The Shanghai Stock Exchange and the Shenzhen Stock Exchange simultaneously released the detailed rules for convertible bonds, which means that the rules for convertible bonds tend to be consistent. This is a friendly measure for convertible bond investors. However, most investors are People who don’t understand the rules, don’t learn the rules and don’t ask for the rules belong to a group of gamblers who don’t understand the rules.

Based on the characteristics of convertible bonds, the “Detailed Transaction Rules” optimize the transaction mechanism, strengthen transaction supervision, and strengthen risk prevention and control on the basis of supporting the reasonable pricing mechanism of convertible bonds, which is conducive to preventing excessive speculation and promoting the healthy and long-term development of the convertible bond market.

The main contents include:

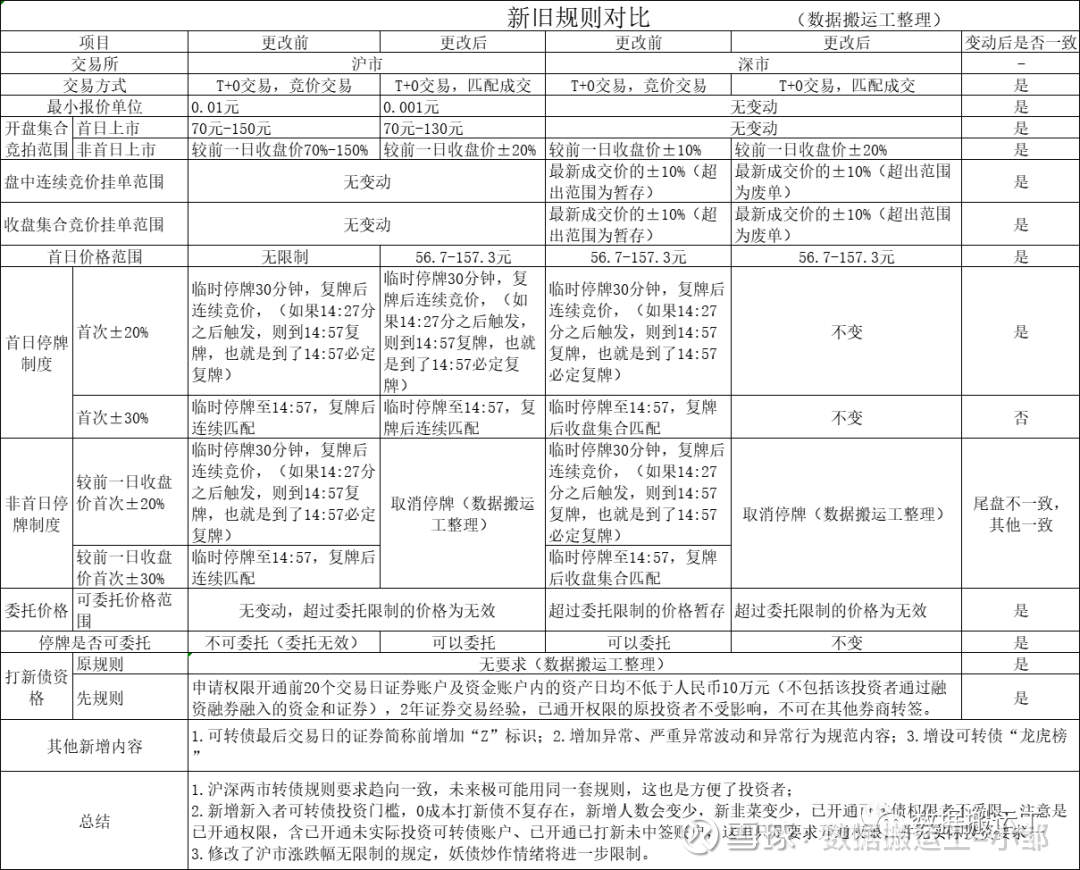

The first is to improve the price stabilization mechanism. On the first day of the listing of convertible bonds, a valid declared price range of 57.3% higher and 43.3% lower than the issue price is set for the whole day, and the current two-level intraday temporary suspension mechanism of 20% and 30% is retained; from the day after listing, a 20% increase is set Drop price limit.

The second is to strengthen the supervision of abnormal transactions. Clarify the abnormal fluctuations and severe abnormal fluctuations of convertible bond transactions, specify the types of abnormal convertible bond transactions and relevant regulatory measures, and clarify that Shenzhen Stock Exchange may require listed companies to disclose abnormal fluctuation announcements or suspend trading according to the abnormal fluctuations of convertible bonds. Verification, or the implementation of an intraday forced trading suspension.

The third is to strengthen risk warnings. A “Z” mark is added before the securities abbreviation on the last trading day of the convertible bonds to fully remind investors of risks and effectively protect the interests of investors.

The fourth is to link bond trading rules. Adjustment of the textual expressions such as transaction method, declared quantity unit, etc., such as changing “bid transaction” to “matching transaction”, and adjusting the processing method of convertible bond declarations exceeding the price limit from “temporary storage transaction host” to “invalid declaration” .

The “Guidelines for Self-Regulatory Supervision” adhere to information disclosure as the core, combined with daily supervision practices, to further improve the business norms and information disclosure behaviors such as the listing and listing, conversion, redemption, and sell-back of convertible bonds, which is conducive to better protecting the interests of investors .

Major revisions include:

First, directional convertible bonds are included in the scope of regulation. It regulates the listing, conversion, redemption, sell-back, principal and interest payment, repurchase and cancellation of directional convertible bonds.

The second is to strengthen the disclosure of convertible bond information. It is clarified that the company shall make pre-disclosure 5 trading days prior to the trigger date of the expected redemption conditions of convertible bonds and the triggering date of the conversion price correction conditions, and shall review and disclose the requirements for exercising the redemption right or modifying the conversion price when the relevant conditions are met; If it is not reviewed and disclosed in accordance with the regulations, it will be deemed that the redemption right is not exercised or the conversion price is revised this time. If the redemption right is not exercised, it shall not be exercised again for at least 3 months to stabilize market expectations.

The third is to optimize the implementation period of redemption and repurchase. It is stipulated that the interval between the trigger date of the redemption conditions of the convertible bonds and the redemption date shall be no less than 15 trading days and no more than 30 trading days, and 3 trading days shall be set aside for investors to convert shares after the suspension of trading. , to help investors reduce unnecessary losses; it is stipulated that the interval between the trigger date of the convertible bond sell-back conditions and the first day of the reporting period should not exceed 15 trading days, and urge the company to implement the sell-back in a timely manner to protect investors’ right to sell-back.

In addition, the “Guidelines for Self-Regulatory Supervision” has made corresponding institutional arrangements in strict short-term trading supervision, compacting the responsibilities of intermediaries, and strengthening risk warnings. The Shenzhen Stock Exchange has simultaneously revised the guidelines and announcement formats for convertible bond-related businesses, adding new announcement formats such as abnormal fluctuations and severe abnormal fluctuations in convertible bond transactions, to improve the operability of convertible bond business processing and the disclosure of relevant information. Targeted, effective, and supporting the revision of the necessary terms of the relevant risk disclosure documents to strengthen risk disclosure.

In order to give everyone the easiest understanding, I made a table. The other interpretations are not much different from the original interpretations, so I will not analyze them one by one:

For details, please refer to the original article: web link

So what is the biggest impact of the new regulations on us?

1. Because there is no temporary stop system, the possibility of leeks being quilted is low. How to understand this? For example, if a certain debt is pulled up to 30CM and temporarily stopped, leeks chase up and buy at 30CM. A large number of sales, only leeks will take over; but from now on, if there is no temporary stop, then the leeks will only chase 20CM. Once the grapefruit is sold in large quantities, the 20CM will not be able to be sealed, so it increases the difficulty of operating the grapefruit.

2. I can no longer see the increase of 30CM or higher on the non-first day. Goodbye to the super long-legged rivers and lakes, and I will never see you again.

3. In order to avoid supervision, in order to be sure to follow the trend of linkage between stocks and debts, at this time, the power of grapefruit is very tested. I estimate that there will be a kind of debt that will be sought after by grapefruit in the future, that is, double small and double low debt. What is double small debt? , one is the small market value of the underlying stock, especially the small current market value, preferably less than 5 billion; the other is small-cap bonds, small-cap bonds refer to convertible bonds with remaining scale or tradable scale of less than 500 million, preferably less than 3 100 million; what is the double low? First, the stock price of the underlying stock is low. I think it is lower than 10 yuan, preferably less than 5 yuan; the second is the low price of convertible bonds, which means less than 130 yuan, because the price is low, grapefruit The cost will be low, after all, it cannot be raised wirelessly at one time.

4. In the future, it is impossible for the demon debt to rise sharply in three trading days. I think it will increase the long-term volatility of the demon debt. How to understand this sentence is that the volatility of the demon debt in the future may be higher Large, the fluctuation within a day is likely to be the same as that of the sky and the floor.

5. The possibility of selling flying in the future will be reduced, and at the same time, there will be no possibility of a super harvest in one day.

6. Considering the increased difficulty and risk of hyping demon debt in the future, I estimate that many grapefruit will choose a demon debt for long-term speculation, and will not explode everywhere like now.

7. The official implementation of the new regulations, I think is the trump card of high-priced demon bonds, and it is estimated that some high-priced demon bonds will plunge on Monday.

The above notice was officially implemented on August 1, 2022. We can regard it as a new dynasty of demon debt and a new chapter in convertible debt. Everything is a new beginning.

P.S.: The Shanghai Stock Exchange has raised the transaction fee for convertible bonds from the original one million yuan (capped at 100 yuan) to one hundred and forty thousand (not capped). I estimate that most brokerages will choose to increase the original transaction fee. Come, it is a small negative for convertible bonds. It is estimated that the bonds of the Shanghai Stock Exchange will open lower on August 1.

Of course, I haven’t seen such a notice from the Shenzhen Stock Exchange. To be honest, from the recent point of view, the Shenzhen Stock Exchange seems to be more friendly.

The convertible bonds described in this article are all used for case studies and are not intended to be investment advice. Investments are risky, and you need to be cautious when entering the market. Please think independently.

Copyright belongs to the author. For commercial reprints, please contact the author for authorization, and friends who like it are welcome to forward and share.

The opinions mentioned in this article only represent personal opinions, and the subject matter involved is not recommended. Buy and sell according to this at your own risk.

I wish you a happy investment; $Sanhua Convertible Bonds (SZ127036)$ $Daotong Convertible Bonds (SH118013)$ $Superstar Convertible Bonds (SH113648)$ # Convertible Bond # # Convertible Bond Trading Rules # #雪 Globe Star Plan # @Today’s topic

There are 38 discussions on this topic in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/8849632795/226725652

This site is for inclusion only, and the copyright belongs to the original author.