost of credit.

Because the bank statement will not disclose the credit cost of each type of asset, only the non-performing rate of classified assets, in order to facilitate research by asset classification, we approximately assume that the credit and management costs of each type of asset are proportional to its non-performing rate. The rate of return and liability cost of the bank’s major loan assets, as well as the ROA statement of the total assets are disclosed. We assume that the ROA of the loan assets is the same as the ROA of the total assets, so that we can inversely calculate the ratio of the bank’s asset credit cost and non-performing rate. . With this ratio, we can easily disassemble and analyze the ROA and profit and loss of each type of asset.

Although it may be quite different from the actual situation, the qualitative analysis of the relative relationship between various industries and regions will not have much error, and ROA, and ROE are always closed by regression correction.

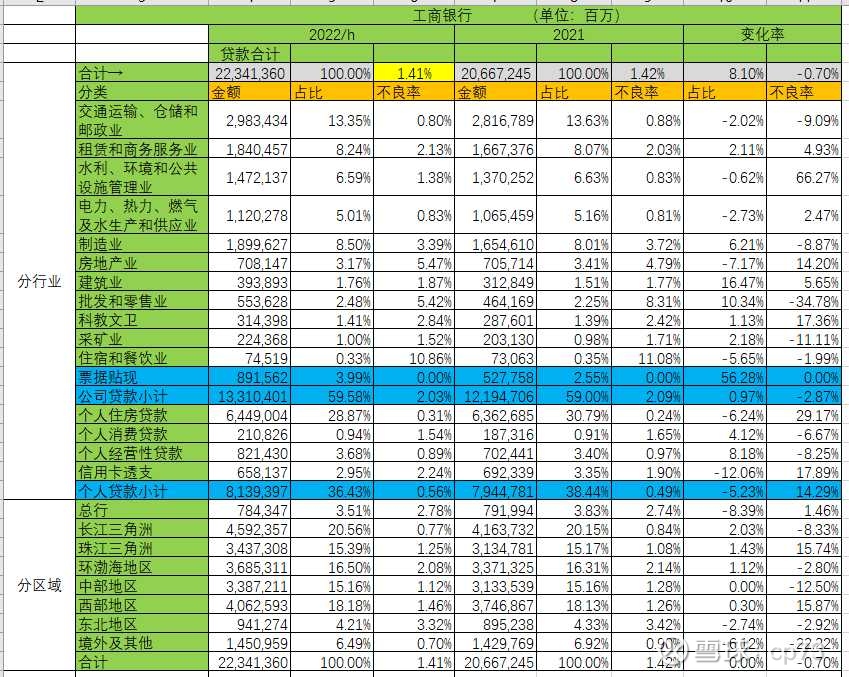

We take ICBC, which has a total loan of more than 22 trillion across the country, as the representative of the national banking industry to analyze the return on assets in different regions and industries under the same management and risk control.

The amount, proportion and non-performing loans of various industries and regions in ICBC’s 2022 semi-annual report are as follows:

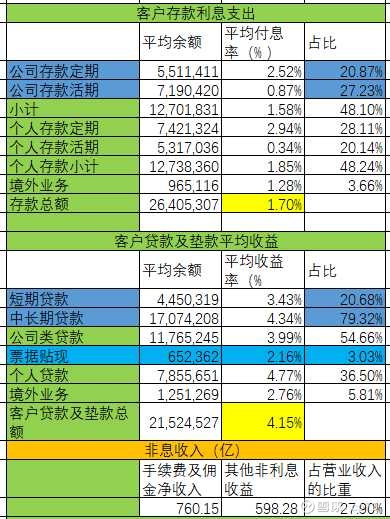

Here are ICBC’s cost of liabilities and return on assets:

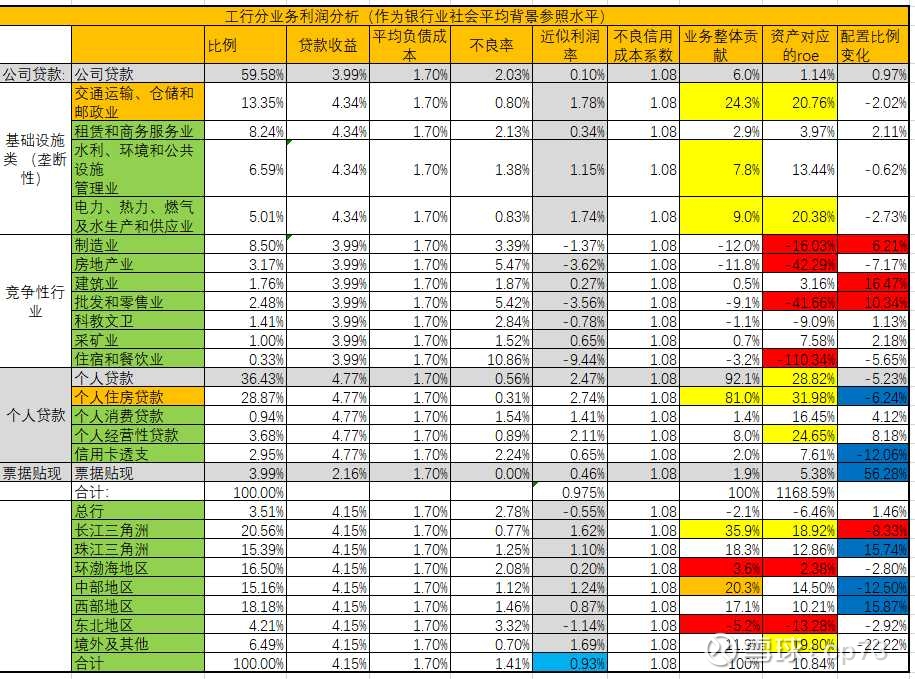

The figure below shows the ROA and ROE of various assets by industry and region and the current trend of asset allocation ratios at the end of 21, calculated according to the aforementioned assumptions:

For the convenience of observation, we split corporate loans into two categories: infrastructure (monopoly) and competitive industries. The combined statistics are as follows:

From these two tables we can find a lot of interesting things.

The ROA of First China’s banking corporate loan business is only 0.1%. Deducting monopoly infrastructure, the non-performing rate in competitive industries is 3.86%. The ROA is -1.88%, and the ROE is -22%! The loan interest rate cannot cover the cost of credit, and the bank is trading at a loss.

As the priority banks are losing money, life is even harder for businesses. The economic situation is not optimistic.

Now let Li mention less, because these businesses of the bank have already lost a lot of money and still insist on doing it. Big banks have indeed fulfilled their social responsibilities in lending to competitive industries.

Second, China’s economic development is seriously divided between regions. The ROE in the Northeast region is -13%. It is no wonder that banks in Liaoning and other places are going bankrupt.

The Bohai Rim region occupies 16.5% of the capital, and the ROE is only a pitiful 2.38%. Trends are dangerous and not optimistic.

The development momentum of the Pearl River Delta is weak, and the ROE is only 12.86%. The development momentum of the Yangtze River Delta is very strong, and the ROE is 18.92%.

The ROE of the Yangtze River Delta business of the Third ICBC has reached an astonishing 18.92%, surpassing that of Chengdu Bank, which is the highest among all banks . If ICBC’s Yangtze River Delta business is split, it will kill all the so-called excellent banks: Chengdu, Hangzhou, Ningbo, China Merchants Bank, Jiangsu… This is a miracle created by low non-performing loans and low capital cost. Chengdu Bank’s debt cost of 2.13 is already very low. ICBC’s 1.7% debt cost, loans with the same yield, and 11 times leverage, ICBC’s ROE can be nearly 5 points higher. ROE!

As a highly leveraged business, banks have a huge impact on profits due to low debt costs and non-performing ratios.

From the comprehensive point of view of the previous aspects, the influence of locality on the bank is much more important than the so-called excellent management. If the soil is not good, no matter how hard you work, it will be in vain. If the soil is good, as long as you don’t make big mistakes, the crops will not grow too bad.

Banks are by no means homogenous. They have surpassed most people when they were born in a wealthy family.

Fourth, from the above table, we can see the allocation strategy of bank assets. First of all, from a regional perspective, do not go to the Northeast and the Bohai Rim , and increase the asset allocation in the Yangtze River Delta . From an industry perspective, corporate loans in competitive industries are toxic assets, so keep them away as much as possible. If the economy continues to decline in the future, asset quality will further deteriorate. Personal loans are high-quality assets and need to be allocated more. The allocation of monopolistic infrastructure loans should also be increased.

The fifth ICBC’s asset allocation is somewhat incomprehensible. If it is a social responsibility and a political task to increase the loss-making manufacturing loans against the trend. The meager-profit construction industry and the huge loss-making wholesale and retail industry have greatly increased, which is a bit incomprehensible.

More especially, it is a bit strange to reversely reduce the configuration of the Yangtze River Delta and increase the configuration of the Pearl River Delta . It may be affected by the epidemic control.

The sixth ICBC has significantly increased the ratio of discounted bills with only 5% of ROE to 56%. It may be that high-yield personal loans and infrastructure loans cannot be released. The lack of credit demand leads to asset shortages, and it is unwilling to give more competition to lose money. Sex industry company loans.

The seventh personal mortgage is a high-quality asset with sufficient collateral and extremely low non-performing loans. Mortgage loan income is the basis for large banks to undertake social responsibilities. Without high-yield mortgages, those loans that subsidize companies in competitive industries with huge losses cannot be released. A few years ago, the China Banking Regulatory Commission assigned a line to mortgage loans, with the highest proportion of the big banks, which is to reduce competition, keep the big banks’ cakes, and enhance their ability to exercise social responsibilities.

On the whole, the big banks have formed a trend of continuous operation, the assets are good and bad, and they bear certain social responsibilities. They are not completely market-oriented, and are stable but not flexible.

From the above analysis we can draw a picture of the best banks:

1) Most of the assets are located in banks in advantageous regions such as the Yangtze River Delta or the Chengdu-Chongqing region.

2) Banks whose personal loans, especially mortgages, have been over-allocated a few years ago.

3) Banks with government resources over-allocated high-quality monopoly infrastructure assets. In particular, the superposition of superior areas + monopoly infrastructure is extremely powerful.

4) Banks with low asset allocation in toxic competitive industries.

5) Banks with low cost of debt.

$ China Merchants Bank (SH600036)$ $ Chengdu Bank (SH601838)$ $ Industrial Bank (SH601166)$

@Today’s topic @不國泰东宝真@云蒙@ice_中行谷子地@星台場hat @太原@ -yihu- @koala uncle @王建的angle @Mark Chen

This topic has 115 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/7297620365/229938341

This site is for inclusion only, and the copyright belongs to the original author.