Recently, I have studied the financial reports of Focus Media (SZ002027) in the past five years, and I have found some risk points to share with you.

1: Risks caused by the concentration of large customers

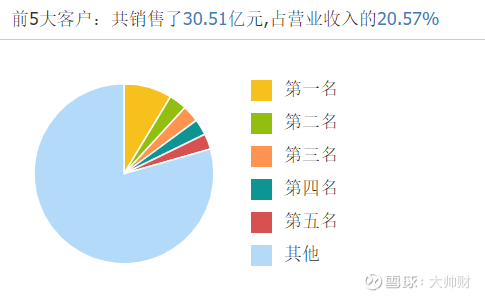

In the past three years, the proportion of the top five customers in Focus’s operating income has hovered around 20%. It cannot be said that this is not good, but we can think about it from another angle. If the top five customers join forces to reduce prices, how should enterprises respond, should they cut prices or not?

What happens if the top five customers churn? Will other scattered clients follow?

2: Risks caused by accounts receivable accounting for too high a proportion of total assets.

As can be seen from the above table, the amount of Focus Receivables is huge, basically more than 3 billion, and its proportion to total assets is also relatively high.

Take the first quarter report of 2021 as an example, the impact of the epidemic in the first quarter, the current credit impairment loss was 117.14 million, and the accounts receivable in the first quarter financial report was 2.382 billion yuan, accounting for 4.9% of the accounts receivable.

Although Focus has a strict credit impairment loss policy in its financial report, this risk is unavoidable. Assuming that the company’s accounts receivable are false, and a large number of impairment losses are accrued later, the consequences will be unimaginable.

In the accounts receivable subject, Focus has a greater risk, which needs to be focused on.

3: Earnings are unstable

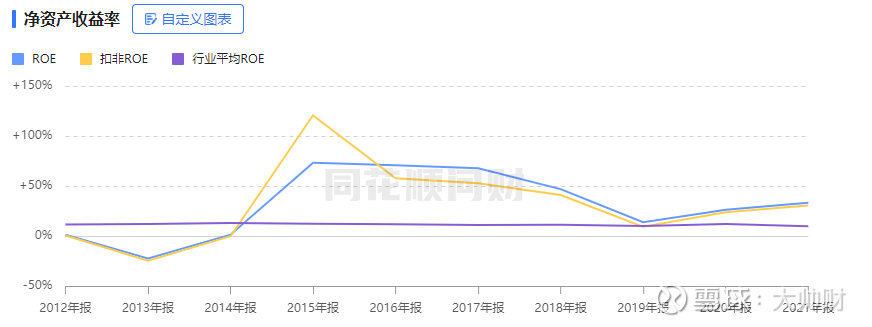

Focus’s ROE in 2019 was only 13.19%, which has fluctuated greatly in recent years. In fact, what the stock market needs is stable performance. Like Haitian and Maotai, their performance is basically predictable, while Focus’s performance is a bit like relying on the sky to eat. Higher, the economic downturn, operating income is lower.

Just like the vicious competition with Xinchao Media in 2019, the performance dropped sharply. In the 2022 epidemic, Focus’s performance fell by nearly 50% in the first half of the year.

The uncertainty of the future and the decline in profits in the past six months have led to a further decline in Focus’s share price.

4: The proportion of investment assets in total assets is increasing year by year, and the proportion is too high

The company’s expansion is divided into extensional expansion and endogenous expansion. In recent years, Focus has been increasing its external investment. It can be seen from the side that the company’s main business should encounter a development bottleneck. Take 2021 as an example, its investment Such assets account for 24% of the total assets, and the amount is as high as 6.1 billion. If a large number of impairment losses are accrued in the future, the consequences will be very serious.

This article is only used for communication and learning, not as investment advice.

This topic has 23 discussions in Snowball, click to view.

Snowball is an investor’s social network, and smart investors are here.

Click to download Snowball mobile client http://xueqiu.com/xz ]]>

This article is reproduced from: http://xueqiu.com/1662685772/227175068

This site is for inclusion only, and the copyright belongs to the original author.