“

Income is a chain of events, and patience is an essential part.

– Lao Tang

“

After the market closed yesterday, Yanghe released its semi-annual report for 2022, with outstanding performance growth, with an operating income of 18.9 billion, a year-on-year increase of 21.65%. The net profit attributable to the parent was 6.89 billion, a year-on-year increase of 21.76, and the deducted non-net profit was 6.64 billion, a year-on-year increase of 28.54%.

From a quarterly perspective, the revenue in the second quarter was 5.882 billion, an increase of 17% year-on-year, the net profit attributable to the parent was 1.908 billion, an increase of 6% year-on-year, and the non-net profit deducted was 1.745 billion, an increase of 28% year-on-year.

The performance growth of more than 20% seems normal against the background of the substantial increase in advance receipts last year, but it is also rare. In the first half of the year, especially the second quarter, the epidemic was raging, and many cities adopted closed management, which obviously restricted the growth of liquor. In the consumption scenario, in the current environment, the non-net profit can be increased by nearly 30%, which can also indicate that the vitality of the company is further blooming.

Simply make a split, see the bright spot in the financial report, and a few things that you don’t understand, record it, and verify it on your behalf

1

Main business

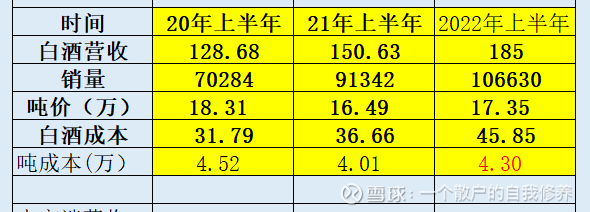

From 2021, Yanghe’s operating data has also improved significantly. In the first half of this year, the sales volume of liquor has reached more than 100,000 tons, and the sales volume has increased by 16.7% compared with last year, while the revenue increased by 21.7% in the same period. Compared with last year, it has also increased, and the price per ton has also increased.

Of course, the higher ton price in the first half of 2020 was more because the impact of the epidemic on ordinary liquor was far greater than that of mid-to-high-end liquor, resulting in a decrease in the proportion of ordinary liquor and a higher ton price, because Yanghe did not disclose The sales volume of mid-to-high-end and ordinary liquor cannot be directly compared. It can only be judged that the increase in revenue this year is greater than the increase in sales volume, and the structure is more of the contribution of mid-to-high-end liquor.

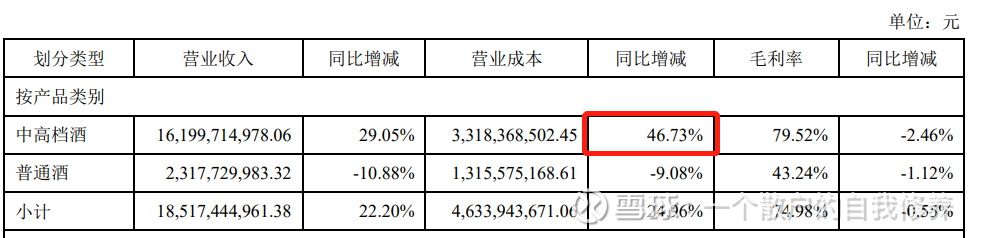

The second is the increase in cost, which is in the normal range if only in terms of the average ton cost, but not so normal in terms of the disclosed cost of mid-to-high-end liquor.

The mid-term report shows that the revenue of mid-to-high-end liquor increased by 29%, but the operating cost increased by 46%, which also led to a 2.5% drop in the gross profit margin of mid-to-high-end liquor. This is also a very abnormal situation, because under normal circumstances, the operating cost The growth rate is often lower than the revenue growth. If calculated according to the same revenue growth data, the difference is about 400 million.

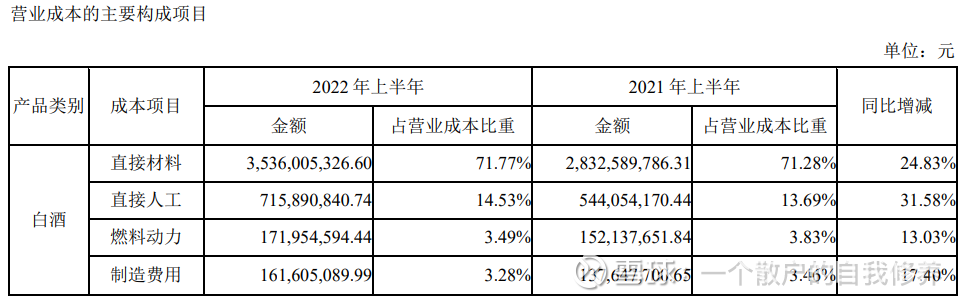

In terms of the main components of operating costs, the increase mainly includes direct materials and direct labor. So I wonder if prices have gone up? However, compared with Wuliangye and Maotai, operating costs have not risen significantly.

The answer to this is not yet known.

2

cash flow

The most eye-catching aspect of the 2021 annual report is the contract liabilities. This year’s semi-annual report shows that the contract liabilities are 7.9 billion yuan, compared with 5.5 billion in the same period last year, while the advance receipts are 2.5 billion, compared with 1.5 billion in the same period last year. surplus grain.

From the perspective of operating cash flow, there are several main reasons for the net outflow.

The first is to reduce inflow

Because the money was collected in advance last year. The net operating cash flow in 2021 is 15.3 billion, compared with 3.9 billion in the same period in 2020, and the operating cash flow was negative in the first quarter of this year, which is also the reason.

The second is the increase in outflow. From the data point of view, it is mainly the cash paid to employees and various taxes and fees.

Cash paid for employees increased by 39% year-on-year, and taxes and fees increased by 53% year-on-year. The difference between these two items is also several billions.

Let’s take a look at taxes and fees: From the perspective of a single quarter, taxes and fees are basically the same in the second quarter, which is almost 3.1 billion. The main difference is that in the first quarter, the tax paid in the first quarter was 6.8 billion, compared with 3.4 billion in the same period last year. The difference is 3.4 billion, which is an increase in the first quarter, mainly because the sales revenue increased significantly last year, and the cash received from sales includes the value-added tax collected on behalf of the company. caused.

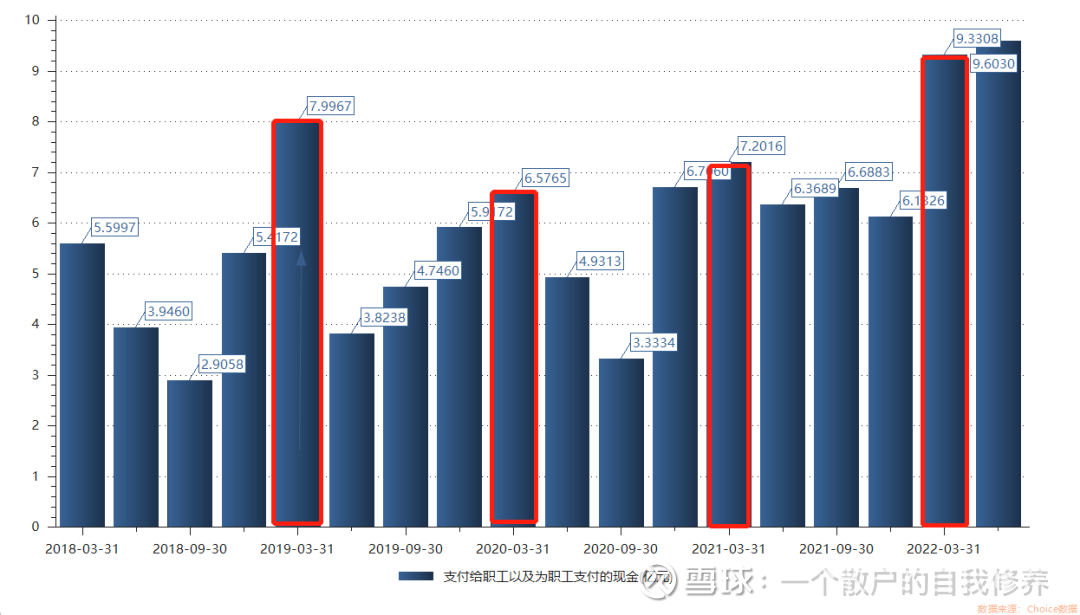

Let’s look at the cash paid by employees: the first quarter data shows that the cash paid to employees was 930 million, compared with 720 million in the same period last year. If you look at the data for the second quarter alone, you can see that the cash paid by employees in the second quarter of this year was as high as 9.6 The expenditure in the second quarter is higher than the expenditure in the first quarter, which is a bit abnormal.

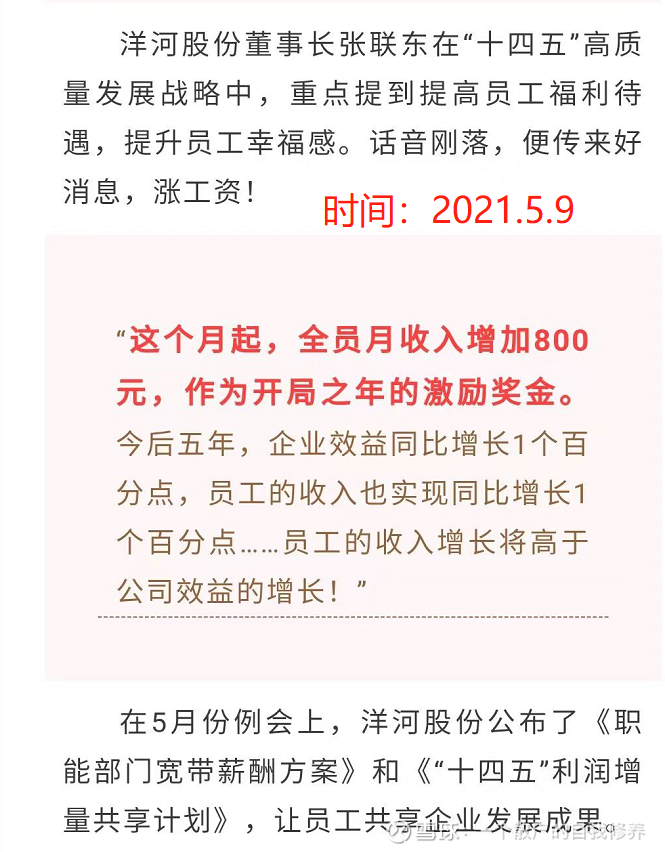

According to previous years, the cash paid to employees in the first quarter is the highest, and why will the proportion increase in the second quarter of this year? No reasonable explanation has been found yet, but it can be seen that the wages paid to employees have also increased significantly. In May last year, Yanghe announced that each employee would increase their wages by 800 yuan, and that the income of employees is linked to the company’s benefits.

In the long run, letting employees increase their enthusiasm for work, as well as their sense of identity and belonging. If you want a horse to run, you have to feed the horse.

3

Out-of-province revenue

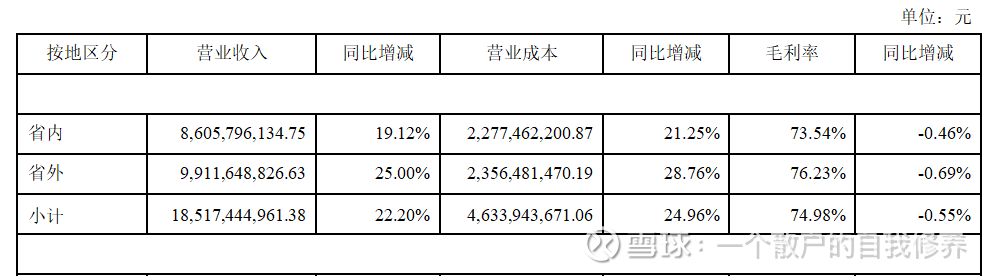

From the perspective of gross profit margin and revenue growth, the gross profit margin and revenue growth outside the province are higher than those in the province, and the expansion outside the province is still the main driving force for Yanghe’s future growth.

Looking back on the past few years, the expansion of Yanghe outside the province has not been smooth in recent years. First, it pressed goods to the channel, and then dealt with the channel problem and encountered the new crown. However, with the success of M6+, Yanghe’s position in the middle and high-end liquor It is also more stable, and the outside of the province has also improved. Since 2019, the income outside the province has been higher than the income in the province. Although there have been repeated periods, the proportion outside the province has gradually increased. In addition, the expansion of the cellar in 2013 also has nearly 10 years. , the future production of high-end liquor also has a foundation, time is Yanghe’s friend.

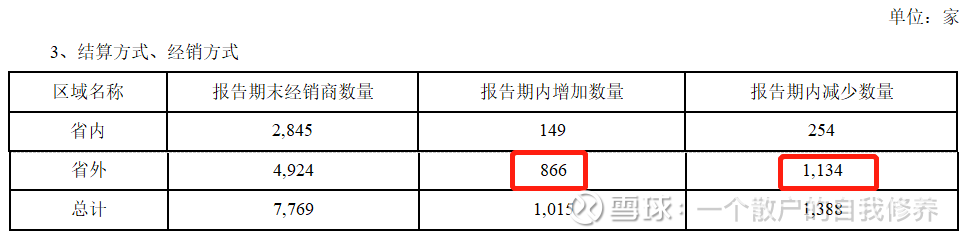

On the other hand, the number of dealers

Distributors outside the province still fluctuate greatly. Are manufacturers actively optimizing distributors, or are distributors withdrawing?

Last year’s annual report said this:

During the reporting period, the change in the number of dealers was mainly due to the company focusing on the principle of pro-business, safe business, support for business and wealthy business, focusing on the creation of strategic leading products, and optimizing the structure and layout of dealers.

The data in this regard still needs to be tracked to see if it can be stabilized later.

summary:

The performance of the data in this interim report is still very eye-catching. The price per ton and the sales volume have increased simultaneously. The deducted non-net profit has also risen sharply, and there is no overdraft. Although the staff compensation has increased a lot, it also gives full play to the offensive power of employees, which is not a bad thing for shareholders.

According to the current situation, there is still a chance to achieve a net profit of 10 billion this year. The current market value is around 2600, and the current price-earnings ratio of 10 billion is 26 times, which is a reasonable range, and the future can enjoy and corporate growth. The simultaneous increase did not take advantage of Mr. Market!

The above content is for records only, not as a recommendation for buying and selling. Profits and losses are at your own risk

$Yanghe (SZ002304)$ $Luzhou Laojiao (SZ000568)$ $Wuliangye (SZ000858)$

The arch of the sun died, and came unexpectedly

Check out one or two!

There are 32 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/6068349566/229265148

This site is for inclusion only, and the copyright belongs to the original author.