When evaluating the investment value of a fund manager, we often refer to an indicator, that is, the recognition of the fund manager by institutional investors .

Therefore, as a typical representative of institutional investors, public FOF has attracted much attention in fund investment. Many self-media will also launch FOF’s favorite fund managers list for everyone to use as a reference for fund investment. So, how much reference does the preference of institutional investors represented by FOF have on our fund investment? Today we talk about data and talk about it in detail.

1. List of FOF’s Favorite Fund Managers

I summed up all FOFs in each reporting period from 2019 to the present to the net value ratio of all funds under each active fund manager, and finally selected the top 15 active fund managers in each period (according to the ratio of total positions to net value from high to Low ranking), the specific results are shown in the following table:

2. What can we find in the list?

Looking at the list of FOF’s most preferred fund managers in a certain period alone seems to have limited information, but if you compare the lists of each period from 2019 to the present, the information contained in them is still very rich.

In my opinion, at least the following:

(1) The preference of public FOF for fund managers has become very fast. Comparing each issue of the list, it can be found that the fund managers on the list have changed a lot, and there are very few fund managers who can continue to be favored by FOF. Most of the fund managers on the list are short-lived. Institutional investors, like many individual investors, are not very fond of fund managers. Today, a fund manager is the most favored by institutional investors, and it is very likely that it will fall off the list in a few quarters. It can be seen that the gold content of this list is not as high as imagined.

(2) There are more icing on the cake, and less charcoal in the snow. When it comes to individual investors buying funds, what people often criticize is that they choose fund managers based on performance lists, buy those with good historical performance and sell those with poor historical performance. In fact, if you look at the table above, institutional investors are not much better than individual investors. Most of the ones on the list have particularly good historical performance, and most of those who fell off the list have poor performance. Some fund managers even The ups and downs have gone through several ups and downs in the list.

In short , institutional investors favor those with outstanding performance, and once the performance deteriorates, they will be ruthlessly abandoned. We can give a few examples, everyone can clearly feel it:

Case 1: Tang Xiaobin (Listing date: 2021Q3\2021Q4)

Tang Xiaobin’s representative, as a multi-factor of GF, in 2021, the fund achieved an ultra-high investment return of 89% , and because of this, Tang Xiaobin was selected by institutional investors in the second half of 2021. And as GF’s multi-factor performance has flattened this year (-22.89% year-to-date), he will fall off the list in 2022.

Case 2: Yuan Weide (Listing date: 2021Q2\2021Q3\2021Q4\2022Q1)

As Cao Mingchang’s apprentice, Yuan Weide’s masterpiece, China-Europe Value Smart Selection, achieved a 52.41% return on investment in 2021, which is significantly better than Cao Mingchang’s 26.67%. In addition, Yuan Weide’s impressive performance in 2020 is superimposed, which focuses on both valuation and flexibility. The style of the company is on the paper, which is sought after by institutional investors and individual investors. No exception, Yuan Weide was also dropped from the list due to his average performance this year.

Case 3: Lin Yingrui (Listing date: 2021Q1\2022Q2\2022Q3)

Lin Yingrui is a typical example of two ups and downs in the list. As a representative of dilemma reversal\deep value strategy, he first entered everyone’s field of vision at the beginning of 2021. With his outstanding performance in the first quarter of 2021, he attracted the attention of the market, thus becoming the favorite fund of FOF investors. The list of managers, however, as the performance becomes flat after the second quarter of 2021, began to gradually fade out of everyone’s vision. Since 2022, as Lin Yingrui’s performance has performed well again, he has regained the favor of institutional investors.

Other cases: Three representative fund managers are listed above. In fact, there are many similar fund managers in the list, such as Yuan Fang (2019Q4-2021Q2 consecutively on the list), Wang Haifeng (2022Q1\ 2022Q2 on the list), Yang Zongchang (2022Q3 list), Zhou Zhishuo (2022Q3 list), Feng Mingyuan (2020Q1\2020Q2 list and 2021Q2-2022Q2 list), Sun Bin (2021Q2-2022Q3 list), Qiu Dongrong (2021Q3\2022Q1\2022Q2\2022Q3 On the list), Yang Hao (on the list in 2019Q4\2020Q1\2020Q2), Wu Chuanyan (on the list from 2020Q2-2021Q1) and Qiao Qian (on the list from 2020Q1-2021Q2), etc. are all in and out of the list because of performance, limited by space, I will not list them one by one here. Interested friends can observe them one by one by comparing the list and performance.

(3) Institutional investors do not have the ability to discover outstanding fund managers in advance.

Through the analysis of individual fund managers in the second part, it is not difficult to find that FOF, as a representative of institutional investors, also does not have the ability to discover outstanding fund managers in advance. Many current or former fund managers are selected by FOF after accumulating very good performance, rather than being selected by institutional investors when they are unknown. Almost every fund mentioned in the above section Managers are living examples.

The most typical of these is Qiu Dongrong. As a fund manager who has been recognized by institutional investors from 2016 to 2017, his performance in 2019-2020 during his tenure at ZhongGeng was not satisfactory, and FOF investors did not because he has a history. Buying in advance due to the endorsement of performance, but waiting for Qiu Dongrong to come out of the circle with excellent performance in 2021 before starting to snap up. This is true for Qiu Dongrong, not to mention other fund managers.

Not only that, but there are many fund managers whose performance is often booming and declining after being selected into the above-mentioned FOF favorite list, such as Tang Xiaobin , Yuan Weide, Yang Zongchang and Zhou Zhishuo . Many friends may not have noticed that in the past two months, Yang Zongchang and Zhou Zhishuo’s respective masterpieces have withdrawn about 20% from the highest point…

It can be seen that it is not a good thing to be on the list of FOF’s favorite fund managers. It may mean that the performance is about to reverse. It is difficult for us to know in advance what the current trigger is.

3. Can you make money by following the list to buy funds?

For this question, through the above analysis, I believe that everyone has been able to get part of the answer emotionally, because institutional investors are also “chasing up and down”, if you follow the list to buy fund managers, the final result may not be too ideal.

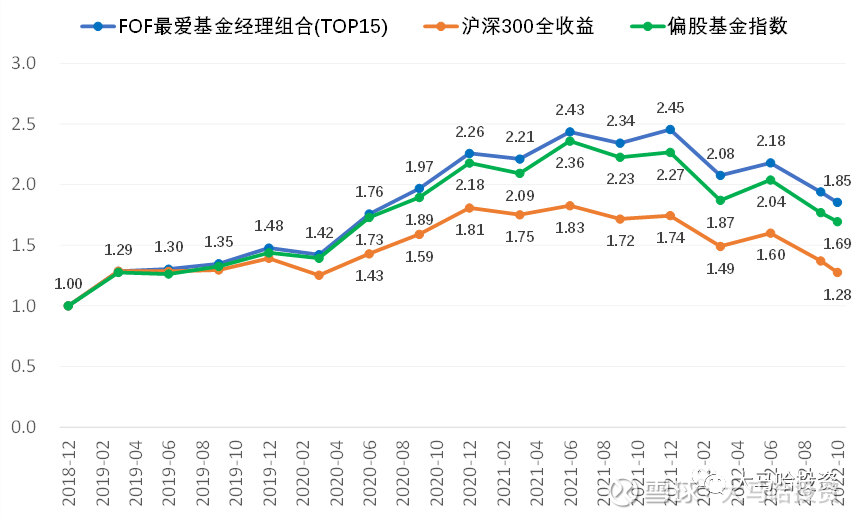

For this reason, I made a rigorous calculation this time. I found the representative works of the fund managers in the list at each time point. It is assumed that the real-time positions of all FOF fund managers can be known at the end of each quarter to obtain the above-mentioned TOP15 list. . Then, at the end of each quarter, the respective representative works of the TOP15 fund managers are purchased with equal rights (de-weighting) and held until the end of the next quarter, and then the positions are adjusted according to the new TOP15 list. The specific performance of the strategy year-to-date in 2019 is as follows:

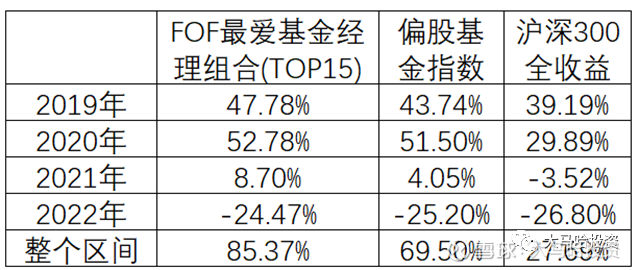

From the beginning of 2019 to the present (October 30, 2022), the investment return of the partial stock fund index is 69.5% , and the return of the CSI 300 in the same period is 27.69% . The investment income obtained by FOF’s favorite fund manager portfolio is 85.37% , although it is significantly better than the CSI 300, but only slightly better than the partial stock fund index.

The following is the annual return of this strategy. It can be seen that whether it is the entire range or the year, the return of this portfolio is basically the same as that of the partial stock fund index. It can be seen that FOF’s favorite fund manager portfolio has been able to beat Shanghai in the past four years. The Shenzhen 300 Index does not provide stable excess returns relative to the stock-biased fund index . Compared with the star fund managers who are popular on the list, the performance that the list can bring us is undoubtedly disappointing. This year’s latest list includes many fund managers who have been resilient since the beginning of the year. However, the strategy’s return in 2022 is -24.47% , which once again shows the lag of the list.

Note: I also used the same algorithm to calculate the FOF favorite fund manager portfolio (TOP5), and the final return was 69.91% .

It should also be pointed out that if we buy funds according to the list, we may not even get the above-mentioned performance, because the timing of the disclosure of data in regular reports is lag (about one month), and we cannot make it at the end of each quarter. Know the above list. Given the characteristics of right-hand FOF trading, the later you buy these funds, the worse the portfolio’s performance will be.

I also give a data here for your reference.

The above strategy has achieved 85.37% investment income since 2019. If we are based on the original strategy, assuming that we know the list three months in advance (for example, we know the list at the end of September 2021 and the list at the end of December 2021) and make purchases. enter. Then the income of this strategy will be greatly increased from 85.37% to 192.85% , which shows the style of FOF fund managers chasing up.

By analogy, if we lag in buying the list, the performance is likely to be lower than the original strategy. Therefore, it can be prudently inferred that the return we get from buying funds based on the list is likely to be inferior to that of the stock-biased fund index .

4. What inspiration can the list bring us?

When we evaluate the investment ability of fund managers and when many platforms promote fund managers, they often take institutional investors’ views on fund managers as an important reference indicator.

However, from the statistical results of this article, this conclusion does not hold, and it is easy to view the investment ability of professional fundraisers. For the vast majority of fund managers favored by FOF, they were chosen by institutions after they became famous, not before they became famous. At this time, the best performance of fund managers has passed. Fund investors including institutions Fund managers often earn money from the “fish tail” of the excellent performance of the fund manager, not the “fish body” let alone the “fish head”.

Moreover, once the performance of the fund manager deteriorates, FOF institutional investors do not choose to accompany, but choose to run away and follow the next popular fund manager, which is impatient. A small number of fund managers who have long been favored by institutional investors either have good sustainability performance in certain market stages (such as 2019 and 2020) or are scarce (such as ICBC Credit Suisse Financial Real Estate and Qianhai Kaiyuan Gold and Silver Jewelry). In addition, given that the investment ability of fund managers is unlikely to change too much in just a few quarters, and their performance fluctuations are mostly due to style, the fast-forward and fast-out of FOF institutional investors in fund managers is very important for us to evaluate funds. Managerial ability does not have much reference value.

Investing is something that requires excessive awareness. It is not easy to do this, even for institutional investors who focus on investment. This once again confirms why I am not keen on digging out dark horse fund managers? point of view in the article.

Finally, through this article, the most important reminder for you is: Be cautious about the list of fund managers most preferred by institutional investors. Once the fund managers we hold are selected, the performance is likely to have reached its peak.

Related reading:

Why am I not keen on digging out dark horse fund managers?

The full text is over! It is not easy to be original. If this article is helpful to everyone, please like , watch , favorite , and follow the four combos. Thank you for your support~

Disclaimer: The above content is for informational purposes only and does not constitute investment advice. Funds are risky and investment should be cautious.

This topic has 12 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/7245734636/234247549

This site is for inclusion only, and the copyright belongs to the original author.